Originally published: 18/05/2020 06:09

Last version published: 30/06/2021 09:43

Publication number: ELQ-46089-4

View all versions & Certificate

Last version published: 30/06/2021 09:43

Publication number: ELQ-46089-4

View all versions & Certificate

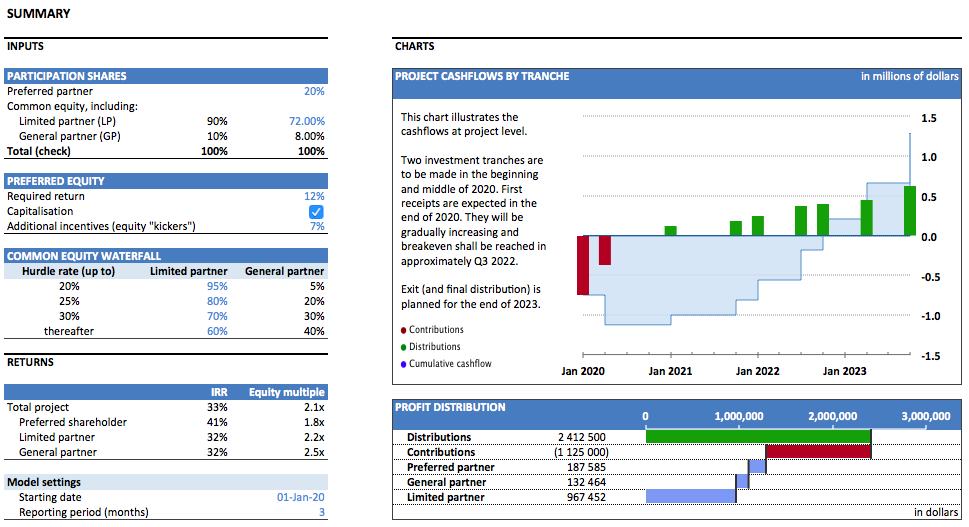

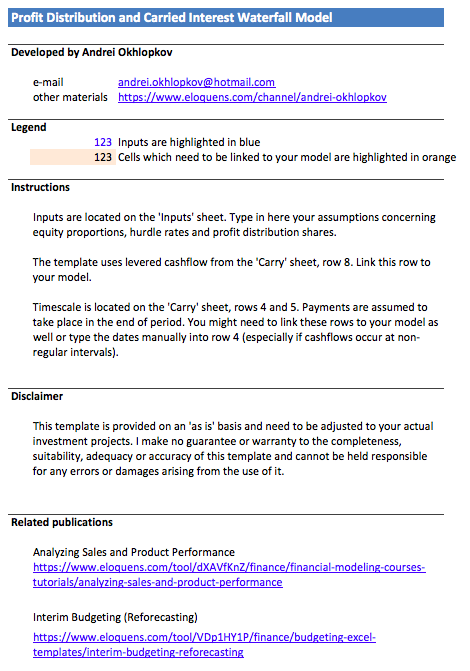

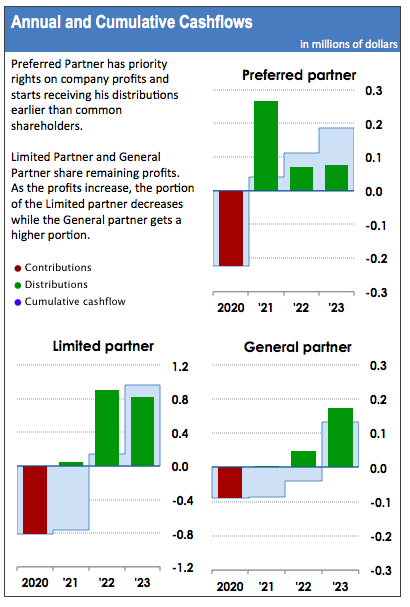

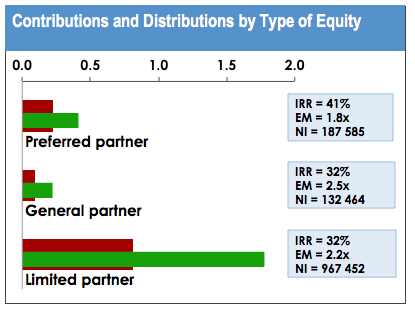

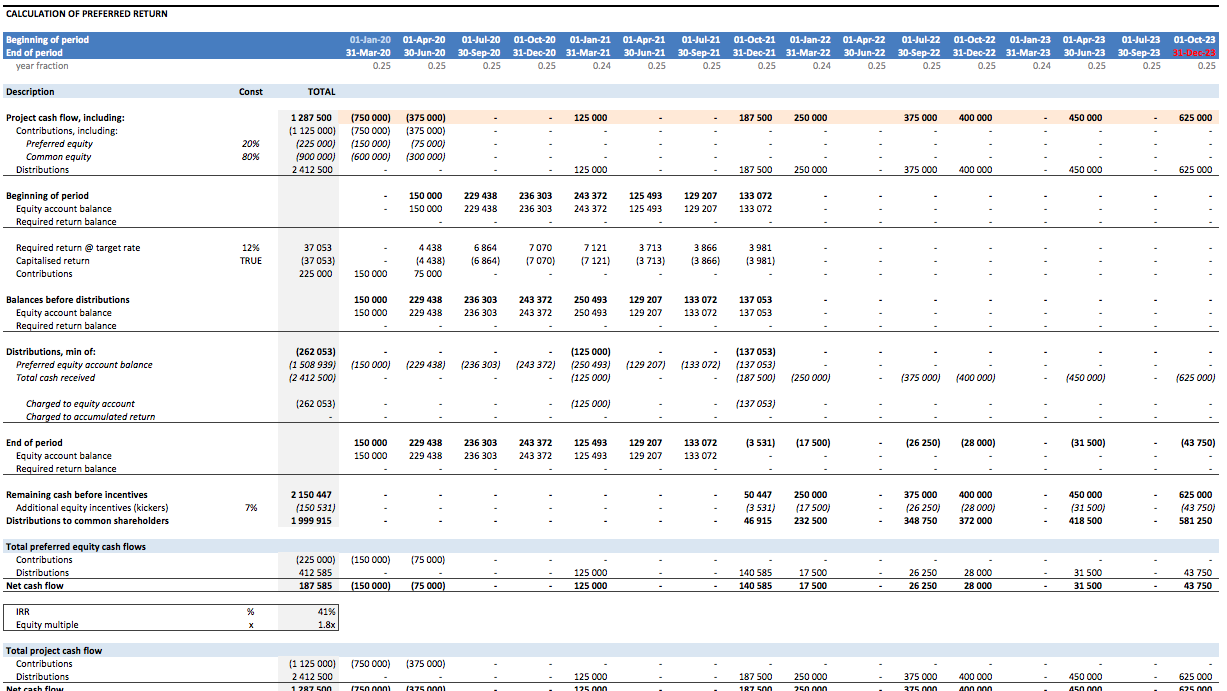

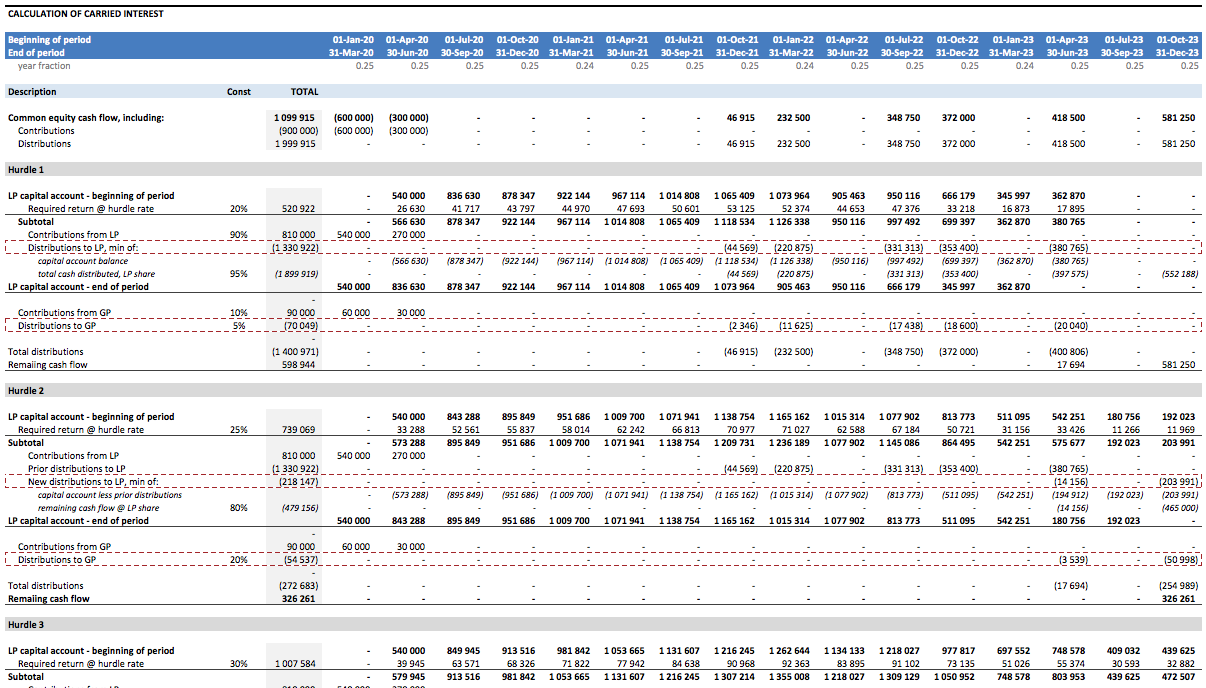

Profit Distribution and Carried Interest Waterfall

A template illustrating various setups of profit distribution between the JV partners with a carried interest waterfall

Further information

Calculate carried interest based on distribution waterfall

Joint ventures or partnerships with carried interest arrangements

n/a