Originally published: 20/06/2016 12:26

Last version published: 25/10/2016 08:18

Publication number: ELQ-37738-3

View all versions & Certificate

Last version published: 25/10/2016 08:18

Publication number: ELQ-37738-3

View all versions & Certificate

Estimating a beta (Corporate Finance)

Compute and estimate a beta for a firm's stock/market index

Prof. Aswath Damodaran offers you this Best Practice for free!

download for free

Add to bookmarks

Further information

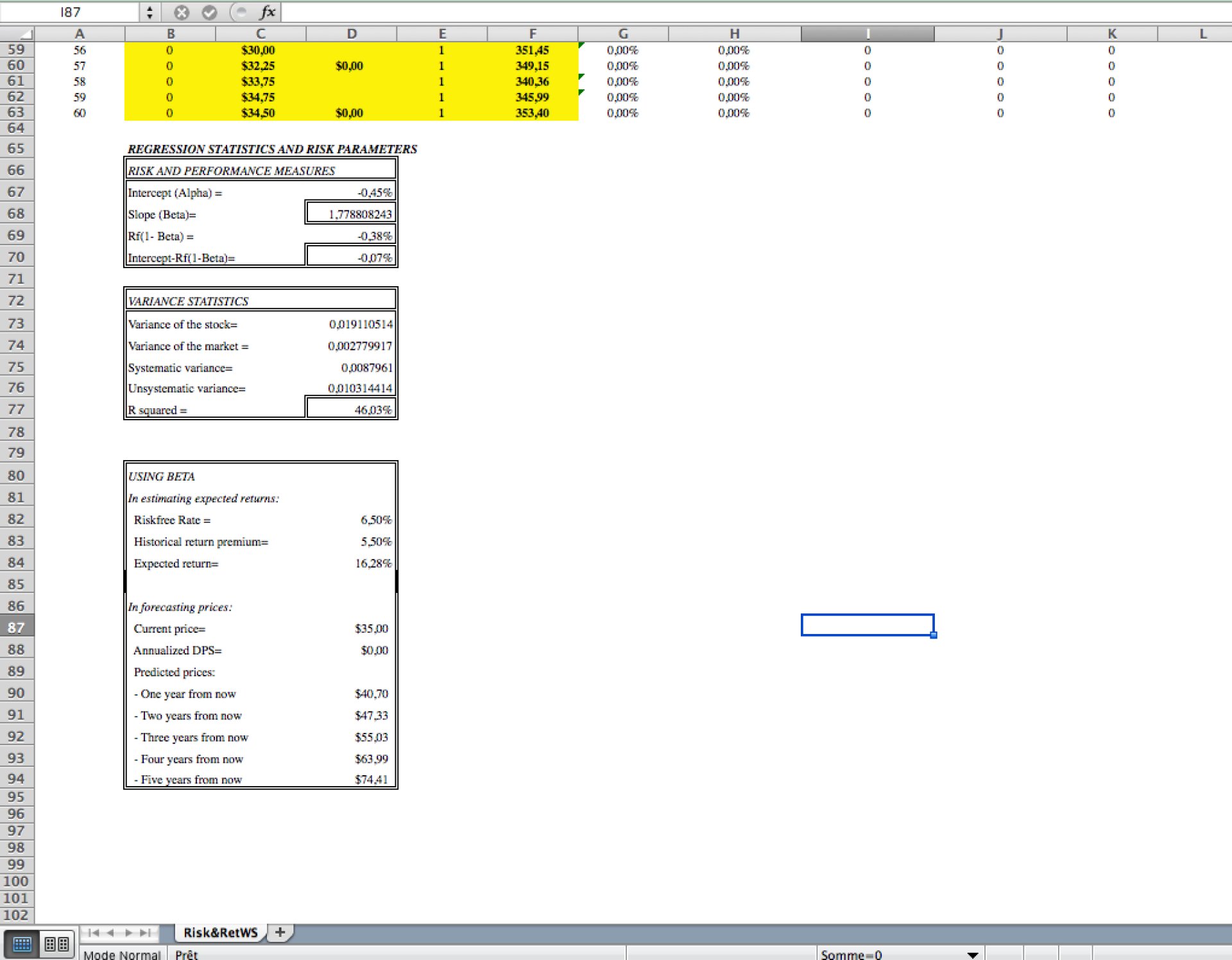

The objective of this model is to get the following output values:

to estimate expected returns:

- risk free rate

- historical return premium

- expected return

to forecast prices:

- current price

- annualized DPS

- predicted prices (one to five years from now)