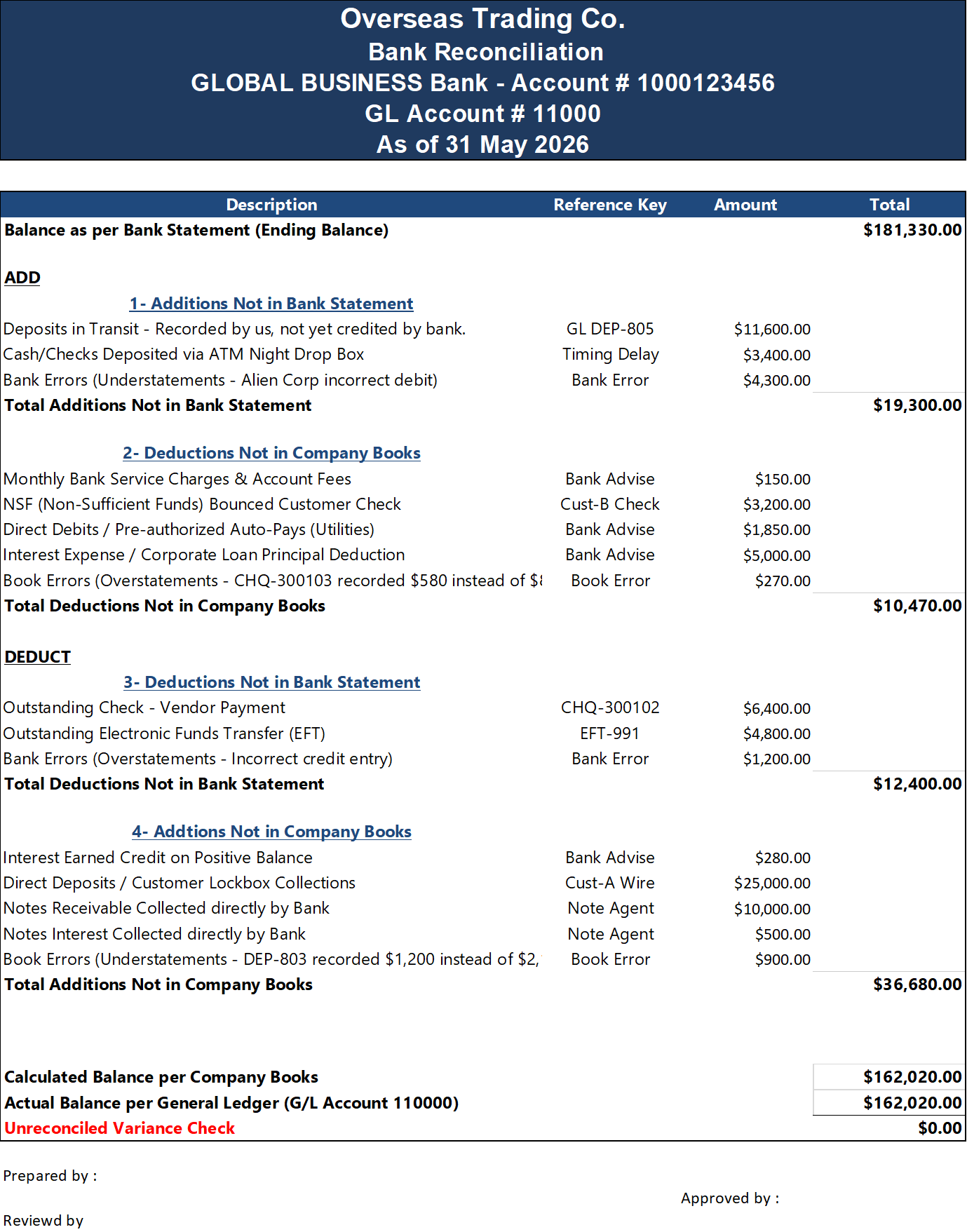

Premium 4-Quadrant Corporate Bank Reconciliation Model (Dynamic Control Template)

This is a bank account reconciliation bridging the gap between bank records and GL accounts serves as an audit control schedule.

Former Head of Treasury (CTP)| Treasury Policies, Cash Management, Liquidity & FX Risk SpecialistFollow

Further information

Stop using messy, manual bank recs that fail audit reviews. Download this Audit-Ready, Corporate-Grade Bank Reconciliation Model. Built on an advanced 4-Quadrant linear bridging formula, it automates your month-end close and delivers an instantaneous zero-variance proof between your bank statement and general ledger."

When you need to have a comprehensive list of all possible reconciling items between bank and books balances listed in a very simple and smart way and serves as audit control schedule.

Cannot be used as a final Month-end reconciliation