Originally published: 31/01/2025 23:03

Publication number: ELQ-88755-1

View all versions & Certificate

Publication number: ELQ-88755-1

View all versions & Certificate

Fintech-as-a-Service (FaaS) Company Financial Model 20 Years 3 Statement

A comprehensive editable 20-year 3-statement, MS Excel spreadsheet for tracking a Fintech-as-a Service (FaaS) Company finances.

AllFinancialModels offer a curated selection of high-quality yet financial model templates designed to support a wide range of business needs.Follow

fintechfaasfintech as a servicesoftware as a servicesaasspreadsheettemplateexcelfinancial modelfinance

Description

20-Year 3-Statement Financial Model for a Fintech as a Service (FaaS) Company.

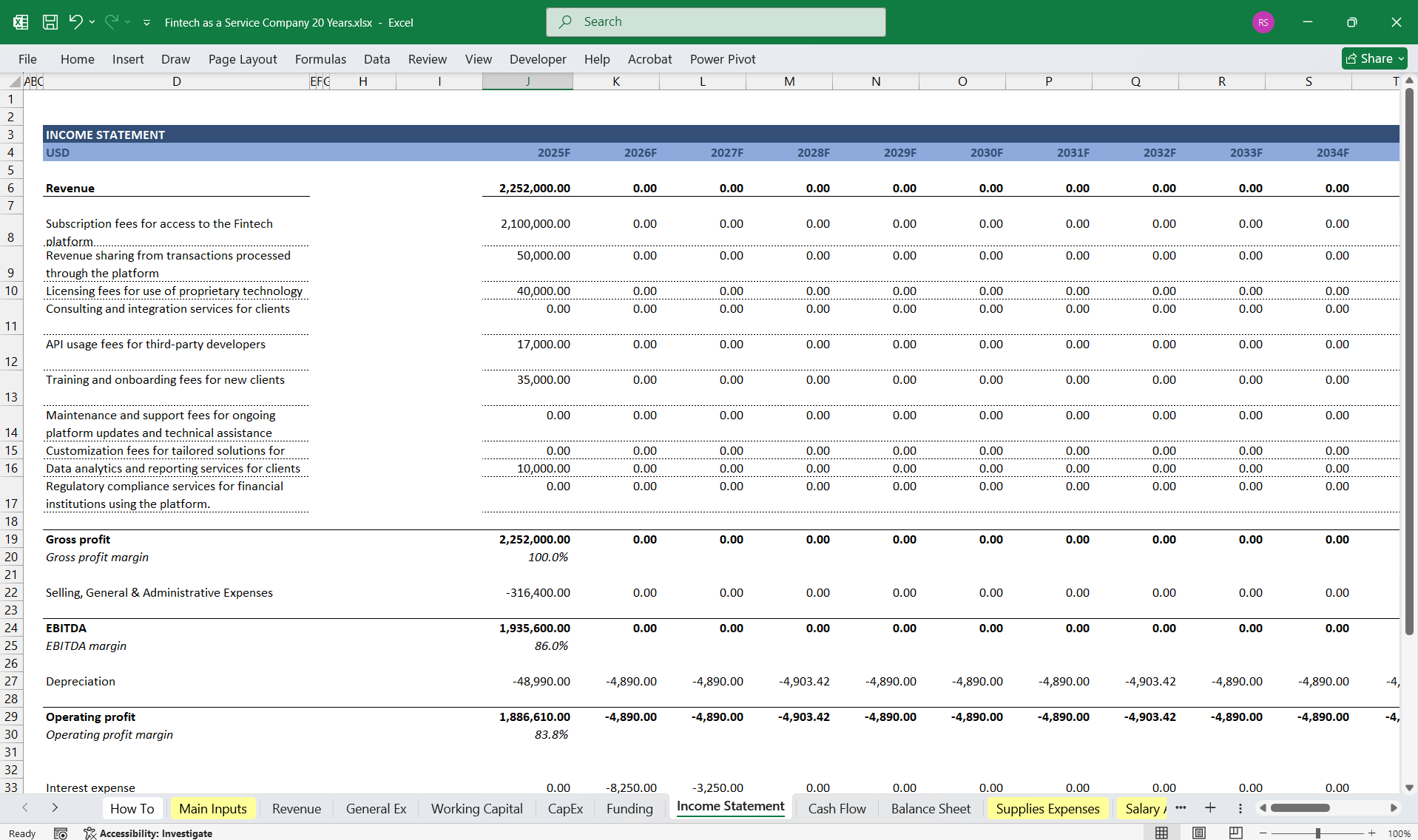

1. Income StatementRevenue Streams: (All fully Editable)

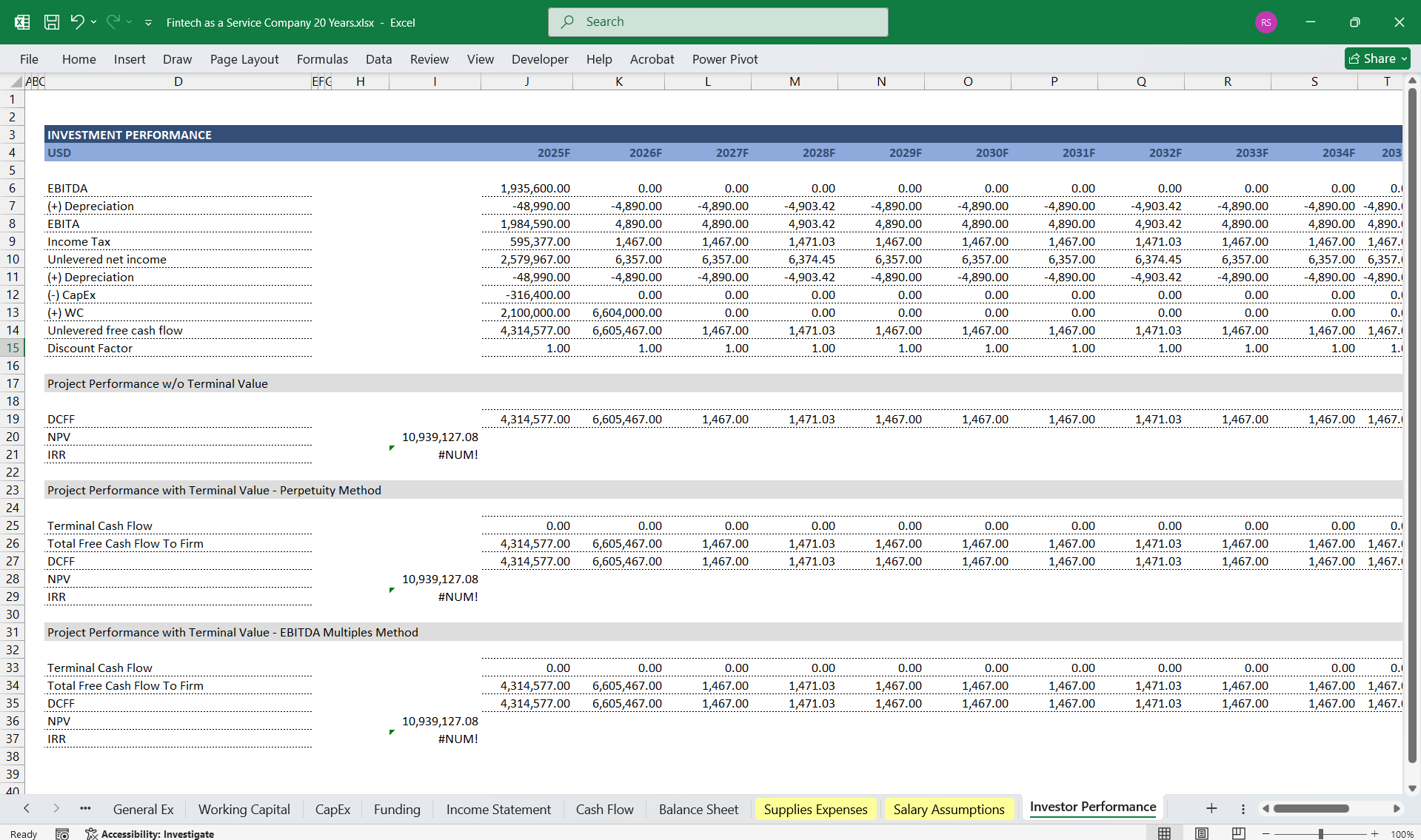

This detailed three-statement model provides a comprehensive 20-year financial projection for a Fintech as a Service company. It integrates various revenue streams and cost structures to support long-term financial planning and valuation.

20-Year 3-Statement Financial Model for a Fintech as a Service (FaaS) Company.

1. Income StatementRevenue Streams: (All fully Editable)

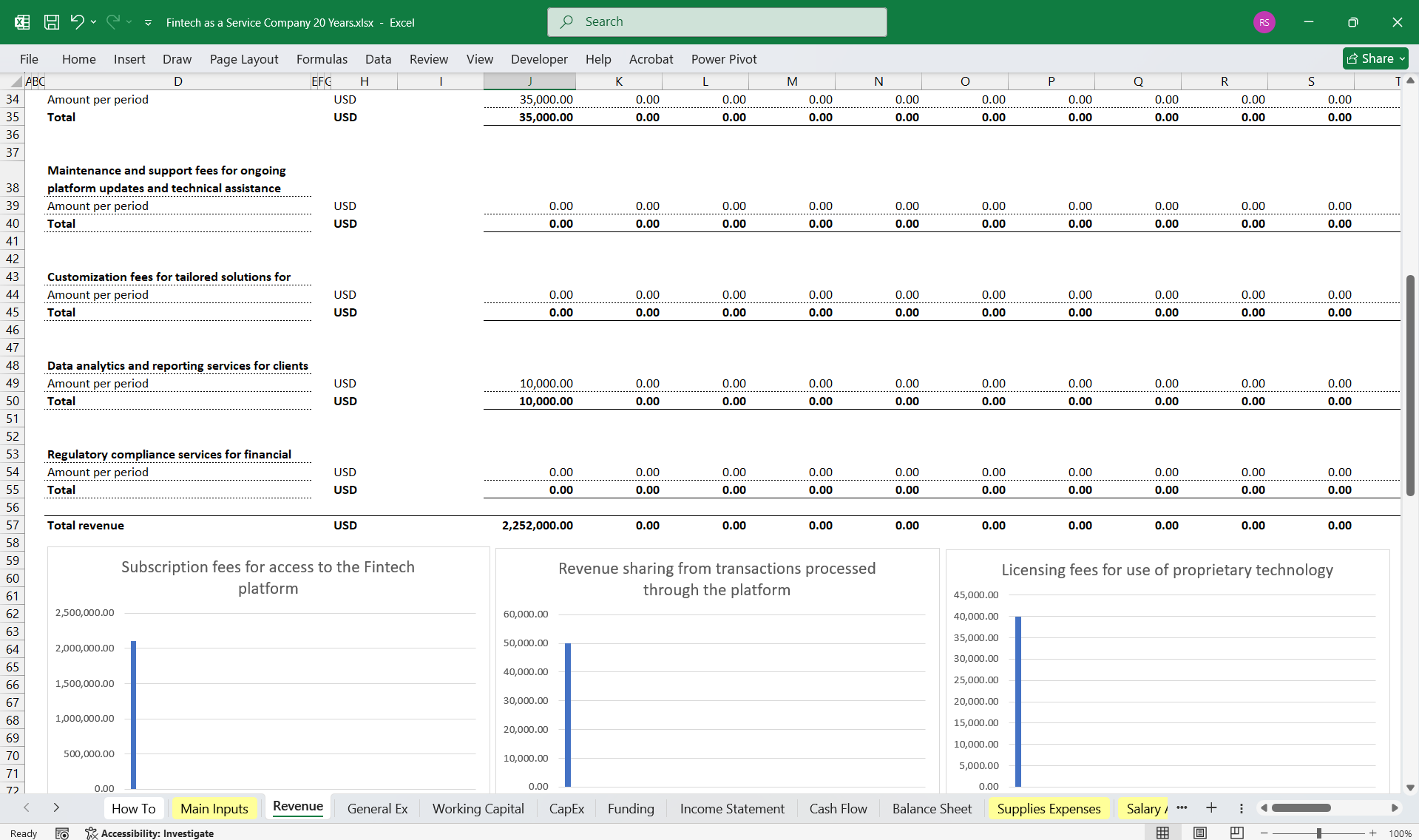

- Subscription Fees – Recurring revenue from clients subscribing to access the Fintech platform.

- Revenue Sharing – Percentage of transaction fees generated from payments processed through the platform.

- Licensing Fees – Charges for external entities utilizing proprietary technology.

- Consulting & Integration Services – Revenue from implementation, advisory, and integration work for clients.

- API Usage Fees – Charges based on API calls by third-party developers.

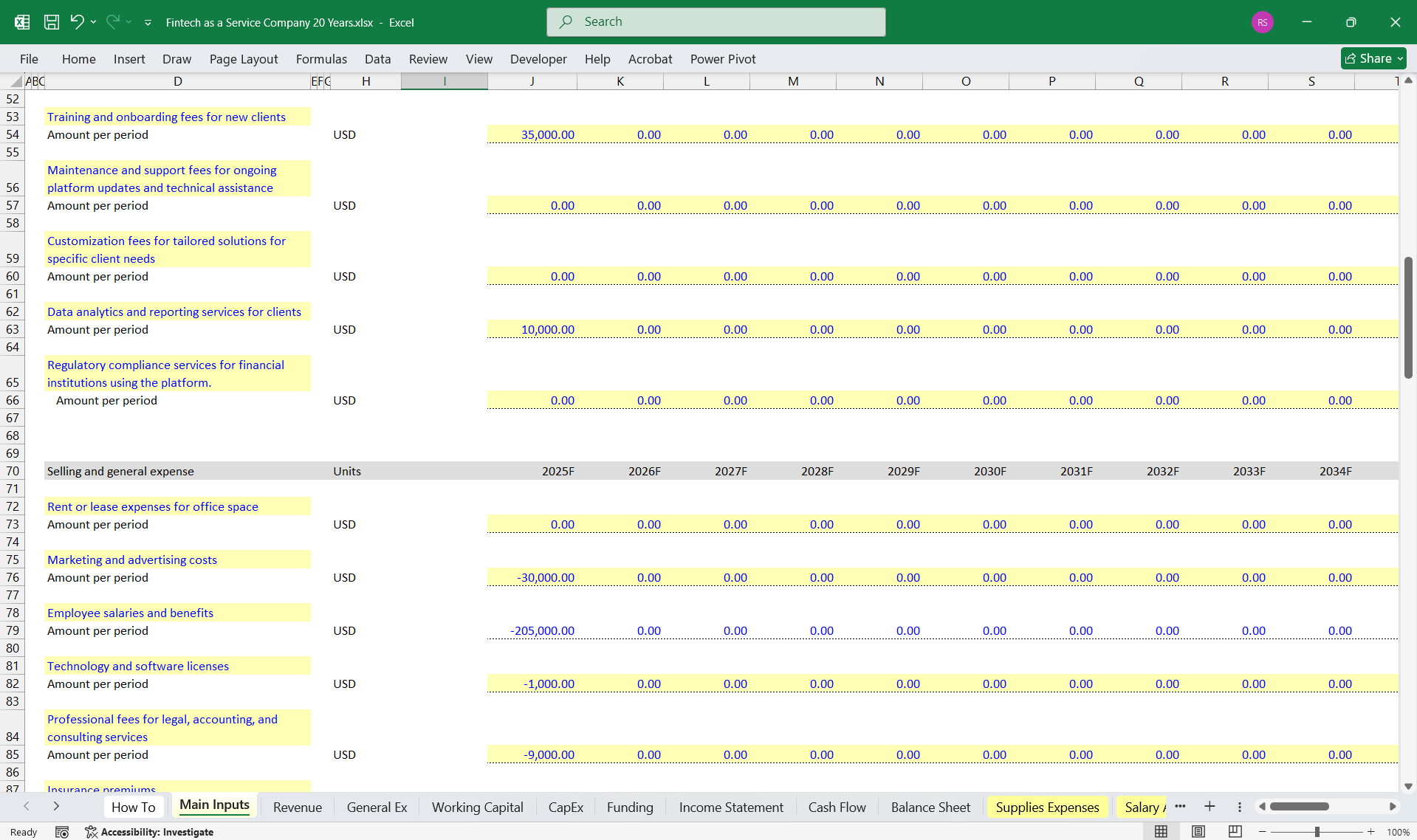

- Training & Onboarding Fees – One-time charges for onboarding new clients.

- Maintenance & Support Fees – Recurring revenue from ongoing platform updates and technical support.

- Customization Fees – One-time revenue from customized client solutions.

- Data Analytics & Reporting Services – Charges for advanced data insights provided to clients.

- Regulatory Compliance Services – Revenue from regulatory compliance support for financial institutions.

- Cost of Goods Sold (COGS) – Hosting costs, third-party service fees, transaction costs.

- Research & Development (R&D) – Investments in platform enhancements and innovation.

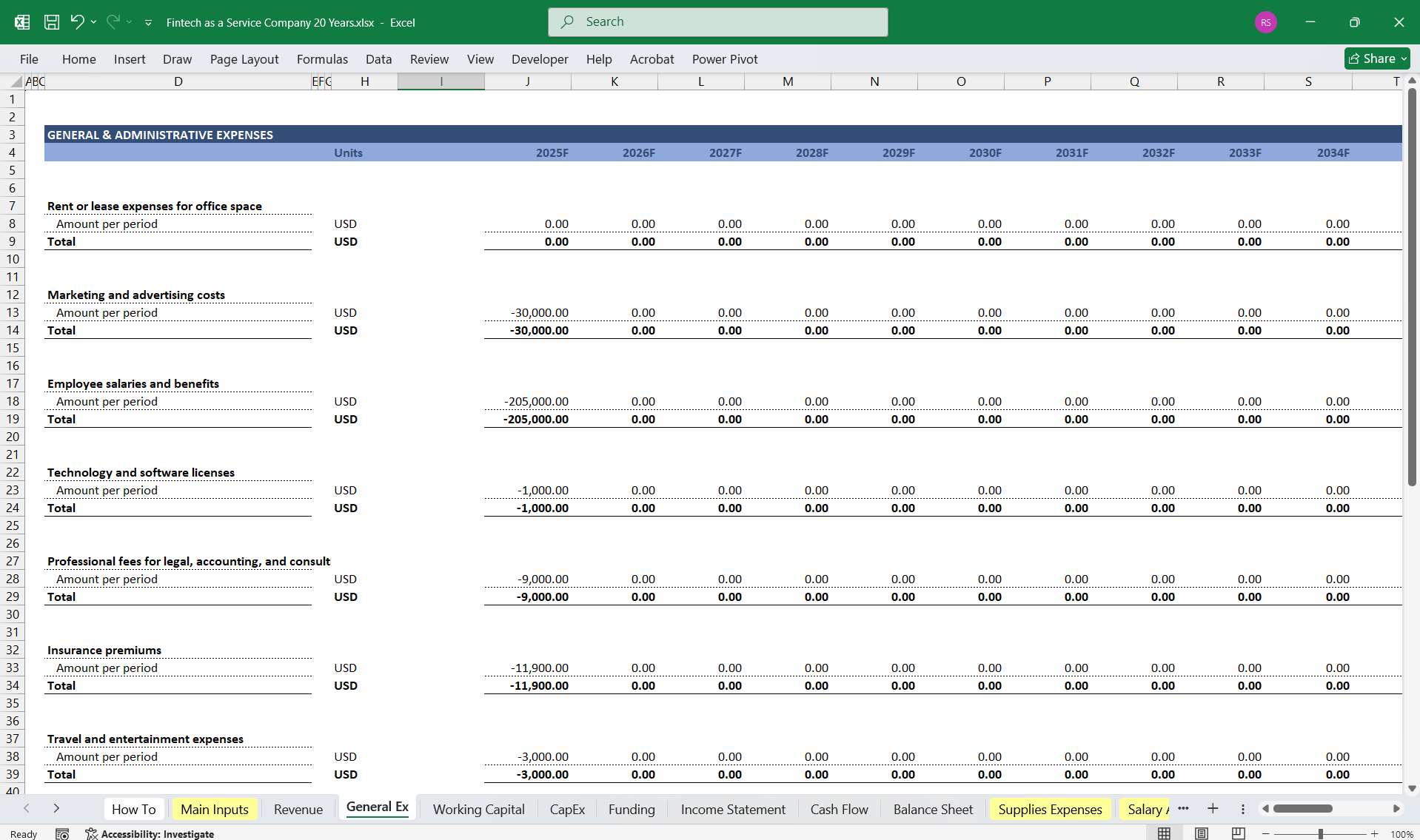

- Sales & Marketing – Customer acquisition, partnerships, and branding.

- General & Administrative (G&A) – Employee salaries, office expenses, legal, compliance.

- Depreciation & Amortization – Asset depreciation, amortization of software development costs.

- Customer Support & Success – Staff costs for assisting and retaining clients.

- Gross Profit = Revenue - COGS

- Operating Profit = Gross Profit - Operating Expenses

- Net Profit = Operating Profit - Interest - Taxes

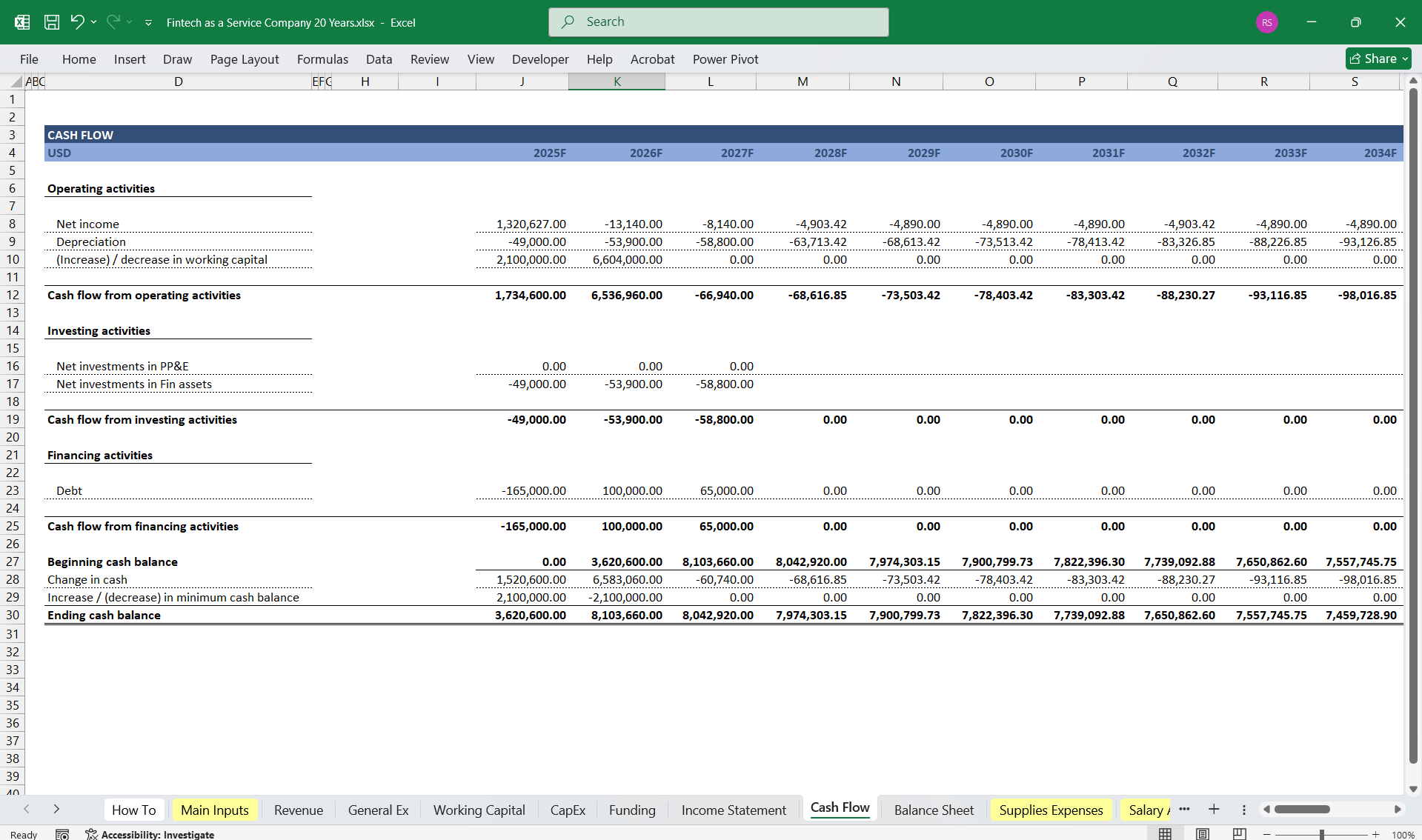

- Net Income – Carried forward from the income statement.

- Adjustments for Non-Cash Items – Depreciation & amortization, stock-based compensation.

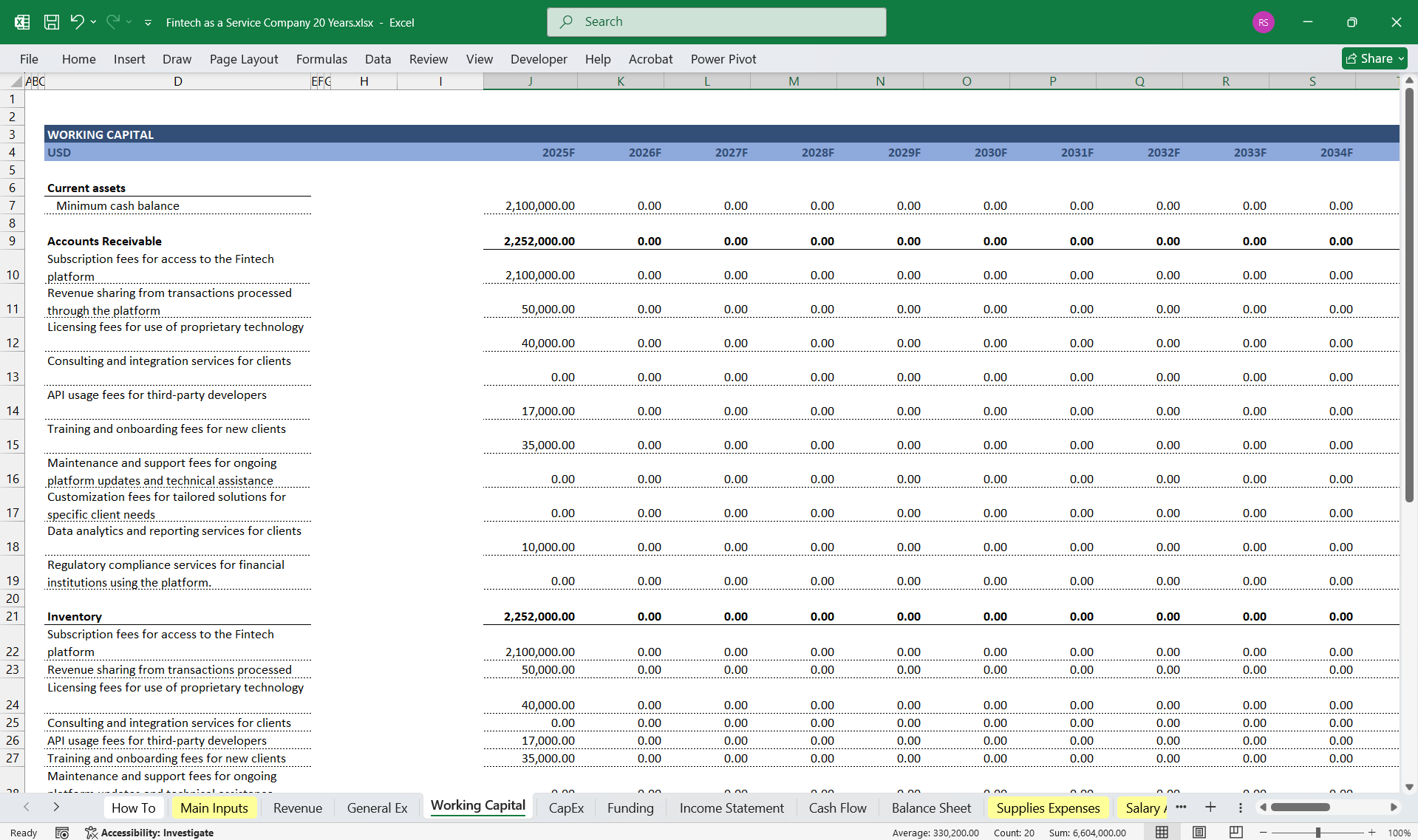

- Changes in Working Capital:

- Accounts Receivable – Adjustments for client payments.

- Accounts Payable – Adjustments for vendor and partner payments.

- Deferred Revenue – Prepaid subscription fees and service contracts.

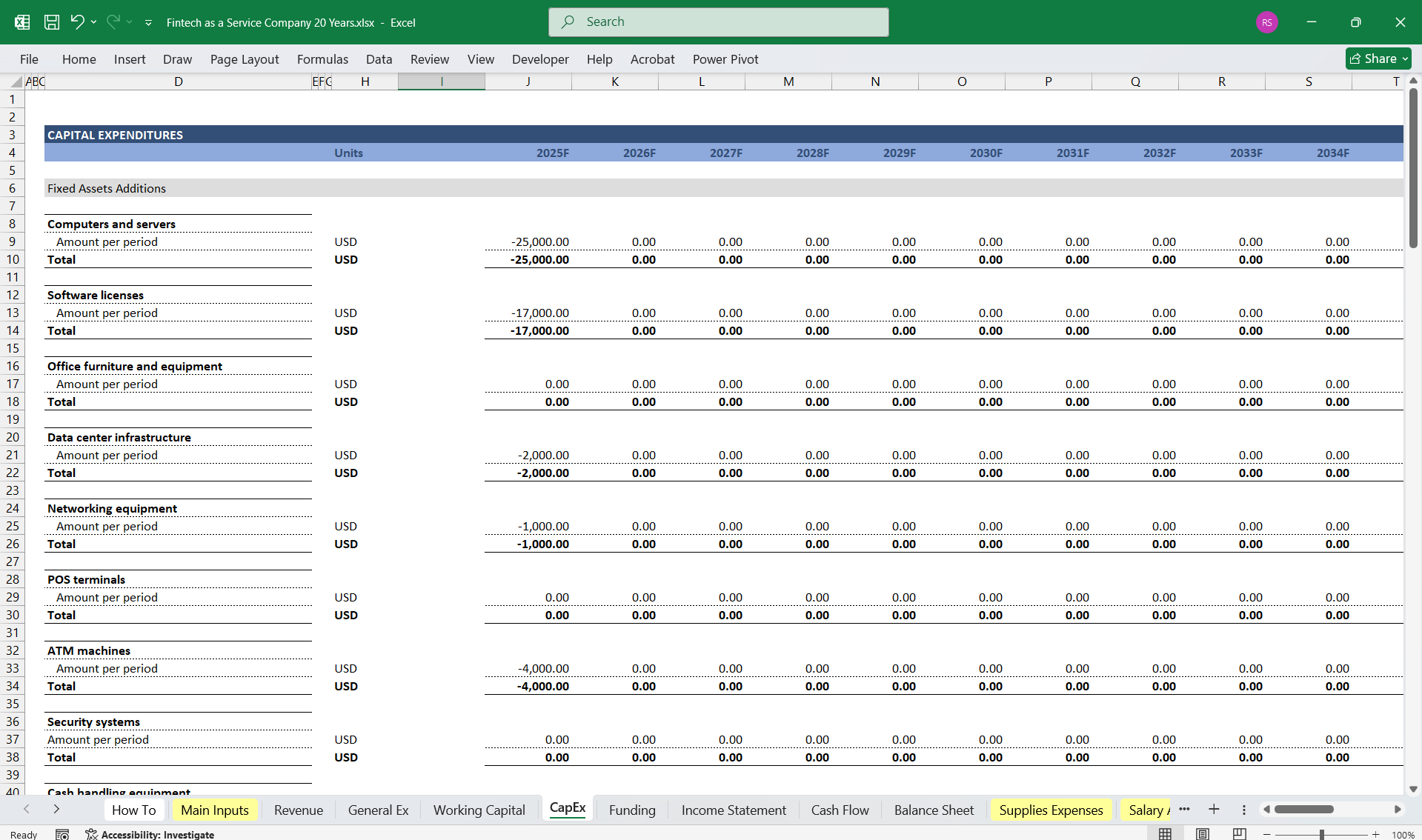

- Capital Expenditures (CapEx) – Infrastructure investment, servers, and software development.

- Acquisitions & Investments – Strategic purchases or investments in technology or partnerships.

- R&D Investments – New feature development and enhancements.

- Equity Issuance – Fundraising rounds (Seed, Series A, B, etc.).

- Debt Financing – Loan proceeds and repayments.

- Dividends & Buybacks – Cash used to return value to shareholders.

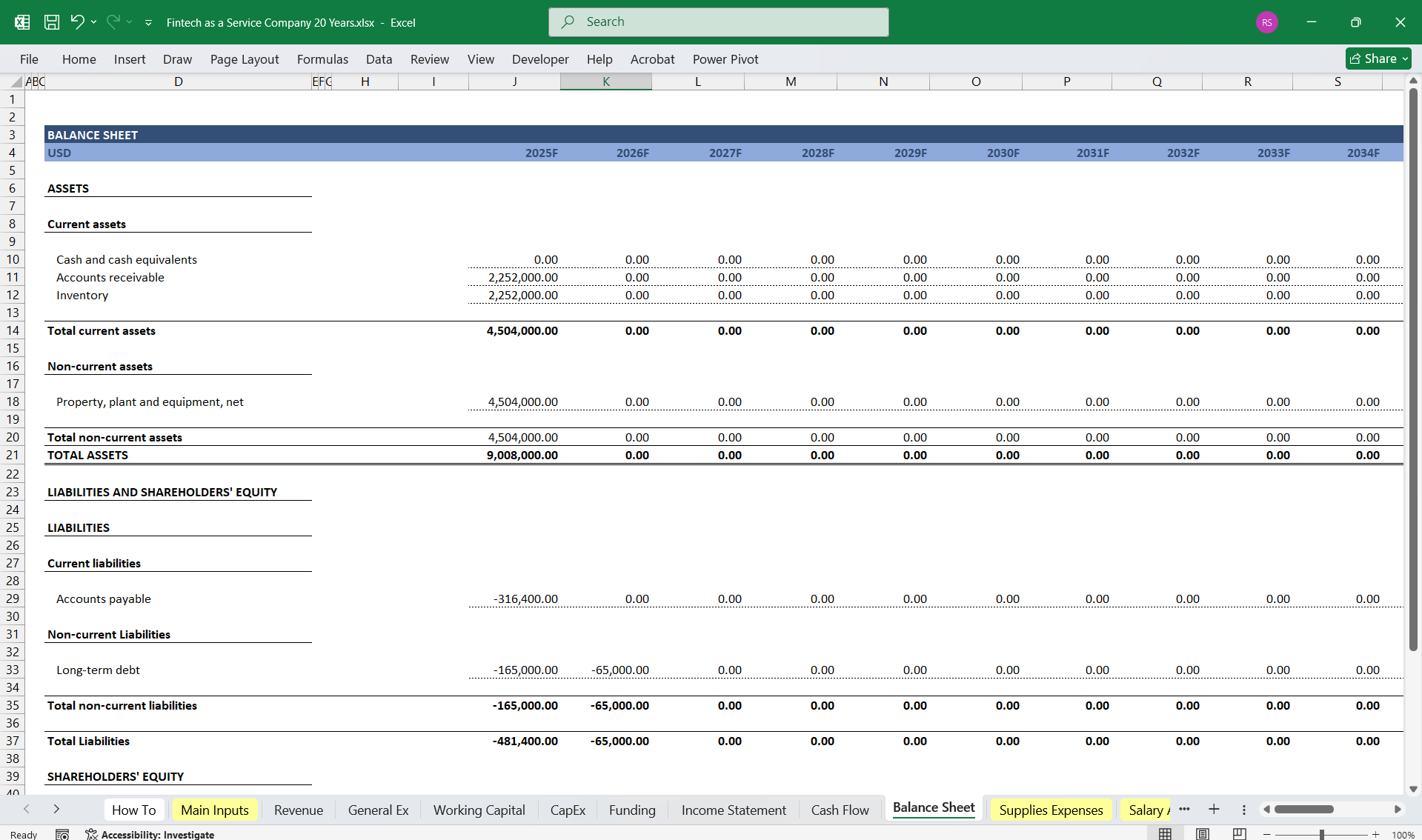

- Current Assets:

- Cash & Cash Equivalents – Available liquidity.

- Accounts Receivable – Pending payments from clients.

- Prepaid Expenses – Costs paid in advance for future services.

- Long-Term Assets:

- Property, Plant & Equipment (PP&E) – Infrastructure, servers, and technology investments.

- Intangible Assets – Software and patents.

- Goodwill – Value from acquisitions.

- Current Liabilities:

- Accounts Payable – Amounts owed to vendors.

- Deferred Revenue – Prepaid services yet to be delivered.

- Short-Term Debt – Loans due within a year.

- Long-Term Liabilities:

- Long-Term Debt – Outstanding loans beyond one year.

- Other Long-Term Liabilities – Pension obligations, lease liabilities.

- Common Stock & Additional Paid-In Capital – Equity financing.

- Retained Earnings – Profits reinvested in the business.

- Treasury Stock – Stock repurchases.

- Revenue Growth:

- High initial growth (~50% CAGR for the first 5 years), stabilizing to ~10-15% annually.

- Operating Margins:

- Improving efficiency as the company scales, targeting 30-40% EBITDA margins.

- Customer Churn Rate:

- Assumed 5-10% annually, offset by new client acquisitions.

- Capital Expenditure (CapEx):

- 15-20% of revenue in early years, reducing as infrastructure stabilizes.

- R&D Spend:

- 20-30% of revenue in early years, declining to ~10% over time.

- Working Capital Management:

- Assumed improvement in DSO (Days Sales Outstanding) and DPO (Days Payable Outstanding) over time.

This detailed three-statement model provides a comprehensive 20-year financial projection for a Fintech as a Service company. It integrates various revenue streams and cost structures to support long-term financial planning and valuation.

This Best Practice includes

1 Excel Financial Model

Further information

Provides thorough oversight, tracking, and reporting of Fintech-as-a-Service finances, including updates on budget utilisation and projections.