Originally published: 15/11/2024 11:21

Publication number: ELQ-17682-1

View all versions & Certificate

Publication number: ELQ-17682-1

View all versions & Certificate

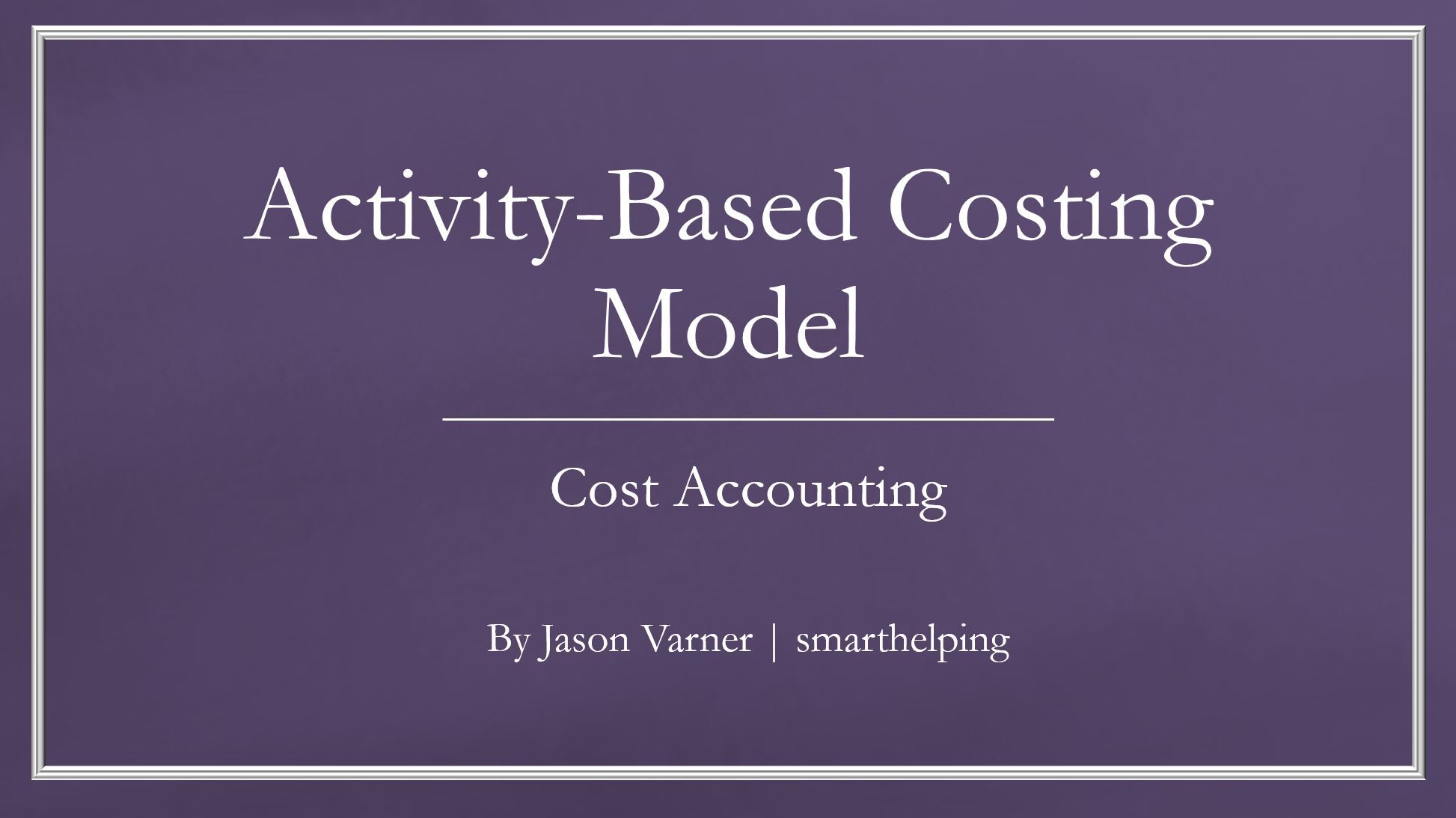

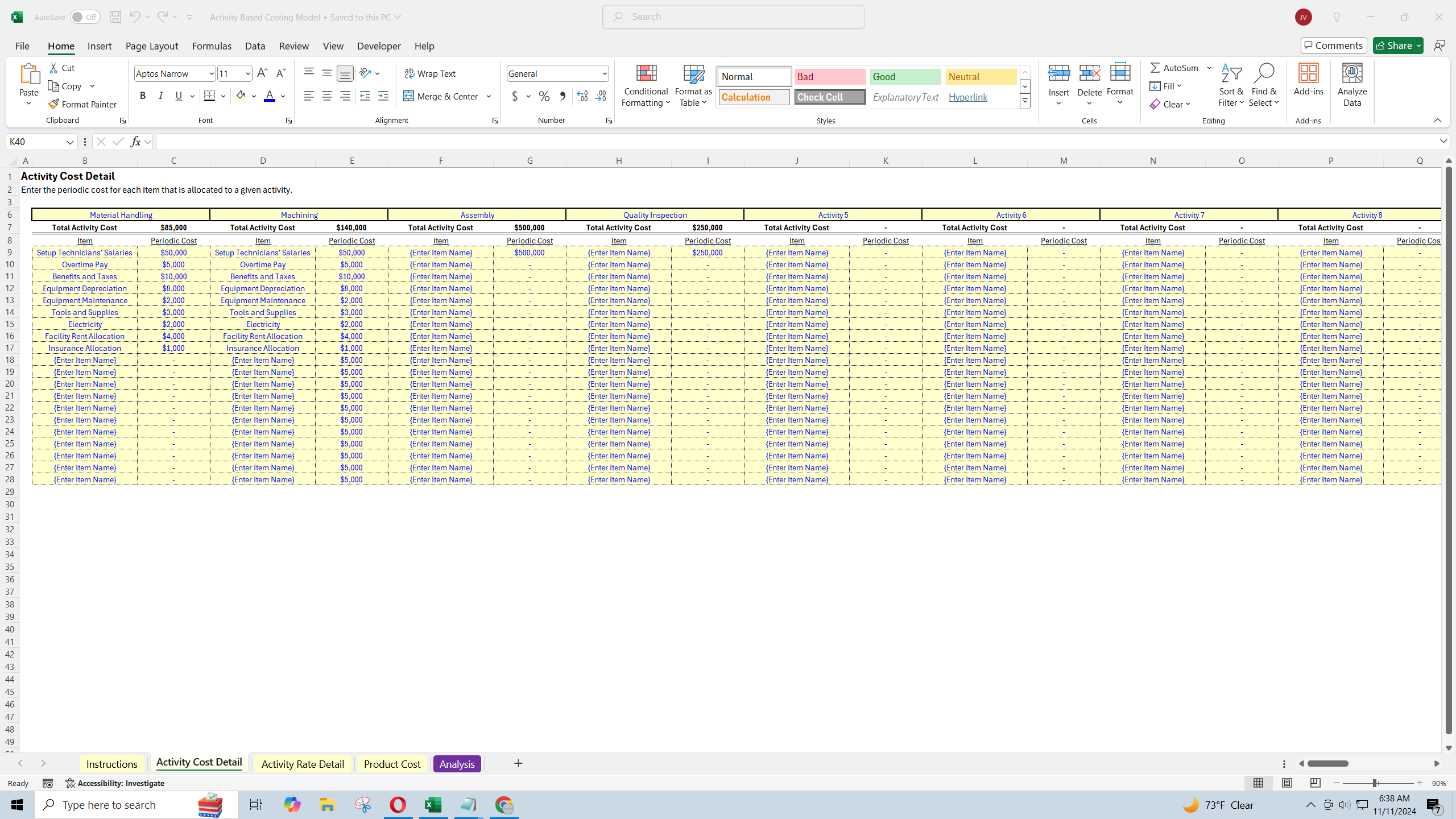

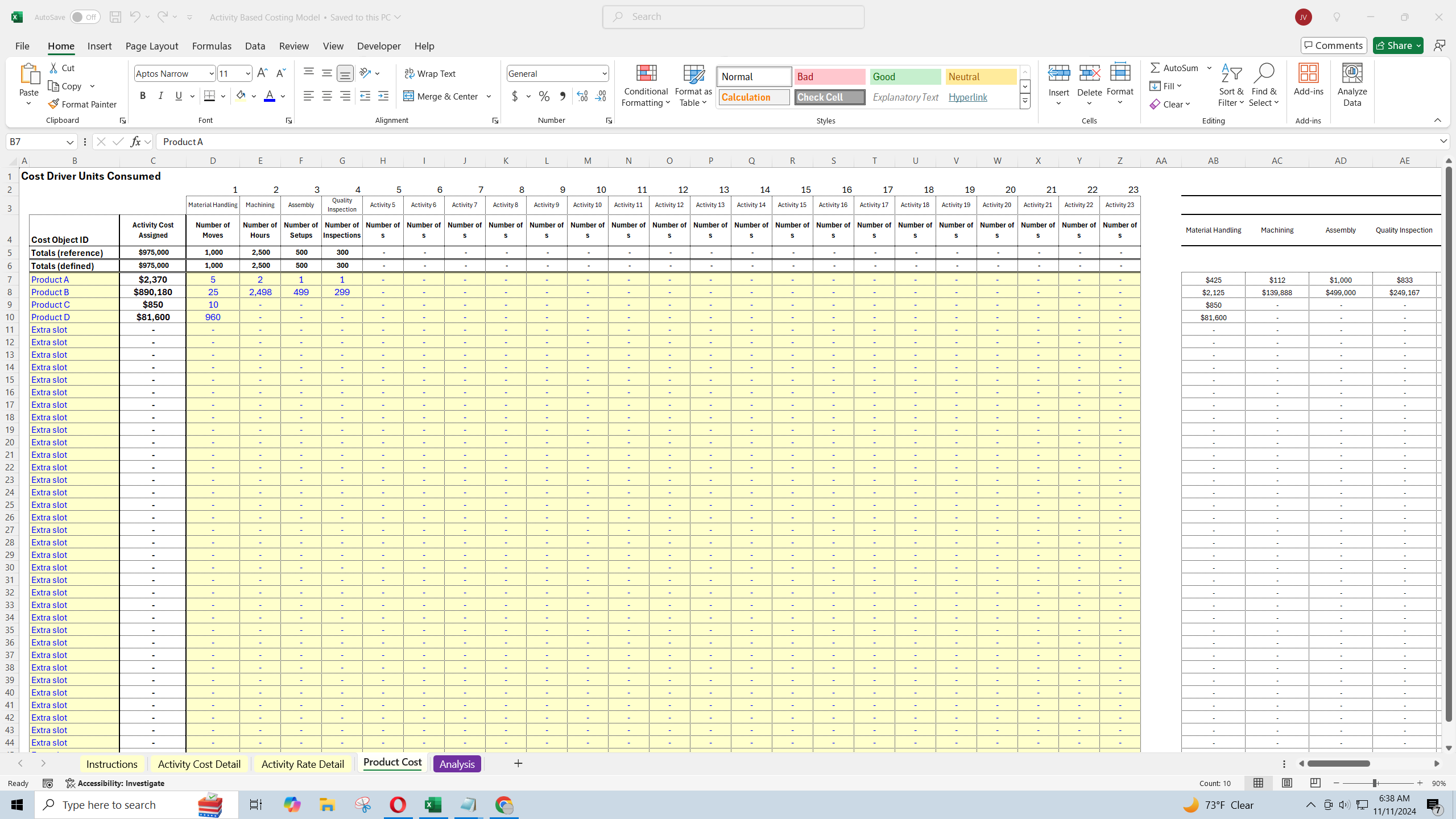

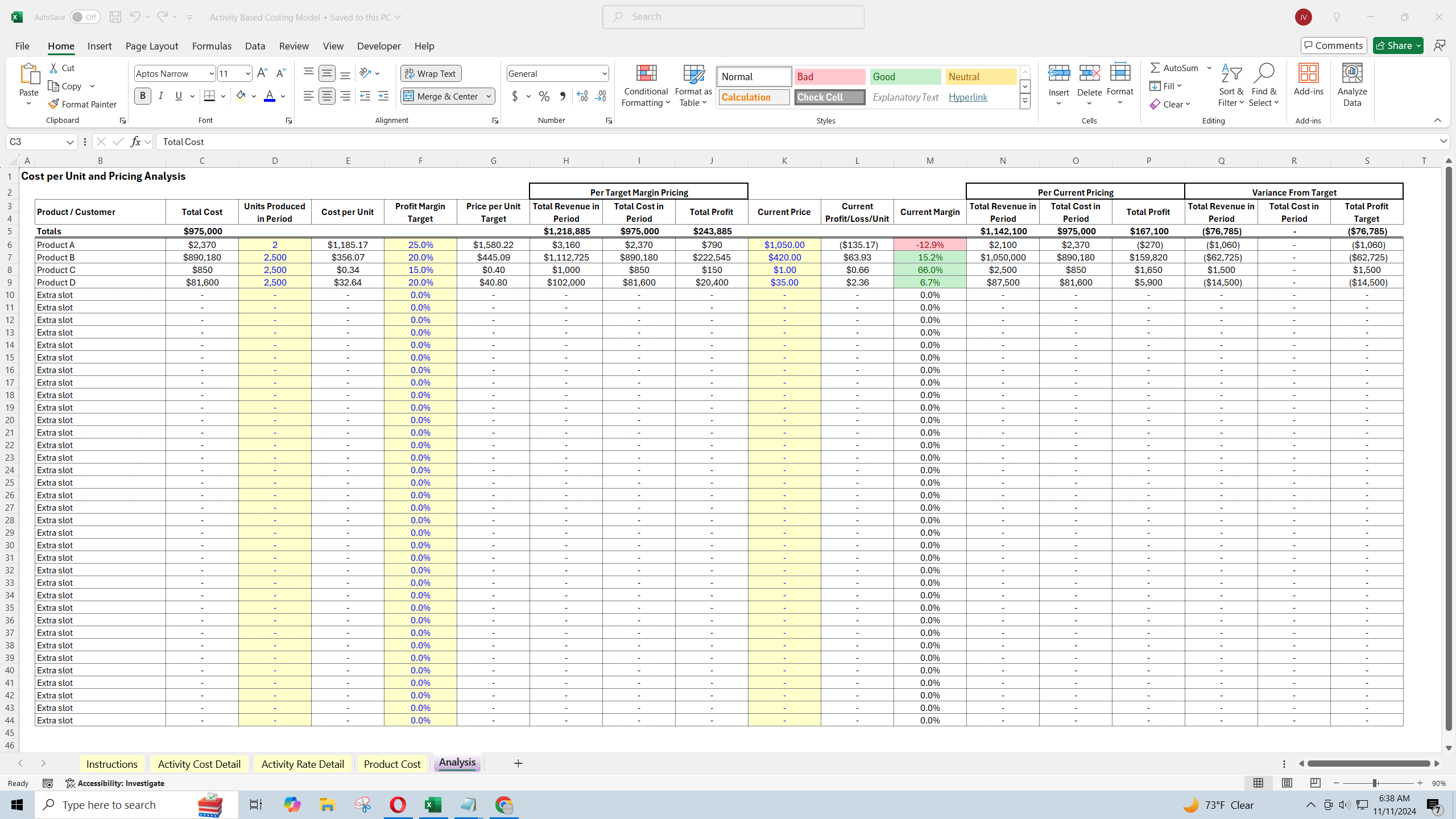

Activity-Based Costing Model for Pricing and Margin Analysis

Gain clarity into what exactly it cost to produce a given product and compare that to your current pricing in order to understand margins better.

Further information

Help businesses understand their product costs better and more accurately.

Any business that produces goods or services.