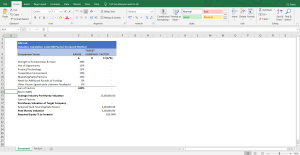

Public SaaS / Software Company Operating & Valuation Model Template

Comprehensive Public Company SaaS Operating & Valuation Model

5,3821add_shopping_cart

free

For any company, business valuation is never going to be a simple task. For startups that have uncertain futures, and little to no profits or revenues, valuating the company is especially difficult. For businesses that are publicly listed and more mature, valuation entails valuing them based on industry-specific multiples or as a multiple of their earnings before interest, taxes, depreciation, and amortization. For a venture that could be years away from sales, it’s much harder to value.

If you are aiming to raise capital for your startup, or you’re considering investing in one, you should firstly evaluate the company’s worth.

VC Investors tend to like this approach. This is because it provides a pretty solid indication of what the market could potentially pay for a company. In a nutshell, the market multiple method values the firm against recent acquisitions of companies in the market that are similar.

For example, if software firms for mobile apps are selling for five-times sales, then you could use a five-times multiple as a base for valuing your own mobile apps business because you know what real-life investors are willing to invest for mobile software. You can adjust the multiple down or up to take different characteristics into account. For example, if your company is in earlier stages of development than the comparison company, you could use a multiple that is lower than five as investors would be investing in a higher-risk company. To value a company at extremely early stages, you must determine extensive forecasts to calculate what the earnings or sales of the business will be when it is mature. Capital providers commonly fund businesses when they have a belief in the firm’s business model and product, even before it generates earnings. Whilst many established companies are valued based on their earnings, a startups value must often be determined by revenue multiples.

This approach arguably comes the closest to what investors are likely to pay. However, it is very hard to find comparable market transactions. It can be a very hard task to find businesses that are close comparisons, particularly in the startup market. Early-stage, unlisted companies tend to keep deal terms under wraps- the ones that are likely to represent the best comparisons.

For the majority of startups, particularly those who haven’t yet started generating earnings- most of the value relies on future potential. DCF Analysis represents a substantial valuation approach. DCF entails forecasting the amount of cash flow that the company is going to produce in the future, and then working out how much that cash flow is worth using an expected rate of investment return. For startups, a higher discount rate is applied, due to the high risk that the company will not generate cash flows that are sustainable.

The issue with DCF is that the DCF quality depends on the ability of the analyst to make good assumptions regarding long term growth rates and forecast future market conditions. In a lot of cases, projecting earnings and sales past a few years into the future ends up being a guessing game. As well as this, the value generated by DCF models is extremely sensitive to the expected rate of return used for discounting cash flows. Therefore, DCF must be used with a lot of care. The DCF is sometimes tricky to apply to valuations in real-life.

Cost-to-duplicate entails calculating how much money it would cost to build the same company over again from scratch. The point of this is that an experienced investor would not invest more than it would cost to duplicate the business. This method will usually examine the company’s physical assets to work out their fair market value.

E.g. for a software business, the cost-to-duplicate may be calculated as the total cost of the time it has taken to program and design the software. For a high-tech startup, the costs could be what the company has paid for R&D, prototype development, and patent protection. The cost-to-duplicate method is usually considered as a starting point for startup valuation, due to it being fairly objective. It is based on historic expense, verifiable records.

The issue with this approach is that the future potential of the company is not considered. It does not reflect on the company’s potential to generate profits, sales, and ROI.As well as this, the cost-to-duplicate method doesn’t take into consideration intangible assets such as brand value, that the venture may have even in its early development stages. Due to the fact it generally underestimates the value of the startup, it is commonly used as a ‘lowball’ company value estimate. The venture’s equipment and physical infrastructure may only be a small factor of the actual net worth when intellectual capital and relationships form the backbone of a company.

Lastly, there is the development stage valuation method, commonly used by VC firms and angel investors to come up with a rough range of company value quickly. Rule of thumb values are generally set by the investors, and depend on the commercial development stage of the venture. The further along the business is on the development pathway, the higher the company’s value and the lower the risk.

There will be various value ranges depending on the business and the investor. But generally, startups that have only a business plan will probably receive the lowest valuations from all investors. Investors will assign a higher value once the company successfully reaches development milestones.

A lot of private equity firms will additionally fund a company when it meets a certain milestone. E.g. the initial financing round could be geared towards paying employees to develop a product. When it is proven that the product is successful, another round of funding is provided to produce the invention in mass and market it.

In summary, for a company still in infancy stages, it is very hard to determine an accurate value due to the uncertainty of success or failure. Many say that startup valuation is actually less of a science than an art. However, the above approaches help to approach startup valuation more scientifically.

If you’d like to read more about Startup Valuation, please visit: