Publication number: ELQ-28465-1

View all versions & Certificate

Comparative Gratuity Financial Impact Assessment Model; Pre-2026 Labour Laws vs. Punjab Labour Code 2026

Model for Assessing the Comparative Financial Impact of Gratuity Provisions: Former Labor Laws versus the Punjab Labour Code 2026

This comparative financial impact model has been designed to help you analyze and visualize the profound shift in statutory gratuity liabilities brought about by the enforcement of the Punjab Labour Code (PLC) 2026 compared to the historical Industrial and Commercial Employment (Standing Orders) Ordinance 1968.

The workbook is structured into four highly polished tabs:

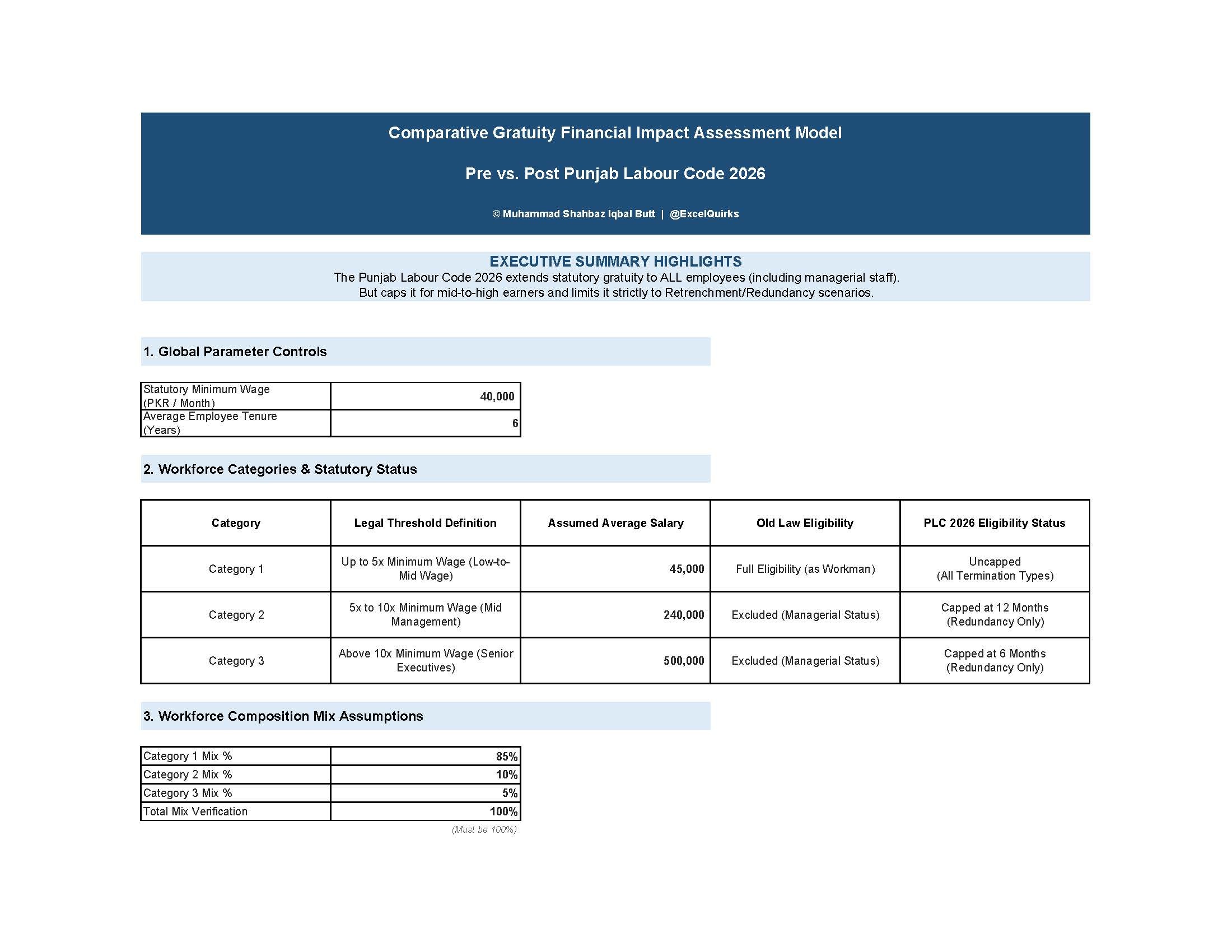

Dashboard & Parameters

Contains global model variables (such as the statutory minimum wage, average workforce tenure, and average salary levels) alongside a strategic breakdown of the new tiers.

Financial Impact Model

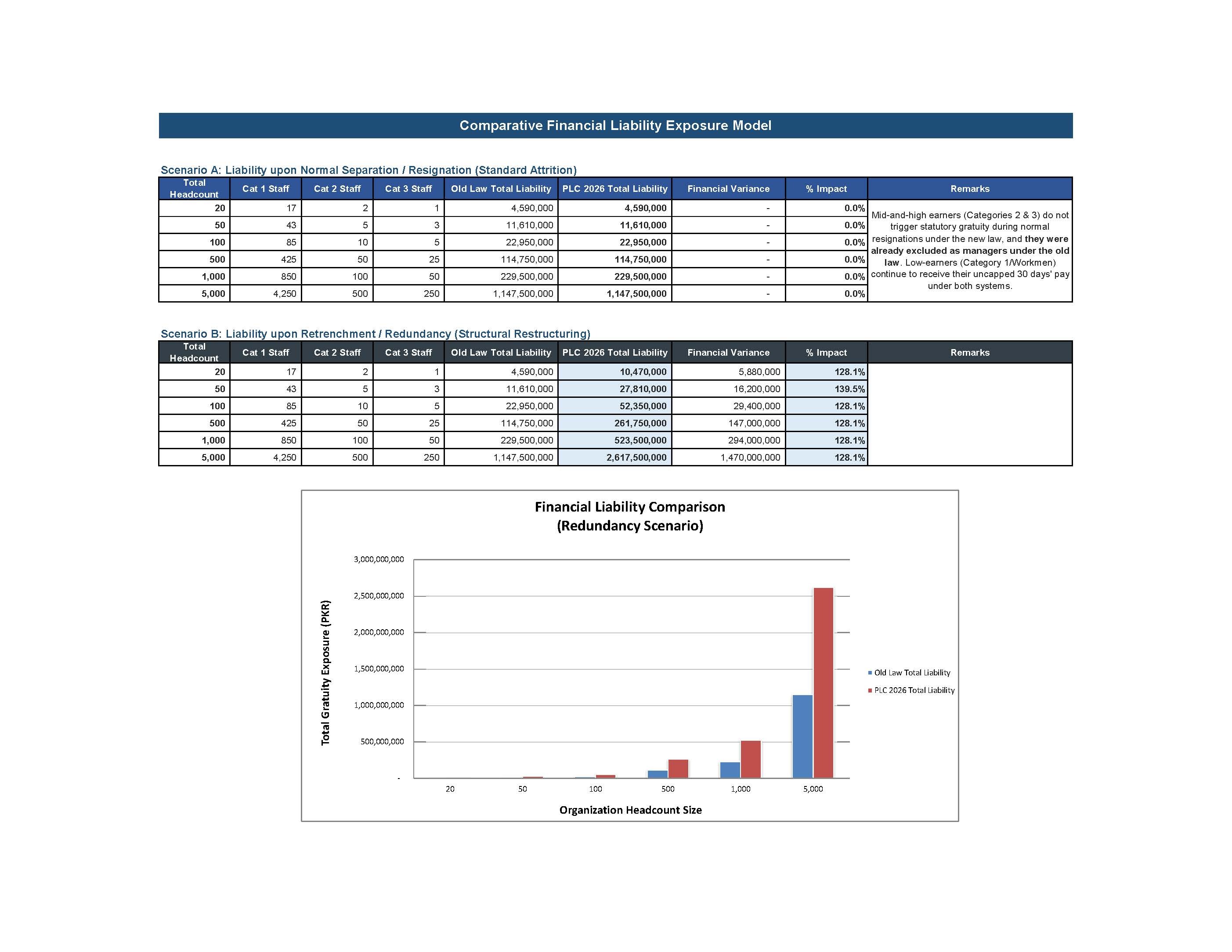

Core comparative matrices assessing organizations with 20, 50, 100, 500, 1,000, and 5,000 employees across two distinct operational scenarios (Normal Separation vs. Redundancy/Retrenchment). It includes a fully native clustered column chart for reporting.

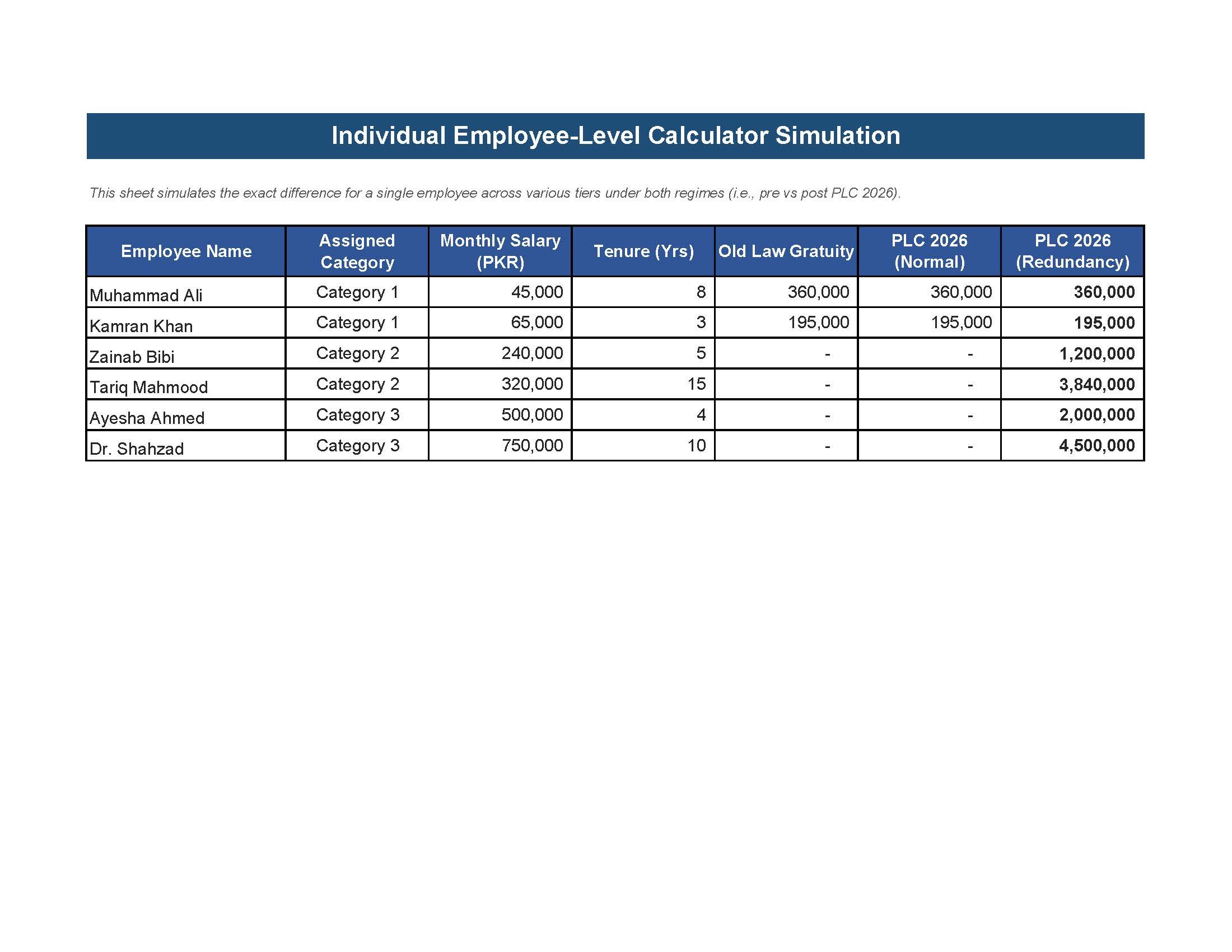

Employee-Level Simulation

A granular look at specific individual profiles (e.g., manual workers vs. mid-level managers vs. senior executives) to trace exactly how the Excel formulas apply the legal logic.

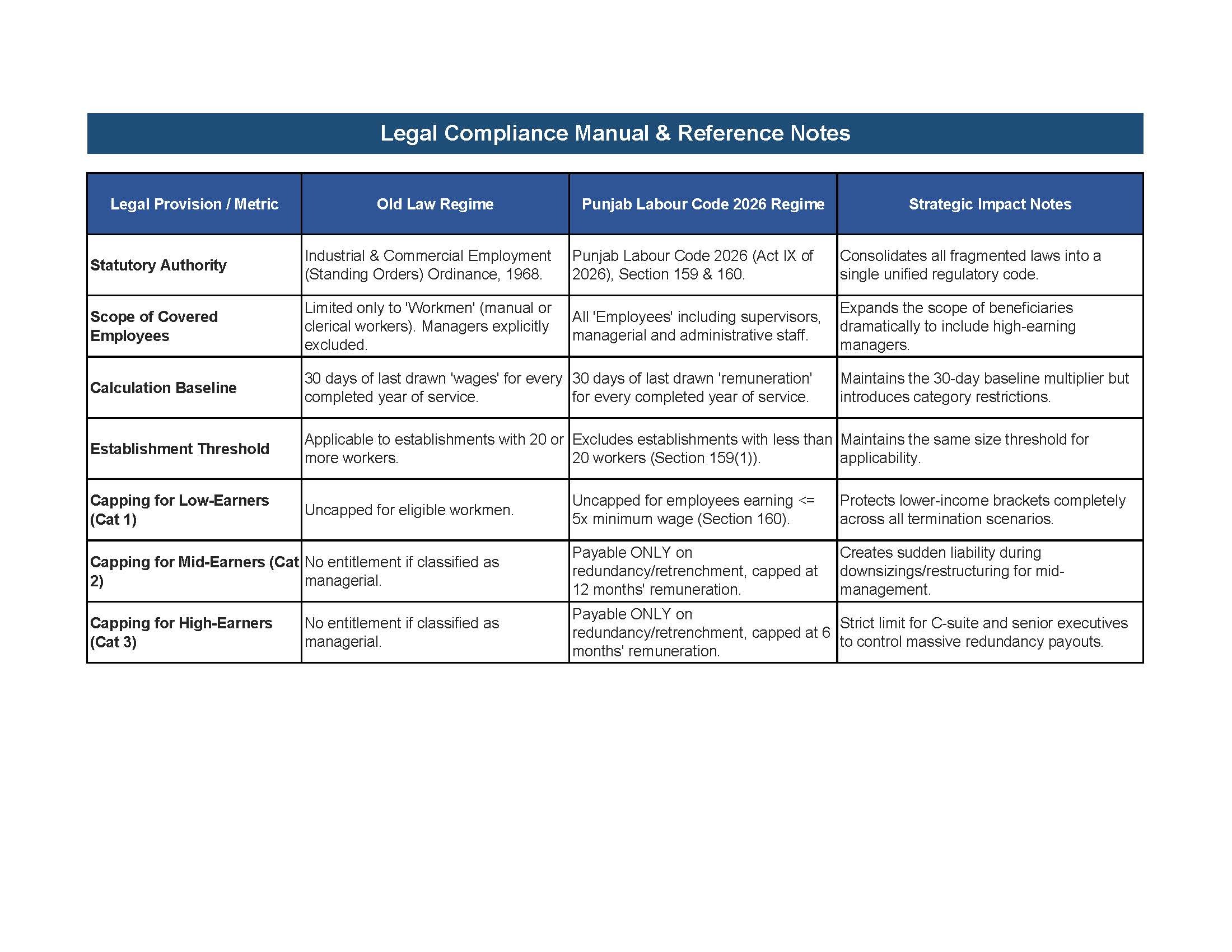

Legal References & Notes

A compliance checklist comparing specific sections of the new Code against the old ordinance.

Critical Legal Differences Embedded in the Model

1. Shift from "Workman" to "Employee" Old Law Regime:

Statutory gratuity was strictly confined to individuals matching the narrow definition of a "workman" (those performing manual, technical, or clerical labor). Anyone working in an administrative, supervisory, or managerial capacity was entirely excluded from the statute and had zero legal claim to gratuity.

PLC 2026 Regime: The Code comprehensively redefines the target population to include all "employees," explicitly bringing supervisors, managers, and administrative executives into the statutory benefit pool (Section 5).

2. Introduction of Wage-Based Tiers and Capping (Section 160)

The new law moves away from a universal un-capped multiplier and implements a tiered system based on the Statutory Minimum Wage:

Category 1 (Remuneration is less than or equal to 5x Minimum Wage): Full statutory eligibility across all non-misconduct termination types (including voluntary resignation). Uncapped (30 days' remuneration per year of service).

Category 2 (Remuneration is greater than 5x and is less than or equal to 10x Minimum Wage): Entitled to gratuity only if the termination is due to redundancy or retrenchment. Furthermore, the total payout is strictly capped at 12 months' worth of remuneration.

Category 3 (Remuneration is greater than10x Minimum Wage): Entitled to gratuity only if the termination is due to redundancy or retrenchment. The total payout is strictly capped at 6 months' worth of remuneration.

Key Financial Insights from the Scenarios

The financial model uncovers two drastically different realities for employers depending on their business situation:

Scenario A: Normal Separation / Attrition Regime (0% Budget Impact) When employees leave via normal resignation or standard termination without restructuring, the total statutory gratuity liability across all company sizes (from 20 up to 5,000 employees) remains completely identical (0% variance) between the old and new laws.

Why? Because mid-and-high earners (Categories 2 & 3) do not trigger statutory gratuity during normal resignations under the new law, and they were already excluded as managers under the old law. Low-earners (Category 1/Workmen) continue to receive their uncapped 30 days' pay under both systems.

Scenario B: Retrenchment / Redundancy Regime (Massive Cost Escalation) If an organization undergoes structural downsizing or site closures, the PLC 2026 introduces a major new financial liability.

Why? Under the old law, laying off 50 corporate managers or executive engineers triggered Rs. 0 in statutory gratuity. Under the new Code, a layoff forces the employer to pay out the capped gratuity (up to 12 months for mid-tier and 6 months for senior executives).

Impact:

For a 1,000-employee company undergoing structural redundancy, the total gratuity liability spikes by millions of PKR, representing a sharp double-digit percentage increase in transition costs.

Excel Spreadsheet Design and Integrity Checklist

Dynamic Links: The entire workbook is fully integrated. If you modify the Statutory Minimum Wage or the Average Employee Tenure, the entire financial model and all individual simulated payouts across all tabs will auto-recalculate instantly.

Chart Inclusions: It includes an automated column chart comparing the total financial exposure under both regimes side-by-side for all requested staff volumes (20 to 5,000).

To review the full model and input your specific payroll variables, please open the generated .xlsx spreadsheet directly in Microsoft Excel.

Link to video:

https://youtu.be/Q7AXgXO1vuw

This Best Practice includes

Excel Workbook

Further information

Retirement Benefits