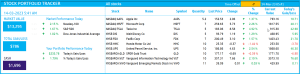

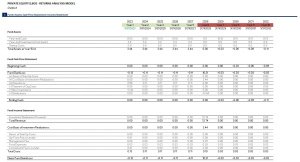

MARKOWITZ PORTFOLIO OPTIMIZATION USING MONTE CARLO SIMULATION

A stochastic simulation is performed based on the Monte Carlo method to obtain an optimal portfolio after evaluating thousands of possible combinations.

96Discussadd_shopping_cart

$15.00