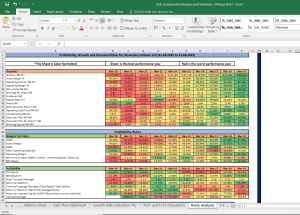

Multiple Equity Stocks Trading FIFO Gain Google Sheet Calculator

Very handy Google Sheet Calculator to calculate trading profits for multiple stocks in single sheet using FIFO method.

3,5879add_shopping_cart

$39.00

All businesses have an intrinsic value, and this value is based on the extent of free cash flow they have available during their lifetime. Money generated in the future is worth less than it is in present time, therefore projected free cash flows have to be discounted at a rate that is deemed appropriate.

Most Stock Valuation methods work on the theory that a business’ value is equal to the total financial worth of all future free cash flows put together. Due to the time value of money, these future cash flows must be discounted accordingly. If the future cash flows of a business are already known, and there is a target rate of return on your money, then you have the tools to work out the exact amount of money you should pay for the business.

However, in practice, Stock Valuation is not so simple. This is because one can only estimate the value of future free cash flows. The inputs are also estimates themselves and need the appropriate skills and experiences to predict them as accurately as possible.

In order to reduce the difficulties and be more accurate, conservative estimates should be used and a margin of safety should be provided.

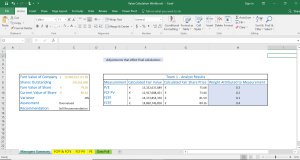

The Discounted Cash Flow analysis method treats the business as a large free cash flow machine. One would value the whole business for all of its worth and hold it for all of its projected free cash flows indefinitely. When we value a company’s worth, we look at its current market capitalisation compared to the company itself in order to determine whether it is profitable and worthy. An alternative method would be to divide the total estimated value by the number of shares, then compare this to the current real price of shares.

The Dividend Discount Model treats individual shares as one small cash flow machine. The free cash flow is the dividends, as that is the money investors receive. A business could spend their free cash flows on repurchasing shares, dividends, acquisitions, or even not spend it at all and let it build up on the balance sheet. In reality however, management decides what to do with it. The dividend takes all of this into account, as the present dividend along with the predicted growth of said dividend takes all free cash flows of the business into account and how management decides to use them.

The Earnings Multiple Approach is one that can be used if a company pays a dividend or not. The financier predicts future earnings over a time period (for example 10 years), and puts a hypothetical earnings multiple onto the final predicted EPS value. Cumulative dividends are then taken into account and the difference in the stock price at present, and the total hypothetical value at the end of the time period, are distinguished to calculate the expected rate of return.