Originally published: 10/03/2025 09:04

Last version published: 09/10/2025 08:00

Publication number: ELQ-84080-2

View all versions & Certificate

Last version published: 09/10/2025 08:00

Publication number: ELQ-84080-2

View all versions & Certificate

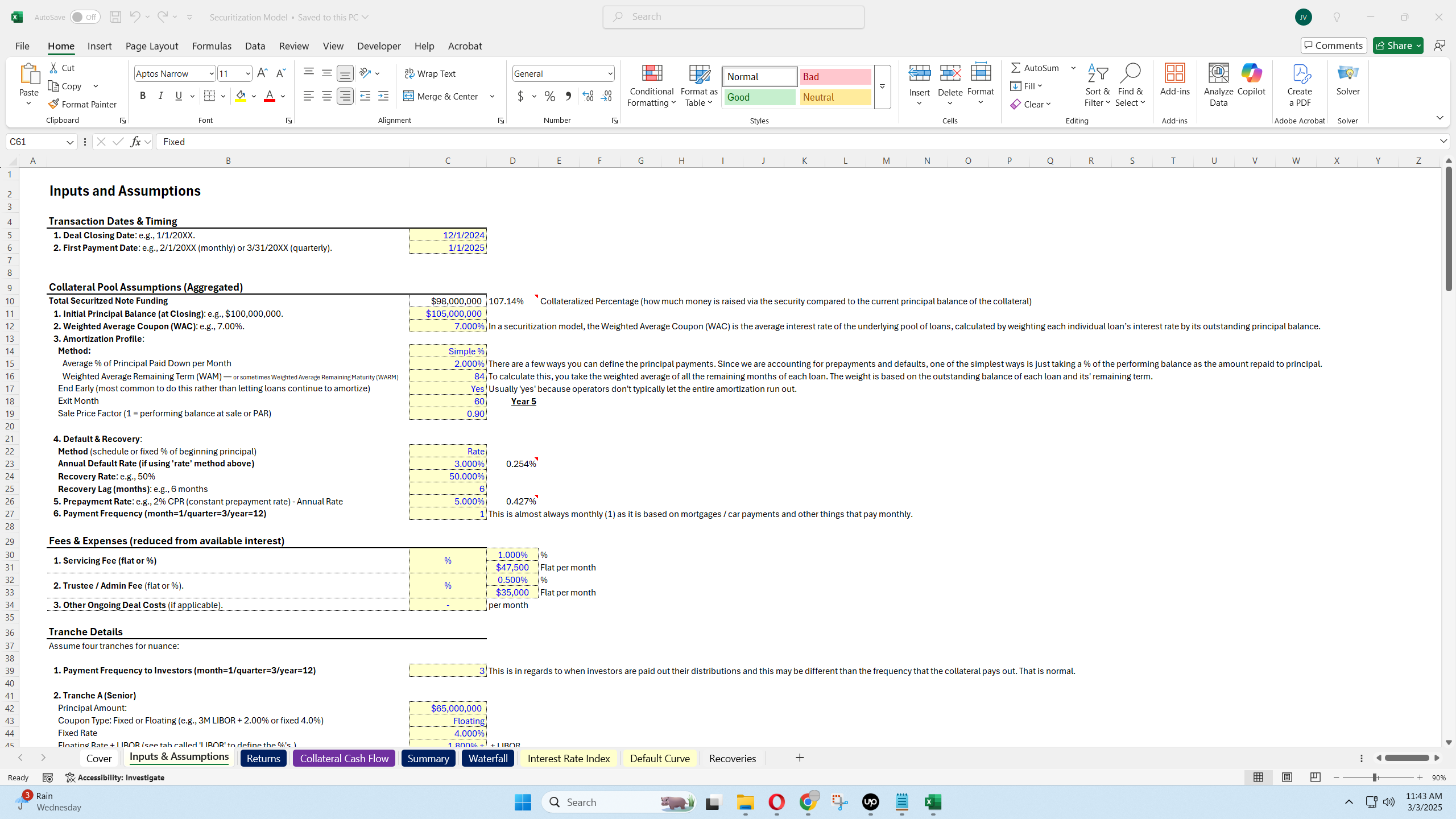

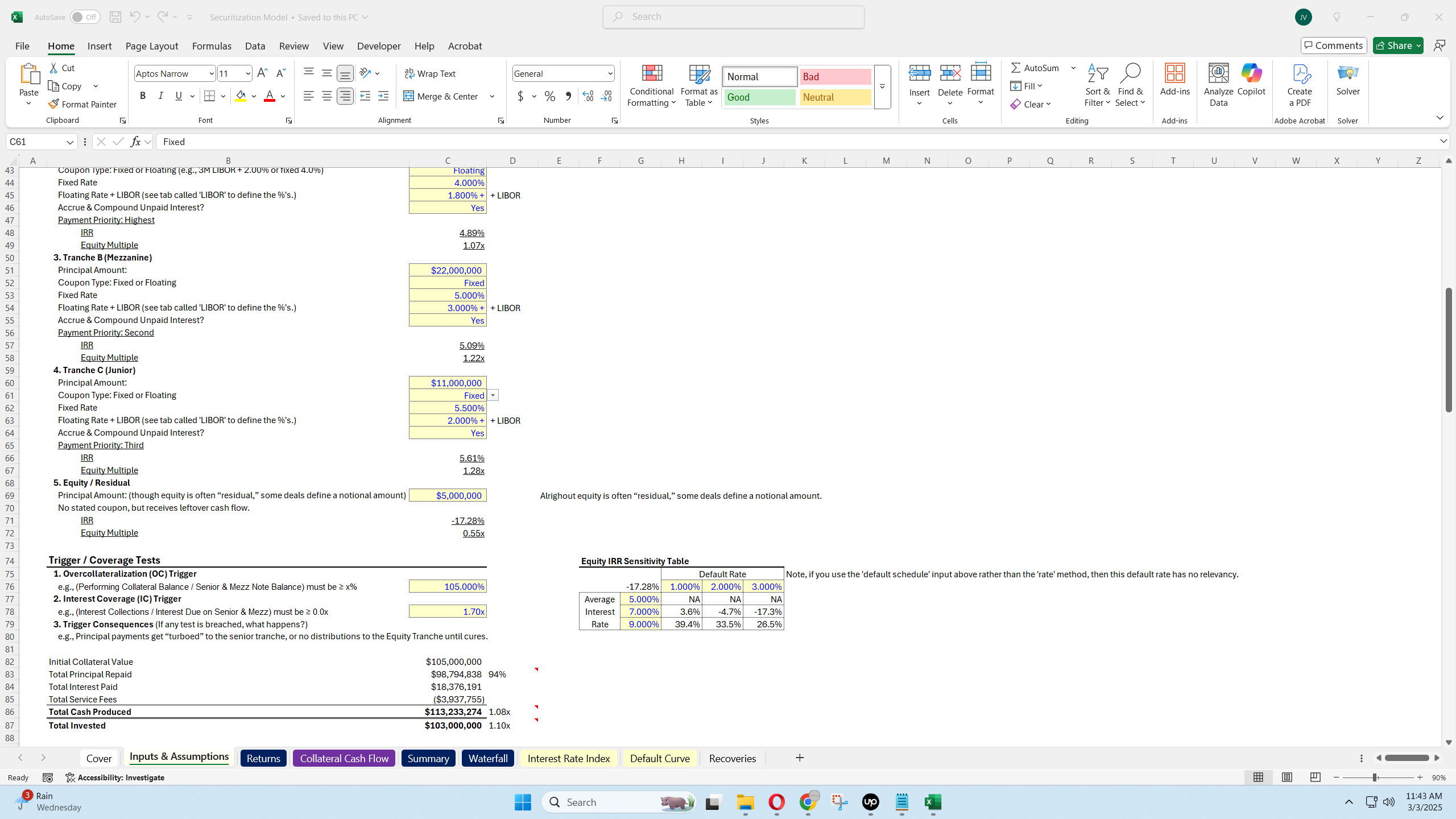

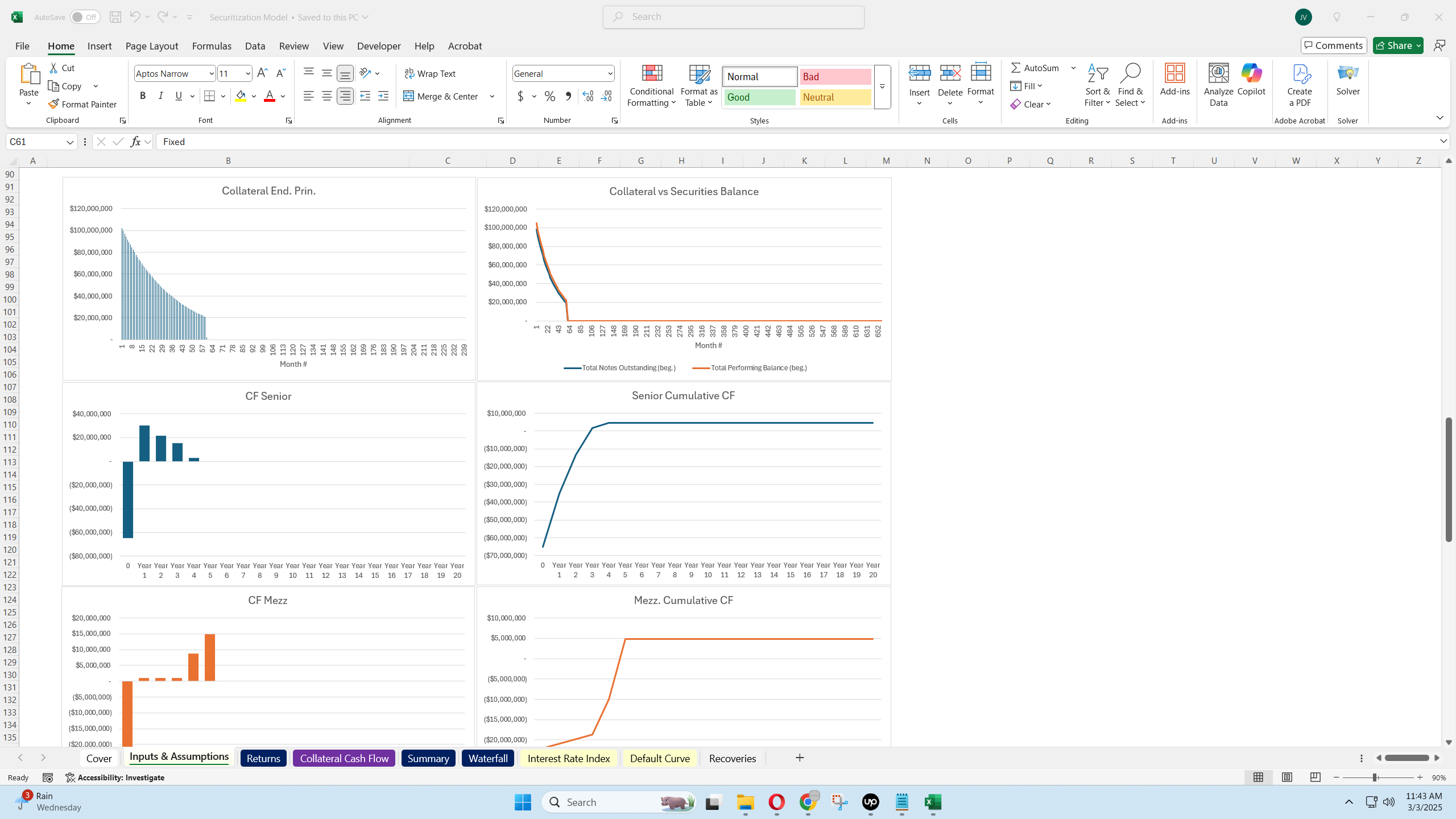

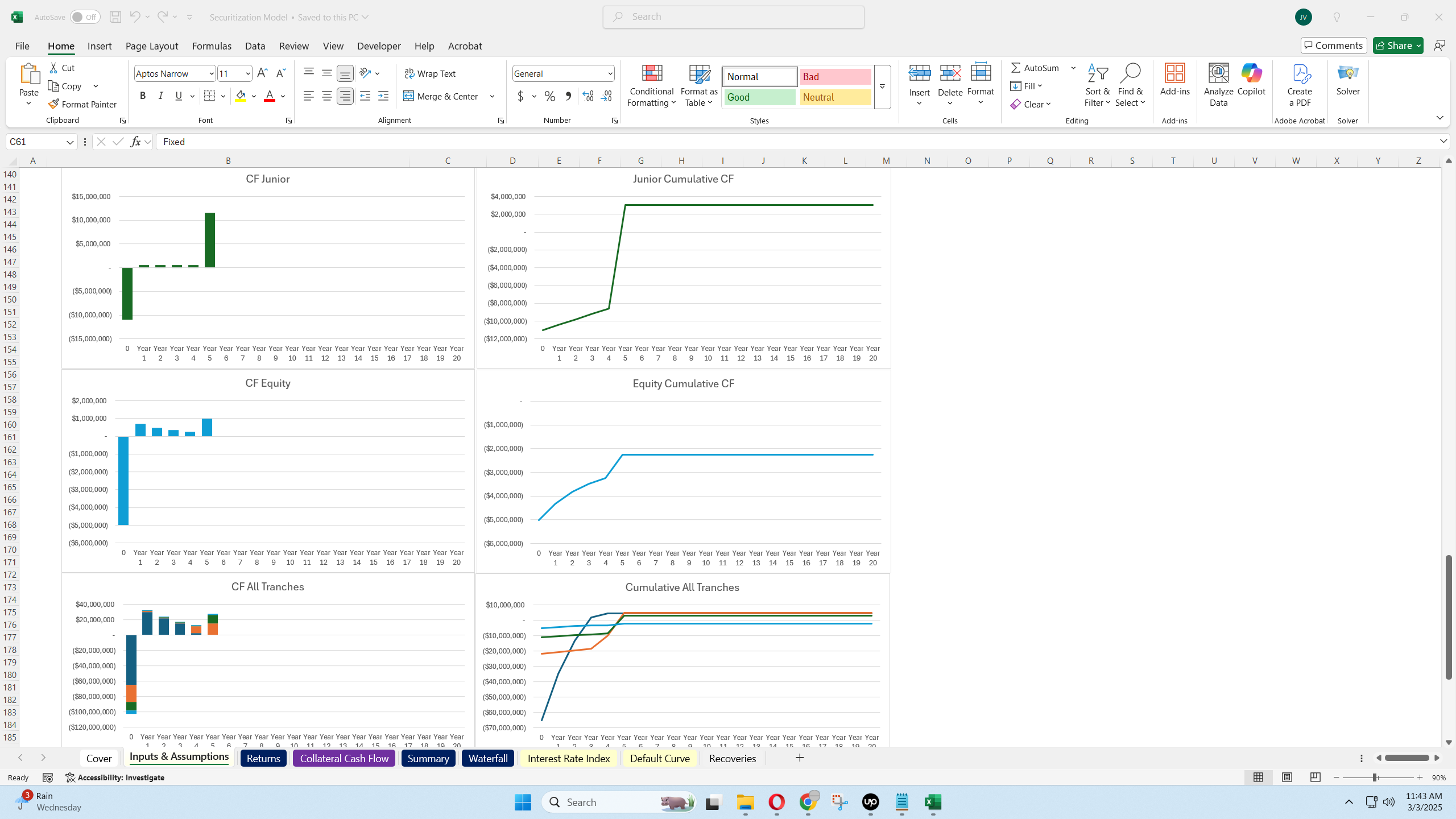

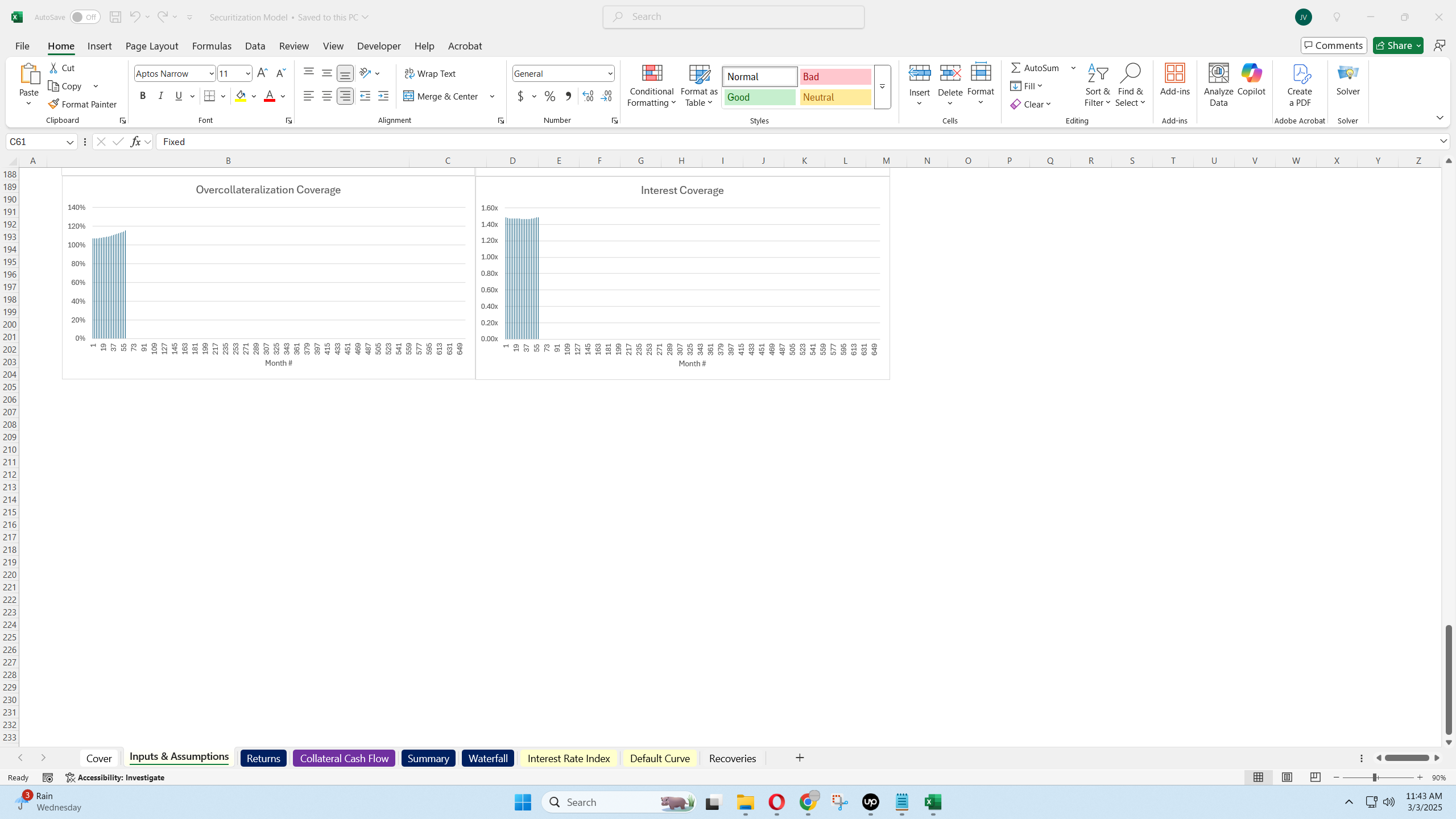

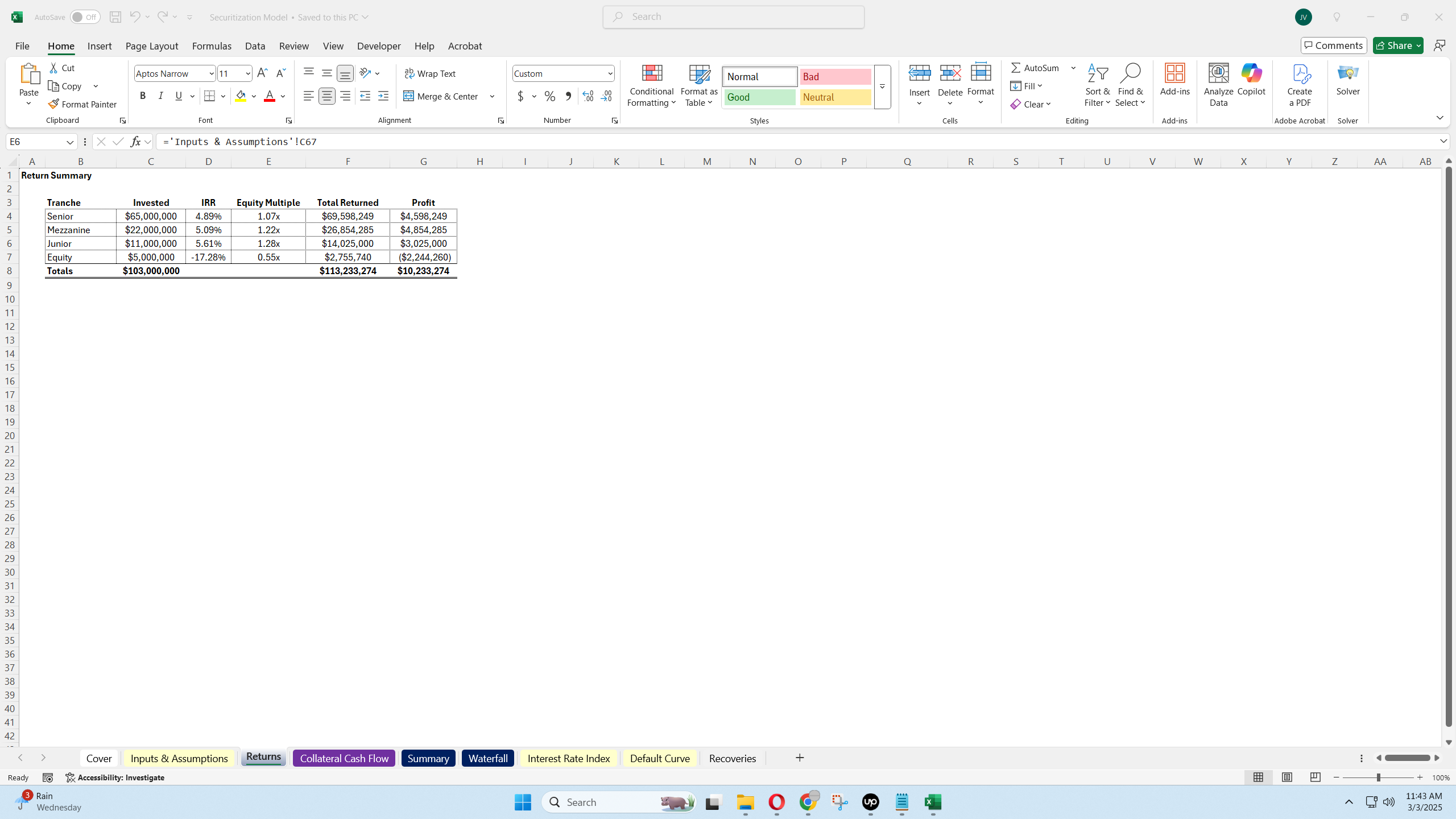

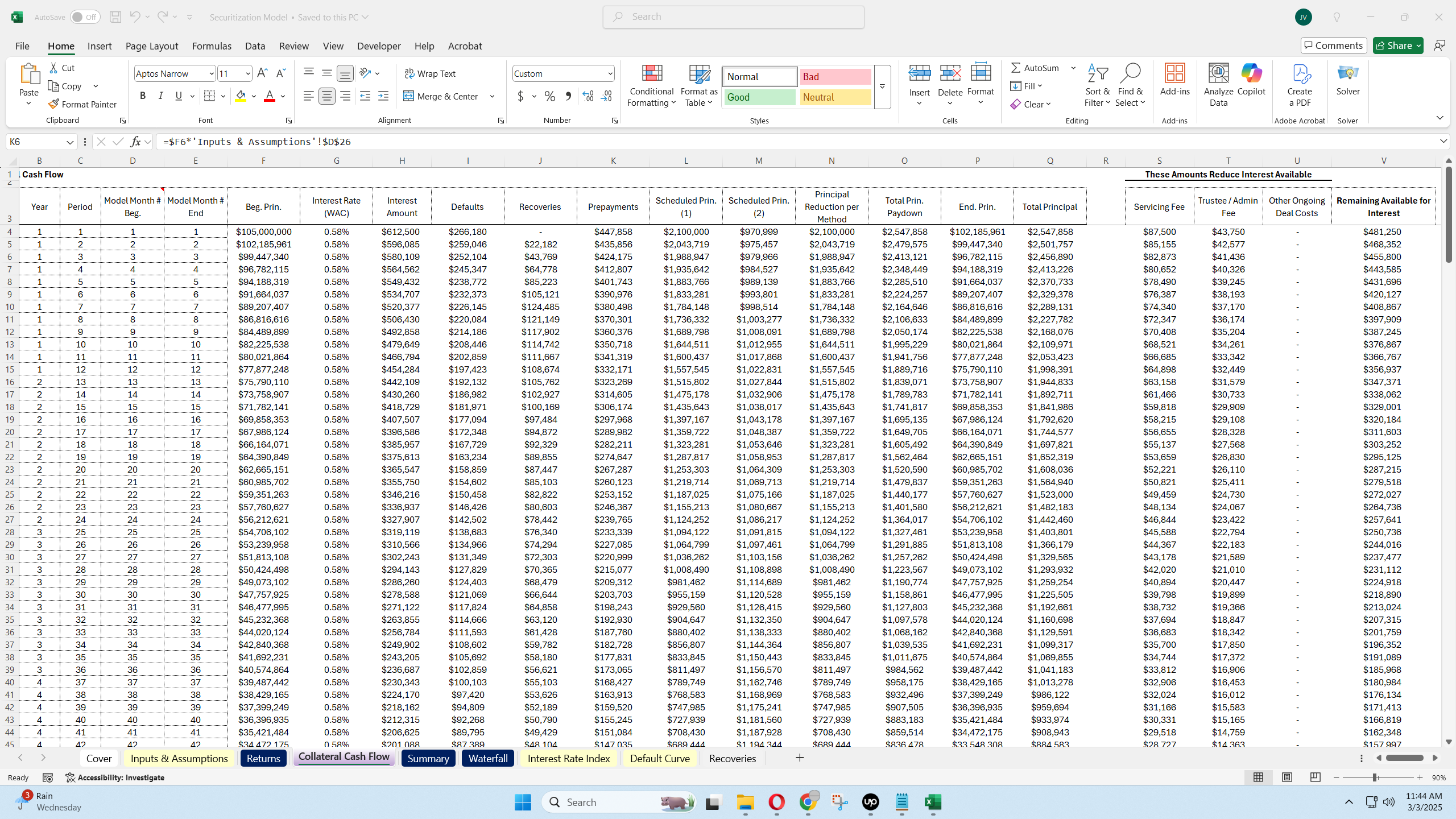

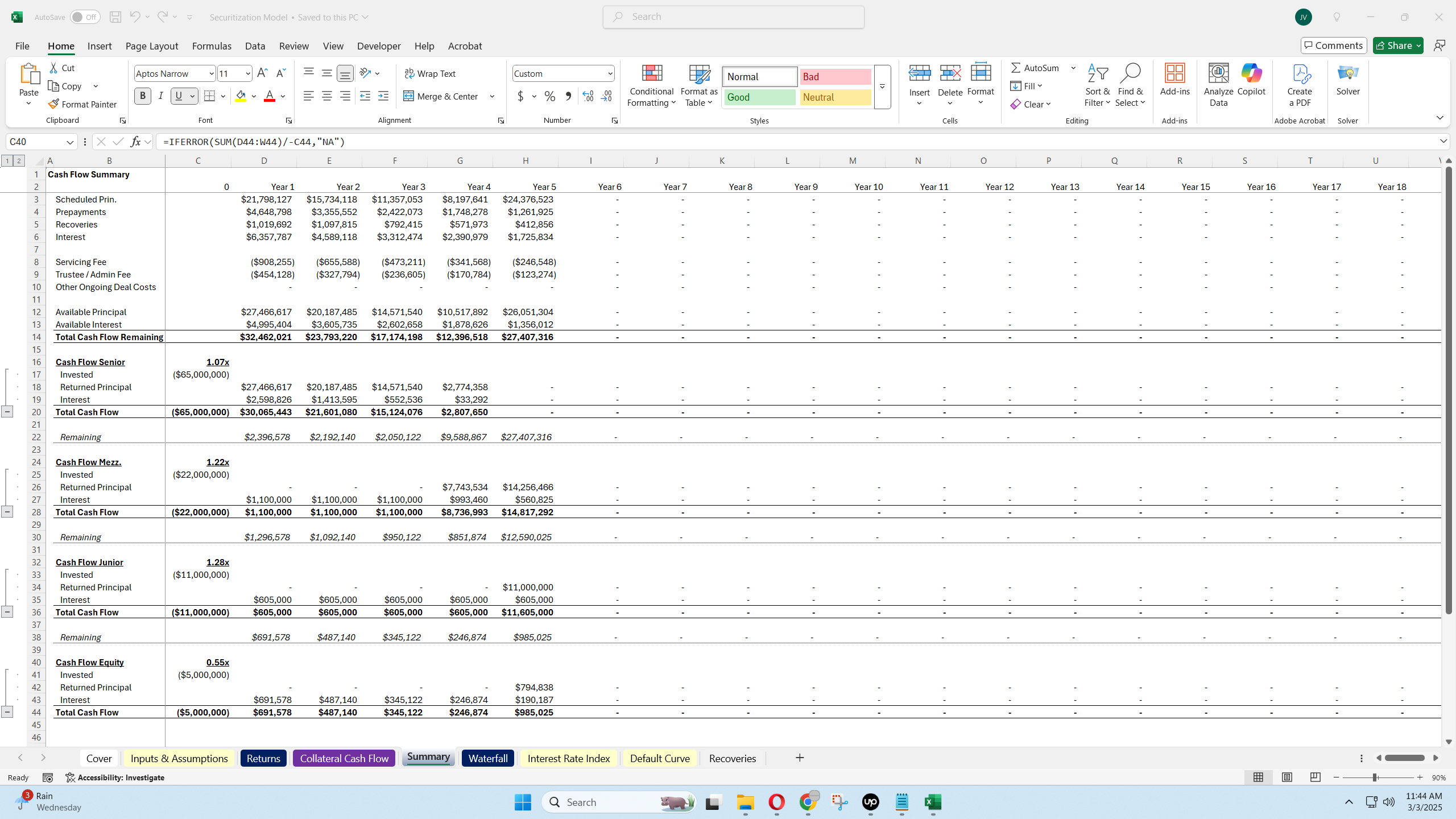

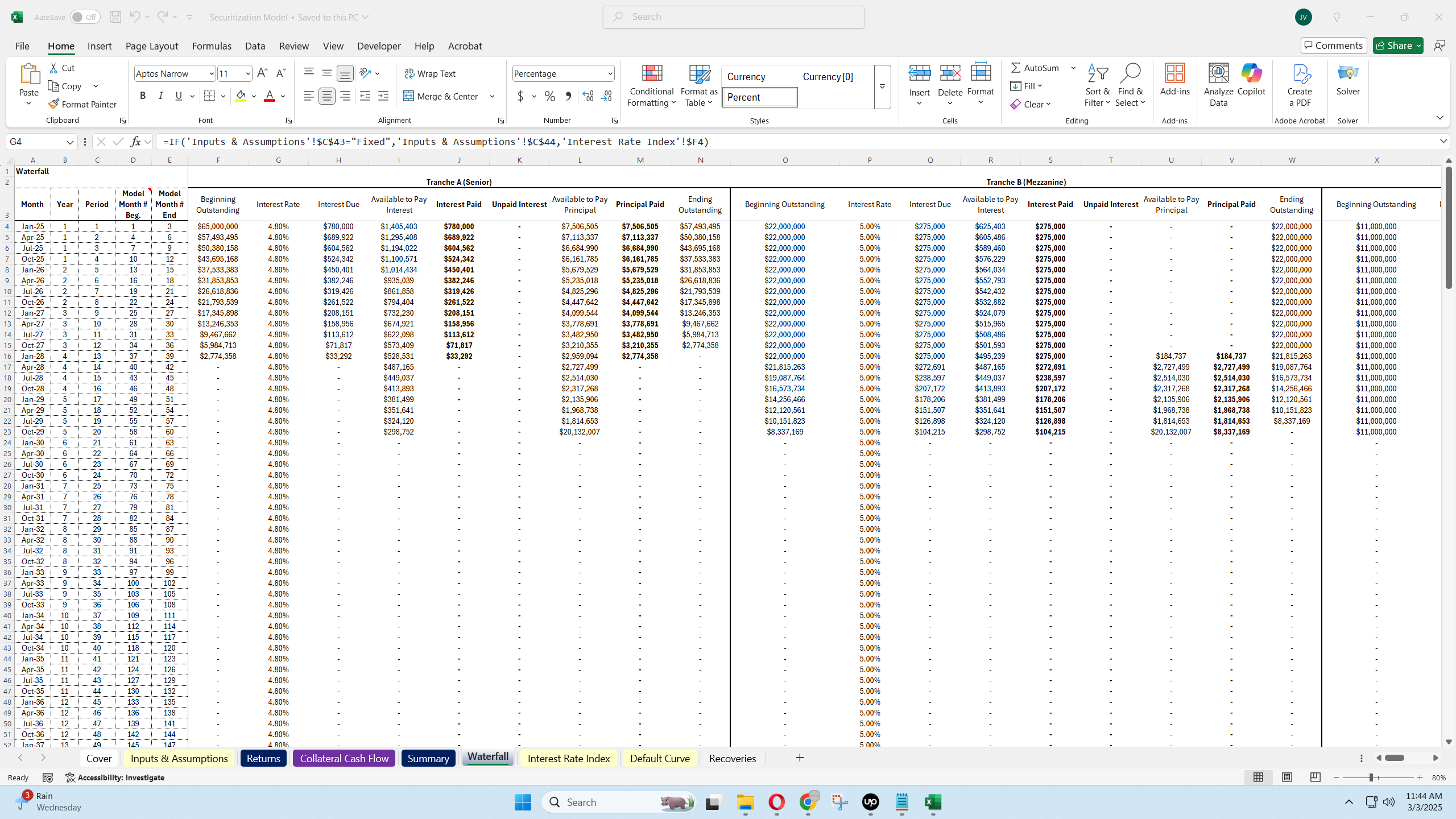

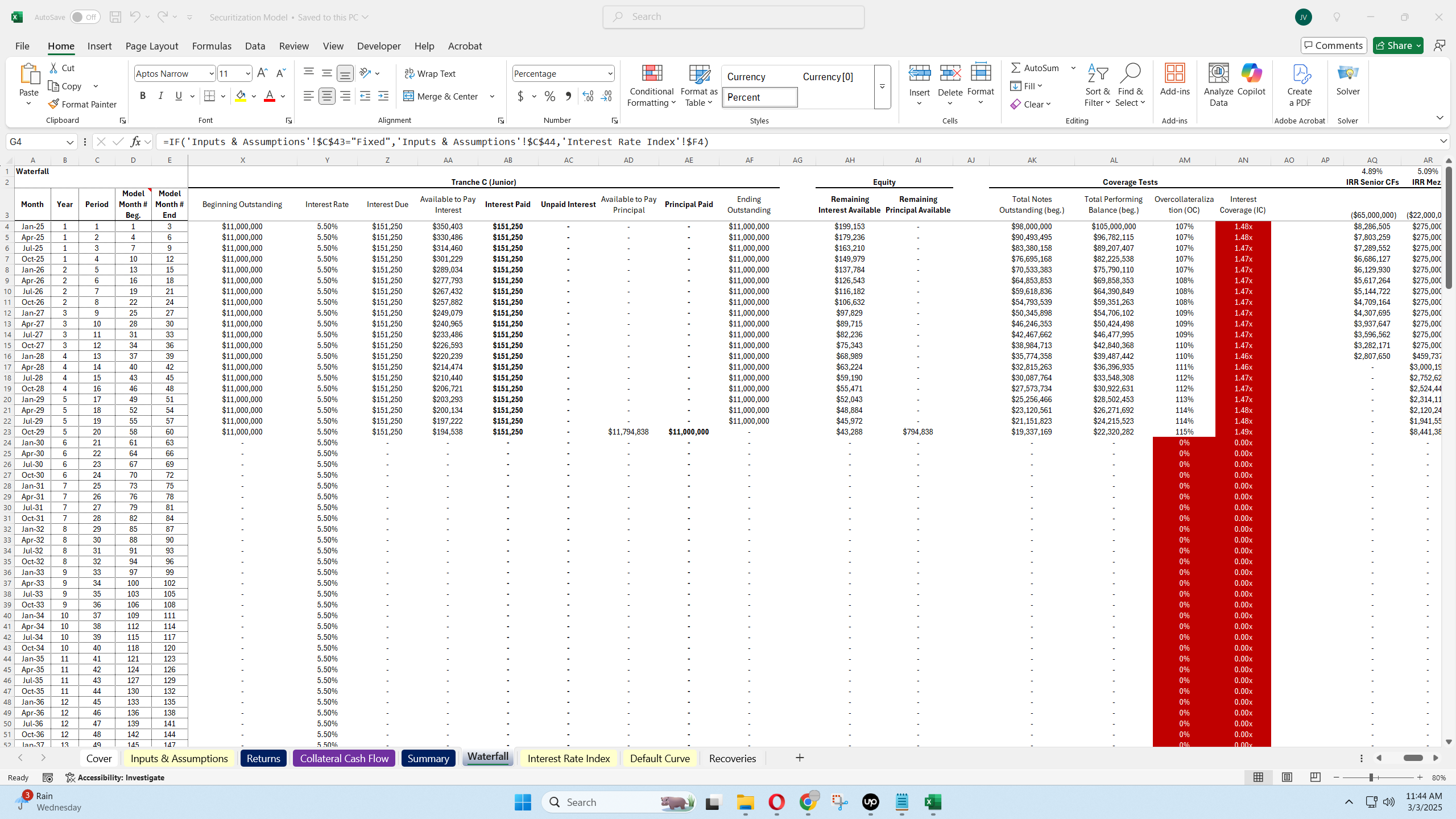

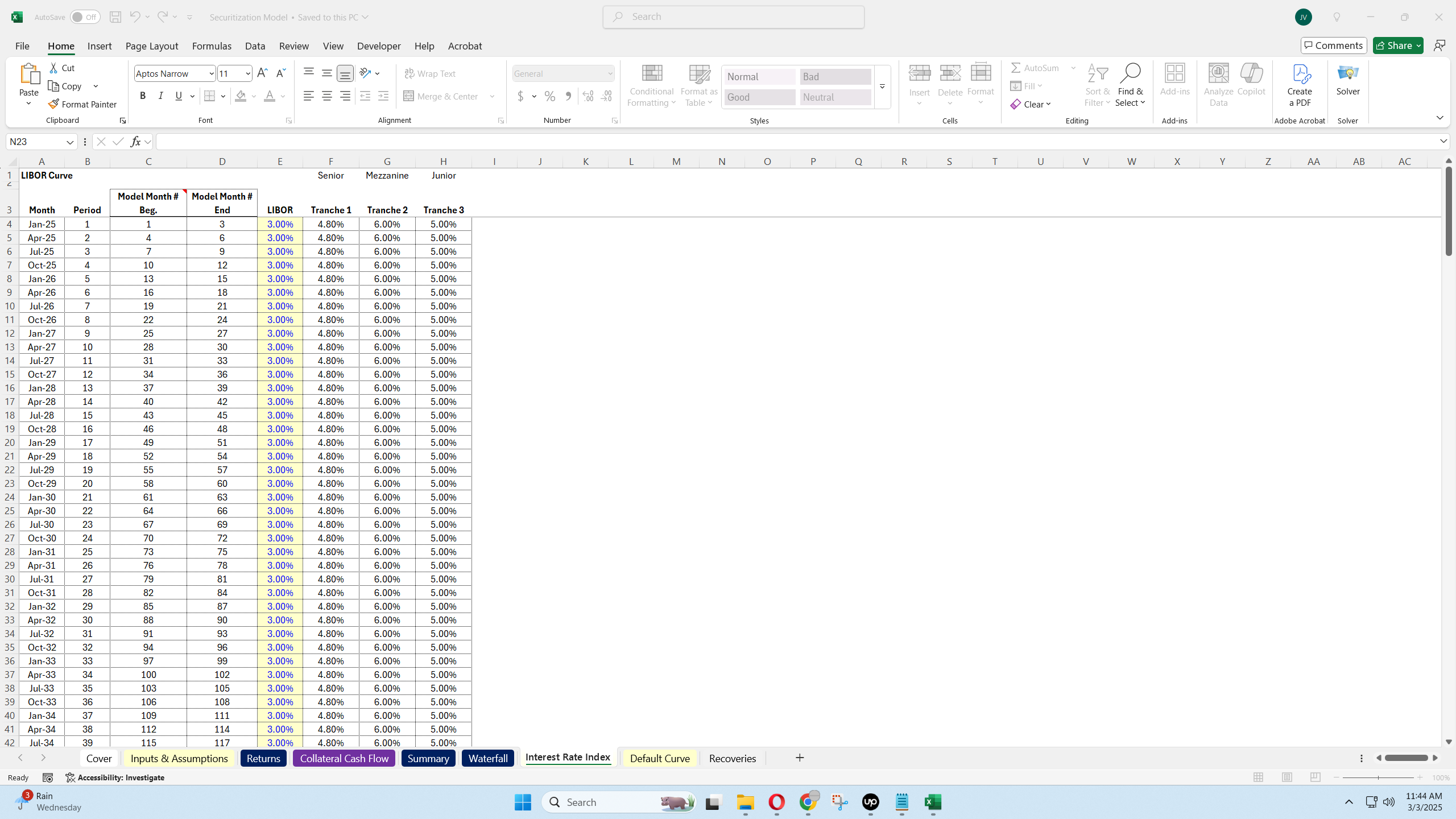

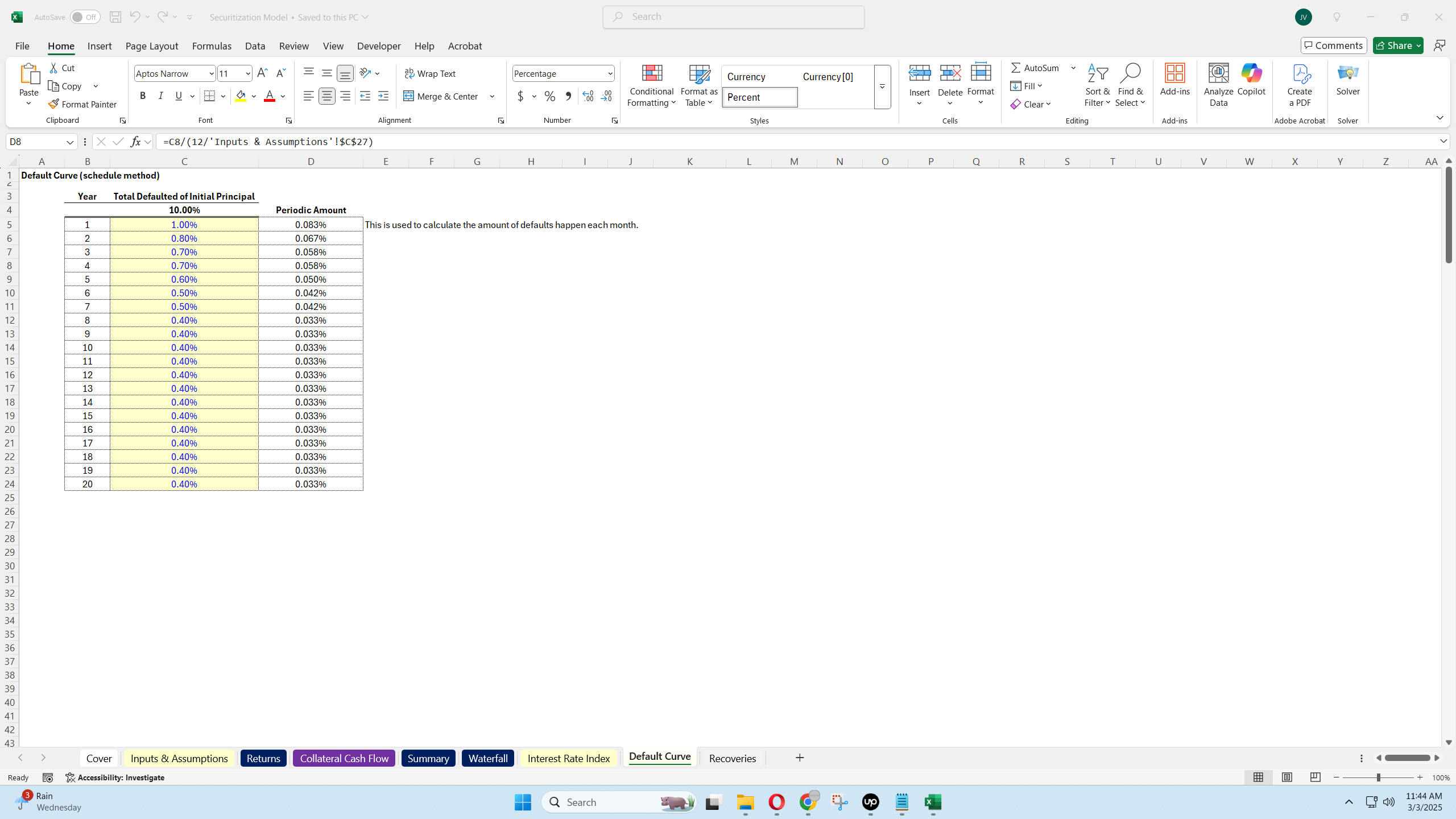

Loan Securitization Model: A Template for Multi-Tranche Structures, Coverage Metrics, and Sensitivity Analysis

A tool used to analyze loan securitization offerings from the view of the notes, Special Purpose Vehicle (SPV), and equity leg if applicable.

Further information

Analyze the performance of a basket of loans against notes, based on varying assumptions.

This works best when the loan pool is for loans with fairly similar attributes, but weighted averages can be used.