Originally published: 31/01/2025 08:36

Last version published: 08/01/2026 16:56

Publication number: ELQ-79106-3

View all versions & Certificate

Last version published: 08/01/2026 16:56

Publication number: ELQ-79106-3

View all versions & Certificate

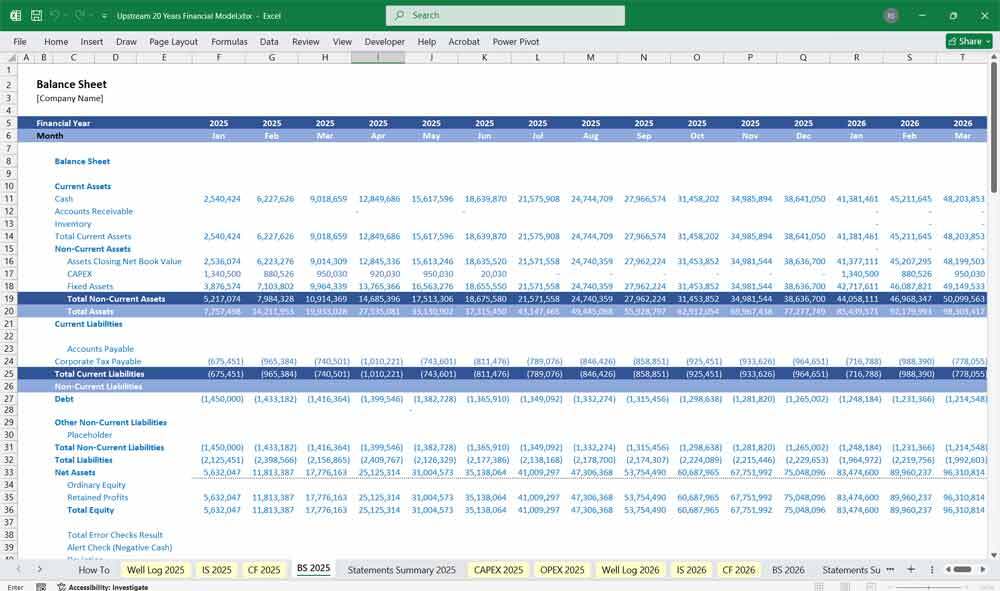

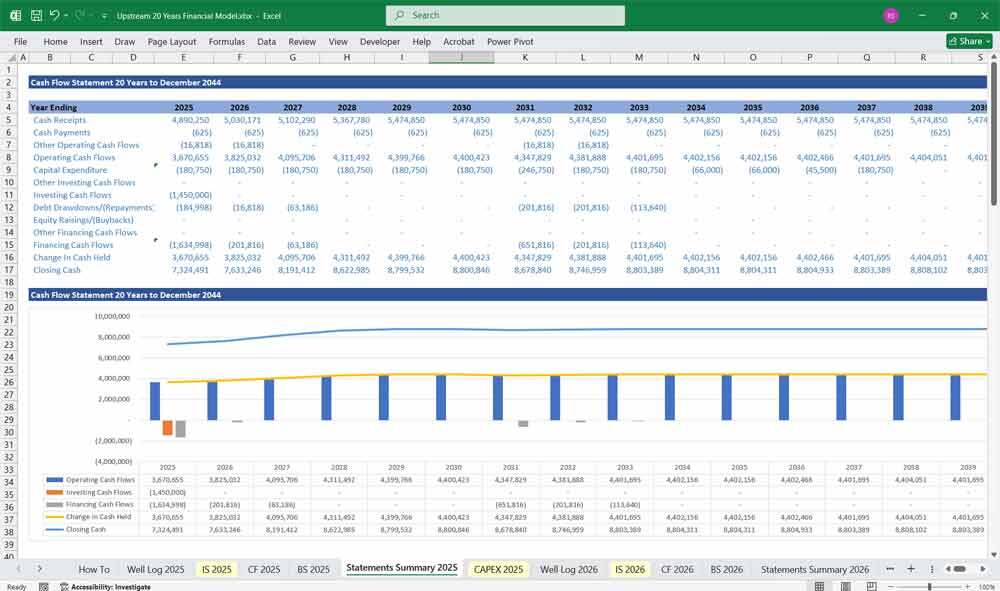

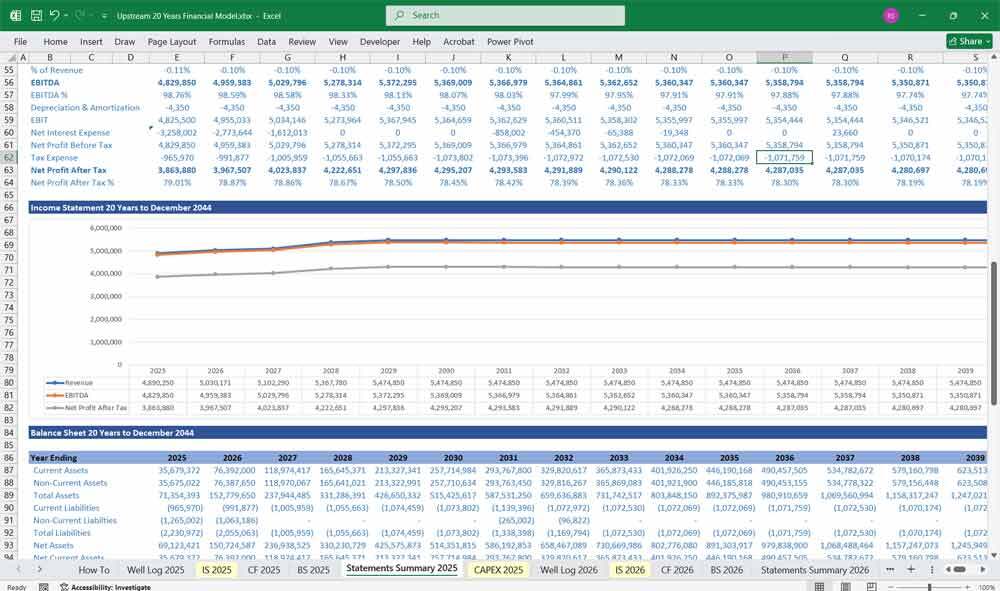

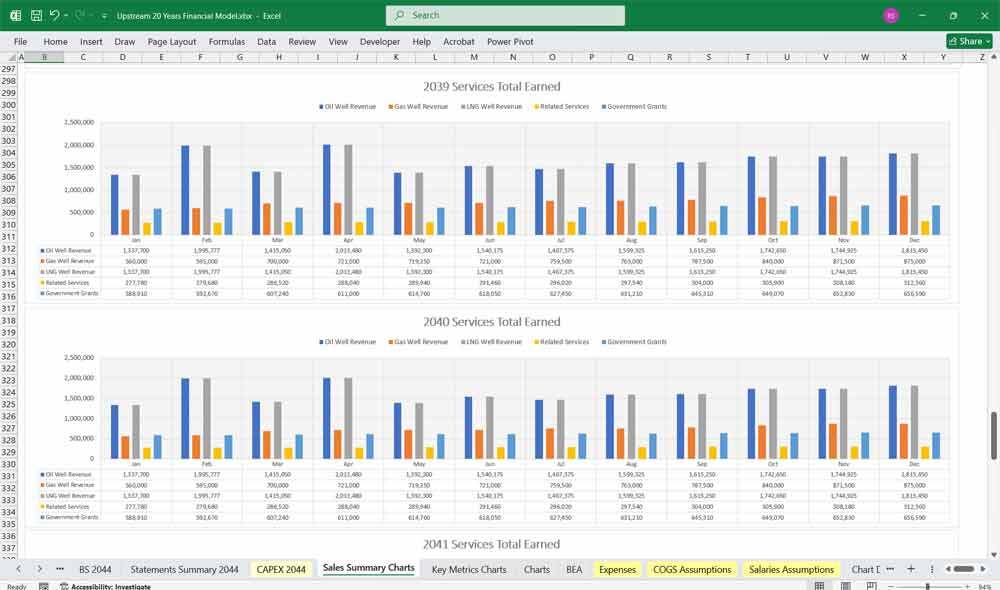

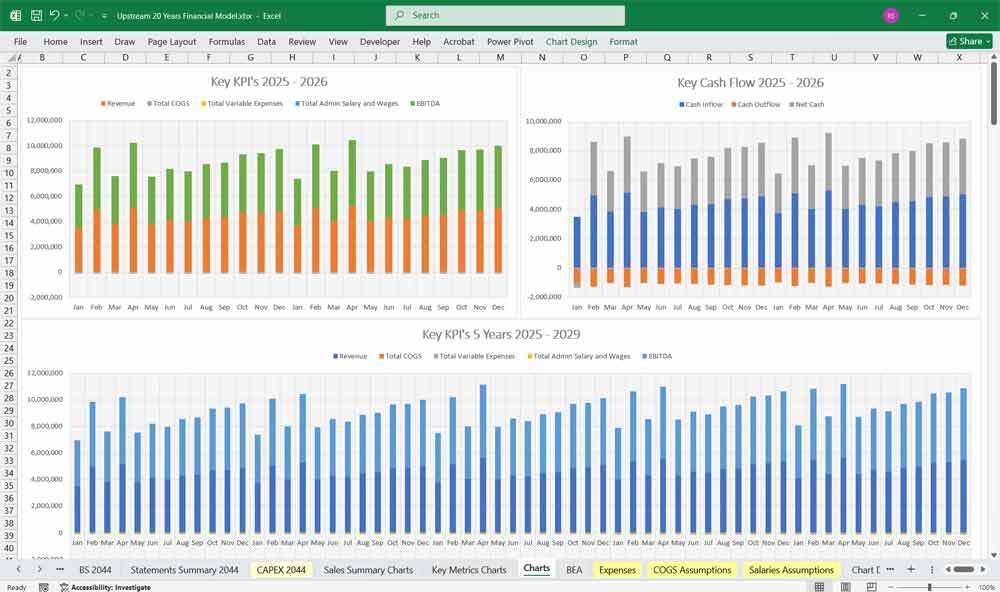

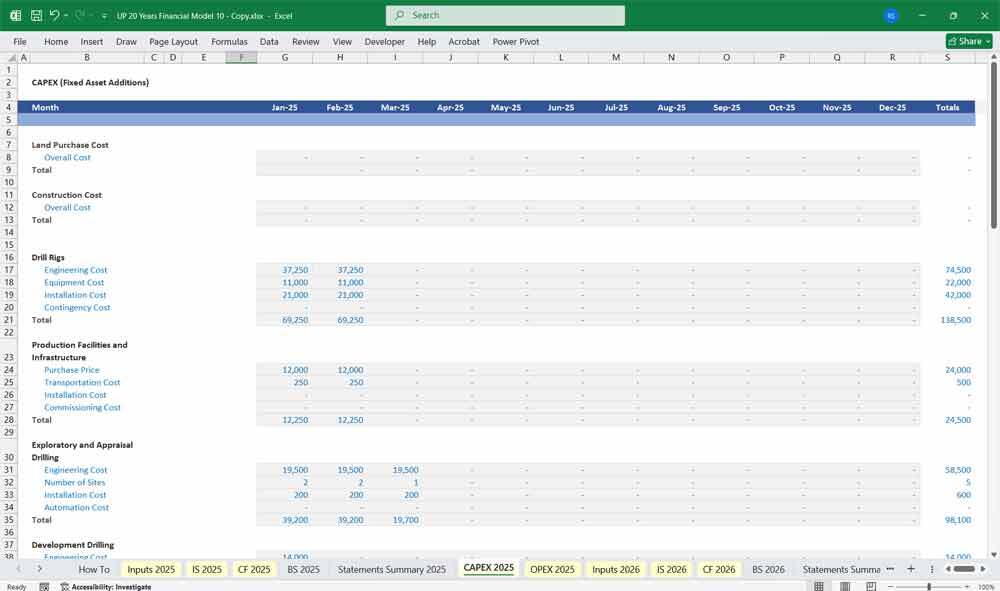

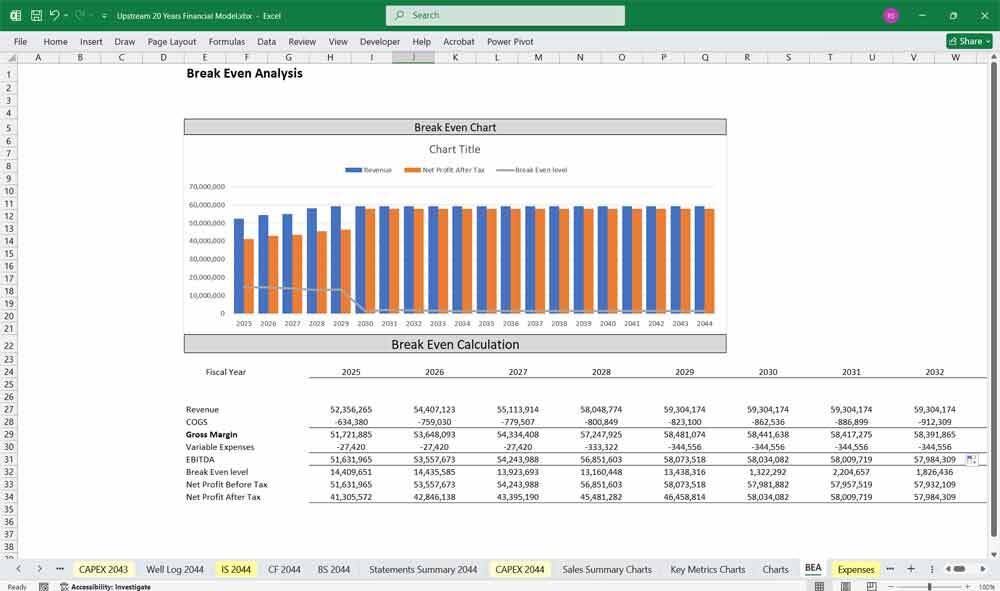

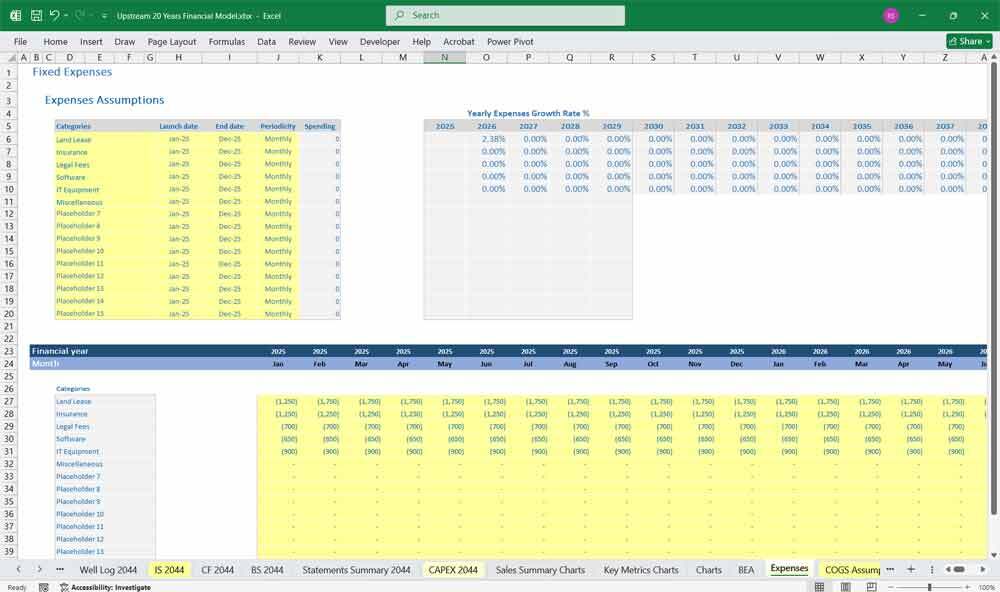

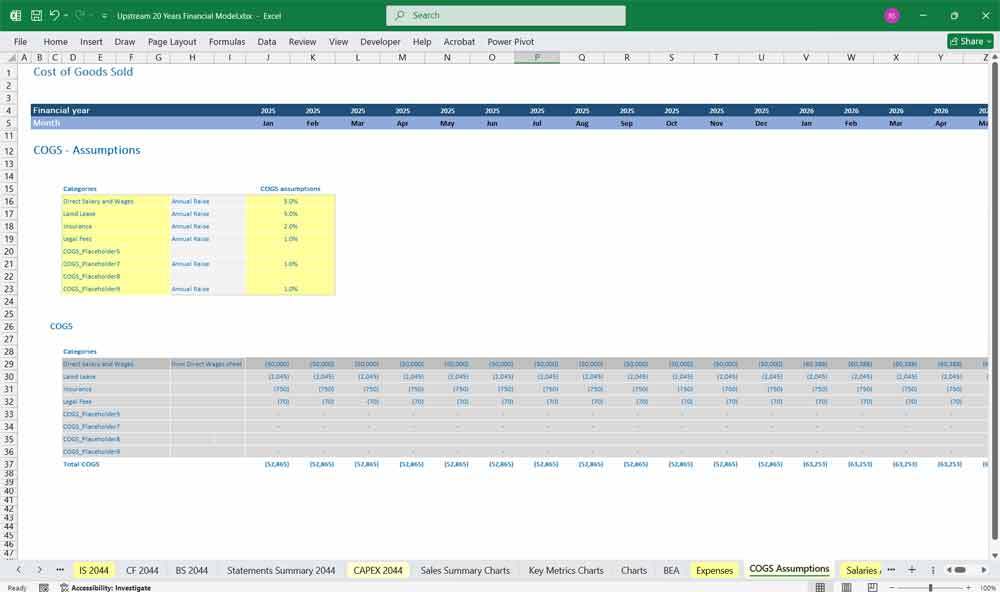

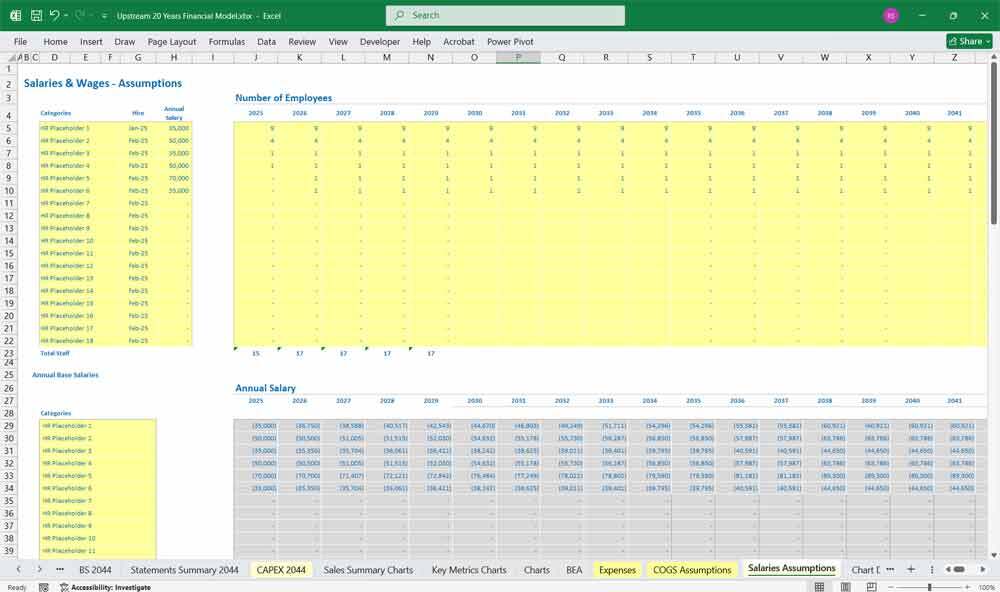

Upstream Oil & Gas Company Financial Model

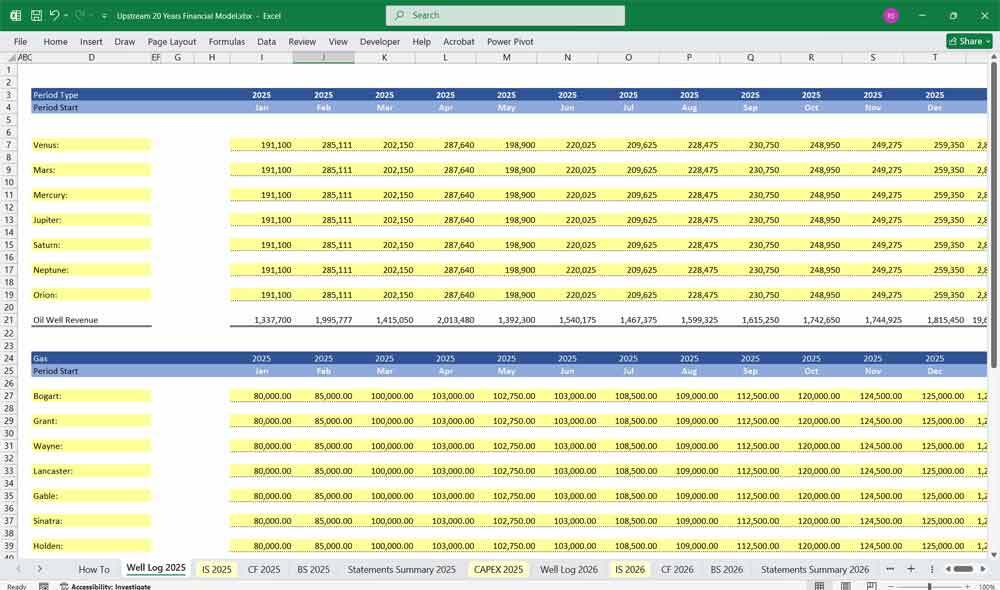

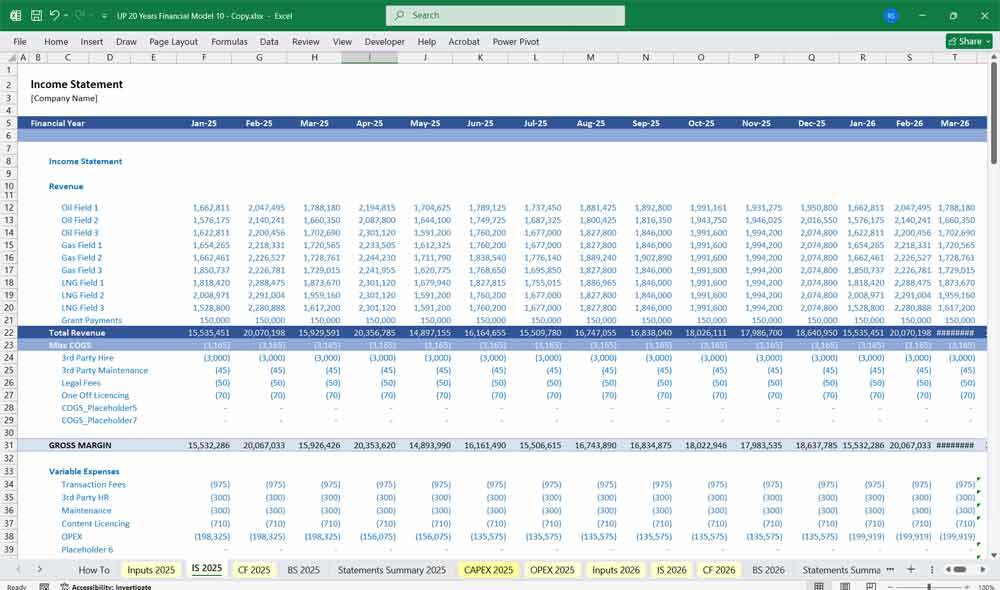

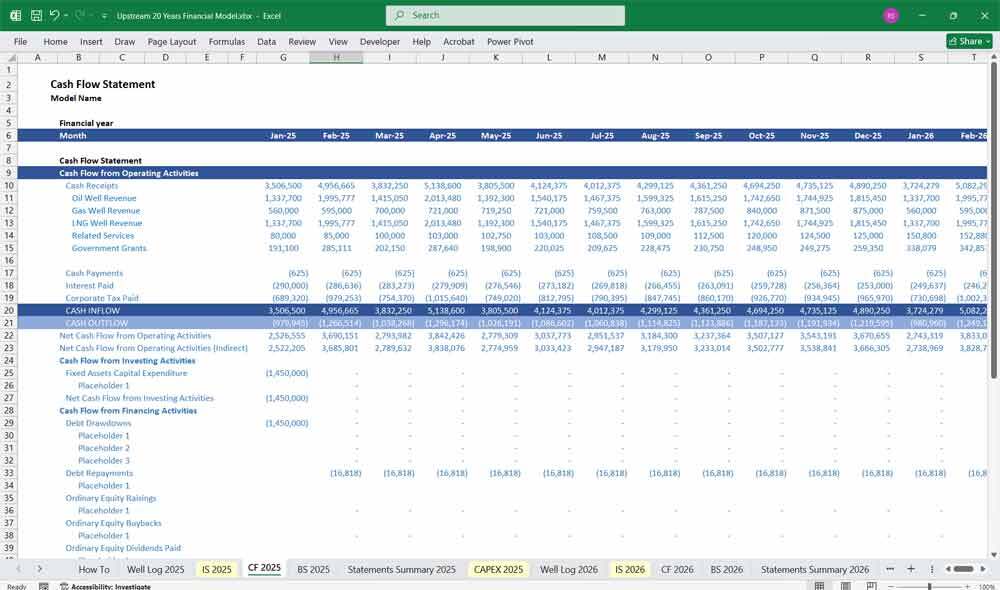

A 20-year 3-statement comprehensive editable, MS Excel spreadsheet for tracking an Upstream Oil and Gas Company's finances

AllFinancialModels offer a curated selection of high-quality yet financial model templates designed to support a wide range of business needs.Follow

Further information

Provides thorough oversight, tracking, and reporting of an Upstream Oil and Gas Company's finances, including updates on budget utilisation and projections.