Originally published: 20/06/2016 12:13

Last version published: 26/03/2018 10:11

Publication number: ELQ-80803-2

View all versions & Certificate

Last version published: 26/03/2018 10:11

Publication number: ELQ-80803-2

View all versions & Certificate

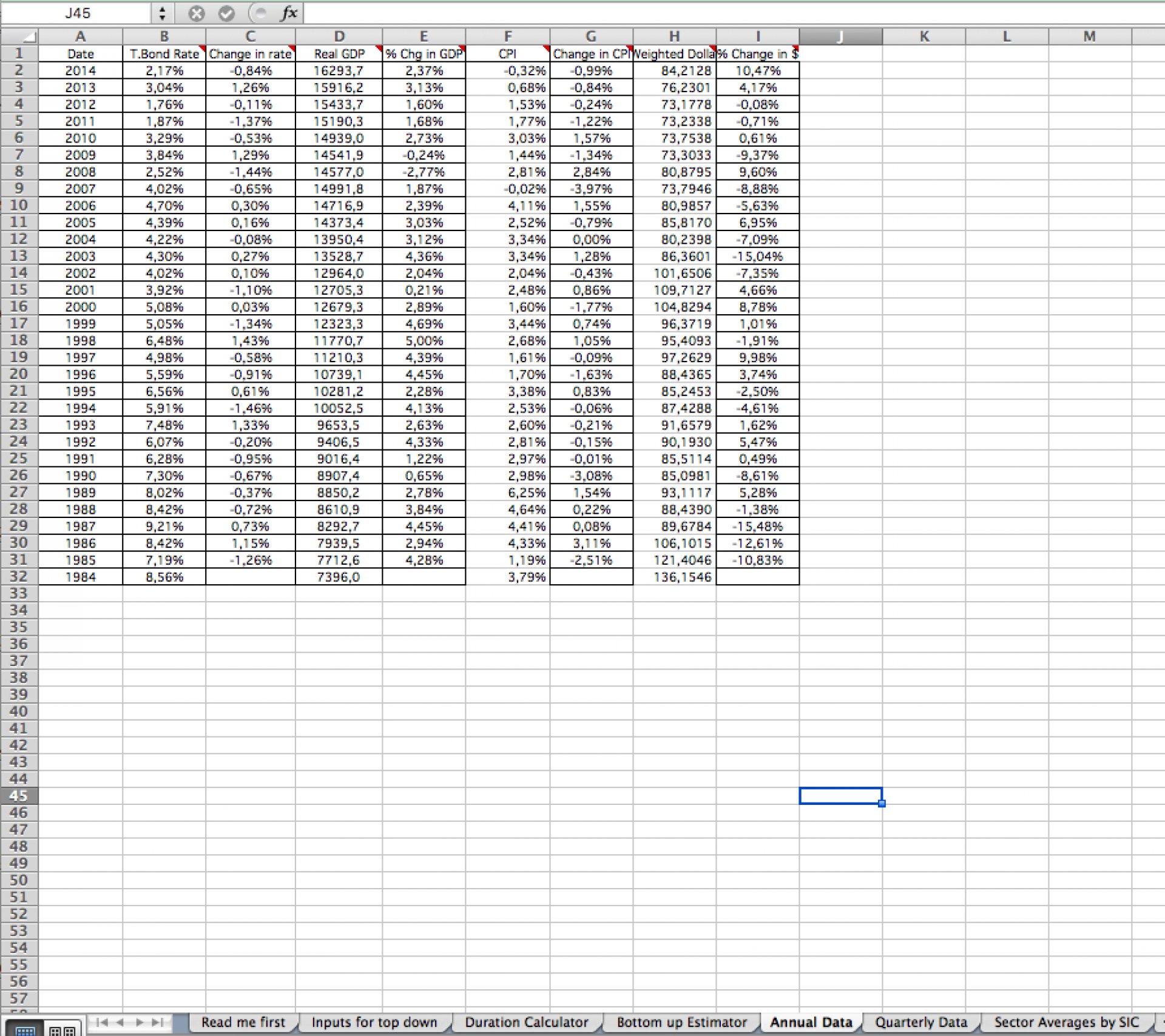

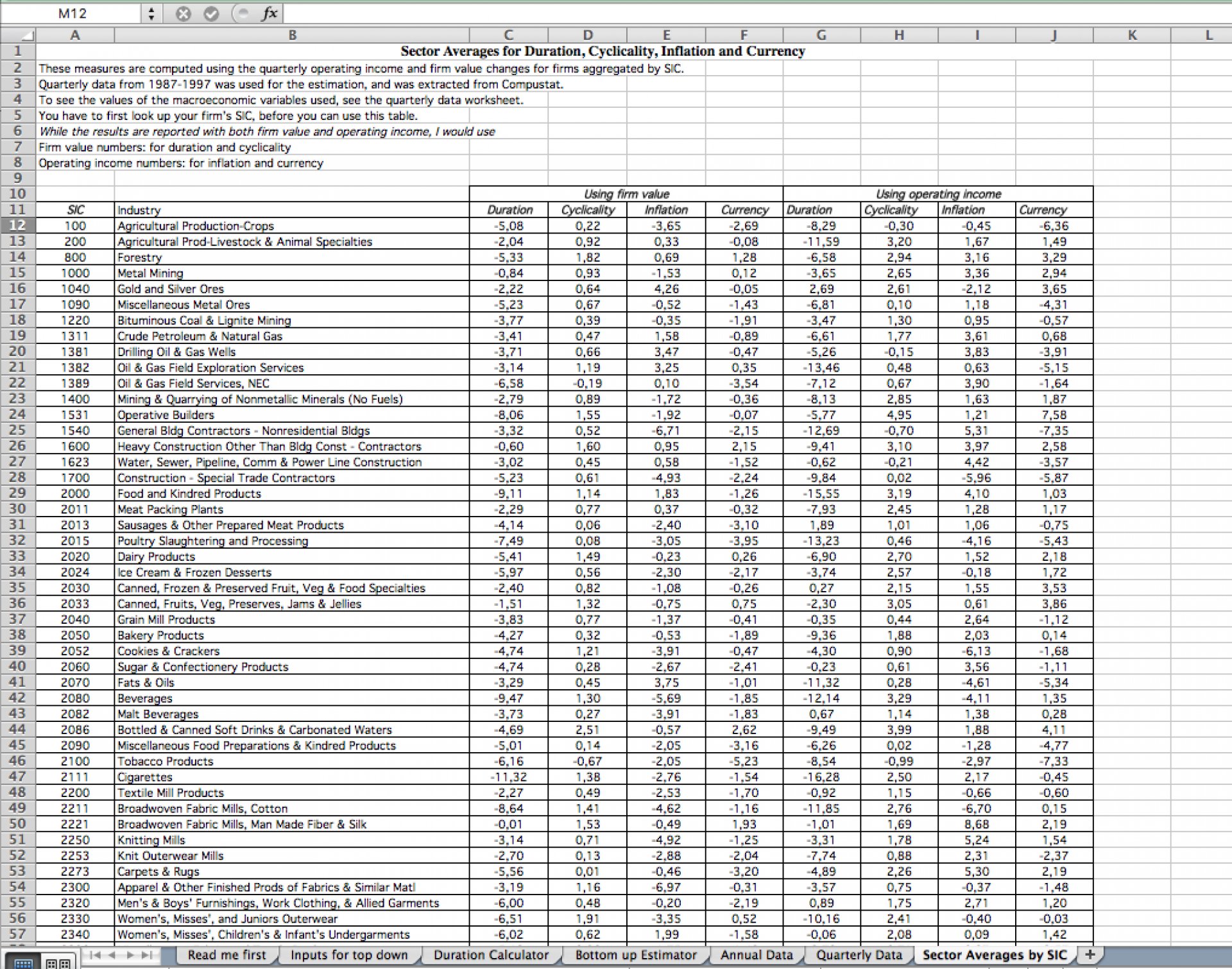

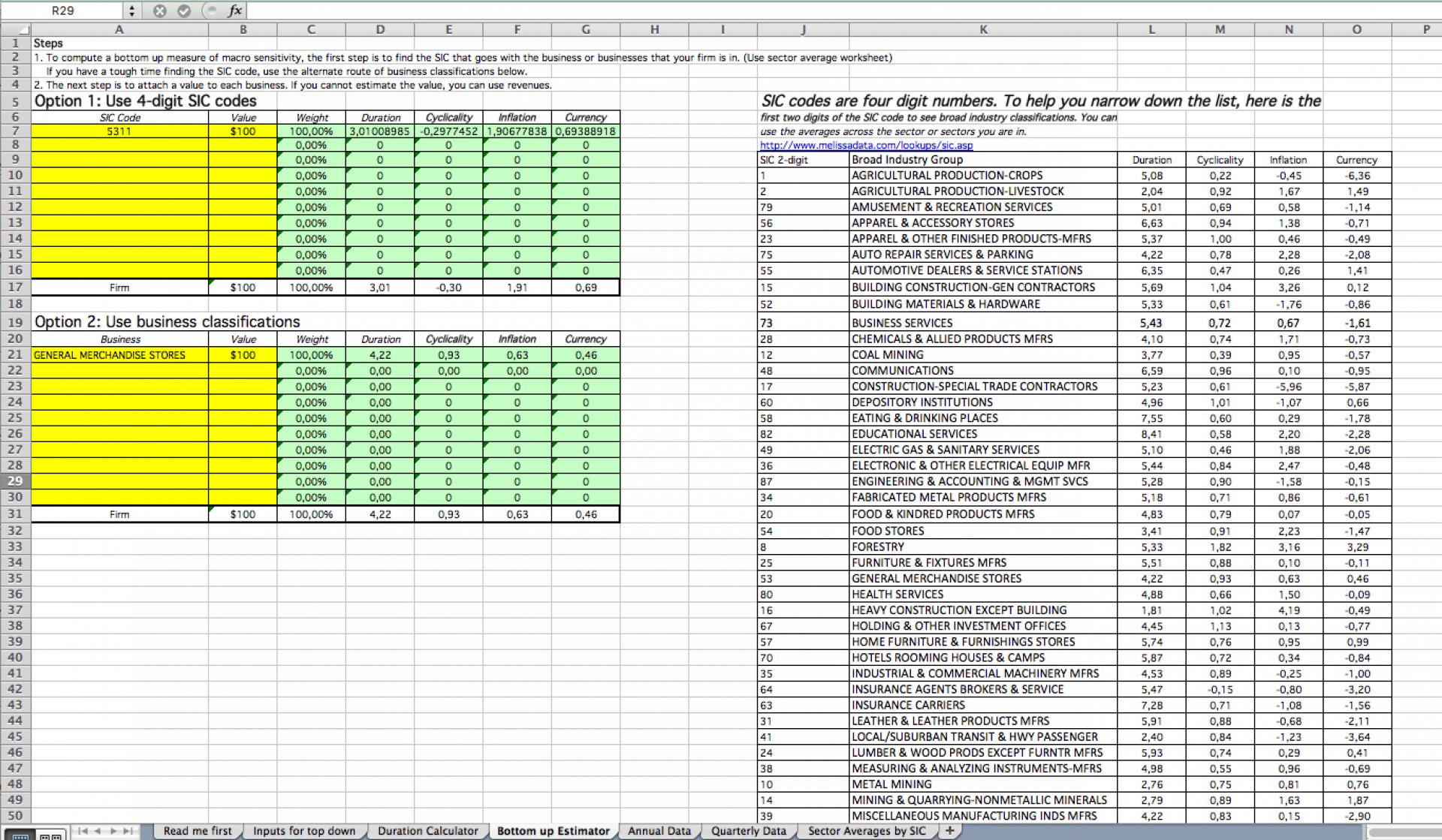

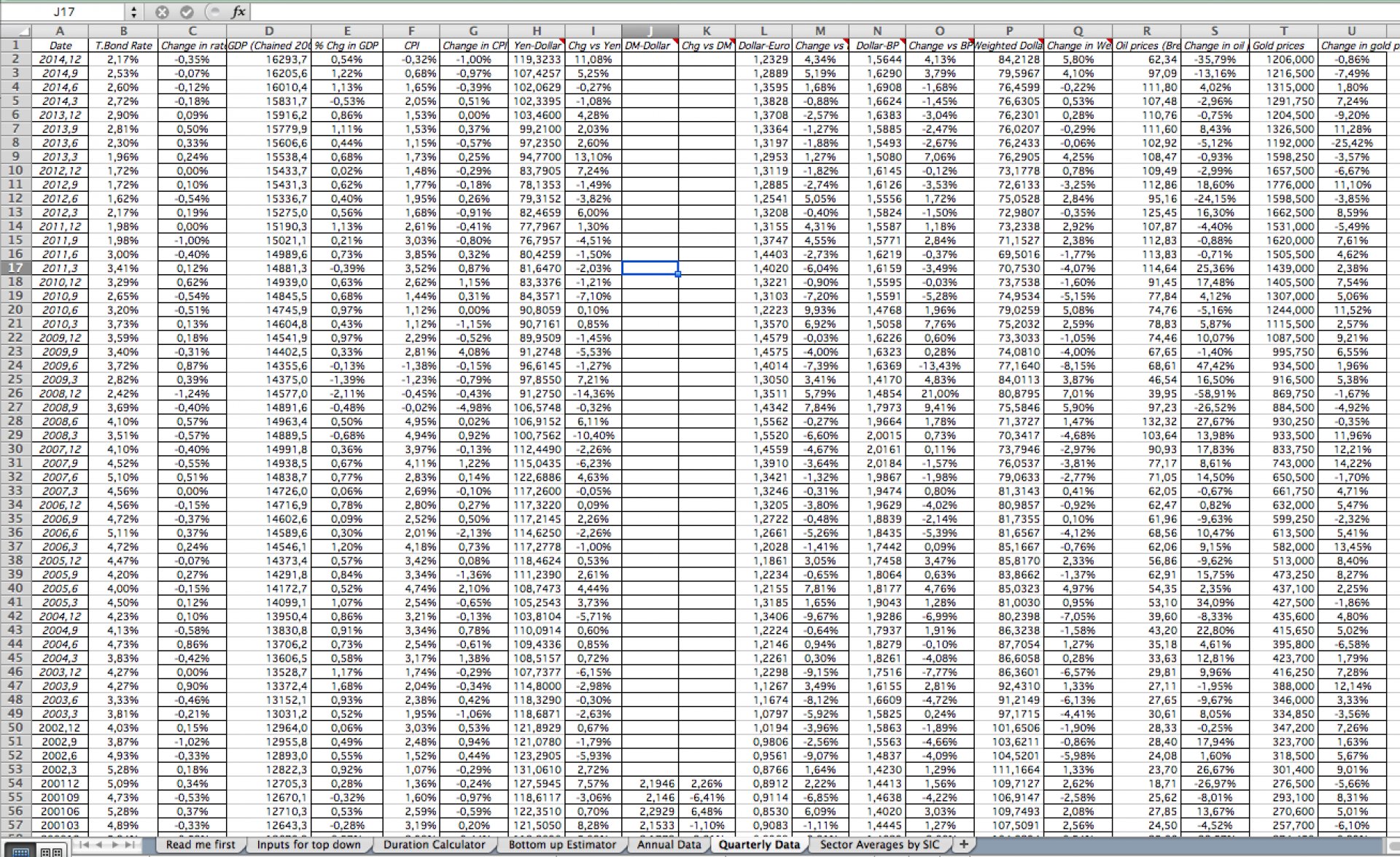

Design debt (by looking at sensitivity to macro variables)

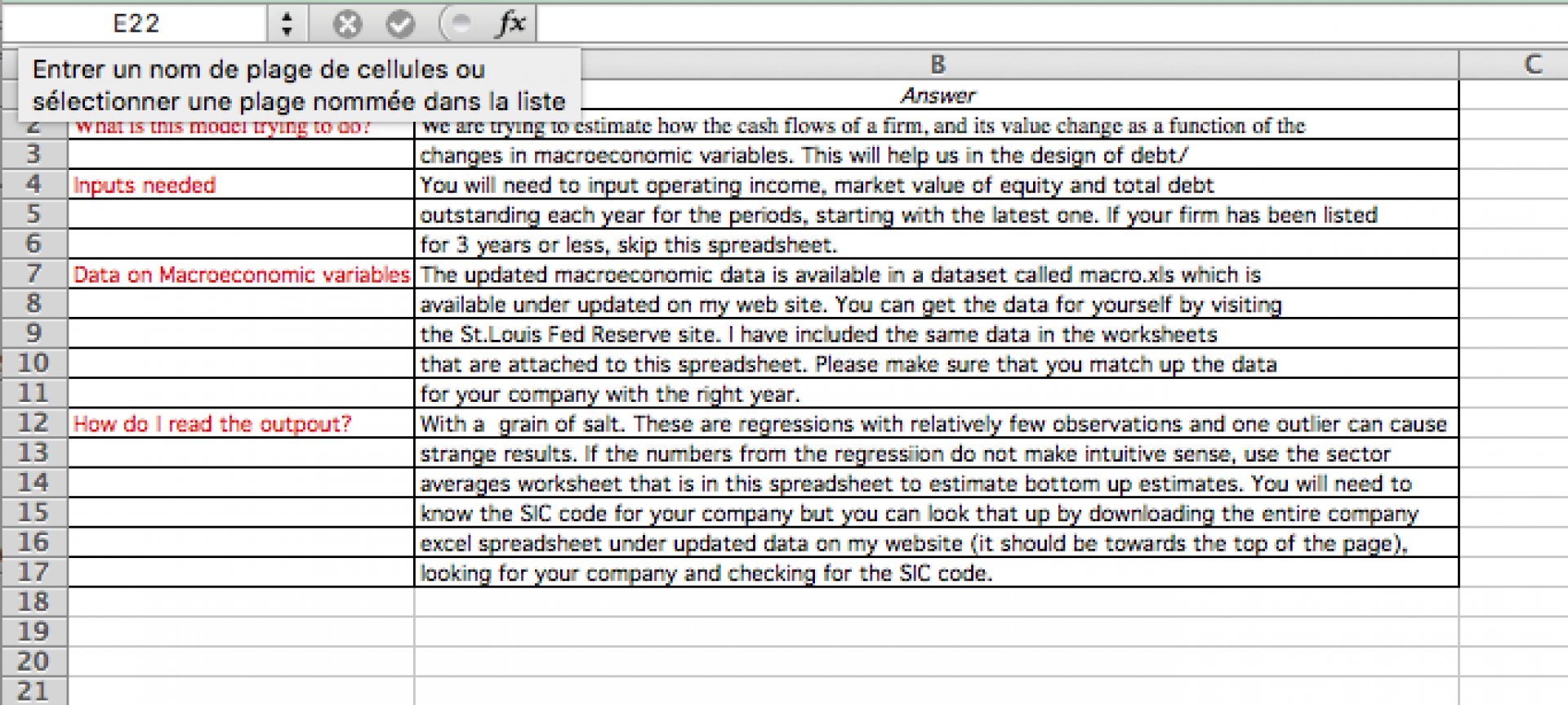

Allows you to estimate the duration of a firm's assets and its sensitivity to other macro economic variables

Prof. Aswath Damodaran offers you this Best Practice for free!

download for free

Add to bookmarks

Further information

The objective of this model is to get the following output values, based on Firm Value or based on Operating Income:

- Slope of regression vs Interest rate change

- Duration of the firm's assets

- Cyclicality of firm's assets

- Sensitivity to Inflation

- Sensitivity to Dollar movements

It may be useful in the design of debt.