Originally published: 22/05/2023 07:32

Publication number: ELQ-33936-1

View all versions & Certificate

Publication number: ELQ-33936-1

View all versions & Certificate

Further information

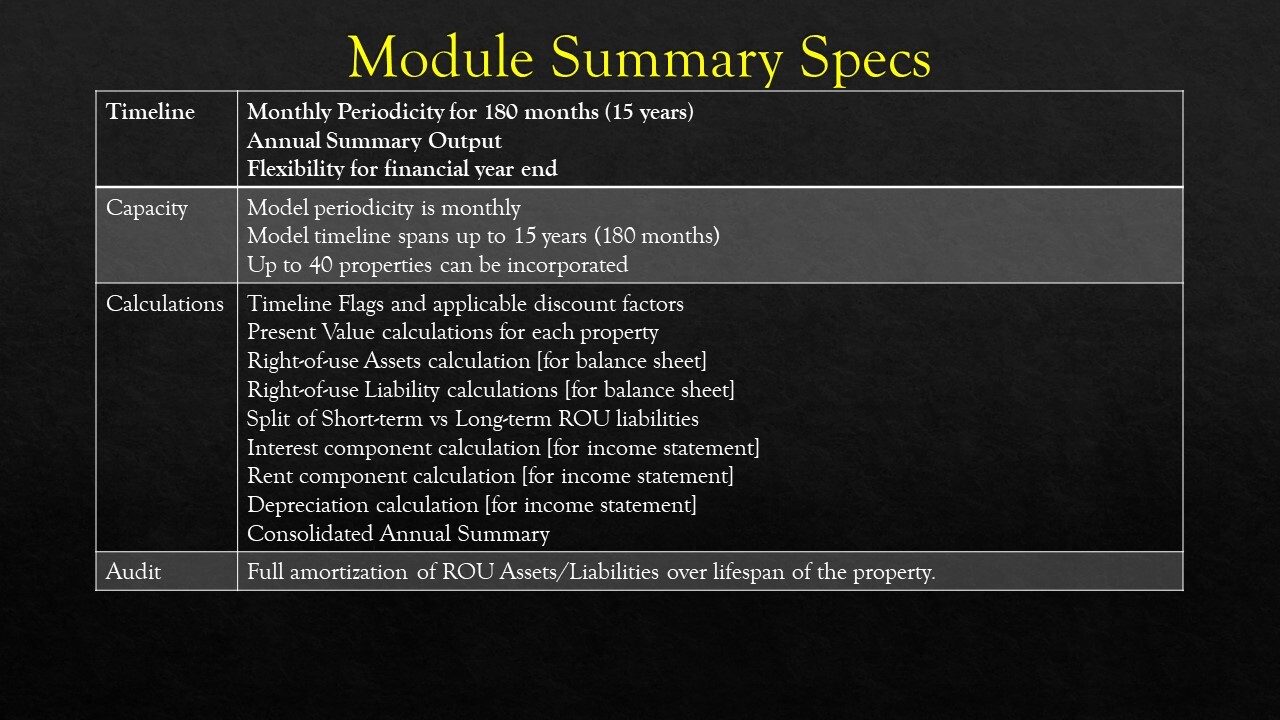

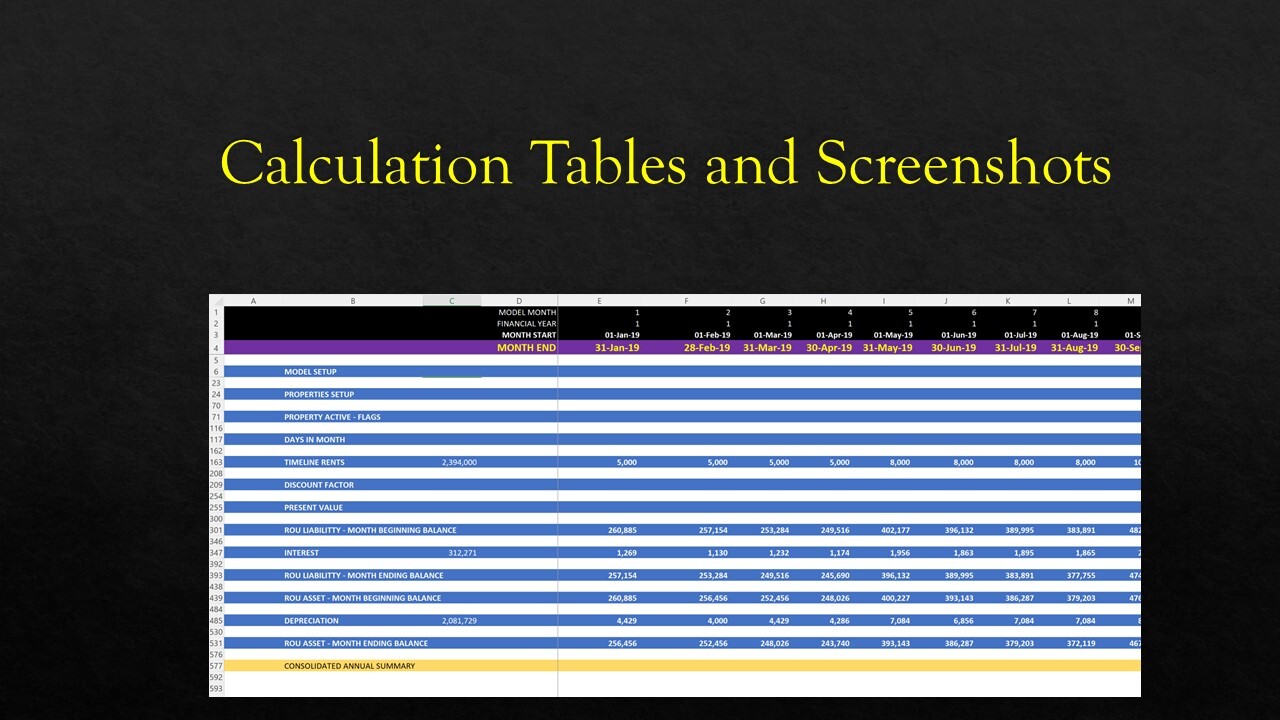

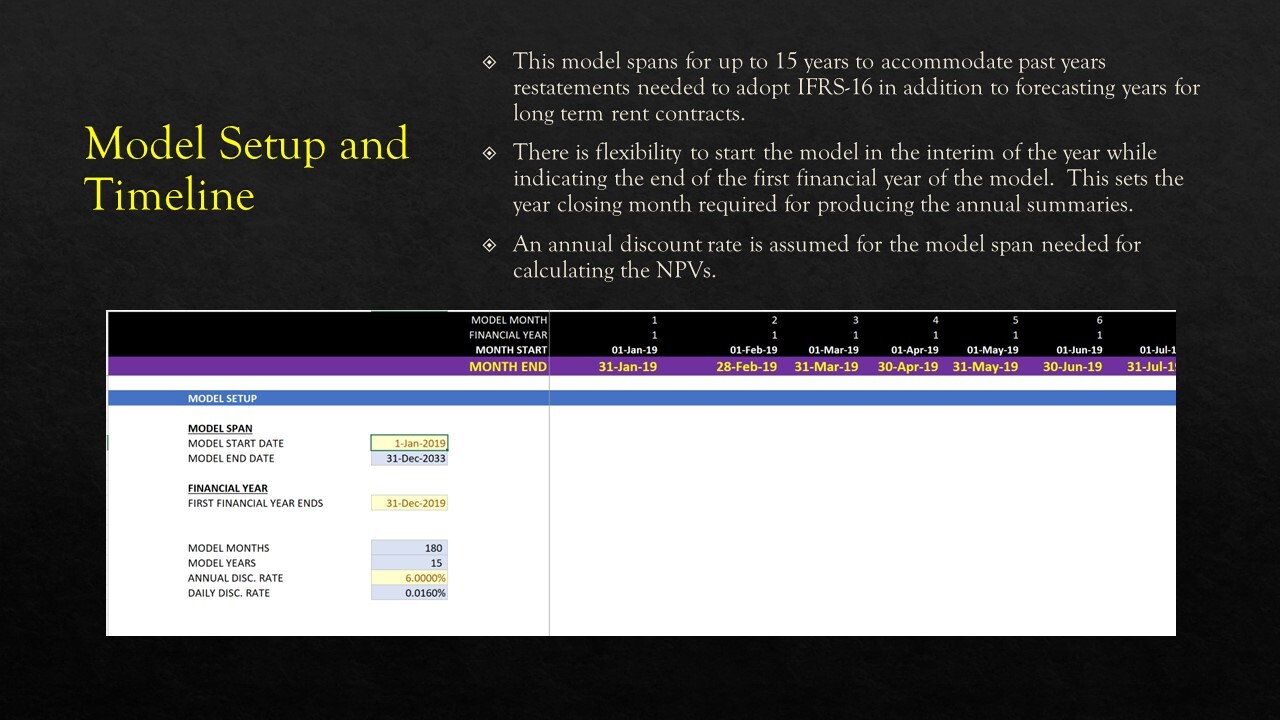

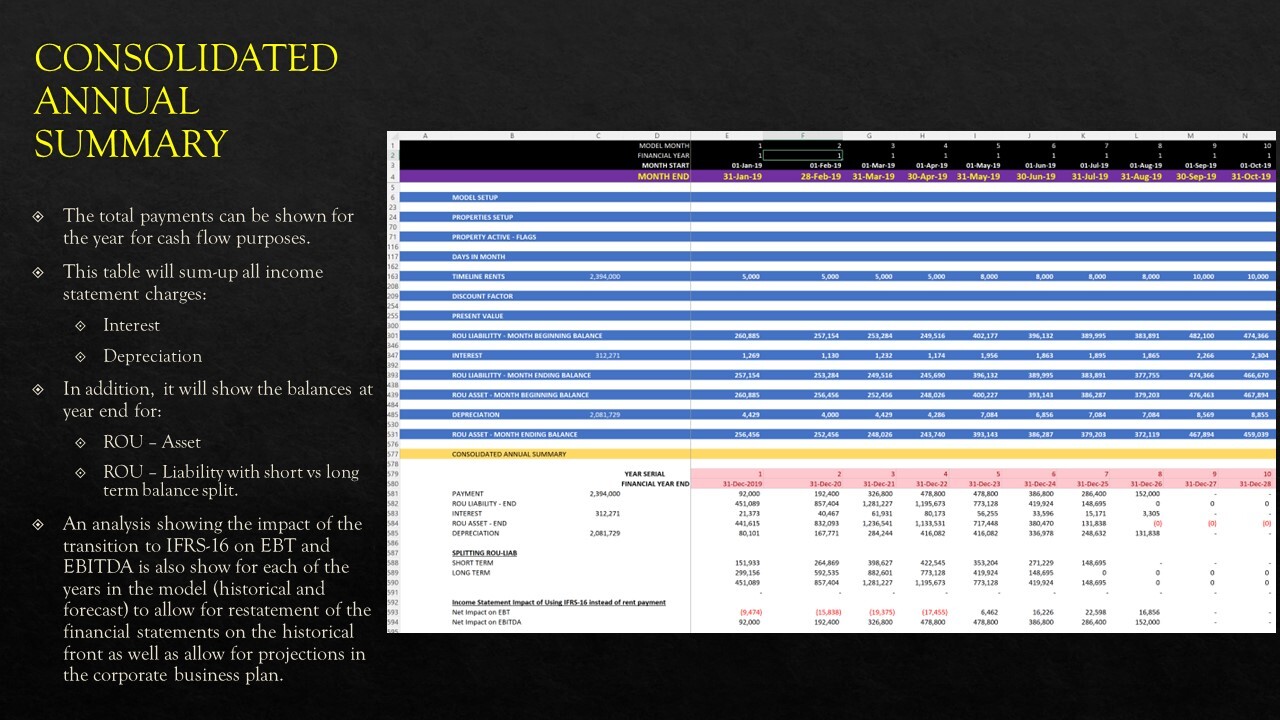

This module allows for a transition to use IFRS-16 in both accounting records and business planning on the corporate level.

User must have the latest office 365 excel version to ensure all function work properly