Originally published: 09/11/2020 09:34

Last version published: 08/01/2024 08:56

Publication number: ELQ-89138-5

View all versions & Certificate

Last version published: 08/01/2024 08:56

Publication number: ELQ-89138-5

View all versions & Certificate

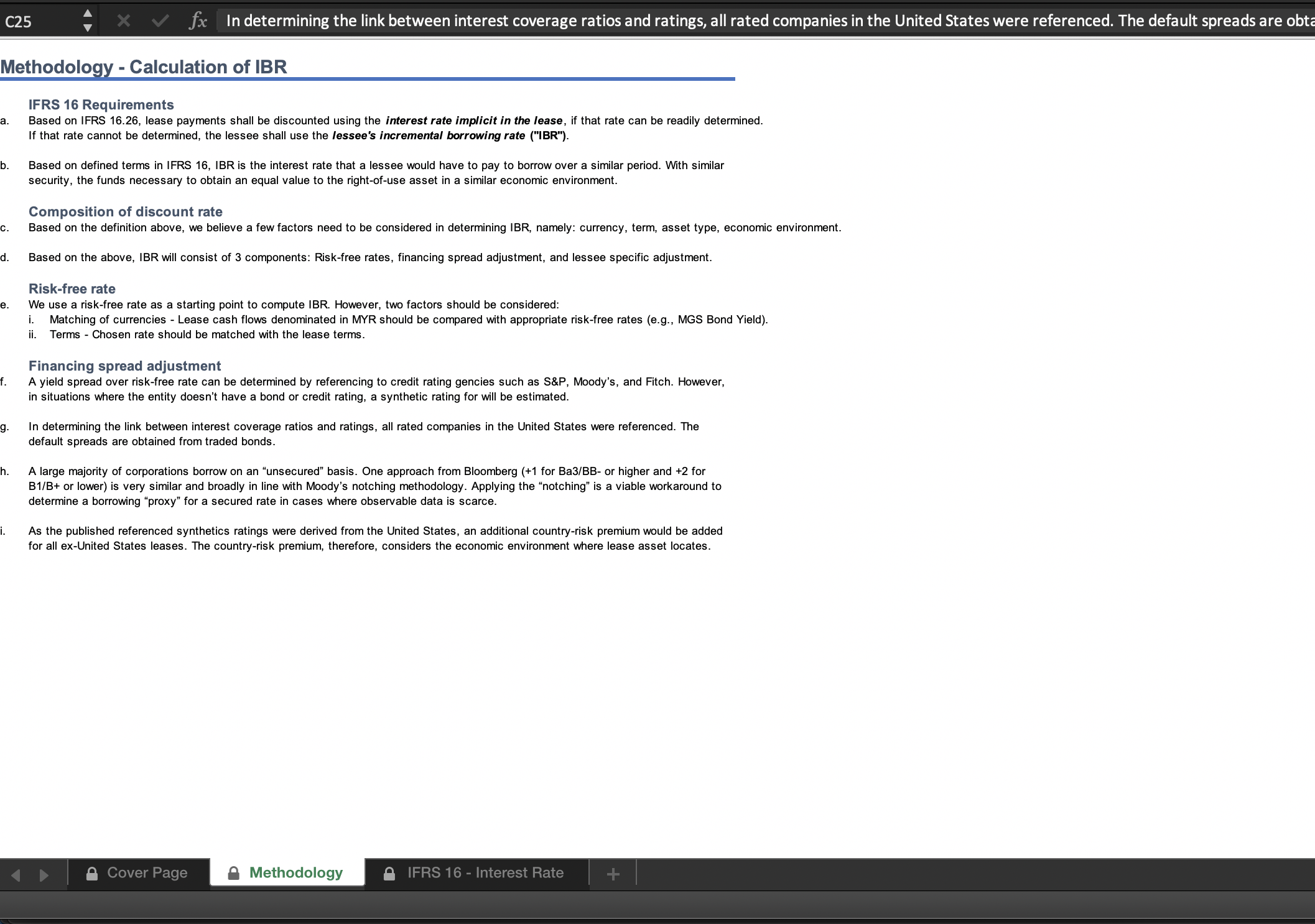

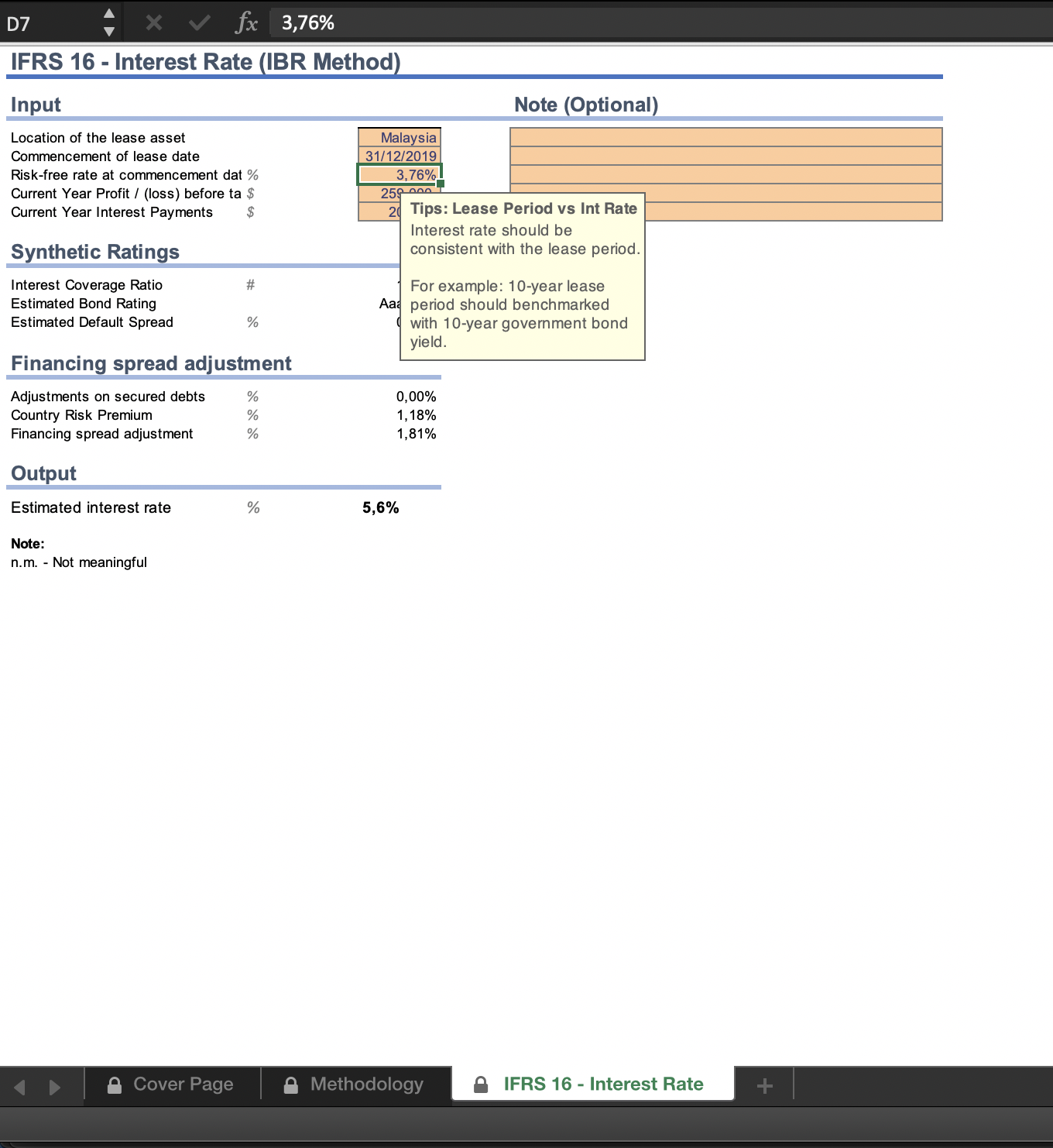

Estimating Interest Rate for Leases - IFRS 16 Requirement (2024 Edition)

This model estimates the leases interest rate.The data in the template is expected to be updated annually.

Business Valuation Expert | Advising Merger & Acquisitions | Working with Start-ups & Established BusinessesFollow 20