Originally published: 20/06/2016 09:03

Publication number: ELQ-96236-1

View all versions & Certificate

Publication number: ELQ-96236-1

View all versions & Certificate

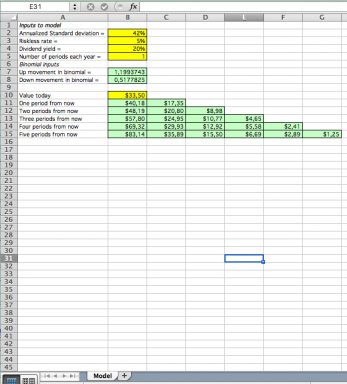

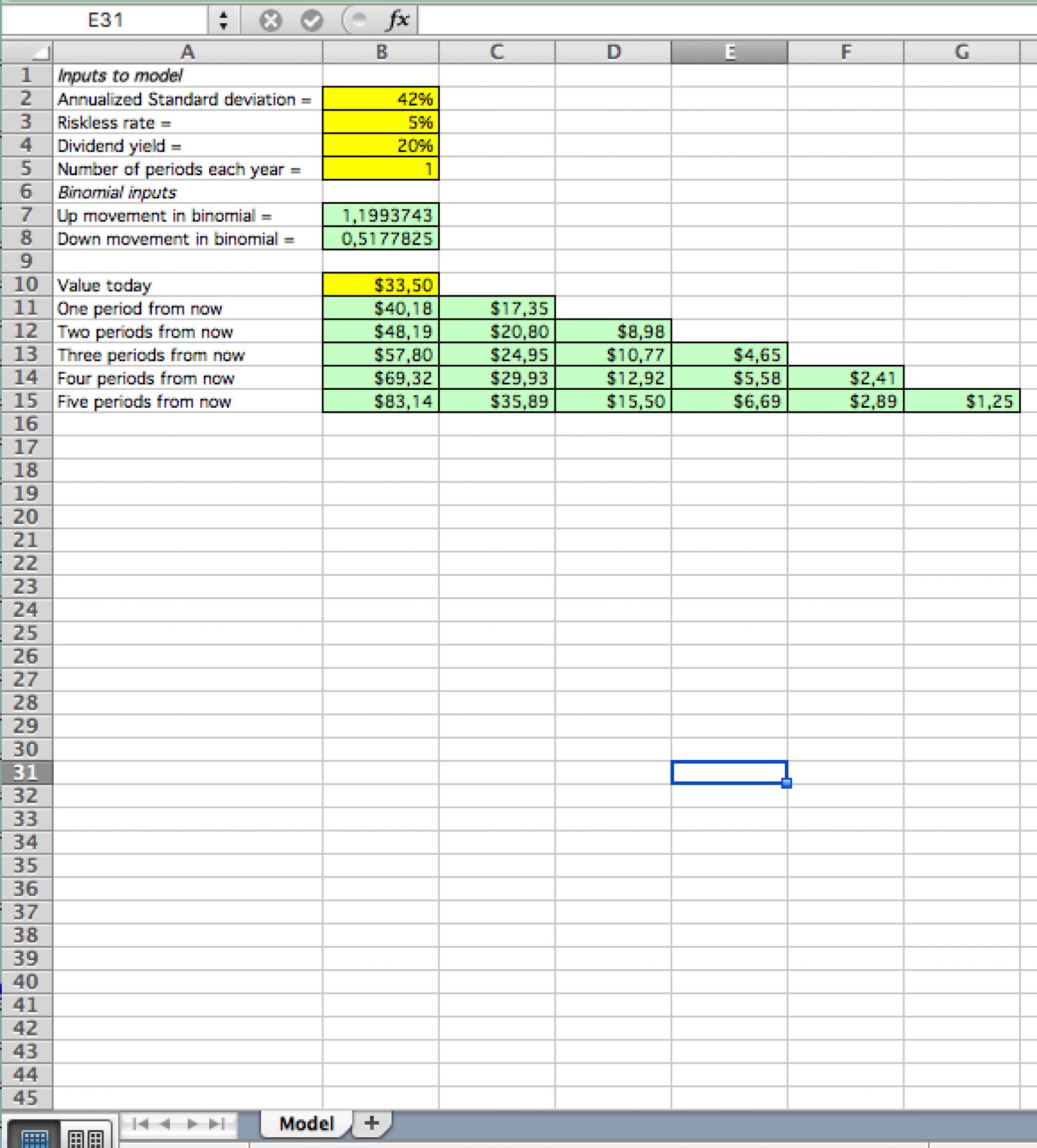

Black-Scholes converted for Binomial Tree

Converts the standard deviation input in the Black-Scholes model to up and down movements in the binomial tree.

Prof. Aswath Damodaran offers you this Best Practice for free!

download for free

Add to bookmarks

Further information

The objective of this model is to get the following outputs:

- Value of options one, two, three, four and five periods from now