Originally published: 20/06/2018 15:49

Last version published: 17/09/2024 09:38

Publication number: ELQ-74300-6

View all versions & Certificate

Last version published: 17/09/2024 09:38

Publication number: ELQ-74300-6

View all versions & Certificate

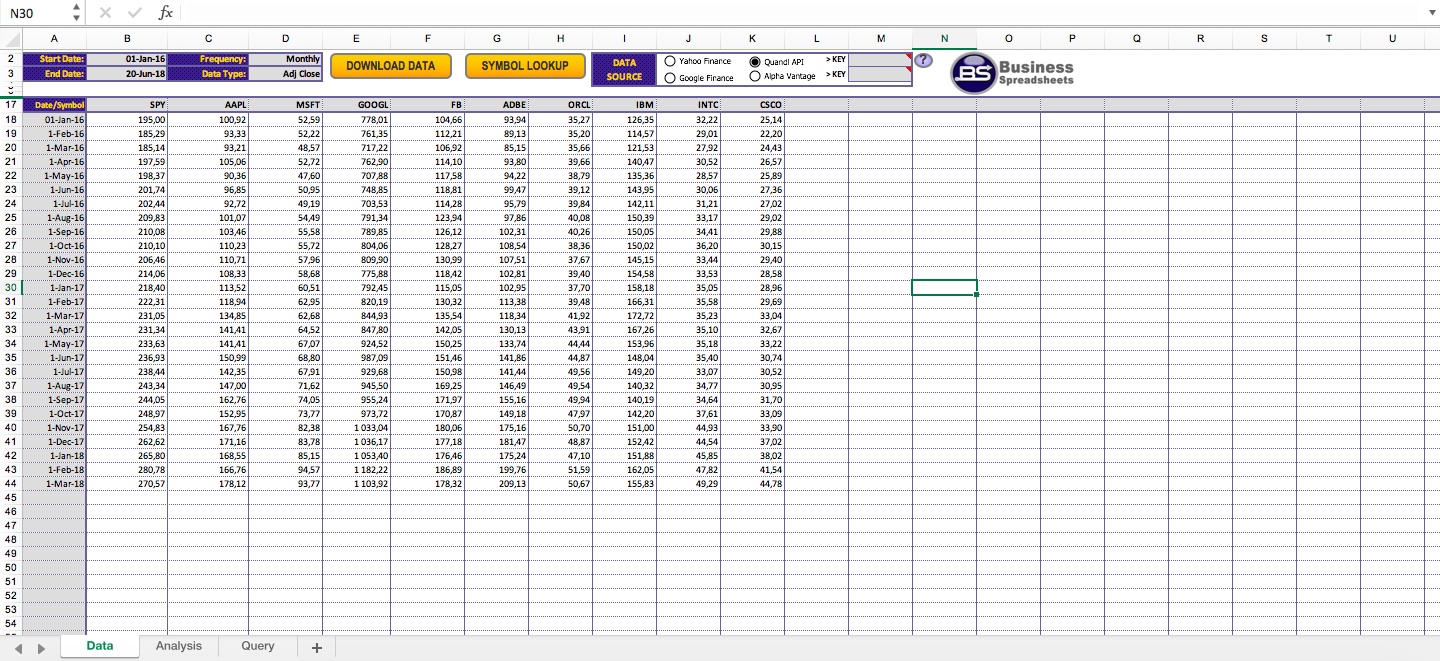

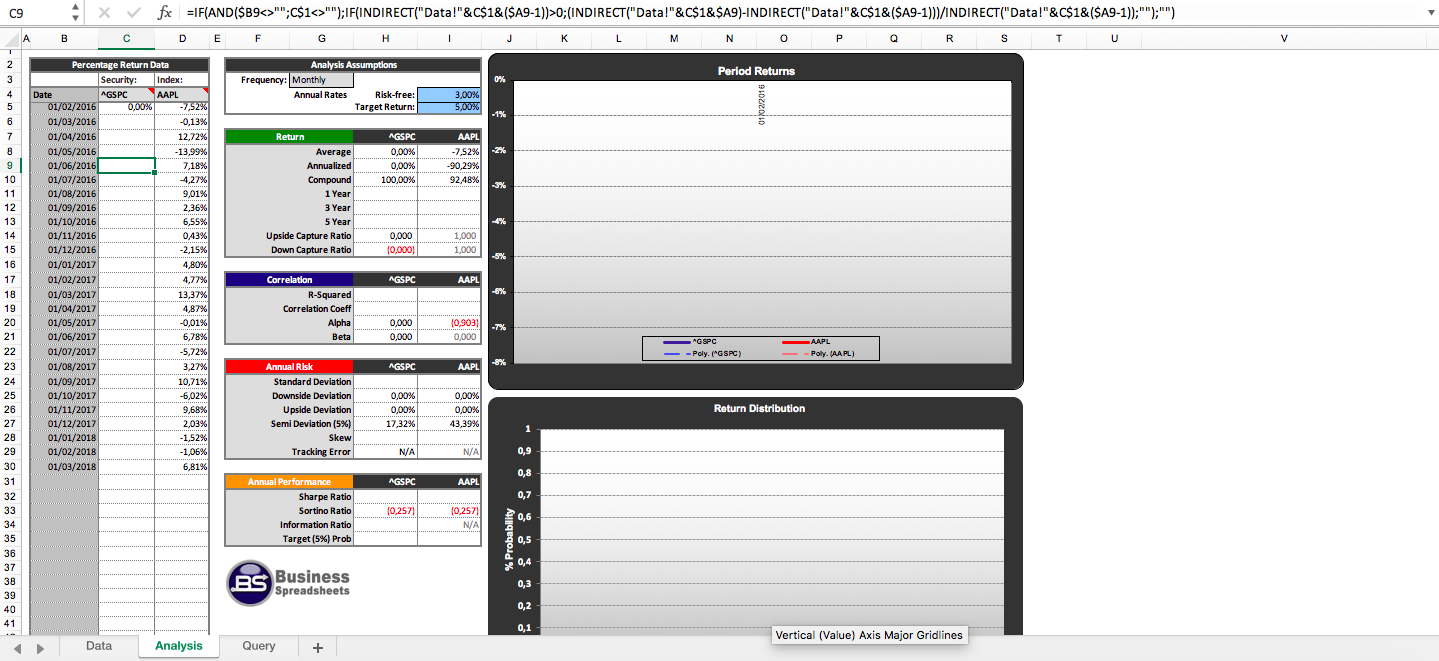

Portfolio Optimization for Asset Allocation and Rebalancing

The Excel portfolio optimization model combines asset allocation and technical analysis to maximize investment returns.

Purpose built Excel solutins for business and finanacial decision makingFollow 183

Further information

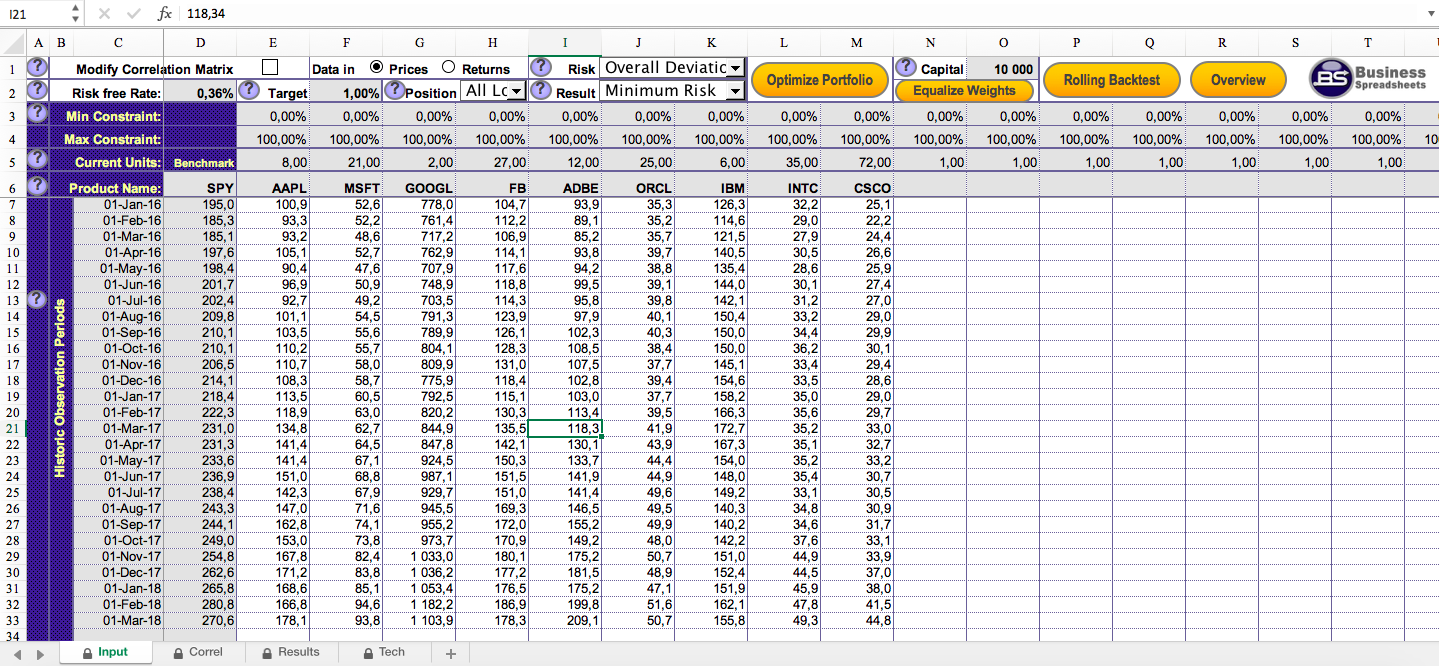

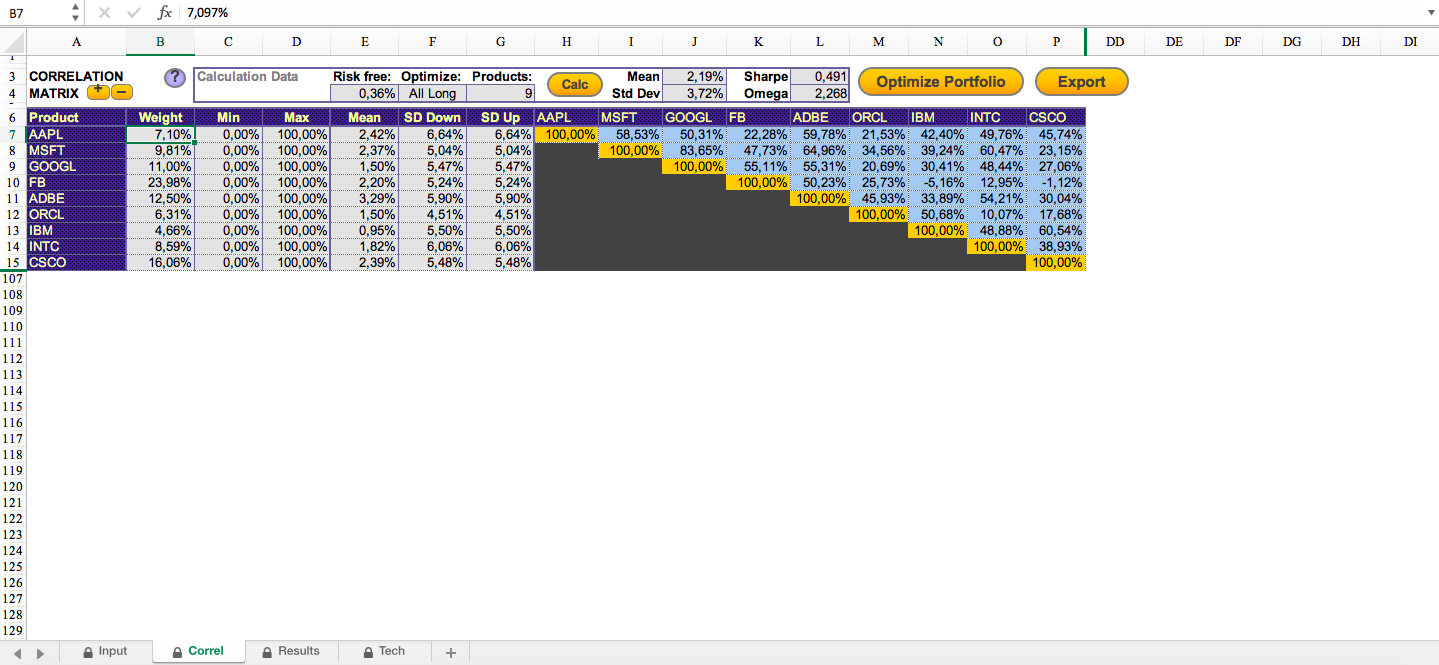

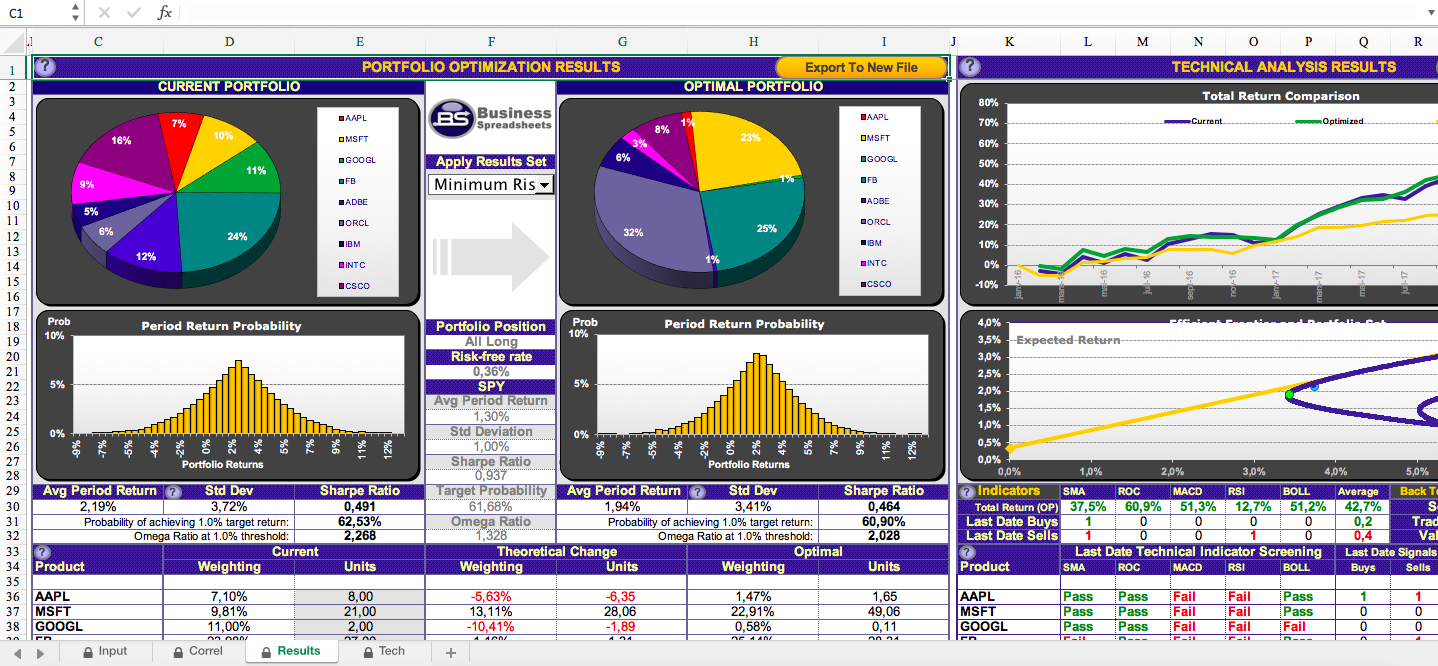

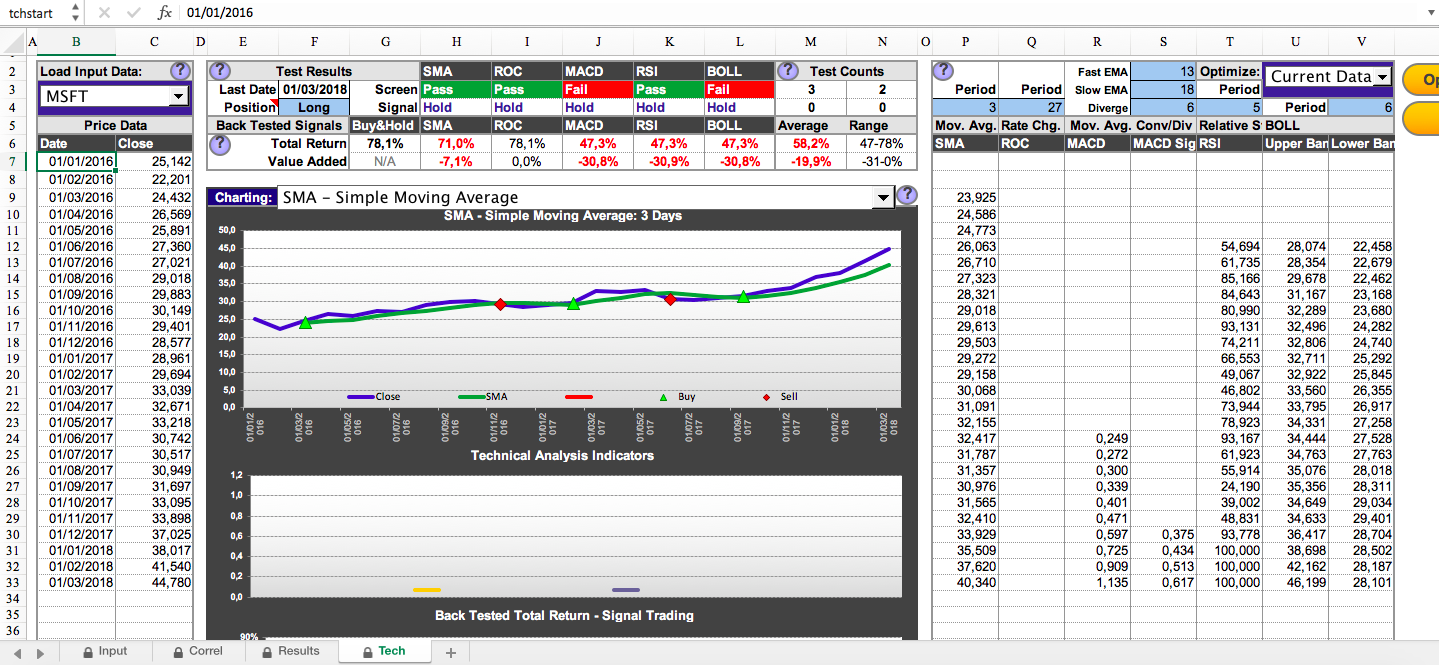

The Excel portfolio optimization model combines asset allocation and technical analysis constant optimization to maximize returns on financial investment portfolios. Portfolio rebalancing incorporates advanced options including risk assessment under Sharpe, Sortino and Omega ratios. Optimal trading strategies are established through back testing of optimized technical indicator constant parameters.

Optimizing portfolios of investments or assets where time series data is available

Portfolios where periodic investment prices or returns are not available.