Originally published: 09/03/2026 08:45

Publication number: ELQ-41516-1

View all versions & Certificate

Publication number: ELQ-41516-1

View all versions & Certificate

Options Pricing Calculator

Price any stock option instantly. Black-Scholes (European) & Binomial CRR (American) models with full Greeks, scenarios, & exercise strategy. Just enter ticker.

Description

Stop guessing what an option is worth.This professional Excel template prices any call or put option on any stock in the Yahoo Finance universe - instantly. Just enter the ticker symbol, current price, and contract details. The spreadsheet does the rest.

Two industry-standard models. One spreadsheet. Zero VBA required.

What's Inside — 4 Fully Linked Sheets

Sheet 1: Market Data & Inputs Enter your Yahoo Finance ticker, stock price, volatility, dividend yield, risk-free rate, strike, and expiration date. Every other cell in the workbook updates automatically. Blue cells are inputs. Black cells are formulas. Days-to-expiration and time-to-expiry calculate themselves.

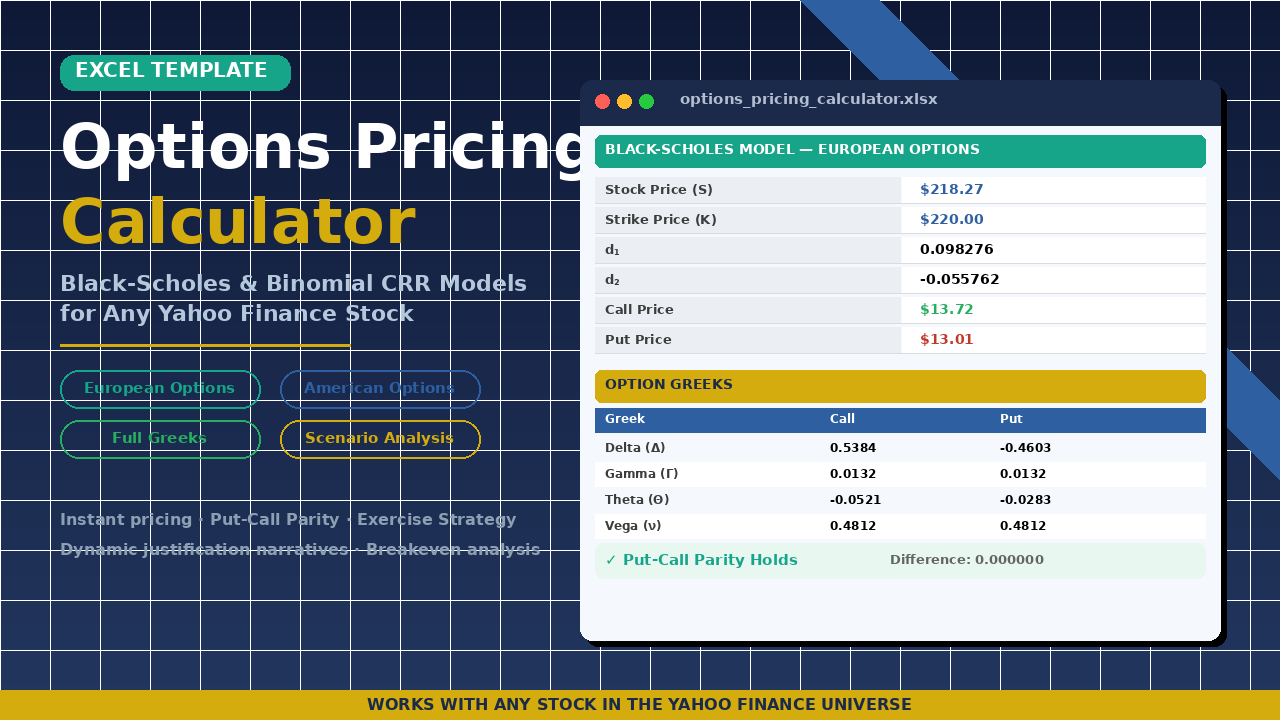

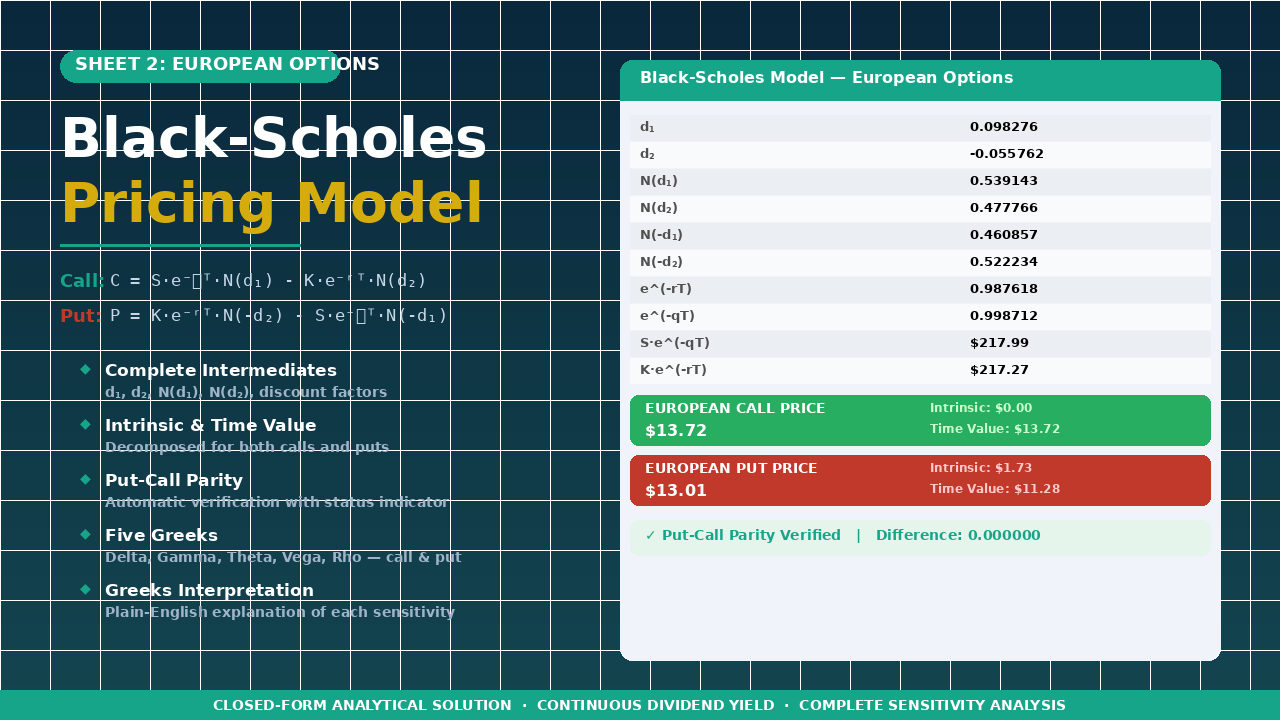

Sheet 2: European Options (Black-Scholes) The closed-form analytical solution with full transparency - every intermediate value is exposed: d₁, d₂, N(d₁), N(d₂), discount factors, and dividend adjustments. Call and put prices with intrinsic vs. time value decomposition. Automatic put-call parity verification. Complete Greeks table: Delta, Gamma, Theta, Vega, and Rho for both calls and puts, with plain-English interpretations.

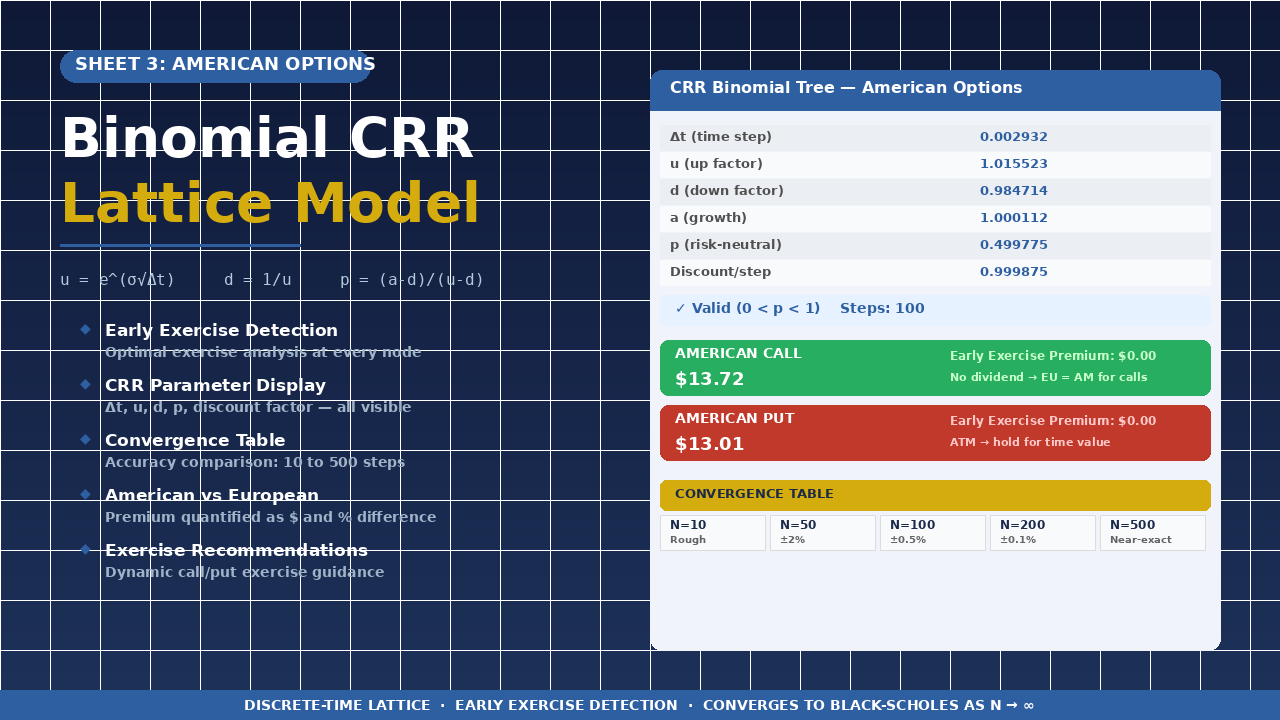

Sheet 3: American Options (Binomial CRR) The Cox-Ross-Rubinstein discrete-time lattice model with early exercise analysis. See every CRR parameter (Δt, u, d, p, discount factor), the early exercise premium quantified in both dollars and percentage, a convergence table showing accuracy from 10 to 500 steps, and dynamic exercise recommendations that tell you when early exercise makes sense - and when it doesn't.

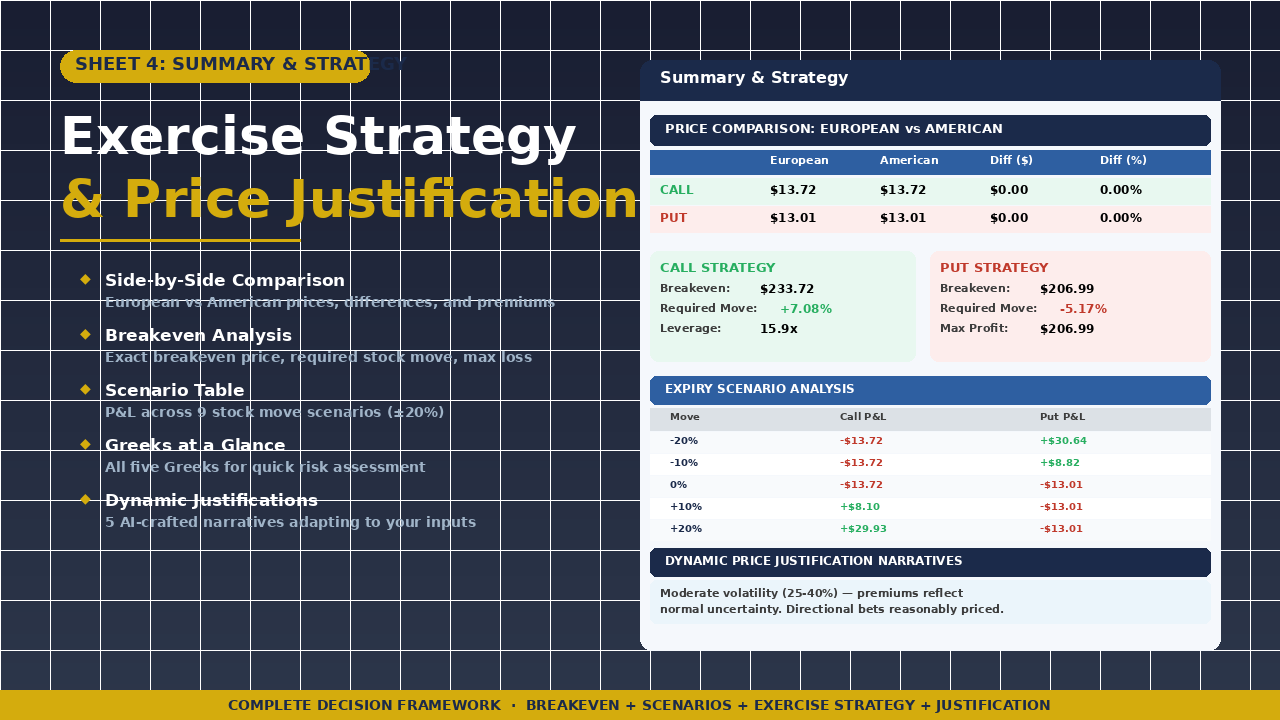

Sheet 4: Summary & Exercise Strategy The decision-making sheet. Side-by-side European vs. American price comparison. Breakeven analysis for calls and puts (exact price + required stock move). A 9-scenario P&L table spanning ±20% moves. Greeks at a glance. And five dynamic justification narratives that adapt to your specific inputs - covering volatility impact, time value, moneyness, European vs. American trade-offs, and an overall assessment. These narratives change automatically as you update inputs.

Key Features

Stop guessing what an option is worth.This professional Excel template prices any call or put option on any stock in the Yahoo Finance universe - instantly. Just enter the ticker symbol, current price, and contract details. The spreadsheet does the rest.

Two industry-standard models. One spreadsheet. Zero VBA required.

What's Inside — 4 Fully Linked Sheets

Sheet 1: Market Data & Inputs Enter your Yahoo Finance ticker, stock price, volatility, dividend yield, risk-free rate, strike, and expiration date. Every other cell in the workbook updates automatically. Blue cells are inputs. Black cells are formulas. Days-to-expiration and time-to-expiry calculate themselves.

Sheet 2: European Options (Black-Scholes) The closed-form analytical solution with full transparency - every intermediate value is exposed: d₁, d₂, N(d₁), N(d₂), discount factors, and dividend adjustments. Call and put prices with intrinsic vs. time value decomposition. Automatic put-call parity verification. Complete Greeks table: Delta, Gamma, Theta, Vega, and Rho for both calls and puts, with plain-English interpretations.

Sheet 3: American Options (Binomial CRR) The Cox-Ross-Rubinstein discrete-time lattice model with early exercise analysis. See every CRR parameter (Δt, u, d, p, discount factor), the early exercise premium quantified in both dollars and percentage, a convergence table showing accuracy from 10 to 500 steps, and dynamic exercise recommendations that tell you when early exercise makes sense - and when it doesn't.

Sheet 4: Summary & Exercise Strategy The decision-making sheet. Side-by-side European vs. American price comparison. Breakeven analysis for calls and puts (exact price + required stock move). A 9-scenario P&L table spanning ±20% moves. Greeks at a glance. And five dynamic justification narratives that adapt to your specific inputs - covering volatility impact, time value, moneyness, European vs. American trade-offs, and an overall assessment. These narratives change automatically as you update inputs.

Key Features

- Works with ANY stock on Yahoo Finance - AAPL, TSLA, MSFT, GOOG, or any ticker

- Two models: Black-Scholes (European) and Binomial CRR (American)

- Full option Greeks: Delta, Gamma, Theta, Vega, Rho

- Put-call parity verification built in

- Early exercise premium quantified (American vs. European difference)

- Breakeven analysis with exact prices and required moves

- 9-scenario P&L table (±20% stock moves at expiry)

- Dynamic narrative justifications that adapt to your inputs

- Implied volatility override option

- 129 interconnected formulas - all transparent, no VBA, no macros

- Professional color-coded formatting (blue = inputs, black = formulas)

- Works in Excel, Google Sheets, and LibreOffice

- Retail traders pricing options before entering a trade

- Finance students learning Black-Scholes and binomial models

- Portfolio managers needing quick option valuations

- CFA/FRM candidates studying derivatives pricing

- Anyone who wants to understand why an option costs what it costs

- 1× Excel file (.xlsx) - 4 sheets, 129 formulas, zero errors

- Pre-loaded with AAPL as a working example

- Immediate download, works right away

This Best Practice includes

1 Excel Template