Originally published: 13/10/2020 07:06

Last version published: 07/02/2024 09:52

Publication number: ELQ-12749-2

View all versions & Certificate

Last version published: 07/02/2024 09:52

Publication number: ELQ-12749-2

View all versions & Certificate

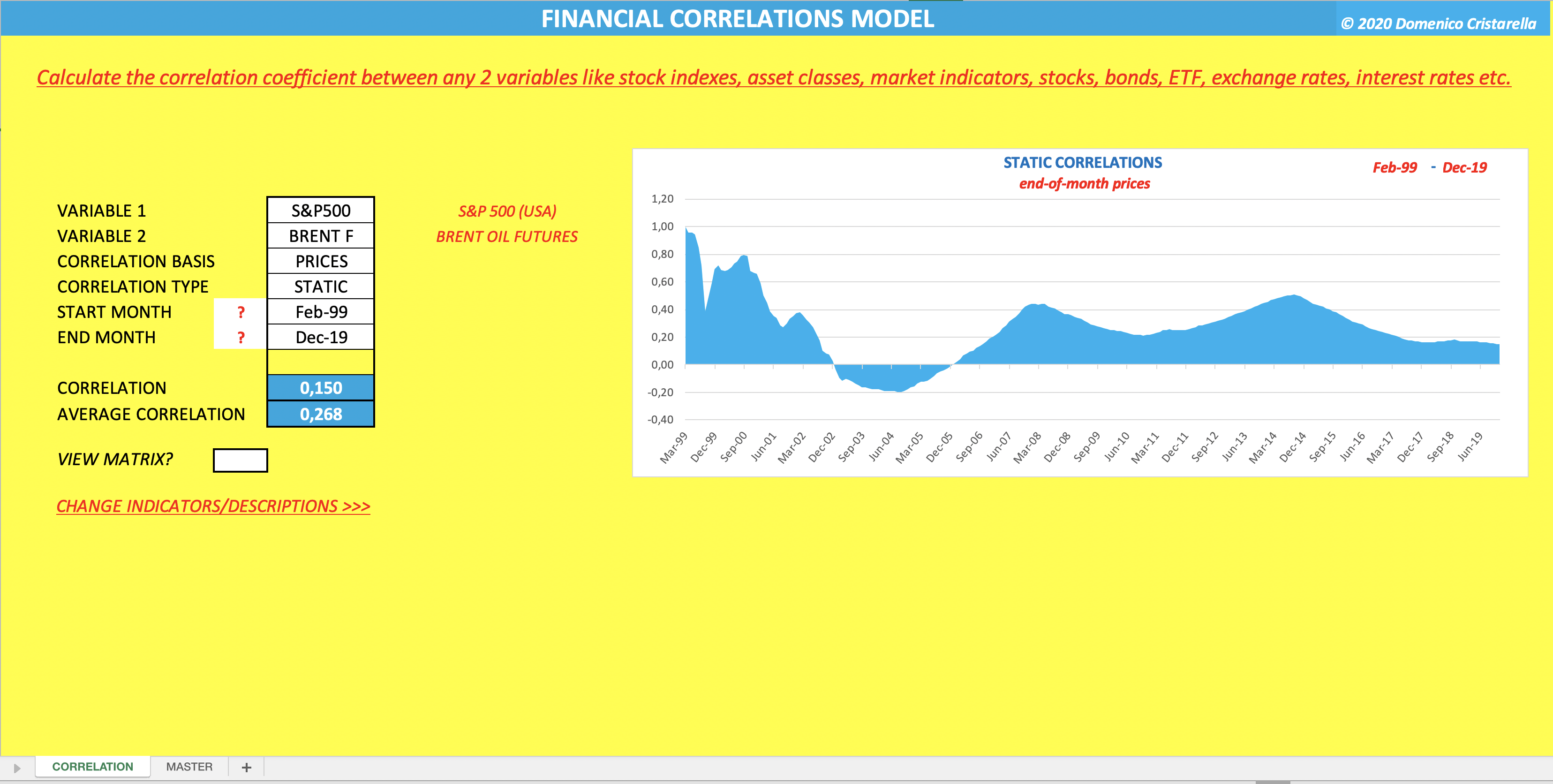

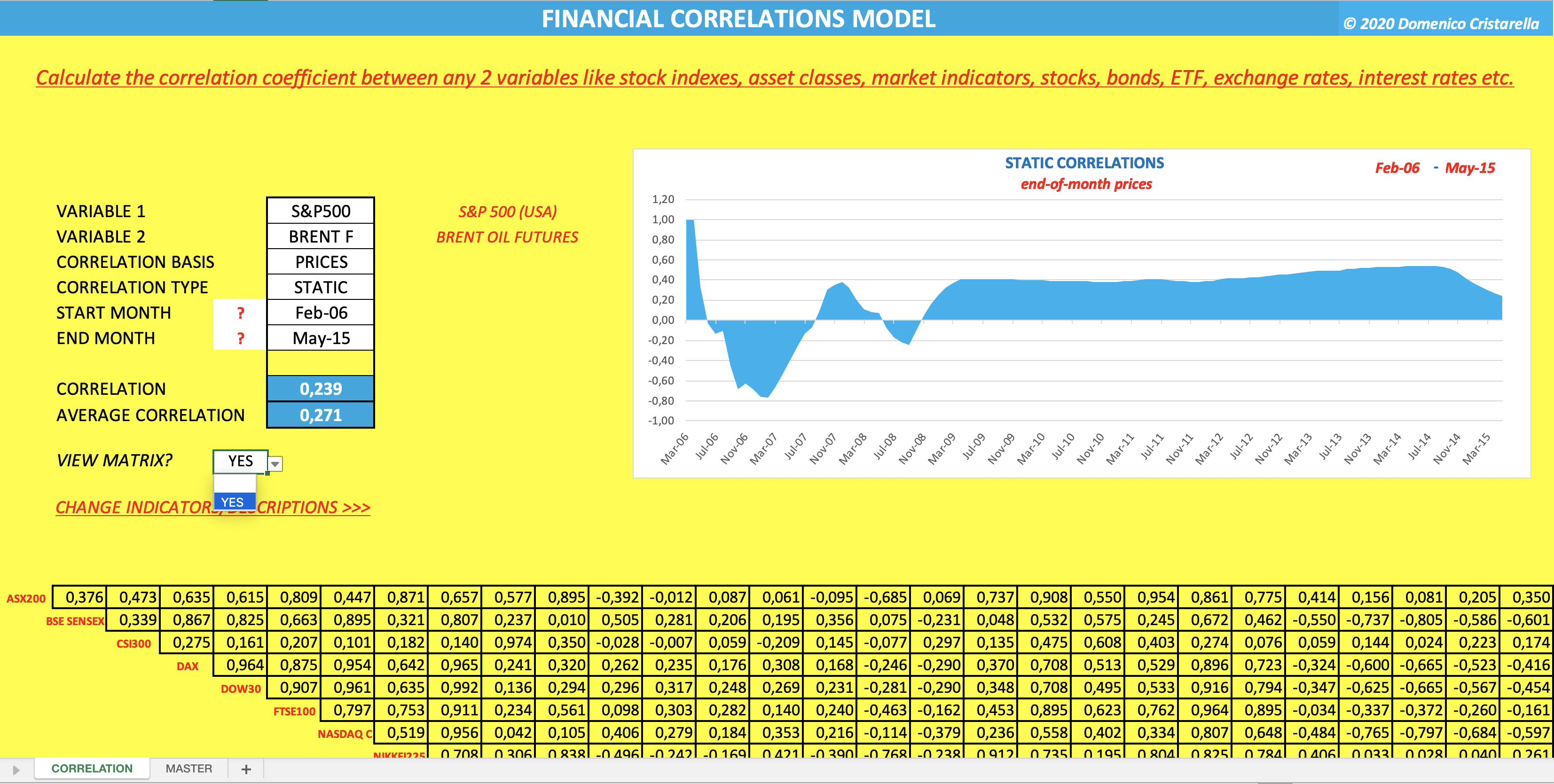

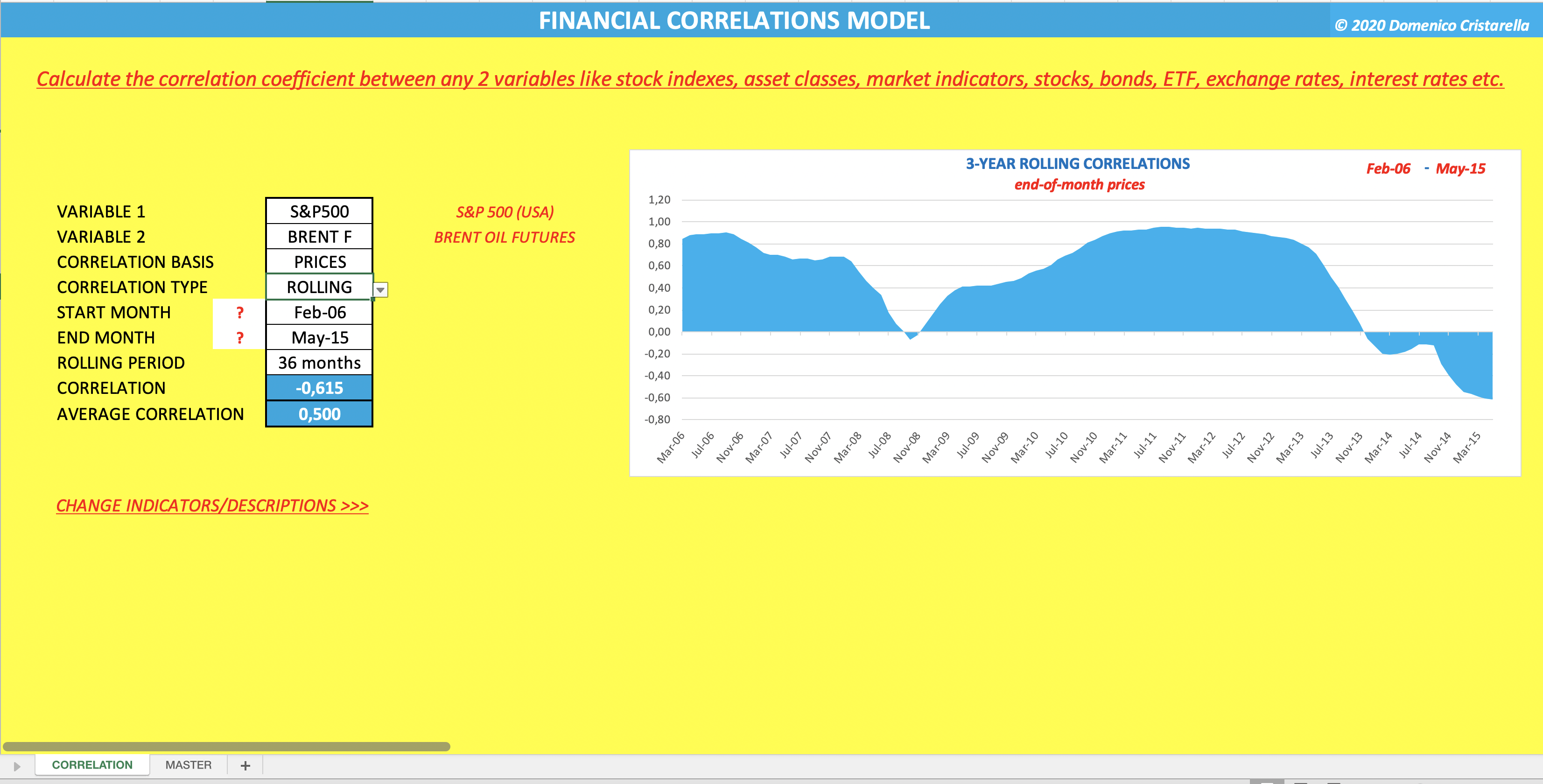

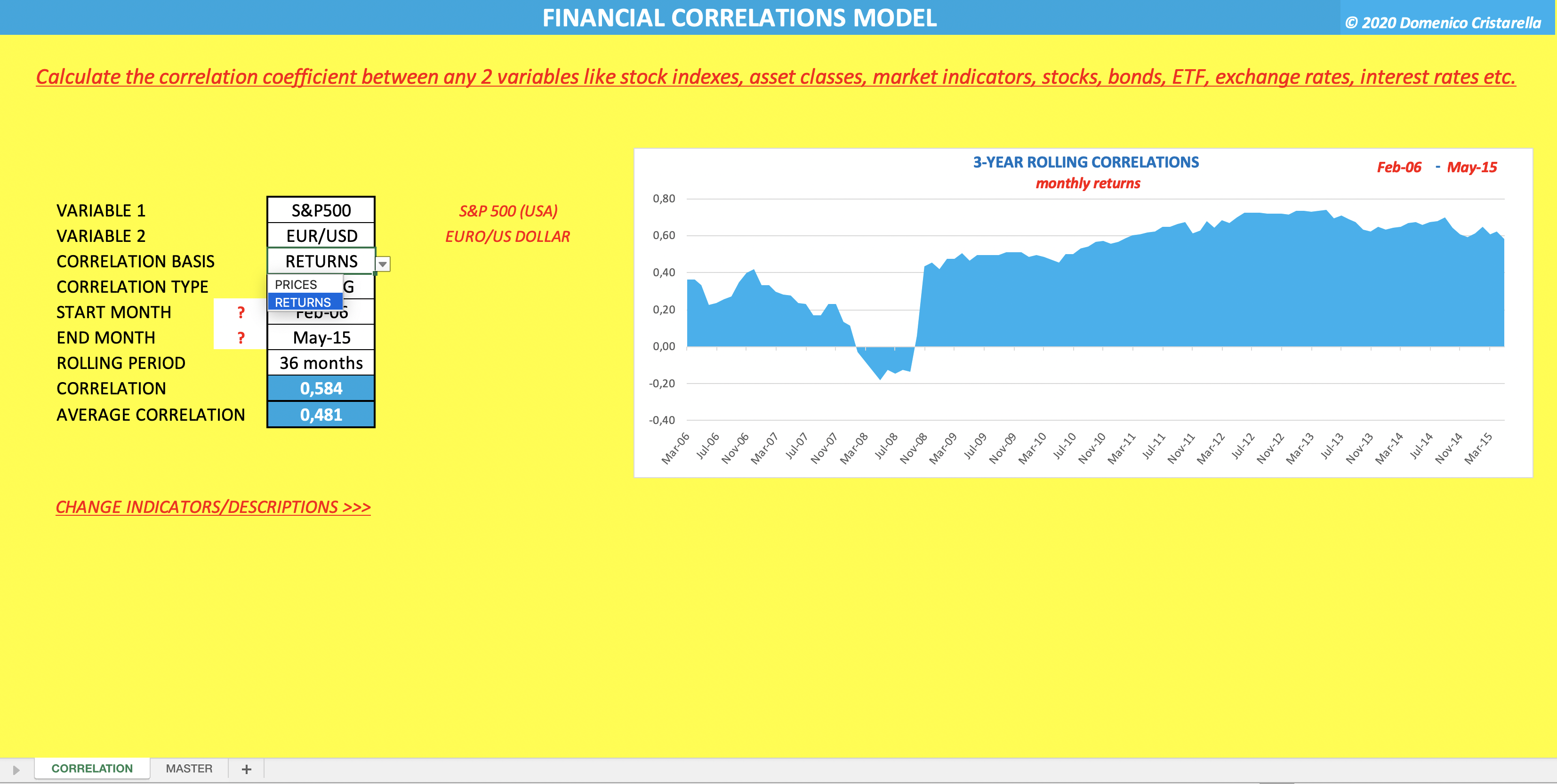

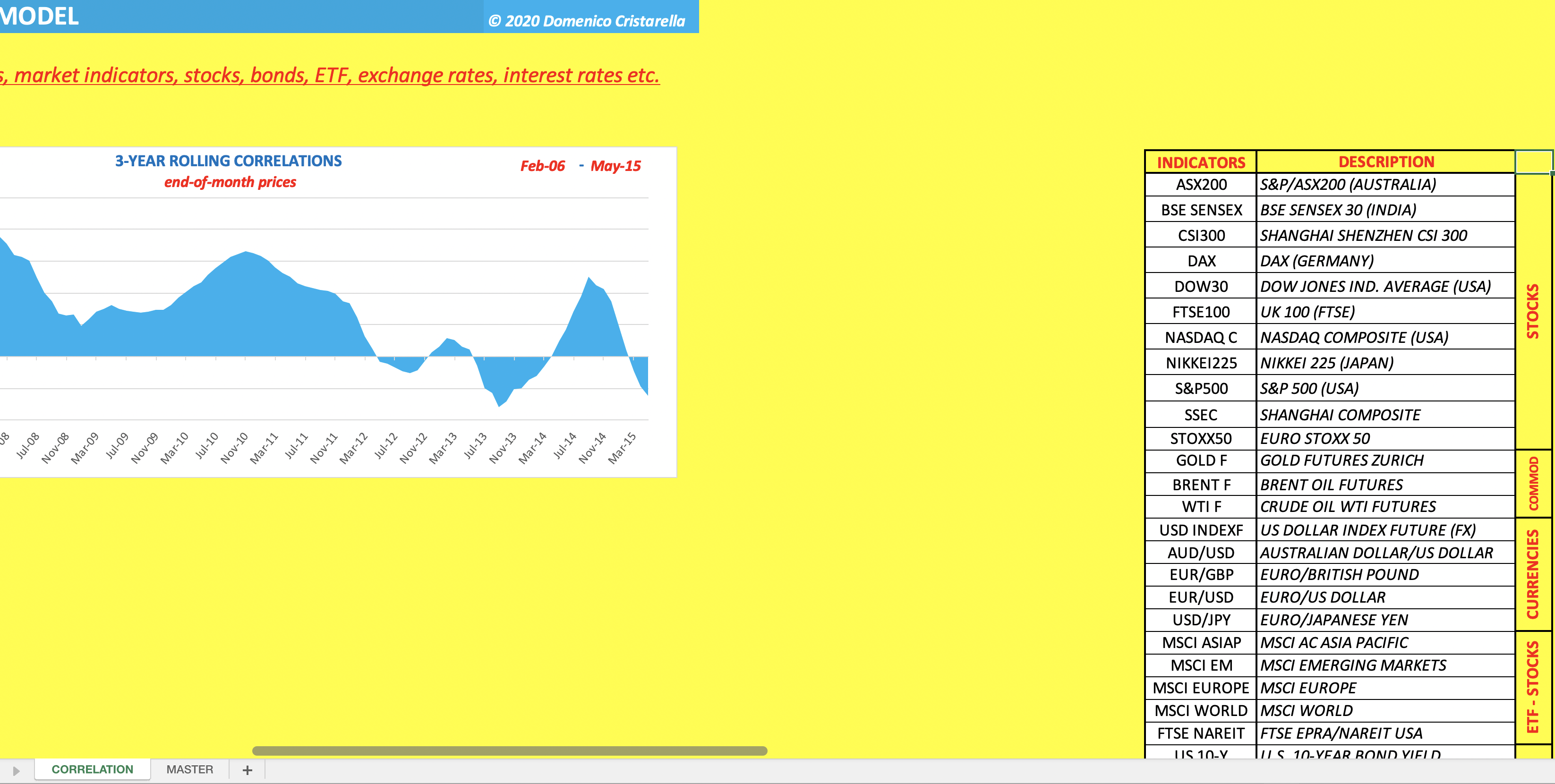

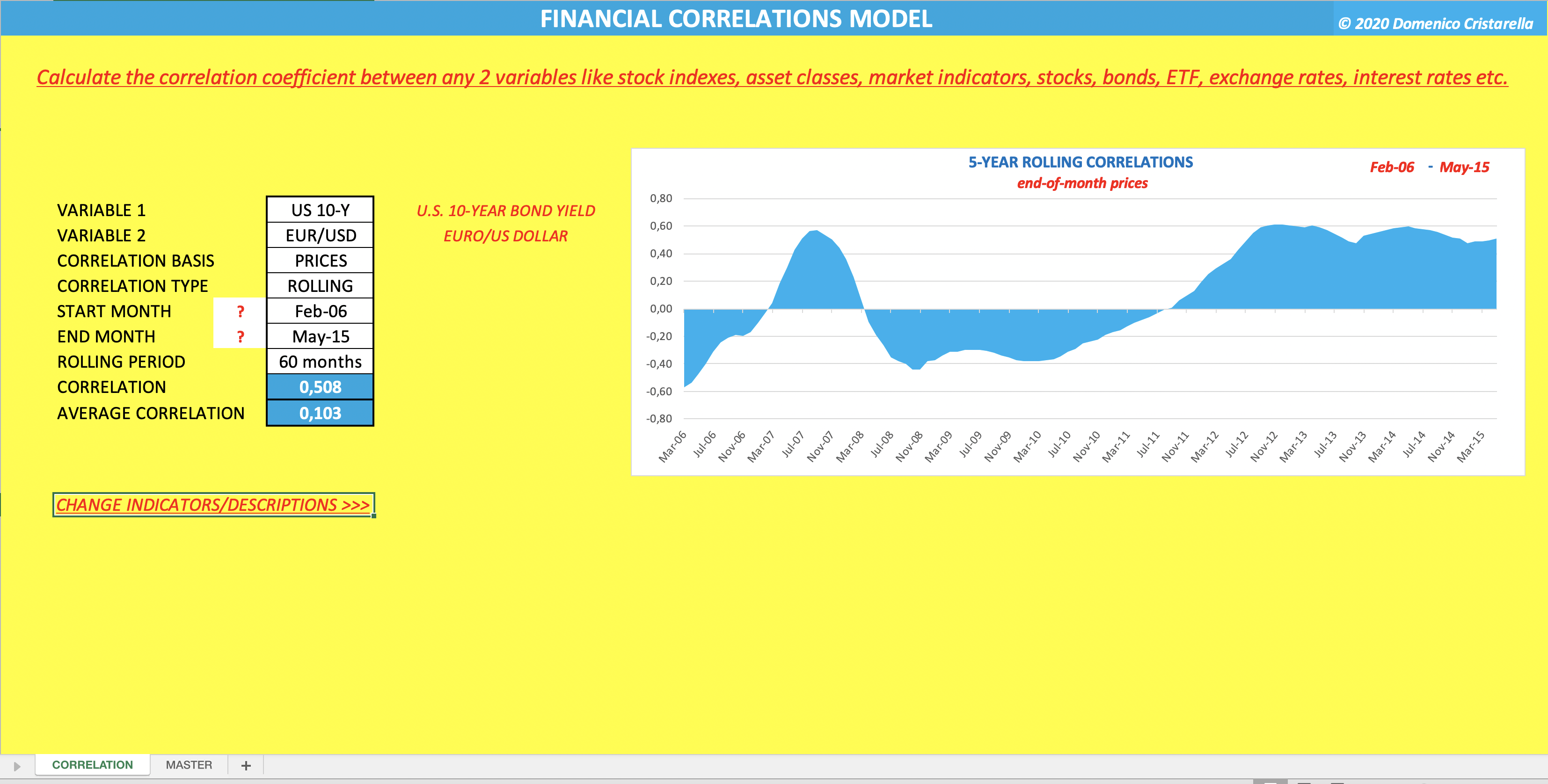

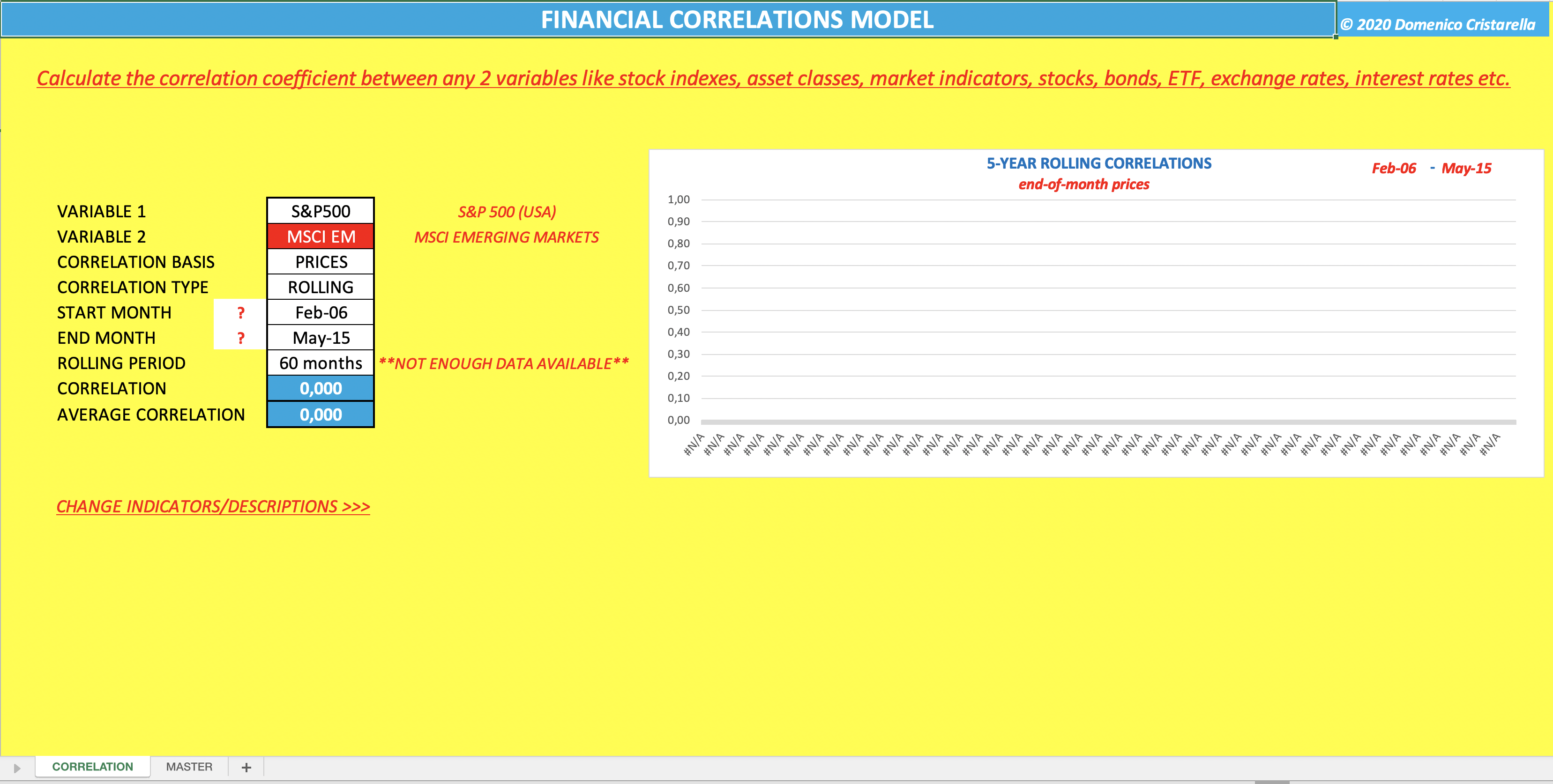

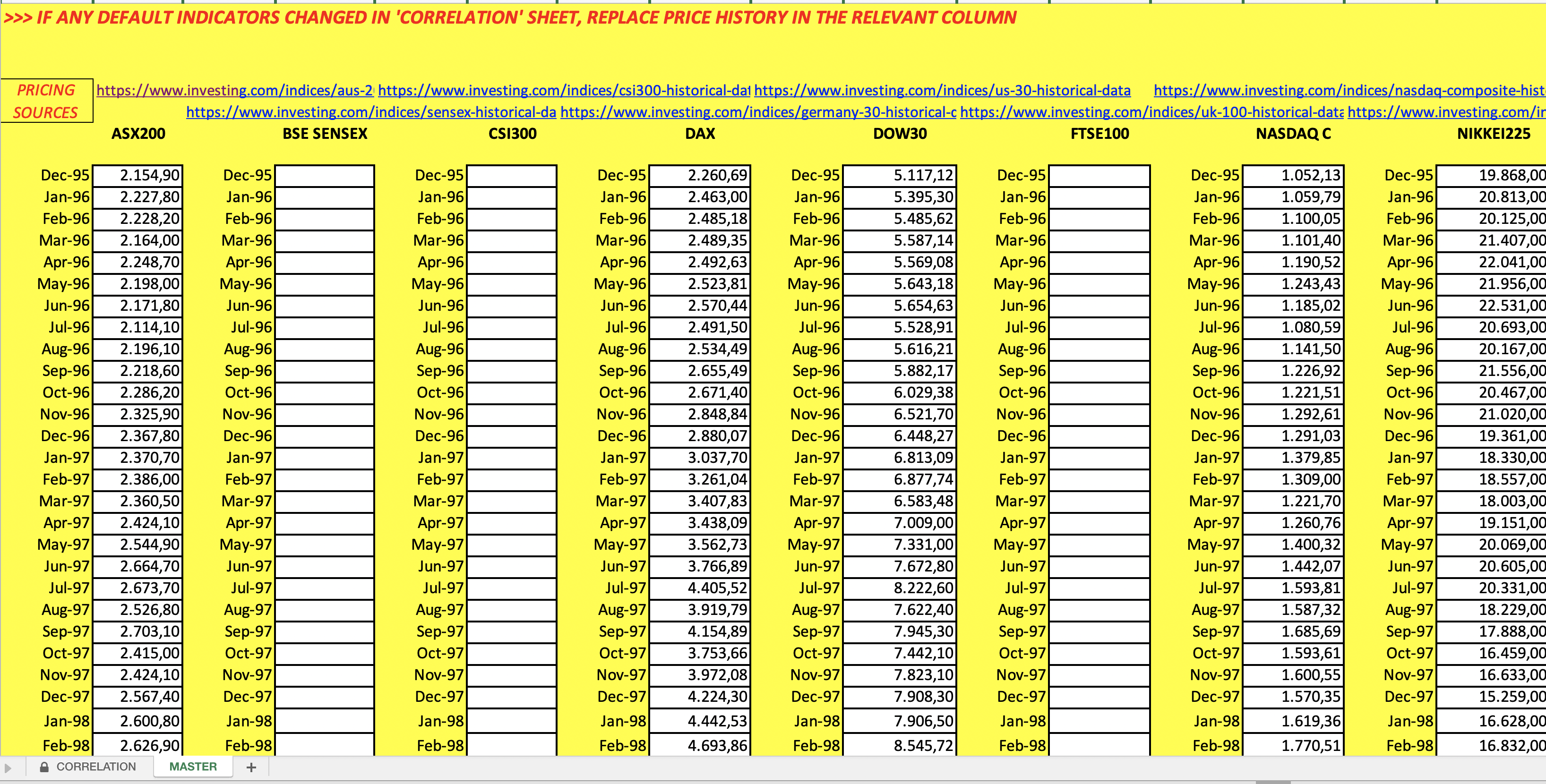

FINANCIAL CORRELATIONS MODEL (2024 VERSION)

Calculate the static or rolling correlation coefficient between any two variables, based on price or return, for optimal asset allocation or research purposes.

Domenico Cristarella offers you this Best Practice for free!

download for free

Add to bookmarks

Further information

CORRELATION CALCULATION FOR APPROPRIATE ASSET ALLOCATION