Originally published: 30/07/2020 08:57

Publication number: ELQ-58264-1

View all versions & Certificate

Publication number: ELQ-58264-1

View all versions & Certificate

Collateralized Mortgage Obligations Model

Presents a simple model where mortgage backed securities are used as a collateral.

cmocollateralmortgage backed securitiespassthrough securitiesexcelfinancial modelfinancial modelinginternal rate of return

Description

Collateralized Mortgage Obligations Model presents a simple model where mortgage backed securities are used as a collateral. Mortgages are pooled and interests in these pools are sold to investors in classes, or tranches. Bondholders buy into these tranches and receive cash flows. The payments are prioritized according to their class. Some bondholders receive cash flows automatically while others choose to defer cash flows based upon a future higher return or some other greater return. Deferring the payments may yield a greater return but this is in exchange for a greater risk taken by the tranches holders.

So, a quick overview of the model, in the contents tab you can see the structure of the model and by clicking on any of the headlines to be redirected to the relevant worksheet.

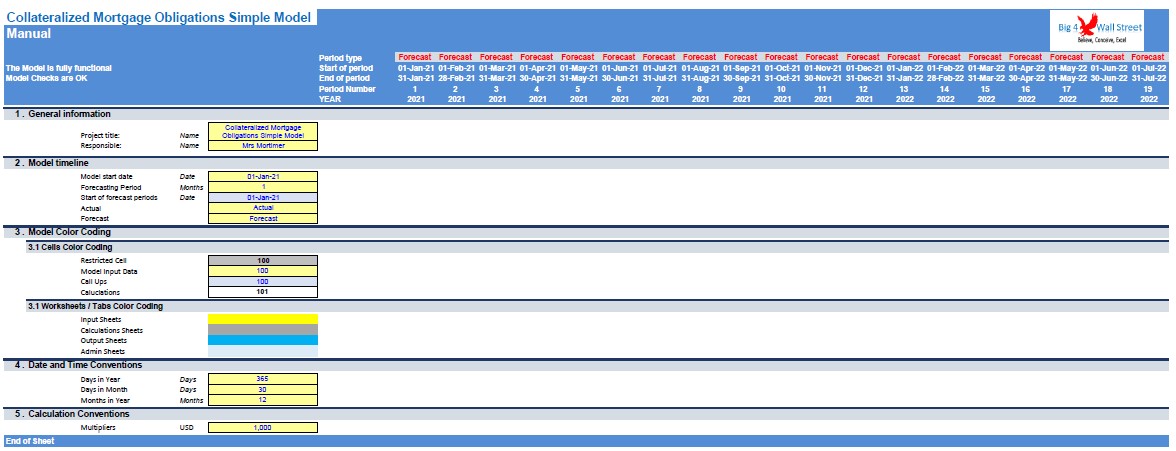

On the manual tab you can feed the general information for the model such as: model name, responsible, timeline of the model and date and currency conventions.

Additionally there is a description of the color coding of the model in the same tab. Inputs are always depicted with a yellow fill and blue letters, call up (that is direct links from other cells) are filled in light blue with blue letters while calculations are depicted with white fill and black characters.

There is also a color coding for the various tabs of the model. Yellow tabs are mostly assumptions tabs, grey tabs are calculations tabs, blue tabs are outputs tabs (that is effectively results or graphs) and finally light blue tabs are admin tabs (for example: the cover page, contents and checks).

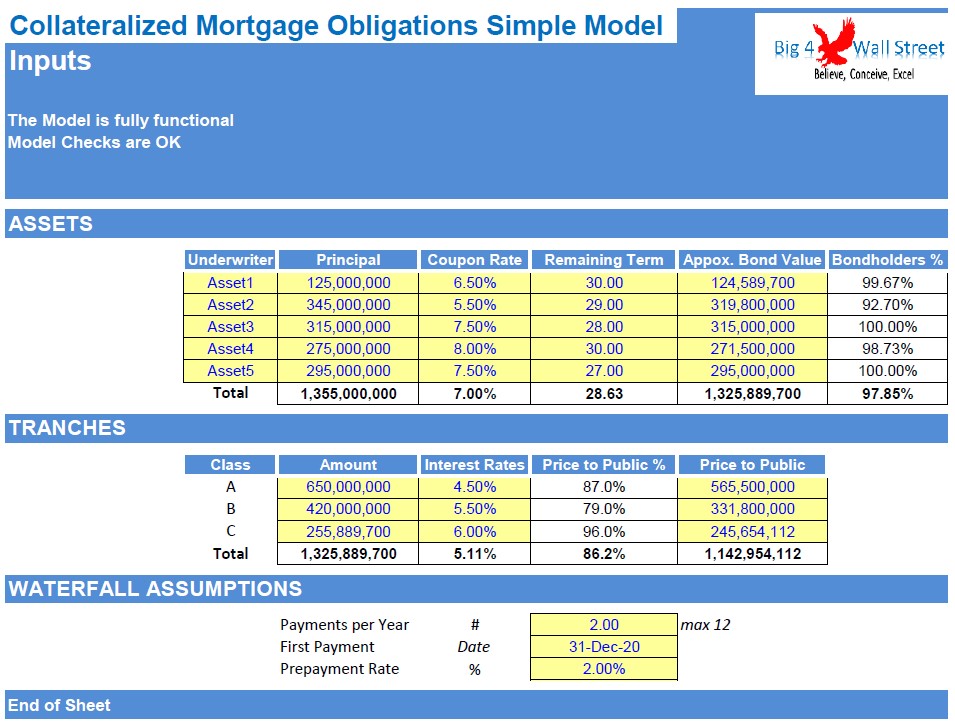

Moving on to the inputs tab, you can adjust the various assumptions of the model based on the specifications and requirements of your business (in yellow whatever can be amended as an assumption): mortgages assets principal, coupon rates and remaining term. You can also set the amount of the tranches (just make sure this is equal to the approximate bond value of the bonds), the interest rates of each tranche, and the price to public.

Furthermore, you can also adjust the payments per year of the tranches (maximum 12), when the first tranche payment is made, as well as the prepayment rate.

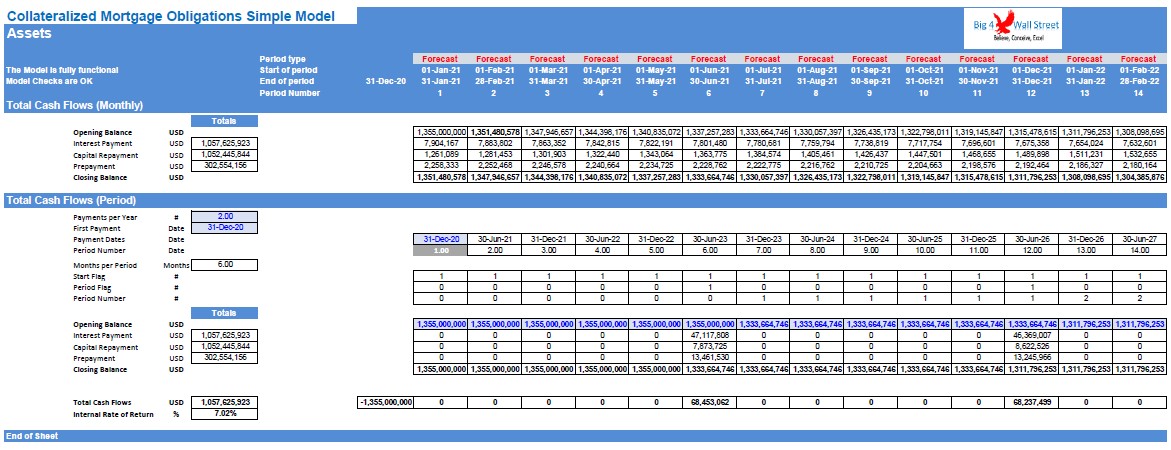

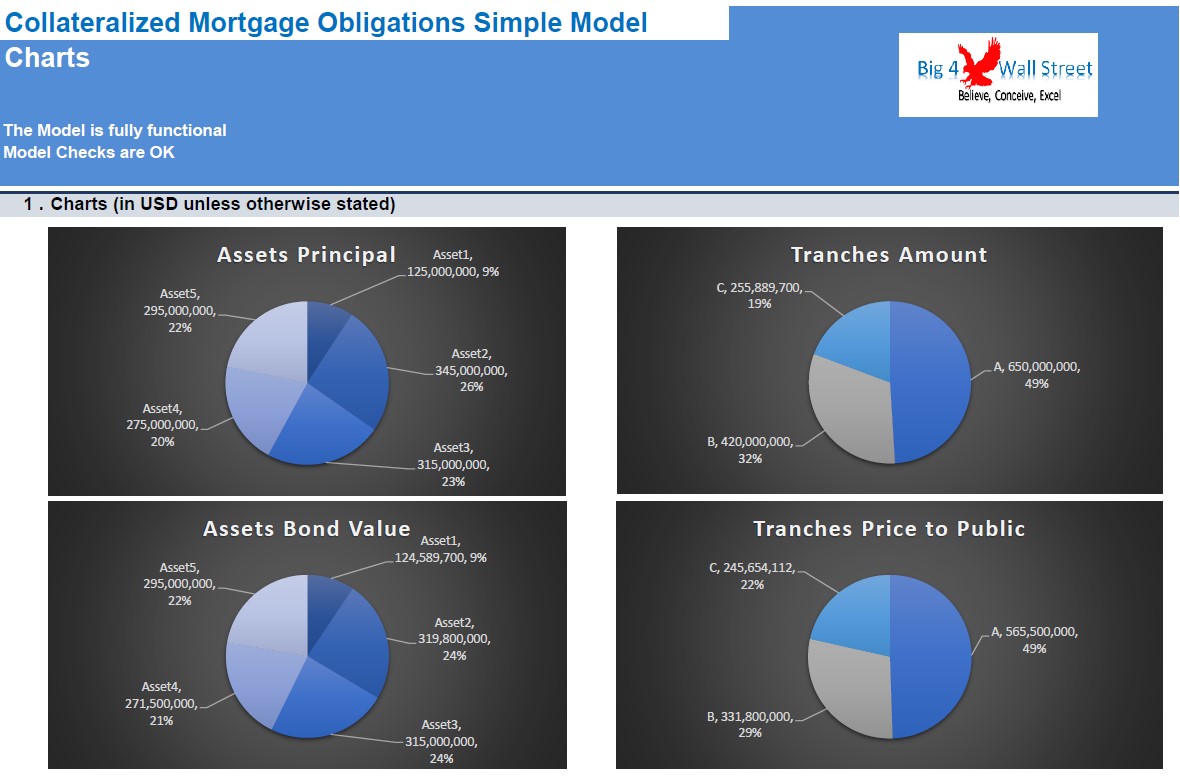

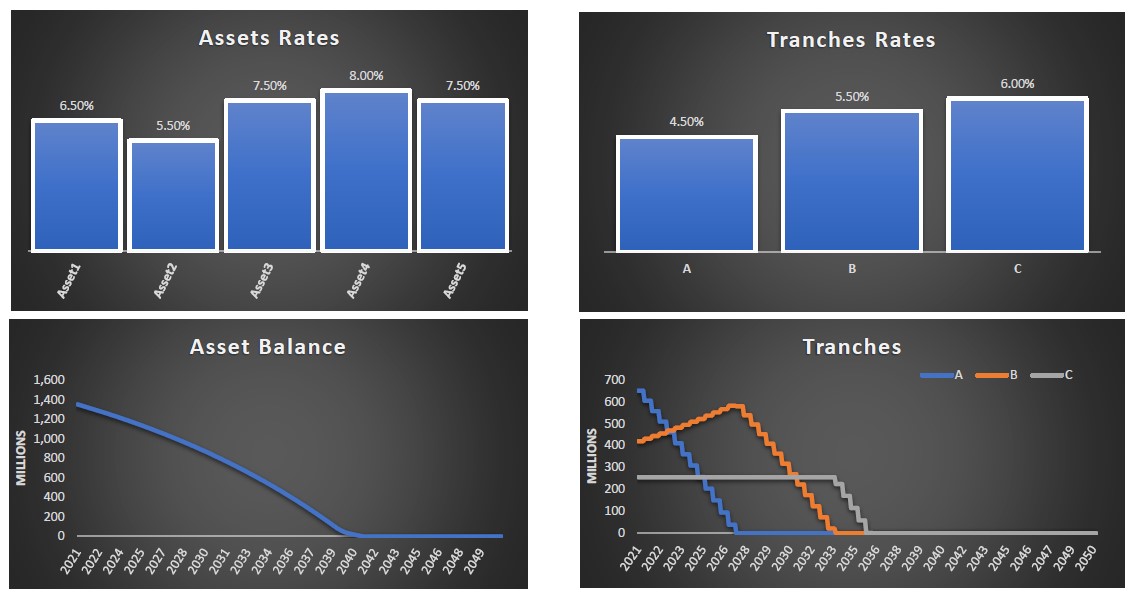

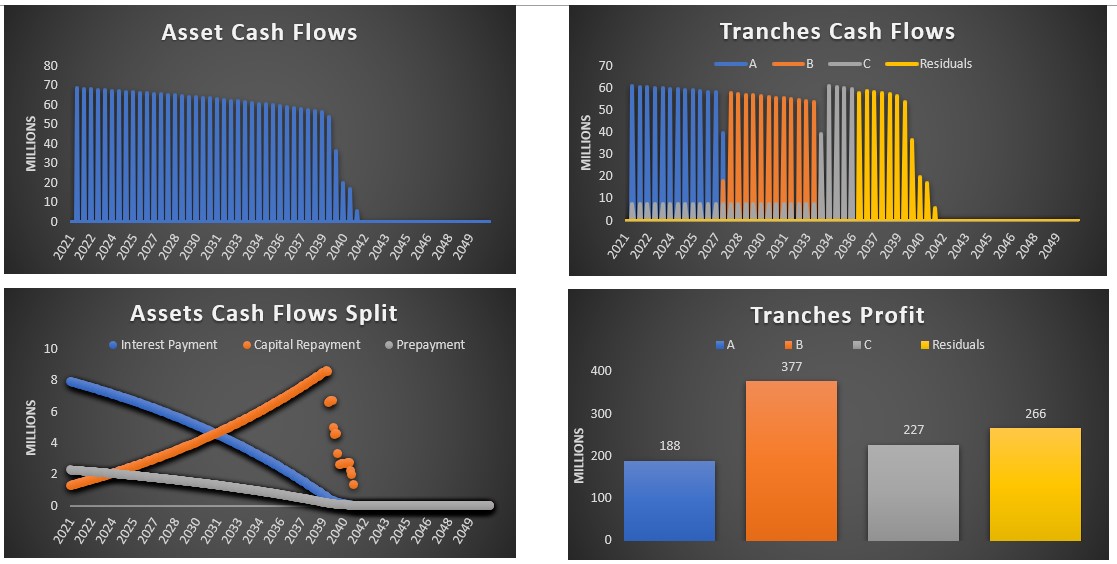

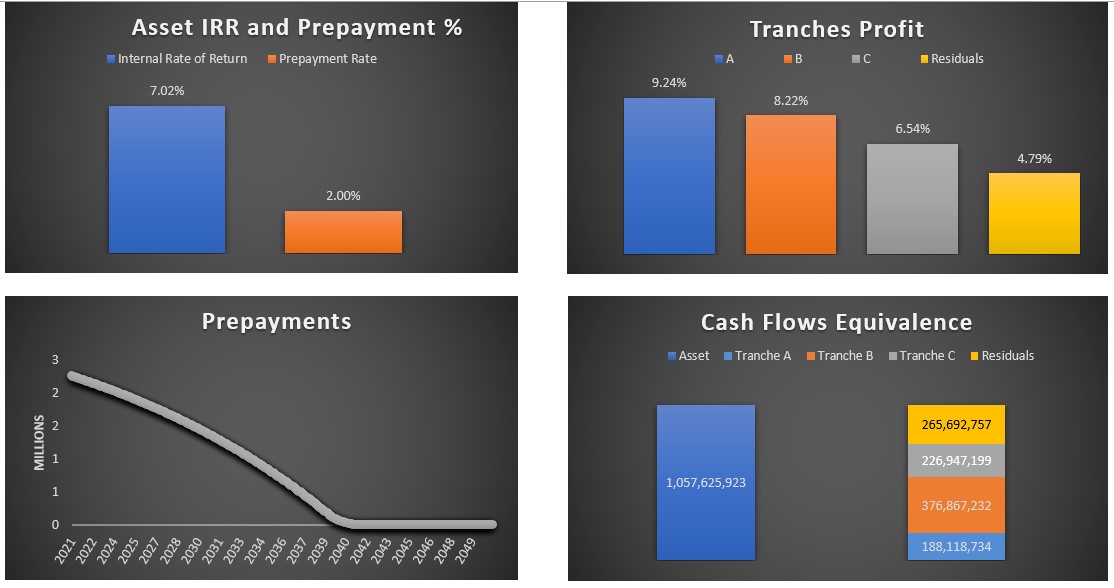

Additionally on the charts tab, a series of charts are presented: assets principals and bond values, tranches amount and price to public, assets and tranches interest rates, asset and tranches balances, cash flows, asset cash flows split, tranches profit and internal rate of returns, asset internal rate of returns and prepayments, and cash flow equivalence.

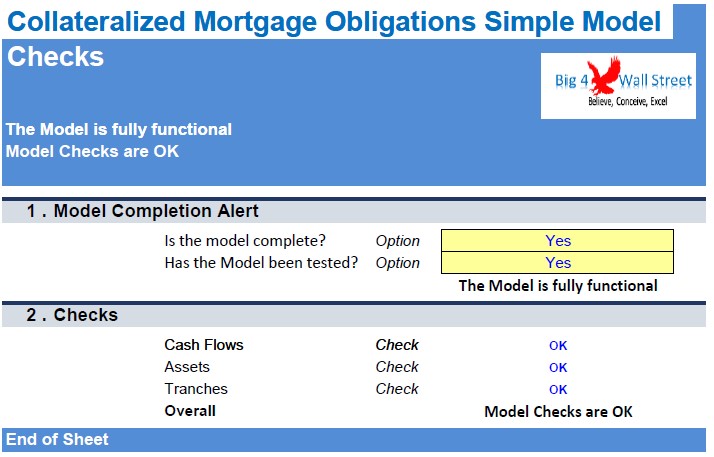

Finally the checks tab where the most critical checks are aggregated. Whenever you see an error message in any page, you should consult this page to see where the error is coming from.

Collateralized Mortgage Obligations Model presents a simple model where mortgage backed securities are used as a collateral. Mortgages are pooled and interests in these pools are sold to investors in classes, or tranches. Bondholders buy into these tranches and receive cash flows. The payments are prioritized according to their class. Some bondholders receive cash flows automatically while others choose to defer cash flows based upon a future higher return or some other greater return. Deferring the payments may yield a greater return but this is in exchange for a greater risk taken by the tranches holders.

So, a quick overview of the model, in the contents tab you can see the structure of the model and by clicking on any of the headlines to be redirected to the relevant worksheet.

On the manual tab you can feed the general information for the model such as: model name, responsible, timeline of the model and date and currency conventions.

Additionally there is a description of the color coding of the model in the same tab. Inputs are always depicted with a yellow fill and blue letters, call up (that is direct links from other cells) are filled in light blue with blue letters while calculations are depicted with white fill and black characters.

There is also a color coding for the various tabs of the model. Yellow tabs are mostly assumptions tabs, grey tabs are calculations tabs, blue tabs are outputs tabs (that is effectively results or graphs) and finally light blue tabs are admin tabs (for example: the cover page, contents and checks).

Moving on to the inputs tab, you can adjust the various assumptions of the model based on the specifications and requirements of your business (in yellow whatever can be amended as an assumption): mortgages assets principal, coupon rates and remaining term. You can also set the amount of the tranches (just make sure this is equal to the approximate bond value of the bonds), the interest rates of each tranche, and the price to public.

Furthermore, you can also adjust the payments per year of the tranches (maximum 12), when the first tranche payment is made, as well as the prepayment rate.

Additionally on the charts tab, a series of charts are presented: assets principals and bond values, tranches amount and price to public, assets and tranches interest rates, asset and tranches balances, cash flows, asset cash flows split, tranches profit and internal rate of returns, asset internal rate of returns and prepayments, and cash flow equivalence.

Finally the checks tab where the most critical checks are aggregated. Whenever you see an error message in any page, you should consult this page to see where the error is coming from.

This Best Practice includes

1 Excel and 1 PDF