Originally published: 17/09/2018 09:22

Last version published: 17/09/2018 09:24

Publication number: ELQ-29871-2

View all versions & Certificate

Last version published: 17/09/2018 09:24

Publication number: ELQ-29871-2

View all versions & Certificate

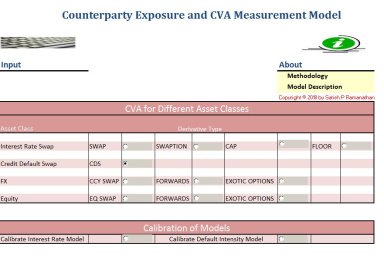

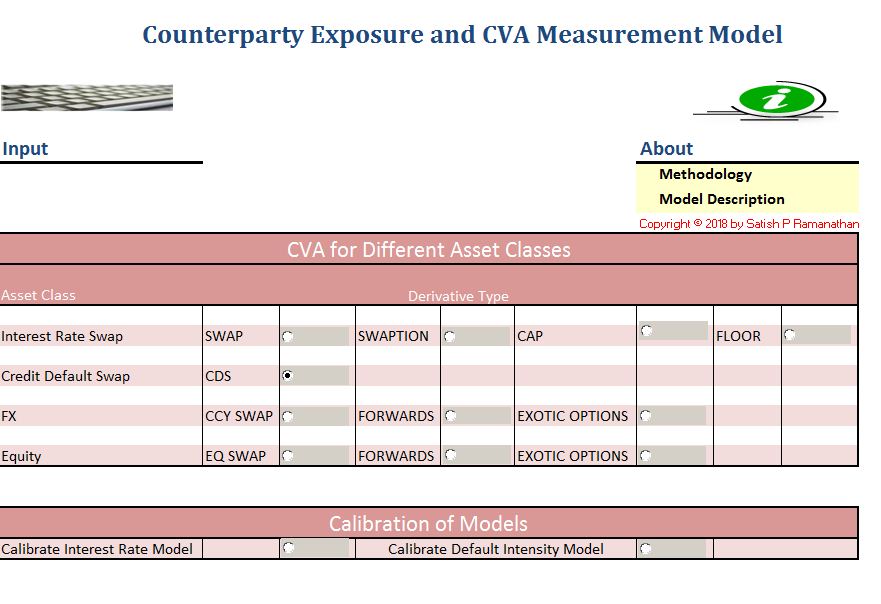

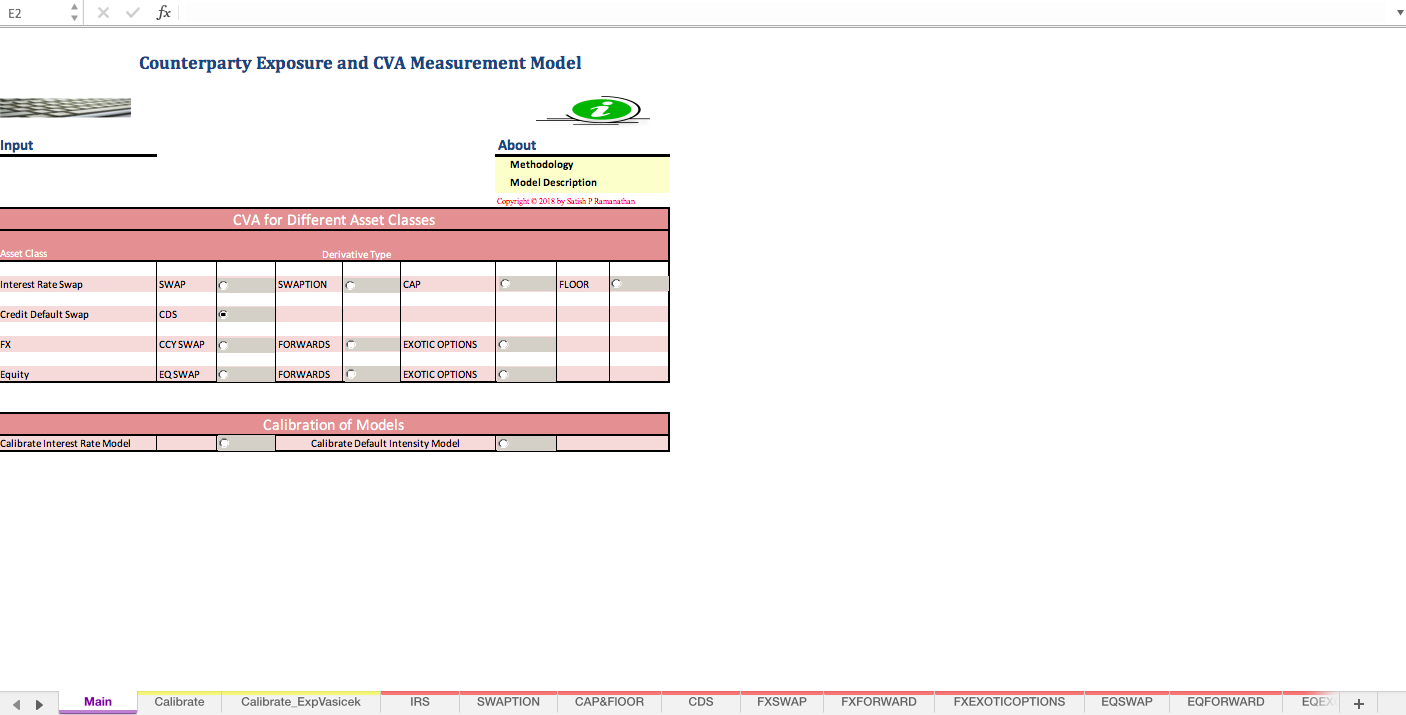

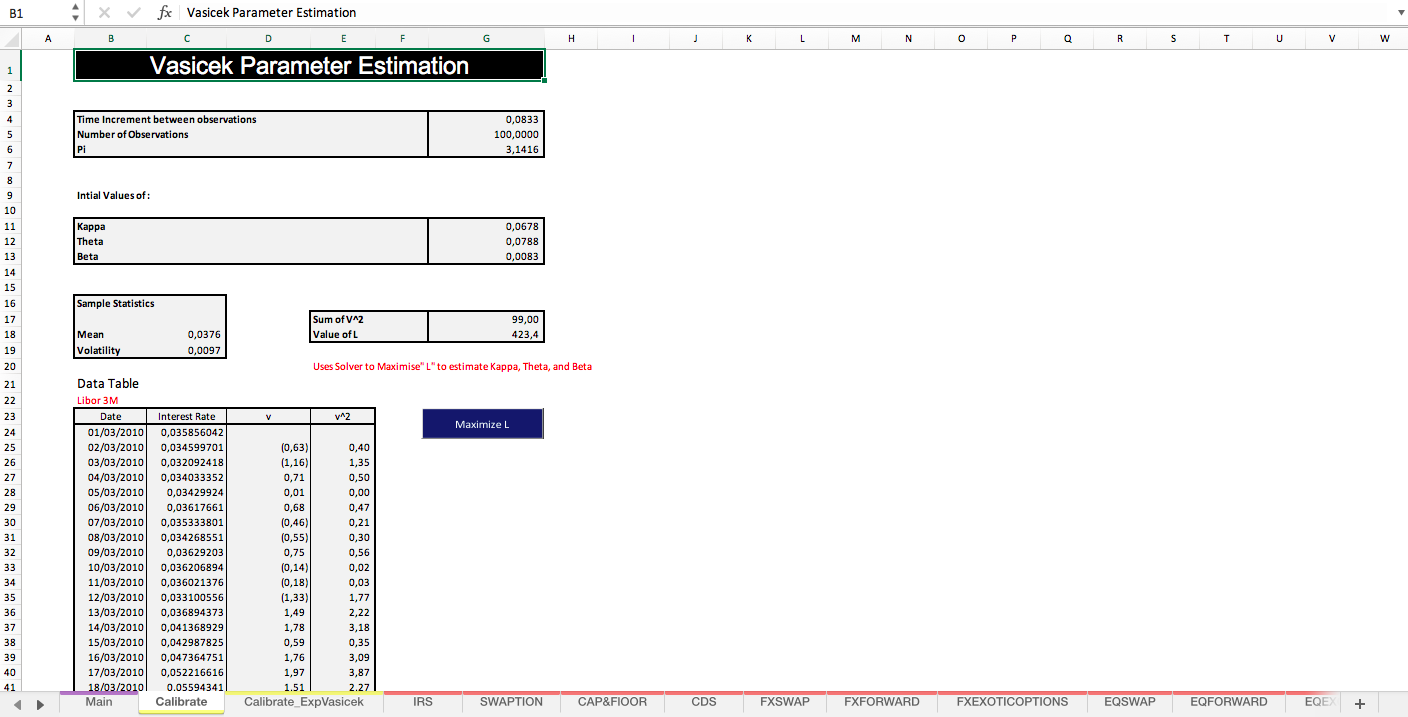

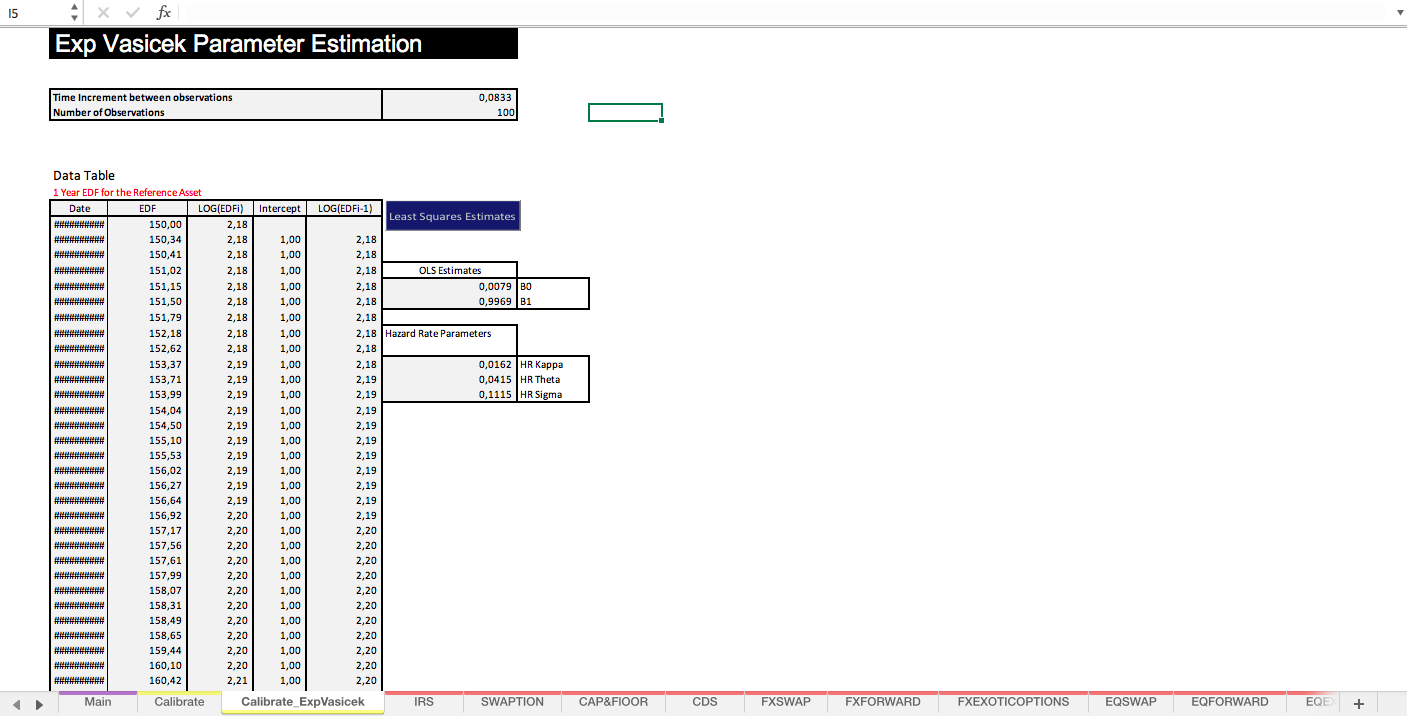

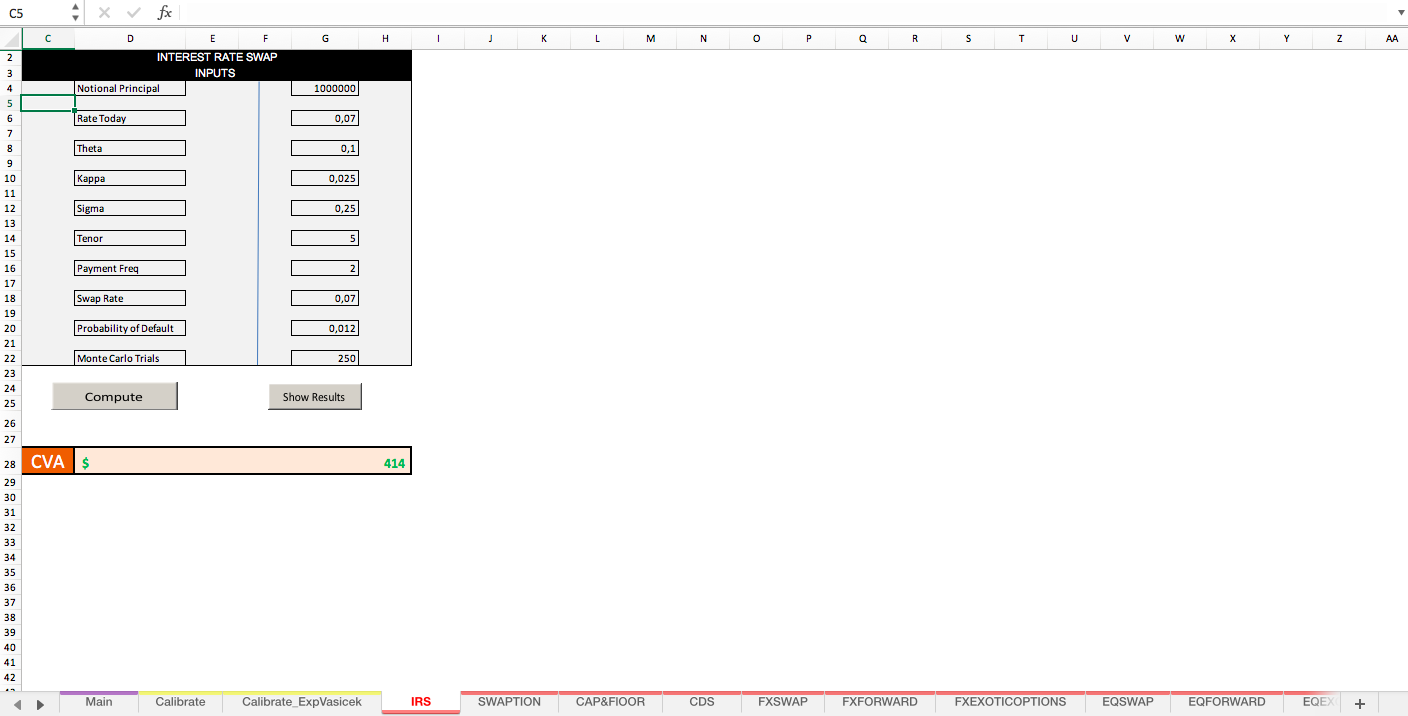

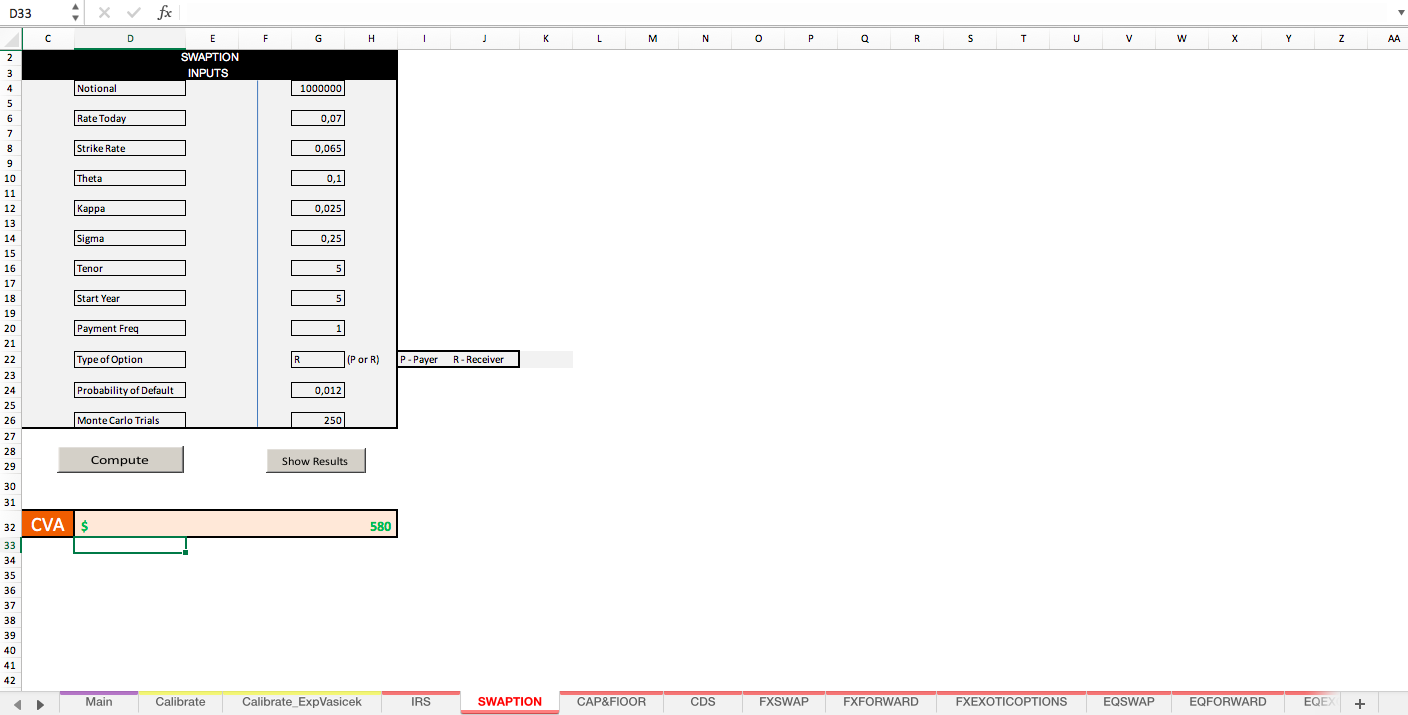

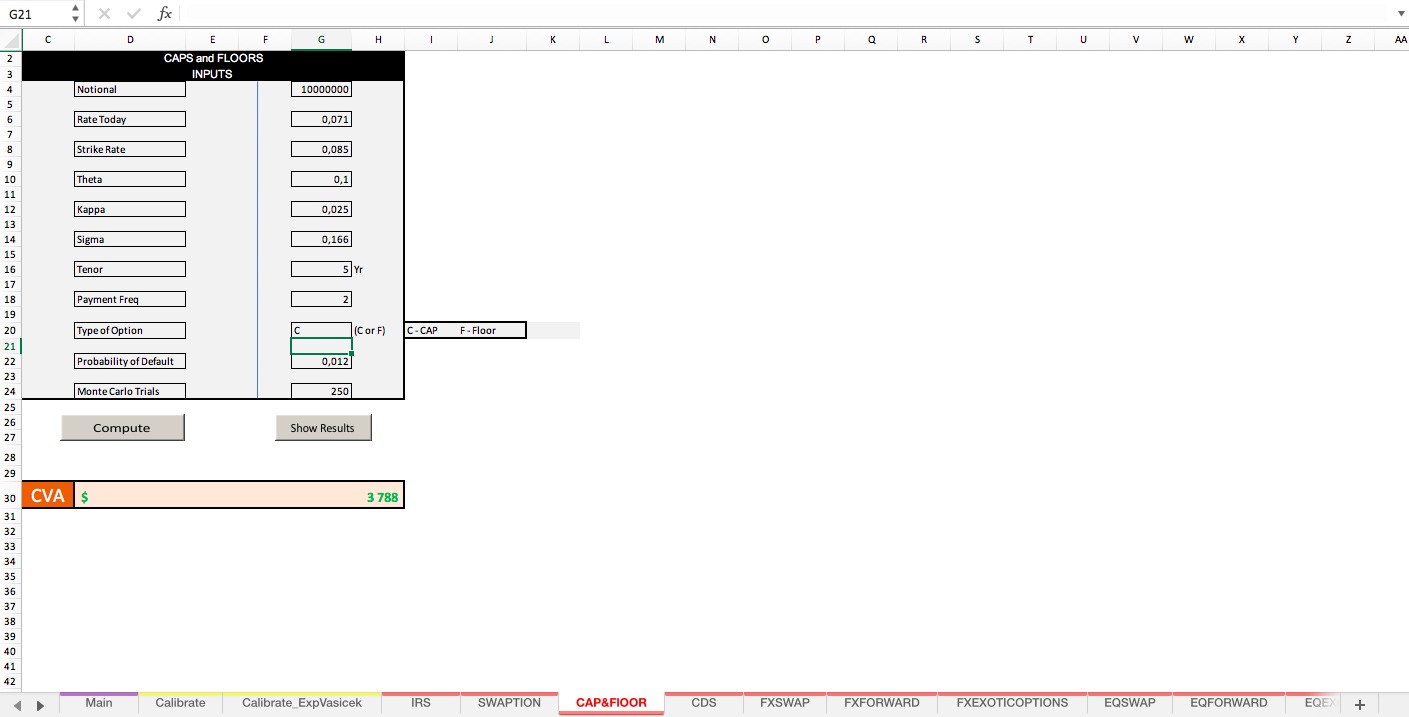

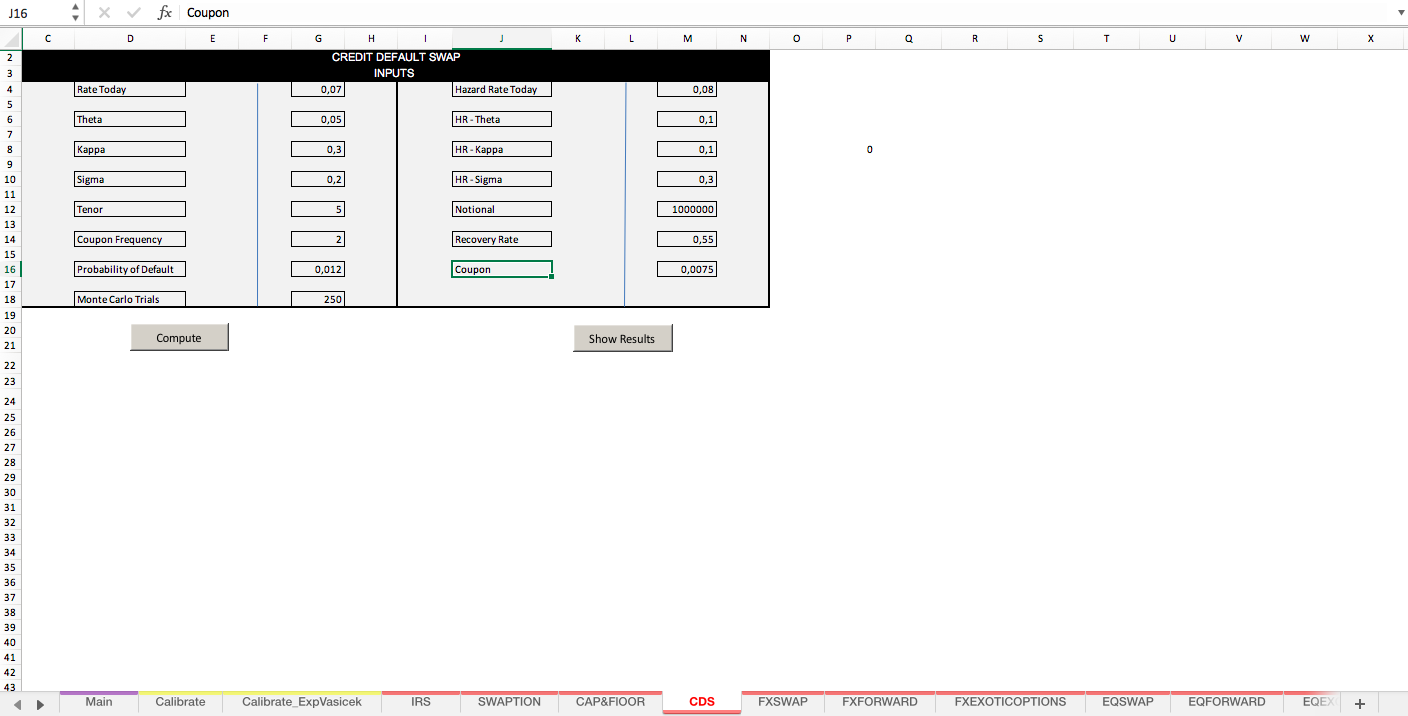

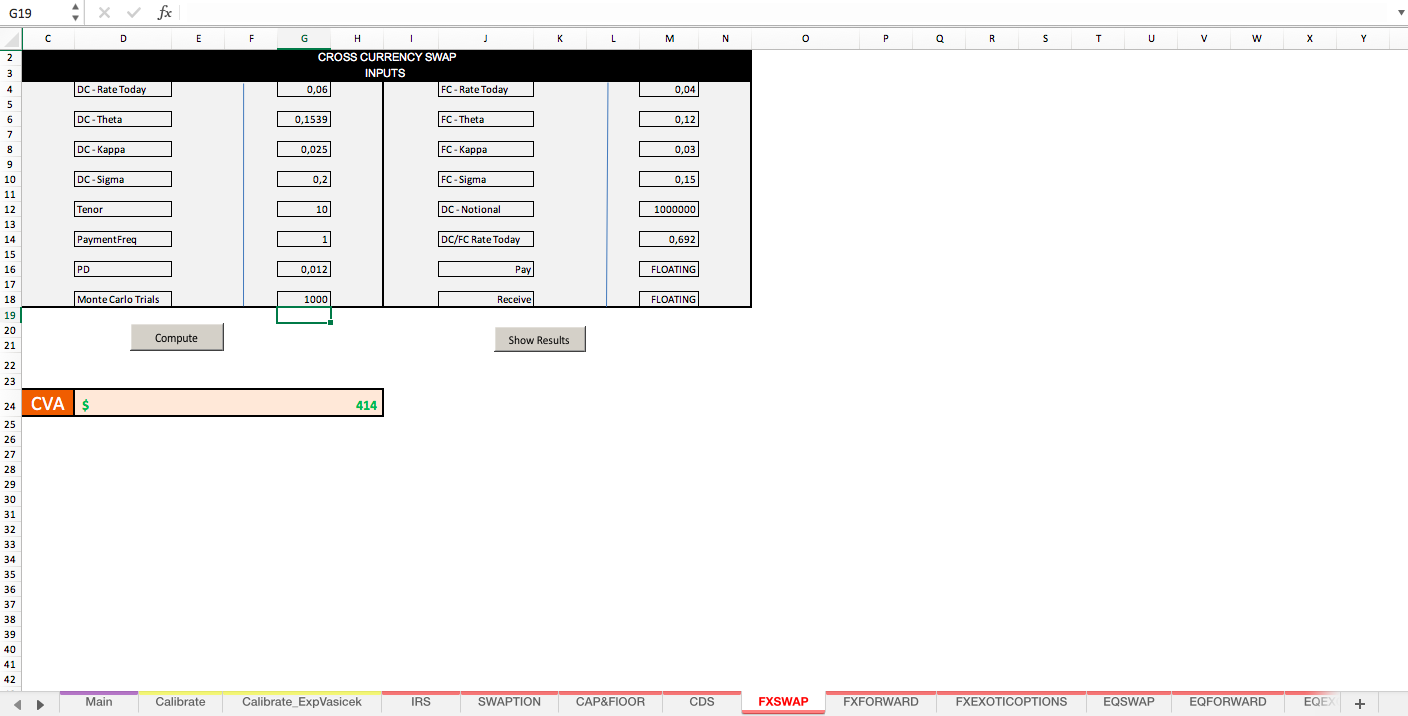

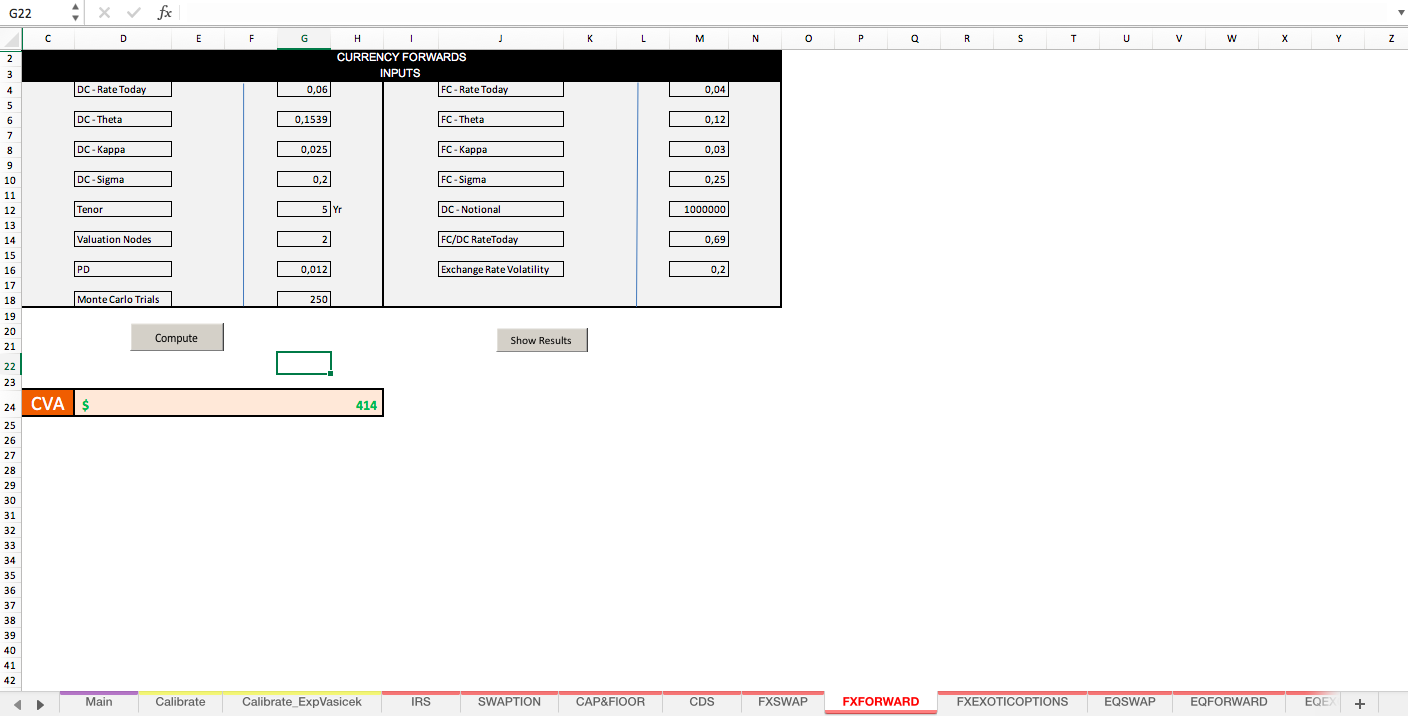

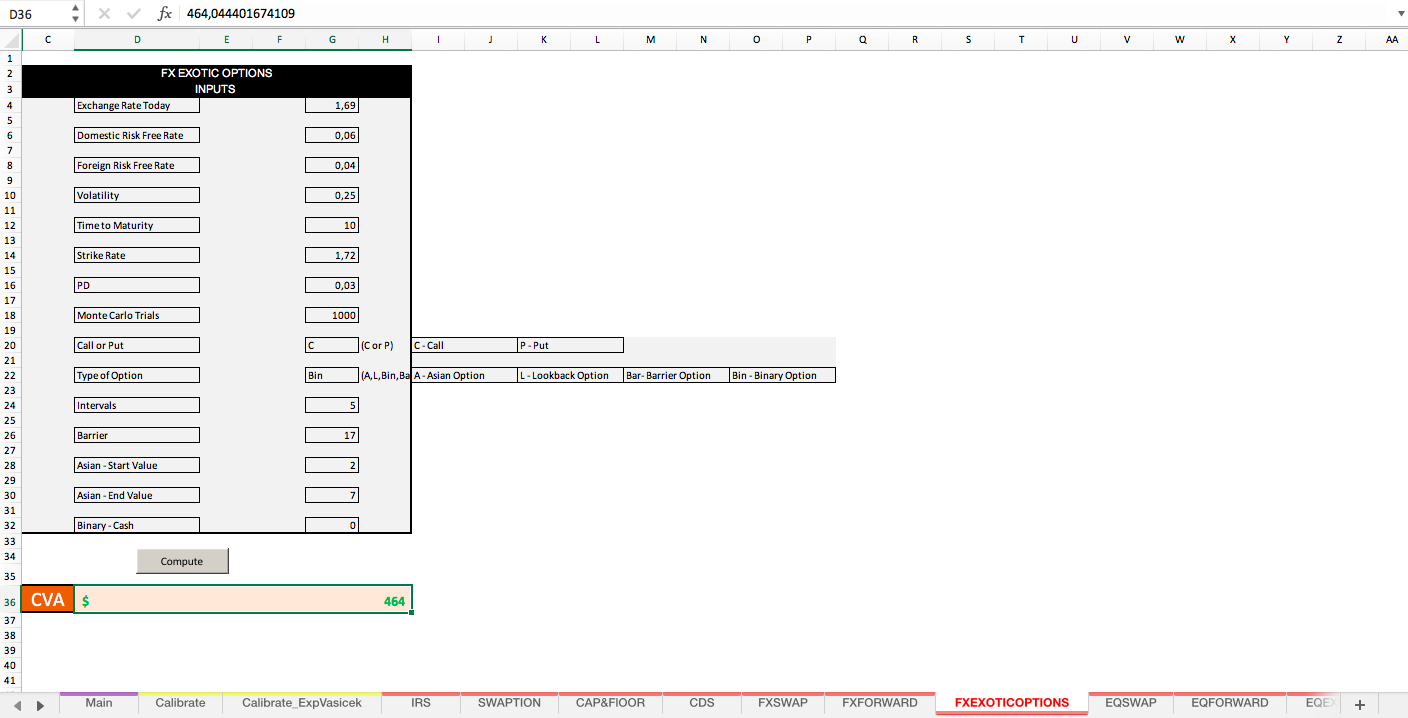

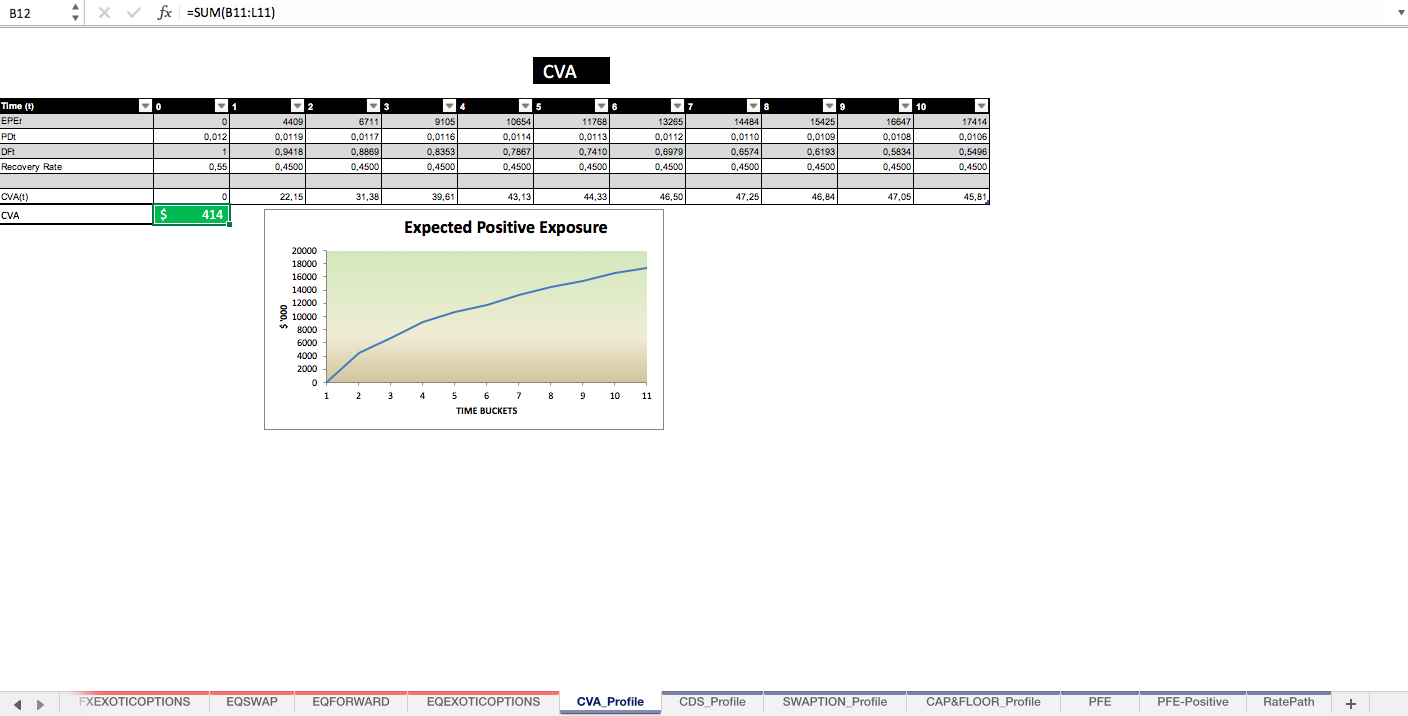

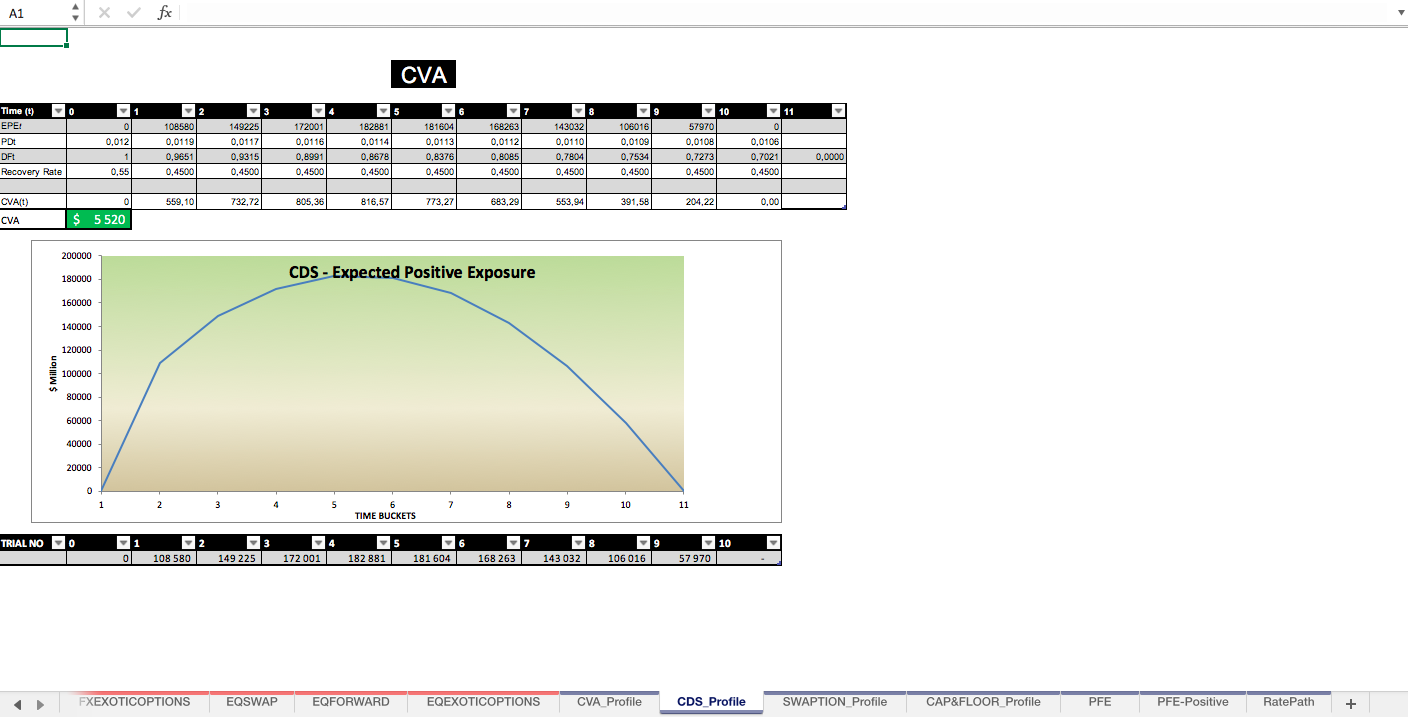

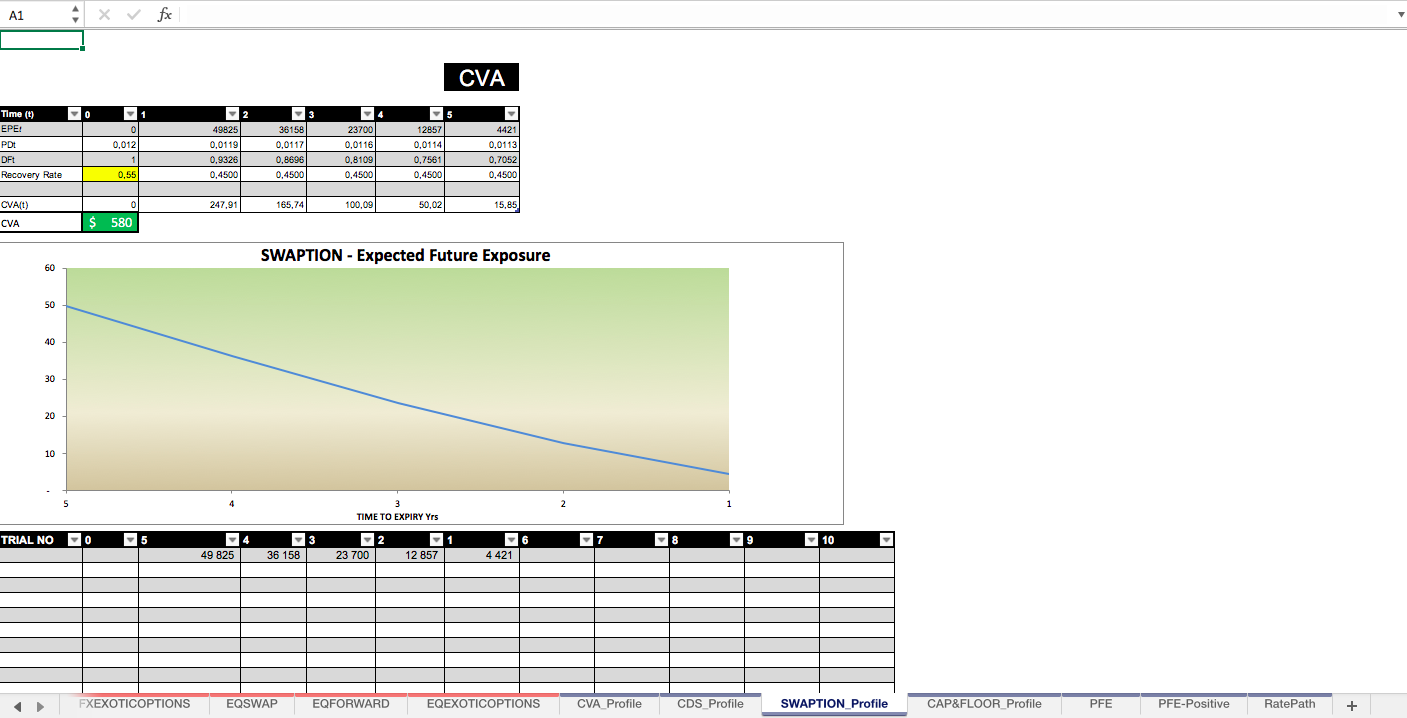

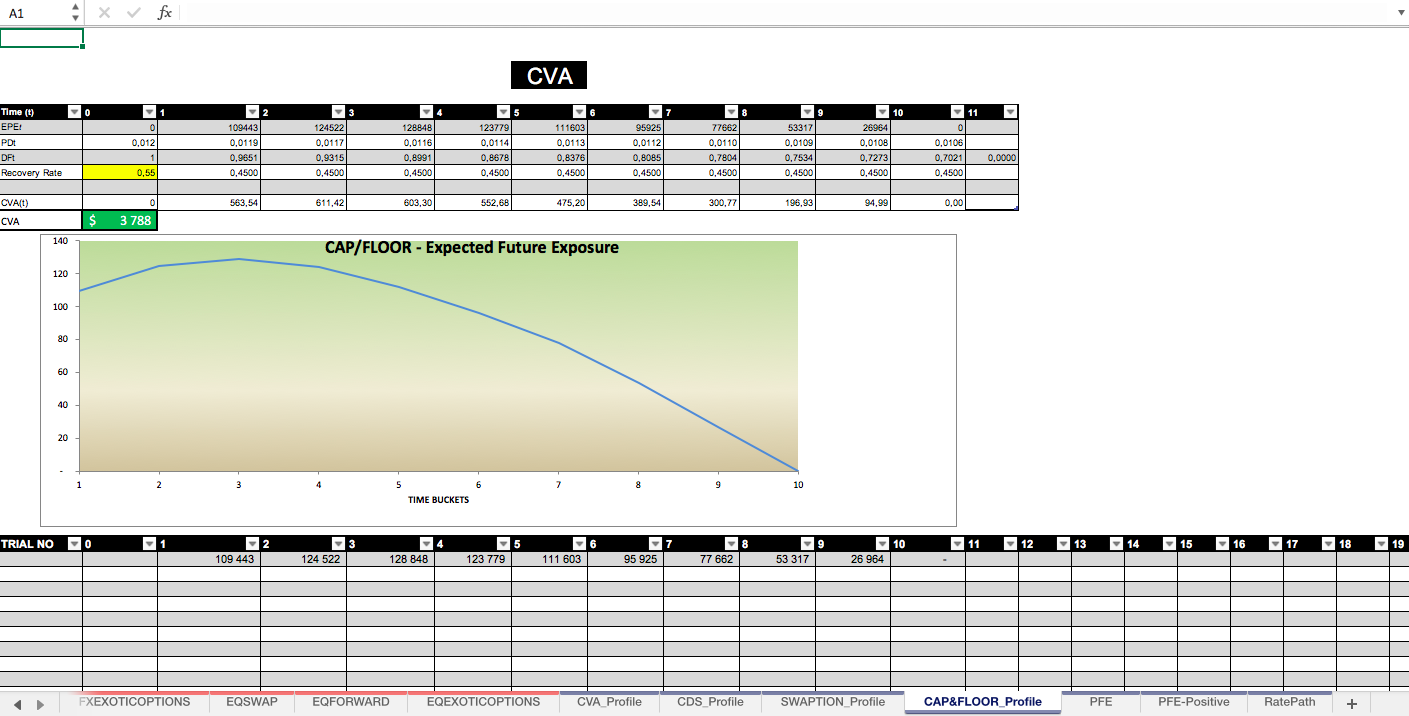

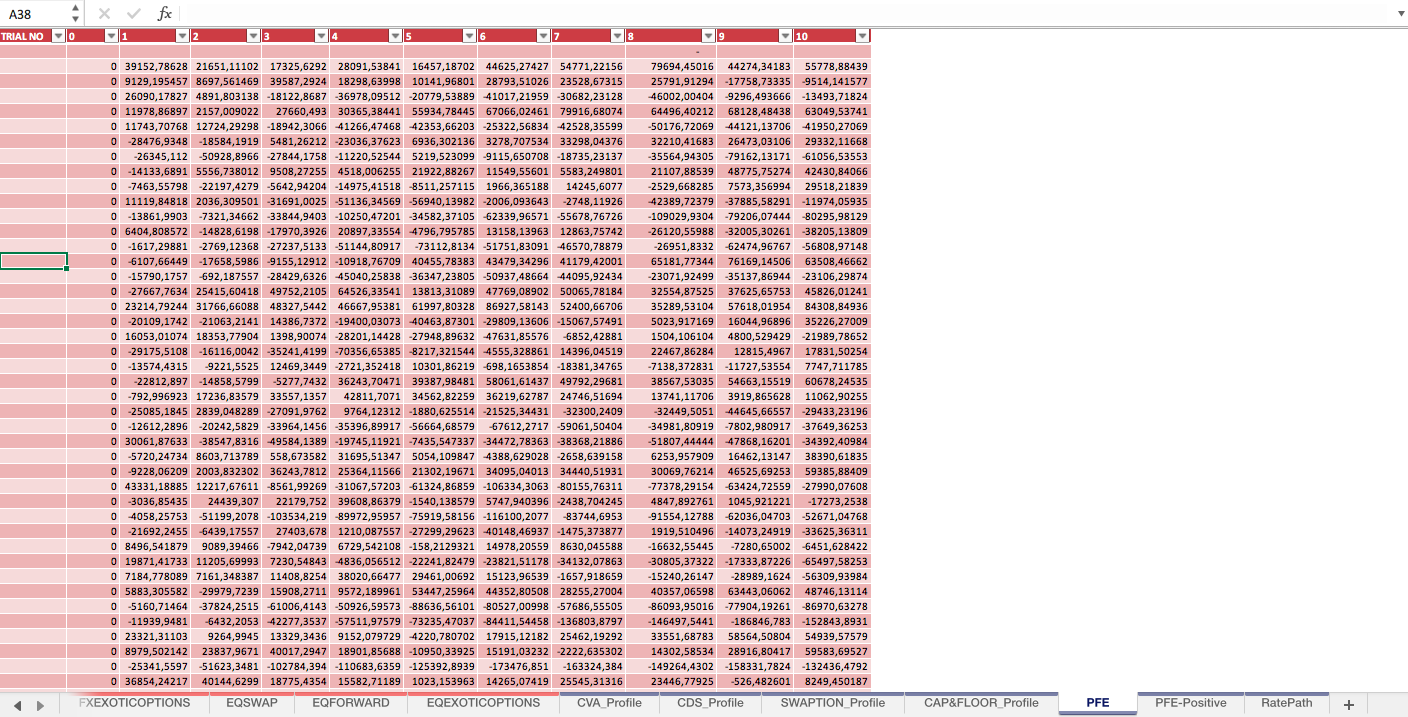

CVA Excel Calculator for Derivatives (Credit Value Adjustment)

Calculation of Credit Value Adjustment and Exposure Metrics

Further information

To compute the Unilateral Credit Value Adjustment for a Bank entering into a derivative contract

To find the credit cost of a counterparty when a bank enters into a derivative contract

It is only good as an approximate.