Originally published: 28/04/2020 12:20

Publication number: ELQ-69586-1

View all versions & Certificate

Publication number: ELQ-69586-1

View all versions & Certificate

Further information

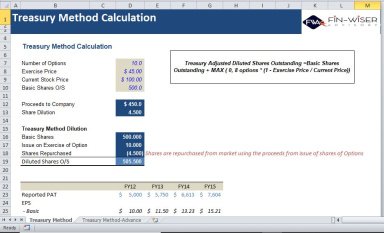

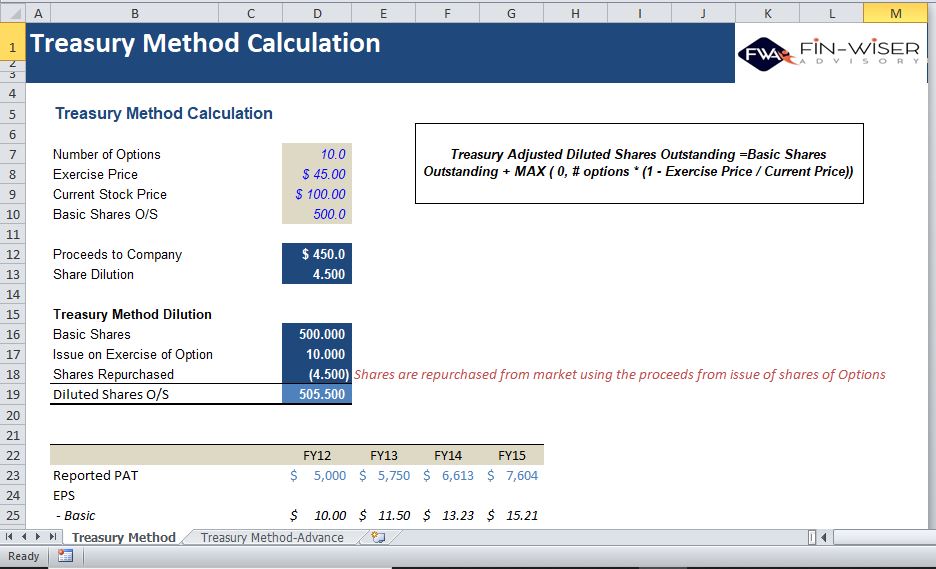

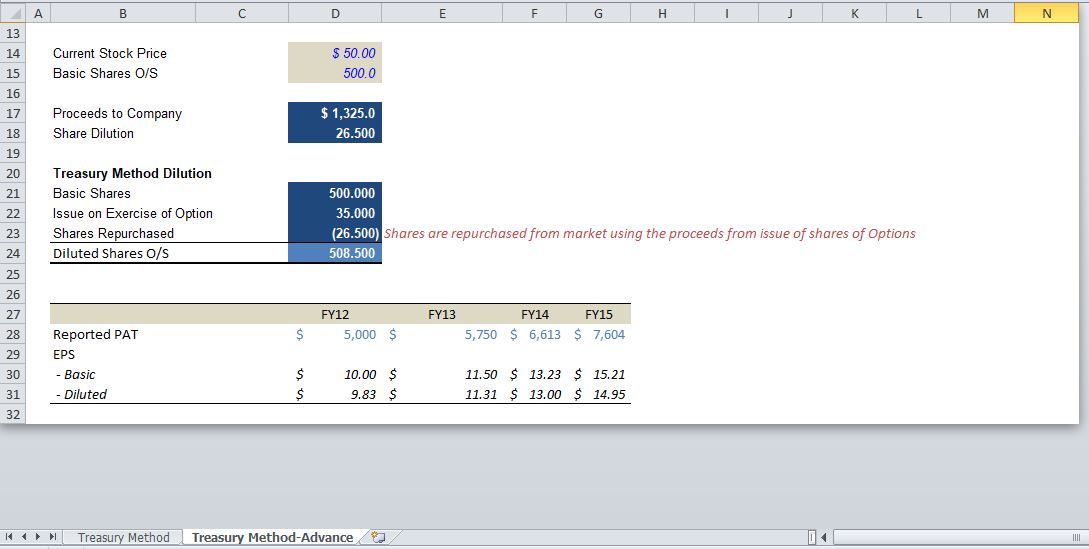

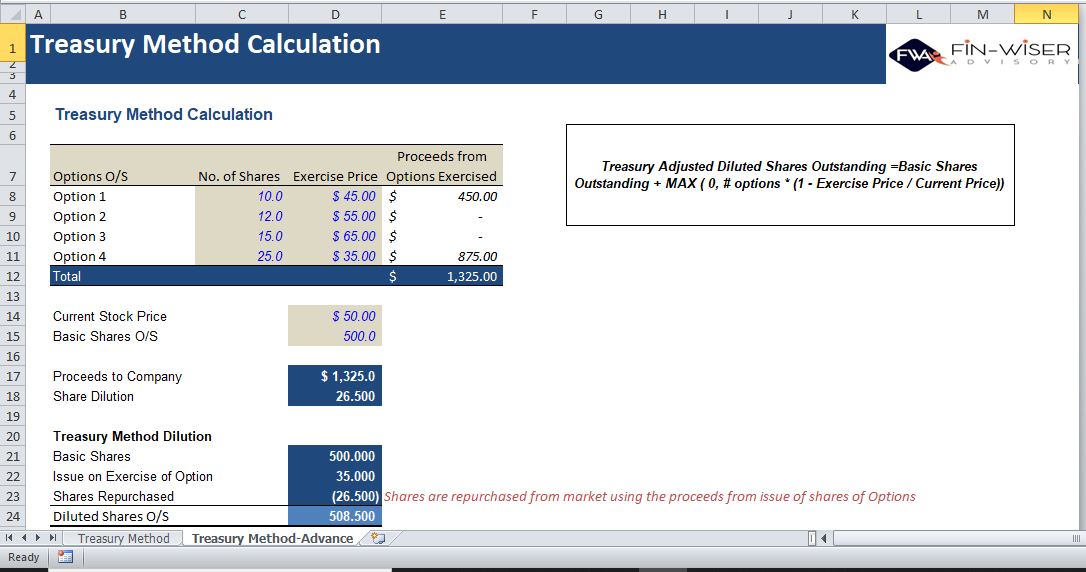

Understand working behind Treasury Method to calculated diluted number of shares

Understand working behind Treasury Method to calculated diluted number of shares

NA