Publication number: ELQ-26613-1

View all versions & Certificate

Discounted Cashflow (DCF) with Scenario Analysis

The discounted cash flow valuation is an intrinsic valuation methodology.

Further information

Determine the cash flows from operations using EBITDA as the proxy.

Determine the unlevered free cash flows by deducting tax, working capital and maintenance capital expenditures from EBIT.

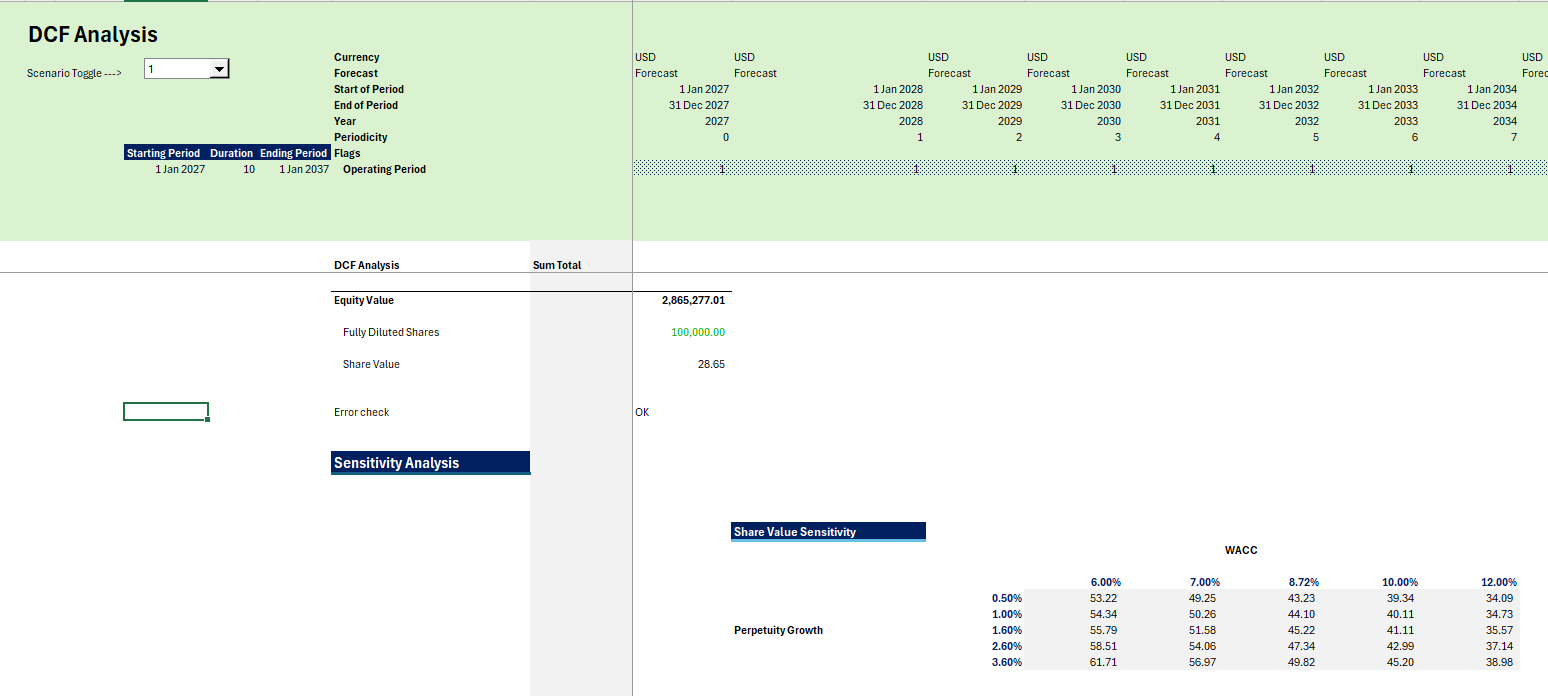

Discount the unlevered free cash flows using the implied WACC.

Determine the terminal value of cash flows by using the exit multiple approach or the perpetuity growth approach.

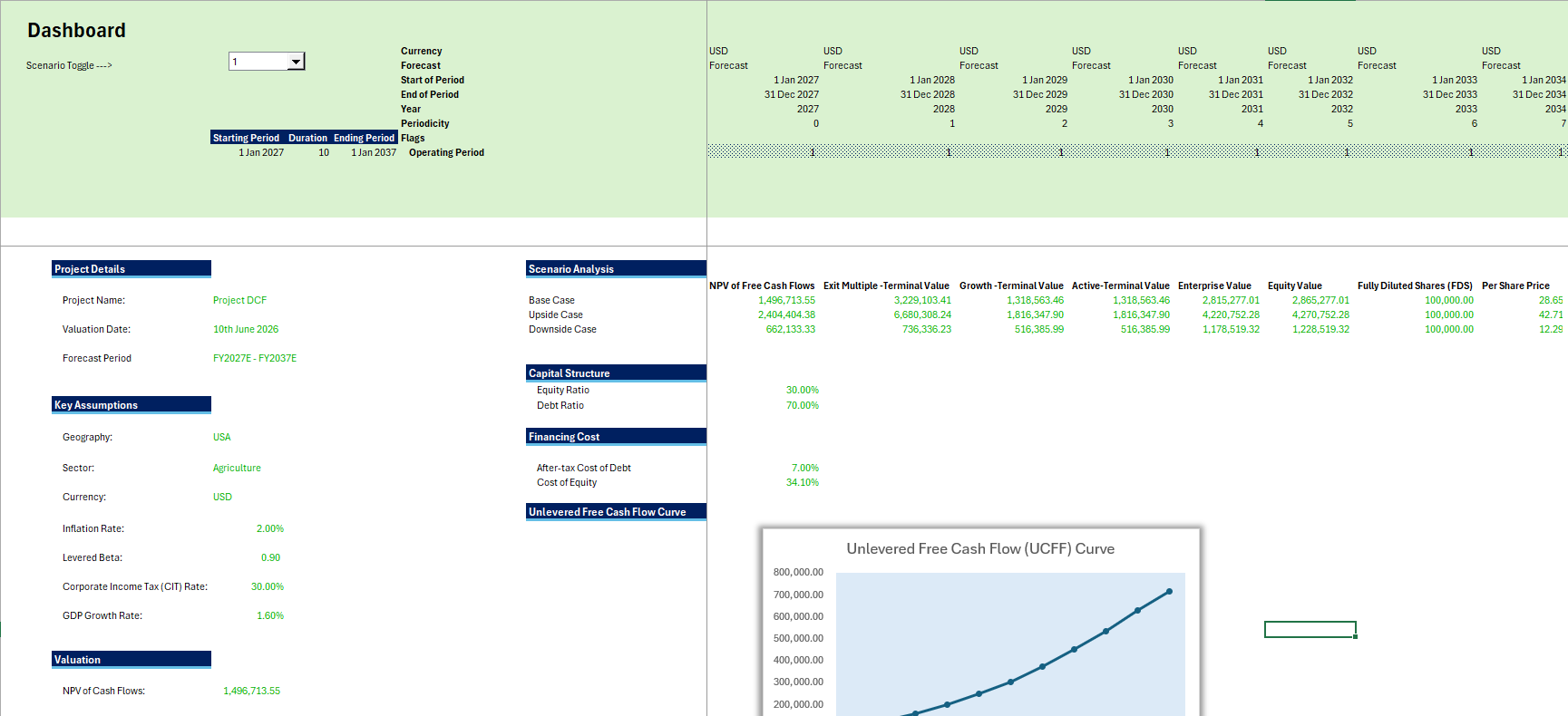

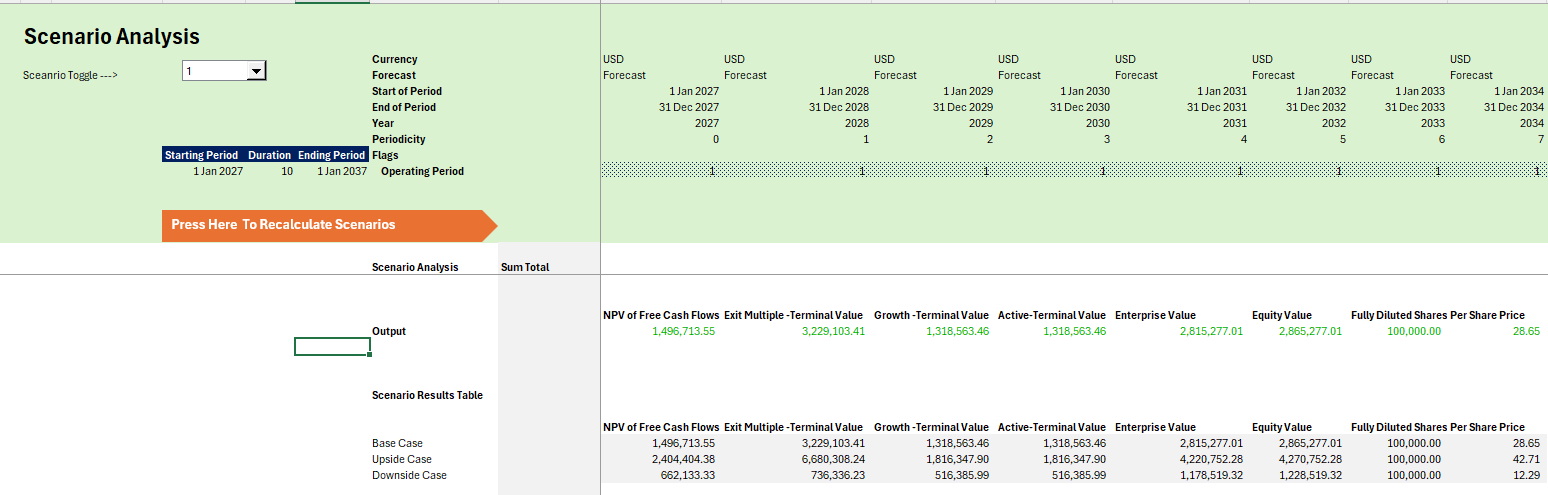

Sum the NPV of unlevered free cash flows with the terminal value to derive the enterprise value.

Subtract the net debt from the enterprise value to arrive at the equity value.

This model applies best to an asset, project or company with stable cash flows.

DCF analysis is prone to errors due to:

• Overstated or understated CAGR

• the WACC not being properly computed.

• the terminal value methodology not being validated with market data.

• the operational cost estimates being unrealistic