Originally published: 12/08/2022 15:52

Publication number: ELQ-20769-1

View all versions & Certificate

Publication number: ELQ-20769-1

View all versions & Certificate

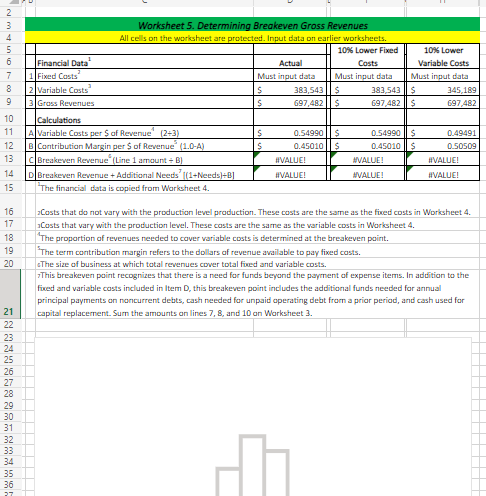

Breakeven and Performance Analysis

Breakeven and Performance Analysis

Our mission is to be a top professional services firm by adhering to our core values which is integrity, objectivity, professional competence, development and maintenance of technical expertise and coFollow