Originally published: 28/06/2020 20:40

Publication number: ELQ-89022-1

View all versions & Certificate

Publication number: ELQ-89022-1

View all versions & Certificate

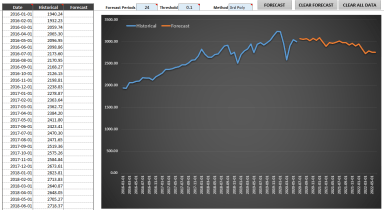

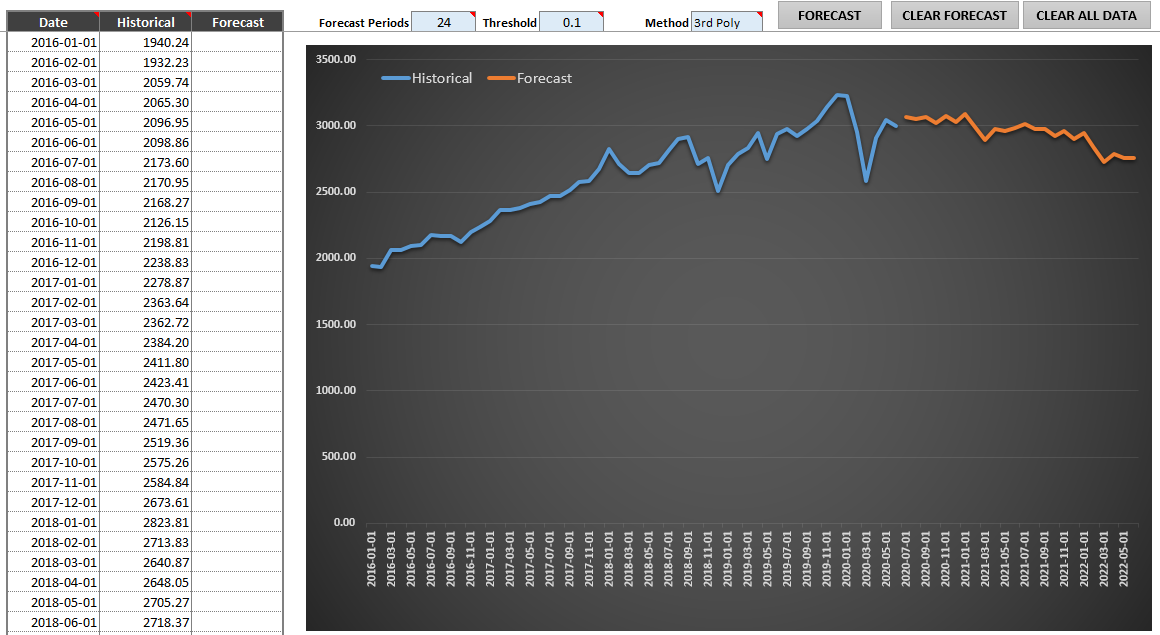

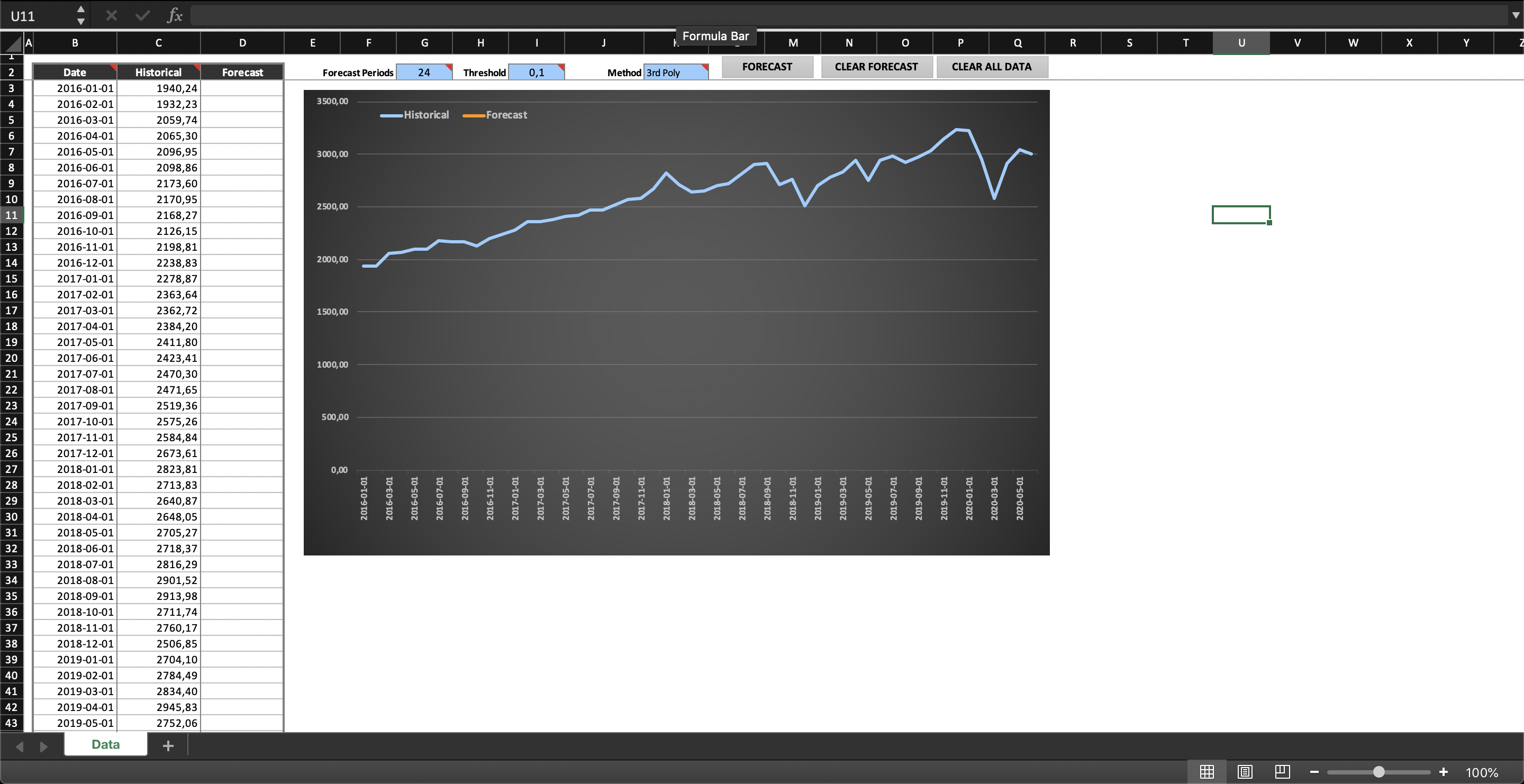

Seasonality Forecasting with Time Series Decomposition

Data forecasting with analysis of periodic variation in predicted data projections.

Purpose built Excel solutins for business and finanacial decision makingFollow 165

Business Spreadsheets offers you this Best Practice for free!

download for free

Add to bookmarks

Further information

Create forecasts with identified seasonality or risk variation within projections.

Financial data projections where repetitive variation such as seasonality is inherent.

Forecasting data where there is no discernible repetitive variation.