Publication number: ELQ-40001-1

View all versions & Certificate

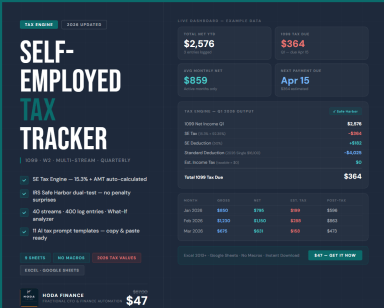

Self Employed Tax Tracker 2026 — Freelance 1099 Quarterly Tax Planner | W2 & Multi-Stream Income | Excel & Google Sheets

Self-Employed Tax Engine — 1099 Quarterly Planner, Excel 2026

UAE Financial Controller | Filing FTA VAT201 Returns Since January 2018 | 9 Years UAE Finance ExperienceFollow

Further information

1. Calculate quarterly self-employment tax (SE tax) accurately using the IRS 92.35% multiplier, the 50% SE deduction, and the 2026 Social Security wage base cap of $184,500 — including the 0.9% Additional Medicare Tax above $200,000.

2. Estimate federal income tax on a quarterly basis by applying the user's blended effective rate to taxable income after the standard deduction.

3. Validate estimated payments against both IRS safe harbor tests: the 90% current-year test and the 100%/110% prior-year test — flagging underpayment risk before each deadline.

4. Separate 1099-NEC, W2, and passive income into distinct tax treatment tracks so the SE tax liability is calculated only on qualifying self-employment income.

5. Track up to 40 simultaneous income streams with month-over-month performance analysis, quarterly goal attainment, and post-tax what-if scenario modeling.

Use this model when

· The user is a US-based sole proprietor or single-member LLC filing Schedule C and Schedule SE on Form 1040.

· The user has 1099-NEC income from freelance work, consulting, digital products, or platform-based self-employment.

· The user also has W2 income and needs to isolate the SE tax liability to the 1099 portion only — avoiding overpayment on blended income.

· The user makes quarterly estimated tax payments and wants to validate each payment against IRS safe harbor thresholds before the Apr 15, Jun 15, Sep 15, and Jan 15 deadlines.

· Annual 1099-NEC net income is between $10,000 and $160,000 — the range where SE tax planning has the most material impact on cash flow.

· The user tracks multiple income streams (Etsy, consulting, YouTube, affiliate, subscriptions) and needs consolidated P&L visibility across all sources.

Do not use this model when

· The user is not a US taxpayer. This model is built specifically for IRS Form 1040 filers and uses US tax concepts (SE tax, Schedule C, standard deduction). It is not applicable to UK, EU, UAE, or other non-US tax systems.

· The user is an S-corporation or multi-member LLC taxed as a partnership. SE tax treatment differs materially for these structures — this model assumes sole proprietor or SMLLC status.

· The user requires bracket-based marginal tax rate calculation. The income tax estimate uses a blended effective rate entered by the user, not a tax bracket lookup table. Users with complex marginal rate situations should use the output as a directional estimate only.

· The user has significant passive income from qualified dividends or long-term capital gains taxed at preferential rates. This model applies the user's ordinary income rate to all income types — it does not differentiate qualified dividend or LTCG rates.

· The user is a US expatriate, nonresident alien, or has multi-jurisdictional tax obligations. This model is designed for standard domestic Form 1040 filers only.