Publication number: ELQ-45433-1

View all versions & Certificate

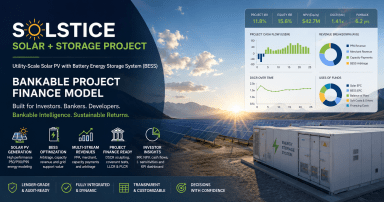

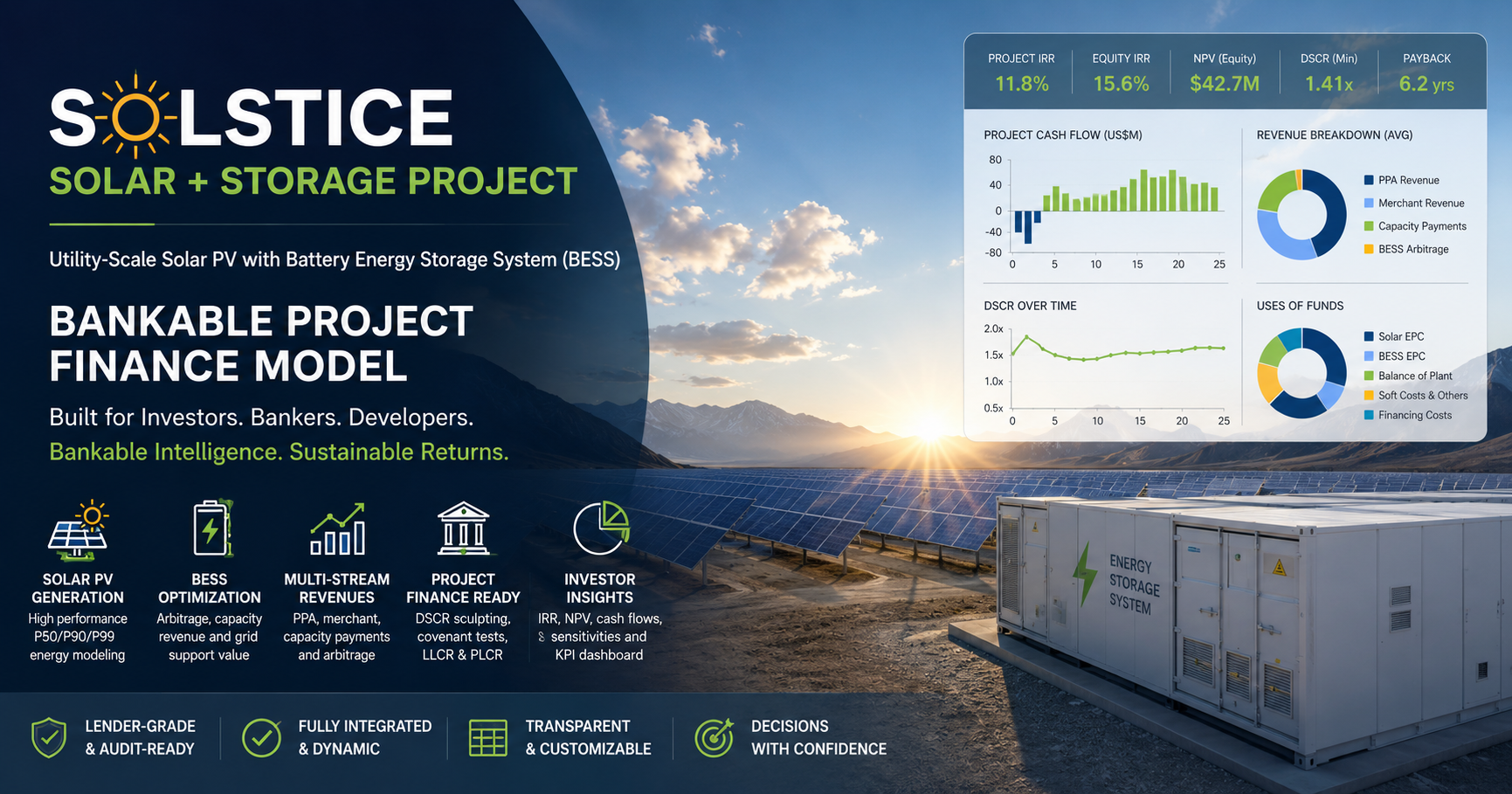

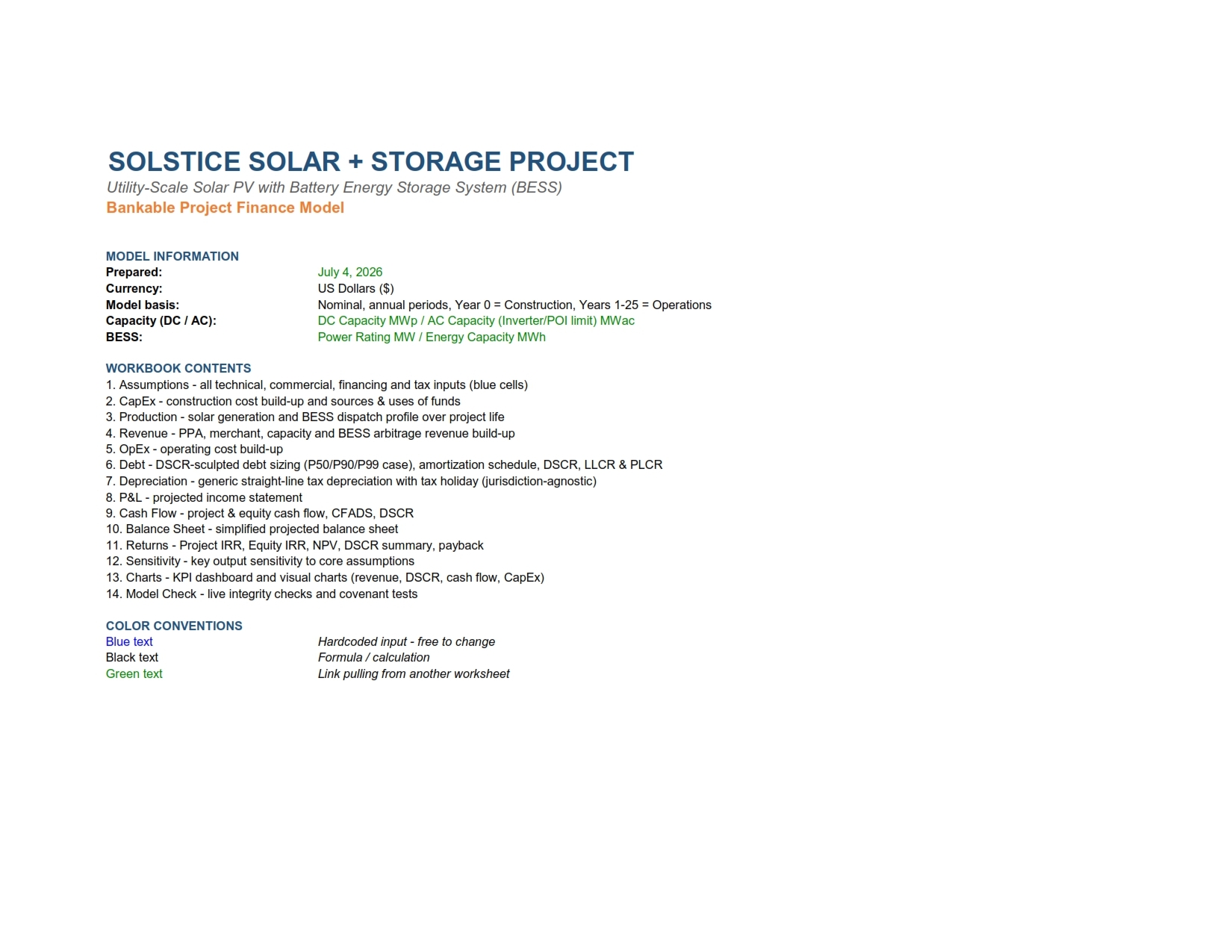

Bankable Solar + BESS Financial Model

Transforming renewable energy projects into bankable, investor-ready financial opportunities.

Further information

1. Assess Project Bankability

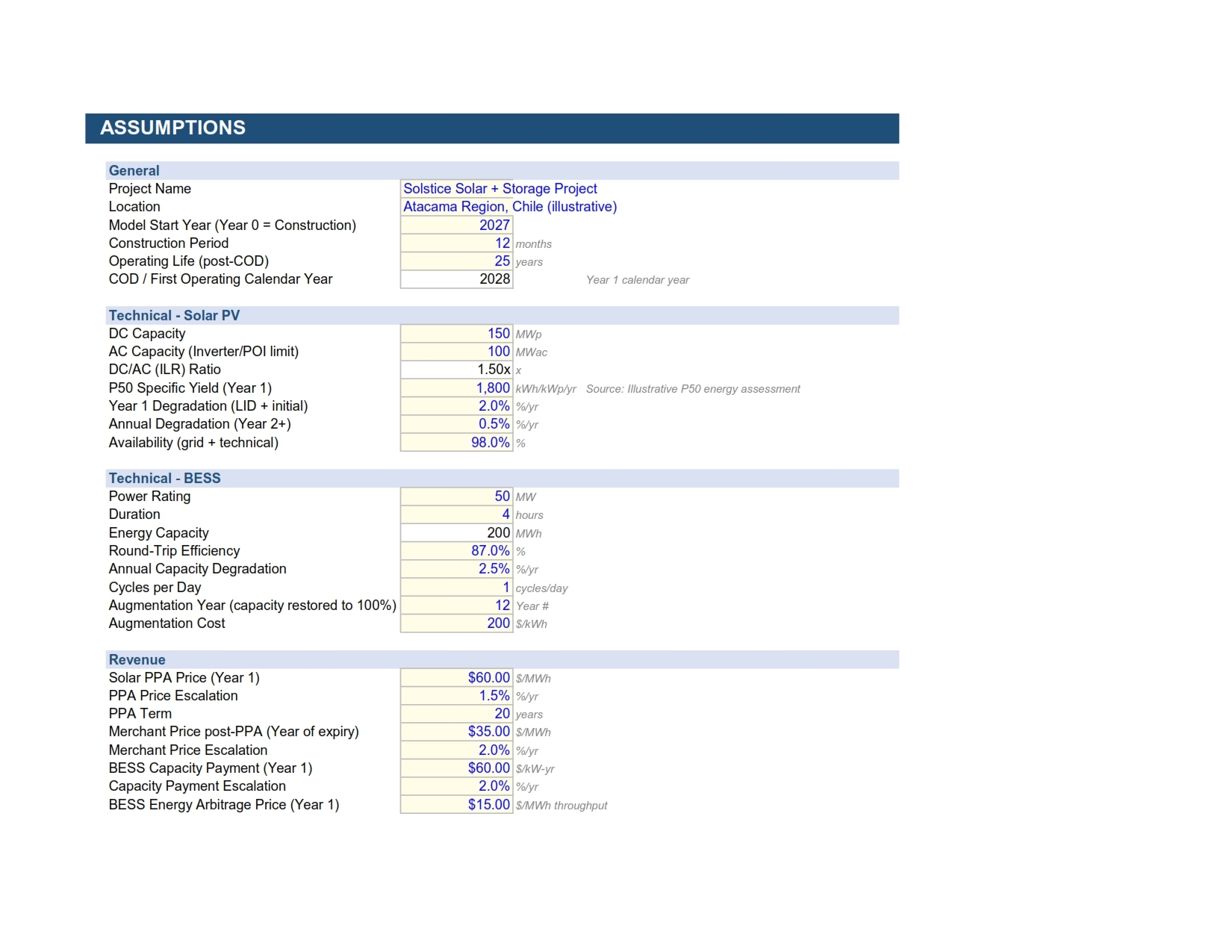

To evaluate whether the solar PV and battery energy storage project generates sufficient and predictable cash flows to satisfy lender, investor, and sponsor requirements.

2. Determine Financial Viability

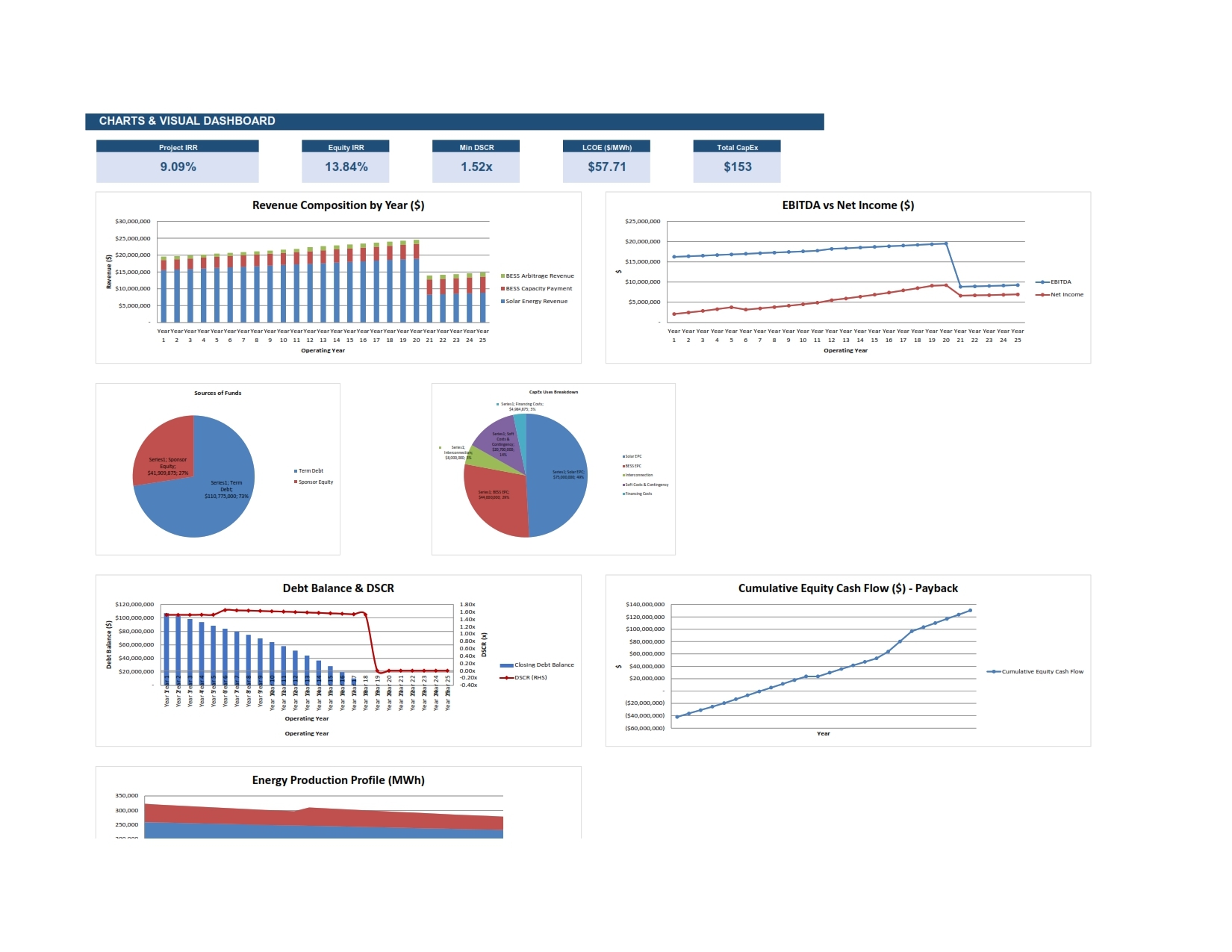

To establish the economic attractiveness of the project through key financial metrics such as IRR, NPV, payback period, and Levelized Cost of Energy (LCOE).

3. Optimize Capital Structure

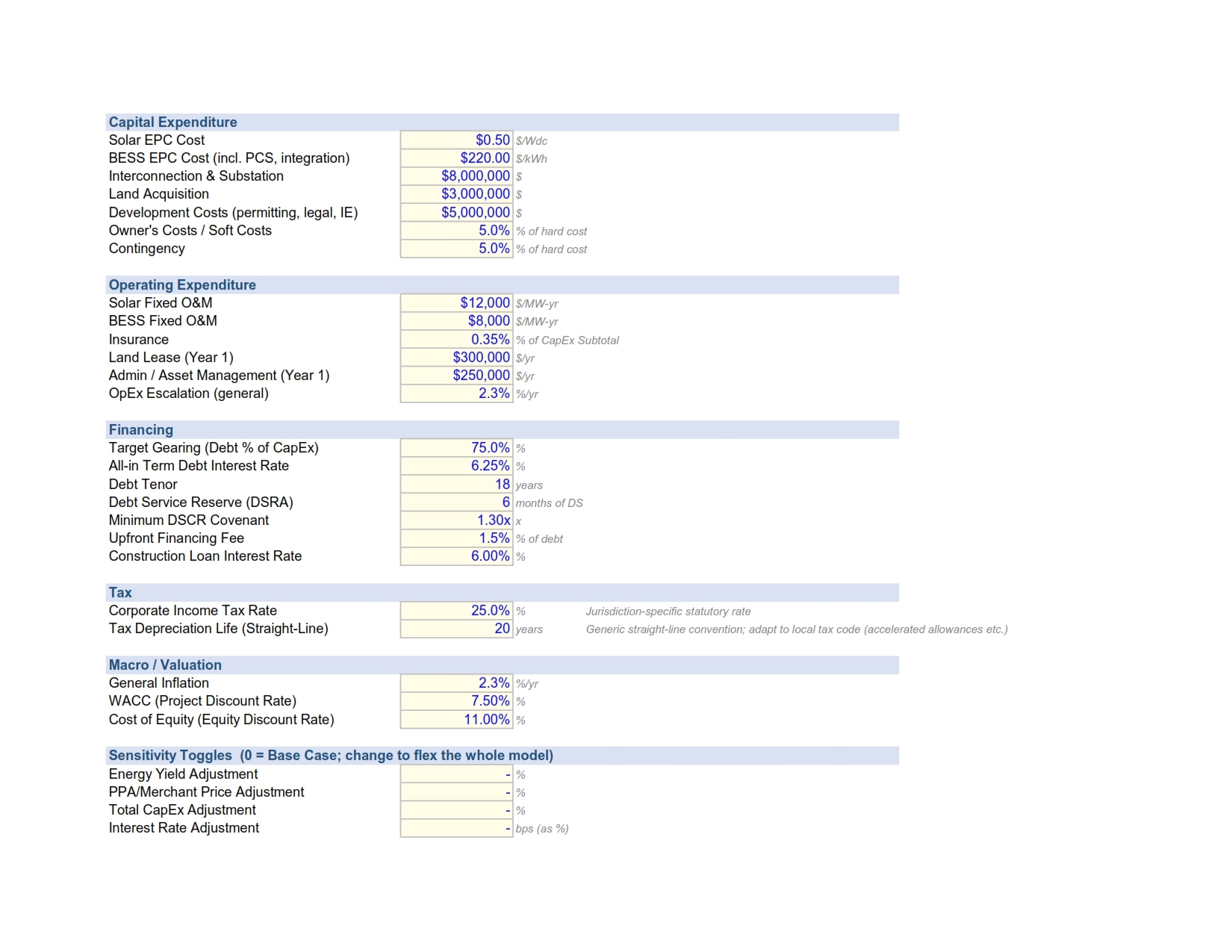

To determine the optimal debt-to-equity mix that minimizes financing costs while maintaining acceptable risk and compliance with lender covenants.

4. Evaluate Revenue Potential

To quantify projected revenues from multiple income streams including power purchase agreements (PPAs), merchant energy sales, capacity payments, and battery energy arbitrage.

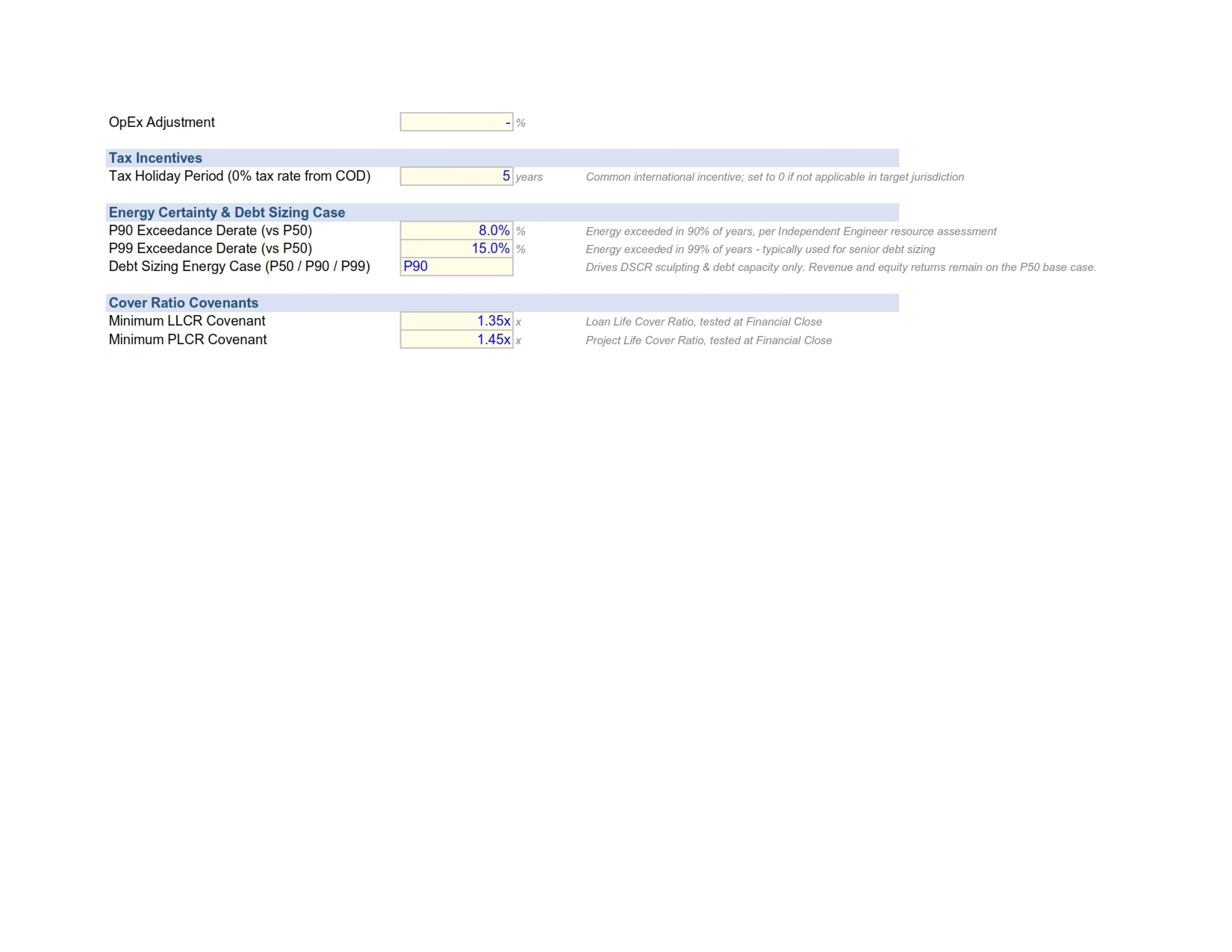

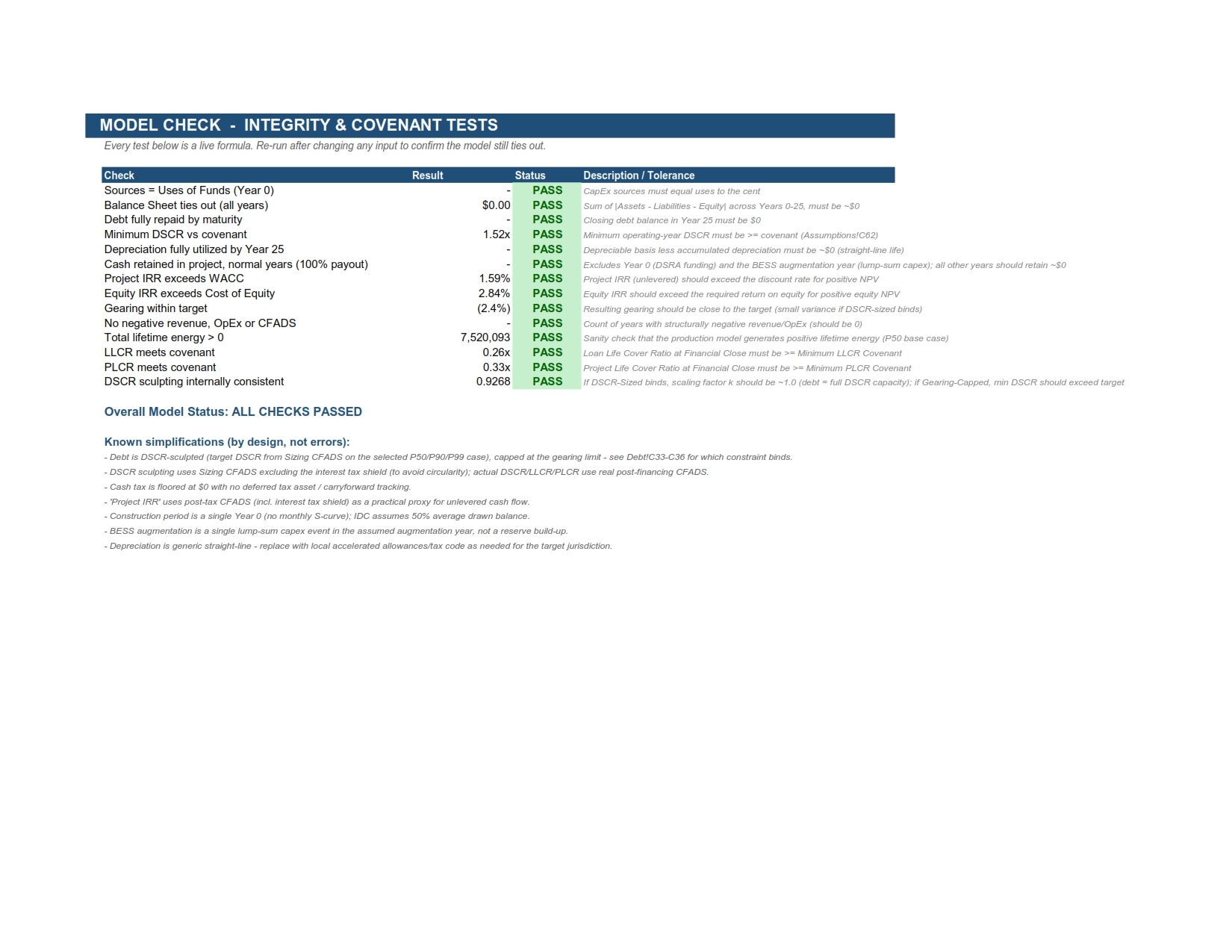

5. Analyze Debt Service Capacity

To assess the project’s ability to service debt obligations using lender-focused metrics such as DSCR, LLCR, and PLCR, ensuring sustainable debt repayment throughout the loan tenor.

6. Forecast Long-Term Cash Flows

To project annual operating cash flows over the full project lifecycle, accounting for generation degradation, operating costs, taxation, maintenance capex, and financing obligations.

7. Support Investment Decision-Making

To provide sponsors, equity investors, lenders, and strategic partners with reliable financial insights for investment appraisal and capital allocation decisions.

8. Perform Scenario and Sensitivity Analysis

To stress-test project performance against changes in key assumptions such as energy yield, tariff, capex, inflation, and interest rates, thereby quantifying downside and upside risks.

9. Facilitate Fundraising and Financial Close

To provide a transparent, auditable, and lender-ready model that supports due diligence, debt raising, investor presentations, and financial close negotiations.

10. Enhance Strategic Project Planning

To serve as a decision-support tool for optimizing project design, operational strategy, commercial structuring, and long-term value creation.

These objectives position the model not merely as a spreadsheet, but as a strategic investment decision tool for bankable renewable energy infrastructure development.

1. Utility-Scale Renewable Energy Projects

Best suited for medium to large-scale solar PV projects integrated with Battery Energy Storage Systems (BESS), typically ranging from tens to hundreds of megawatts.

2. Project Finance Transactions

Most applicable where projects are financed using non-recourse or limited-recourse project finance structures, requiring detailed lender-grade financial analysis.

3. Long-Term Revenue Visibility

Performs best where revenue streams are supported by Power Purchase Agreements (PPAs), capacity contracts, merchant markets, or ancillary service revenues with reasonably predictable pricing.

4. Debt-Financed Infrastructure Developments

Ideal for projects involving significant leverage where debt sizing, amortization sculpting, and covenant testing using DSCR, LLCR, and PLCR are critical.

5. Bankability and Due Diligence Requirements

Highly suitable for projects undergoing financial close, lender due diligence, investor fundraising, acquisition valuation, or refinancing.

6. Markets with Established Regulatory Frameworks

Most effective in jurisdictions with relatively stable energy regulation, tariff structures, taxation, and grid interconnection frameworks.

7. Projects Requiring Scenario Analysis

Particularly valuable where developers need to evaluate sensitivities around **energy yield, capex, tariff movements, inflation, interest rates, and storage performance degradation.

8. Hybrid Energy Systems with Multiple Revenue Streams

Best applied where BESS contributes value through energy shifting, peak shaving, arbitrage, reserve capacity, or ancillary grid services.

9. Medium- to Long-Term Asset Life

Designed for infrastructure assets with operating lives of 15–30 years, where lifecycle cash flow forecasting materially impacts investment decisions.

10. Institutional Investment Evaluation

Especially useful for infrastructure funds, DFIs, private equity investors, utilities, banks, and strategic energy developers requiring robust investment-grade analysis.

1. Small-Scale or Distributed Energy Projects

The model is not ideally suited for rooftop solar, mini-grids, residential storage, or small commercial installations, where project finance complexity is unnecessary.

2. Projects Without Reliable Technical Data

It is less effective where critical inputs such as resource assessments, generation profiles, degradation assumptions, or BESS dispatch data are unavailable or highly uncertain.

3. Early Concept or Pre-Feasibility Projects

Not ideal for projects still at a purely conceptual stage with undefined technology, land, grid access, or commercial arrangements.

4. Merchant-Only Projects in Highly Volatile Markets

Projects relying entirely on uncontracted merchant revenues in unstable electricity markets may require more advanced stochastic price modeling beyond the scope of this model.

5. Non-Project Finance Structures

The model is less suitable for projects funded through corporate balance sheets, grant-based financing, public-sector budgeting, or fully equity-funded structures where lender covenants are not relevant.

6. Projects with Complex Multi-Asset Portfolios

It may not adequately capture highly complex portfolio structures involving multiple generation technologies, transmission assets, or cross-border energy trading without customization.

7. Jurisdictions with Highly Specialized Tax Regimes

The model uses generalized tax logic and may not fully capture jurisdictions with complex tax incentives, accelerated depreciation, tax equity structures, or intricate withholding tax rules.

8. Markets with Unstable Regulatory Environments

Less reliable in countries experiencing frequent regulatory changes, tariff uncertainty, weak offtaker creditworthiness, or evolving grid policies.

9. Projects Requiring High-Frequency Dispatch Optimization

The model is not intended for detailed hourly or sub-hourly energy market dispatch simulations, ancillary service bidding, or advanced battery optimization algorithms.

10. Projects with Highly Customized Financing Instruments

Not ideal for structures involving mezzanine debt, convertible instruments, revenue-sharing financing, securitization, or structured derivatives unless materially adapted.

Key Limitation

This model is designed as a best-practice project finance tool, not a substitute for detailed engineering simulations, legal due diligence, or market trading models. For non-standard projects, significant customization may be required.