Capital Budgeting Excel Model Template

User-friendly Excel model to calculate and compare capital budgeting metricsm across (up to 3) proposed investments

4,3502add_shopping_cart

free

Capital budgeting is the process in which a business or organization plans out its potential future expenses or investments. This can include, amongst other things, the purchasing of new machinery or allocation of funds to research development projects.

The budgeting of major capital is an important strategic procedure that requires detailed analysis of the merits and weak points of any given future investment, idea, or plan. It is vital that the management of a company correctly determines which investments will be able to generate the highest yield, and also take into consideration the level of risk required, over the period planned, in order to effectively set long-term growth goals.

Through the Capital Budgeting, the transfer of information for projects to the required decision-makers is facilitated. It also allows for the overseeing and control of expenditure, which can help make projects more efficient in the long run. Thus, capital budgeting involves both financial decision-making and strategic / investment decision-making.

There are various ways to approach the process of capital budgeting in order to allocate future funds in the most successful way.

Mutually exclusive projects: This is a project that if accepted, all other projects will be ruled out by a firm. The projects considered may be mutually exclusive and thus only the best proposed will be pursued by decision-makers.

Capital rationing: This approach takes more account of a business's budget when making decisions regarding capital. It places constraints on the quantity of new projects or investments planned. Its objective being to prevent over-committal of investment and projects.

Acceptance rule: This is a type of budgeting decision made by creating a minimal acceptable return for a project. If the proposal displays a return below the threshold, it will not be taken. This decision-making approach normally involves the Net Present Value method.

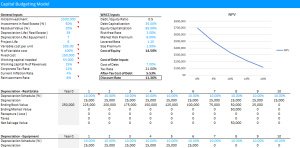

Net Present Value (NPV) method: This is a popular method when taking future investment decisions. It involves discounted cash flows which consider the risk and time variables at stake. If there is a positive NPV, the project will be profitable, whereas the inverse will result in net loss.

Payback Period Method: Simply put, this technique works out the timeframe in which a project takes to recover its initial investment funds.

Accounting Rate of Return (ARR) method: This method measures the rate of return / profit estimated on a project. It is calculates this return by taking into account the net income of the proposed capital investment.

Internal Rate of Return (IRR) method: This is a discount rate that makes the NPV of cash flows for a project equal zero. This method is popular when comparing the profitability of carrying on, or improving existing projects with the planning and implementation of a new project.

Capital Budgeting: Techniques and Importance