Originally published: 09/04/2018 15:33

Publication number: ELQ-84390-1

View all versions & Certificate

Publication number: ELQ-84390-1

View all versions & Certificate

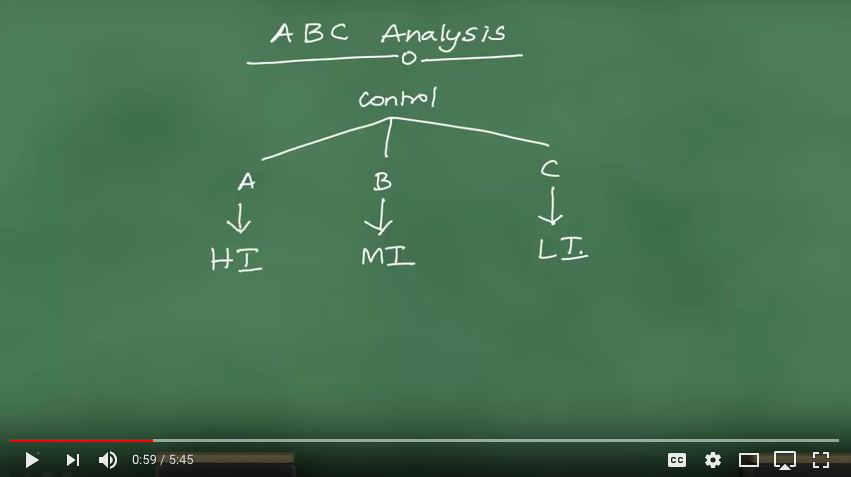

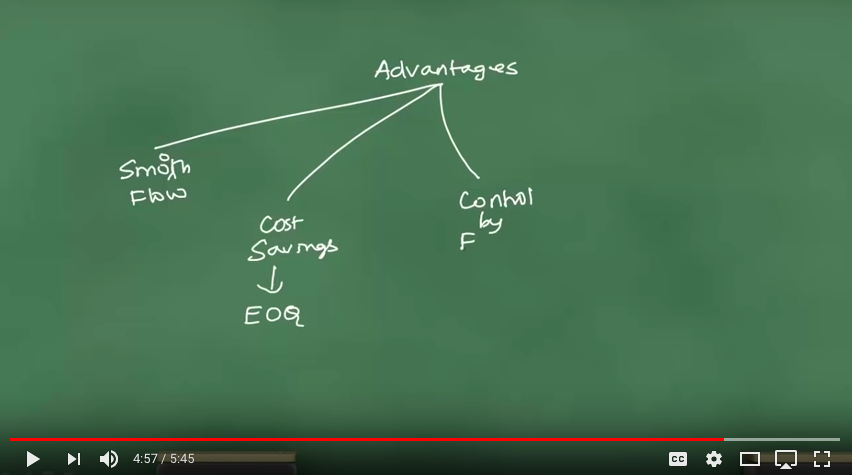

ABC Analysis

Learn how to conduct ABC Analysis and calculate the control you need of your materials.

Add to bookmarks

Did CA N Raja Natarajan's Best Practice help you? You can make a small financial contribution to support the author.

helpSupport