Break Even Analysis / Cost Volume Profit Analysis Excel Model

A full Break-even analysis Excel Model to analyse when your product/service reaches profitability.

4,914Discussadd_shopping_cart

$59.00

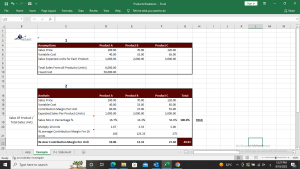

A break-even analysis is a type of analysis that is used to calculate the amount of revenue needed to be generated in order to cover all costs.

This type of analysis is typically used in banking, accounting, and business.

A break-even analysis is carried out by firstly splitting the costs into the variable and fixed categories. (Variable costs are those which fluctuate as the production levels change. Fixed costs are those which are not affected by the level of production.)

These costs are then compared against the sales revenue in order to determine the break-even point for a company.

A typical break-even analysis formula may look like this:

Break even quantity = Fixed costs / (Sales price per unit – Variable cost per unit)

As previously mentioned, fixed costs are those which are not affected by the different levels of production or output that a company generates. Examples of which can include rent of company premises, depreciation, Research and Development (R&D), Marketing expenses, and Administrative costs.

Varying with change in the production levels, a variable cost can include things such as raw materials, direct labour, gas, and other expenses i.e. commission.

There are two main types of variable cost, direct and indirect. Direct variable costs refer to those which are directly affected by production changes, including the cost of raw materials being used and the expenses for the amount of labour that has been required. Indirect variable costs are those which cannot be easily attributed to changes in production and output of a company. This type of cost may include depreciation of items, i.e. a machine’s value will depreciate more quickly if it is used more extensively.

There are also Semi-variable costs, which are costs that are generally fixed, but may be subject to change when there are major output changes for the business.

A break-even analysis can be useful for those running startups in order to understand the point when the business can start being profitable. This also allows analysis on the viability of a business proposition, and also the level of risk involved.

It is also advantageous for those wanting a quick and easy way of estimating the profitability of a business.

A break-even analysis does not consider the fluctuations in sales, or the fact that fixed costs will change over time. Similarly, variable costs may change in different ways over time. This type of analysis should thus be seen as a something to help during planning, rather than carry weight in the decision-making process.

The break-even point can be influenced by a range of things, including market demand, the costs of starting up a business, variable and fixed costs, and pricing strategies.

To find out more about break-even analysis, please visit the following pages:

An introduction to the break-even analysis