Publication number: ELQ-33524-1

View all versions & Certificate

Solar PV Residential Model — Evaluate a Home Solar PV Investment in Any of 8 Countries, Including All Local Incentives

Production-ready Excel model for residential solar PV. 8 countries, 3 scenarios, country-specific incentives pre-loaded. Optional BESS.

Further information

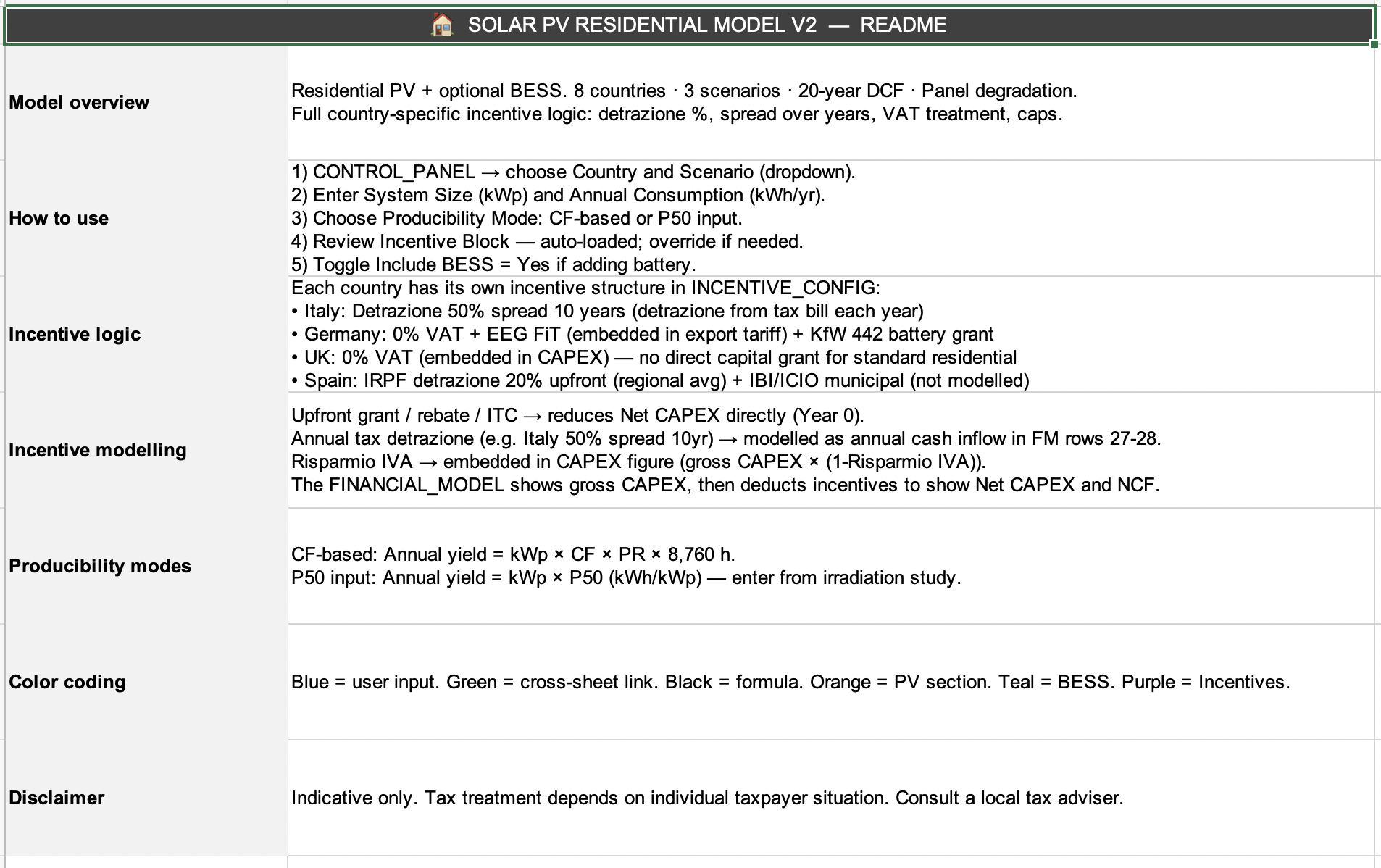

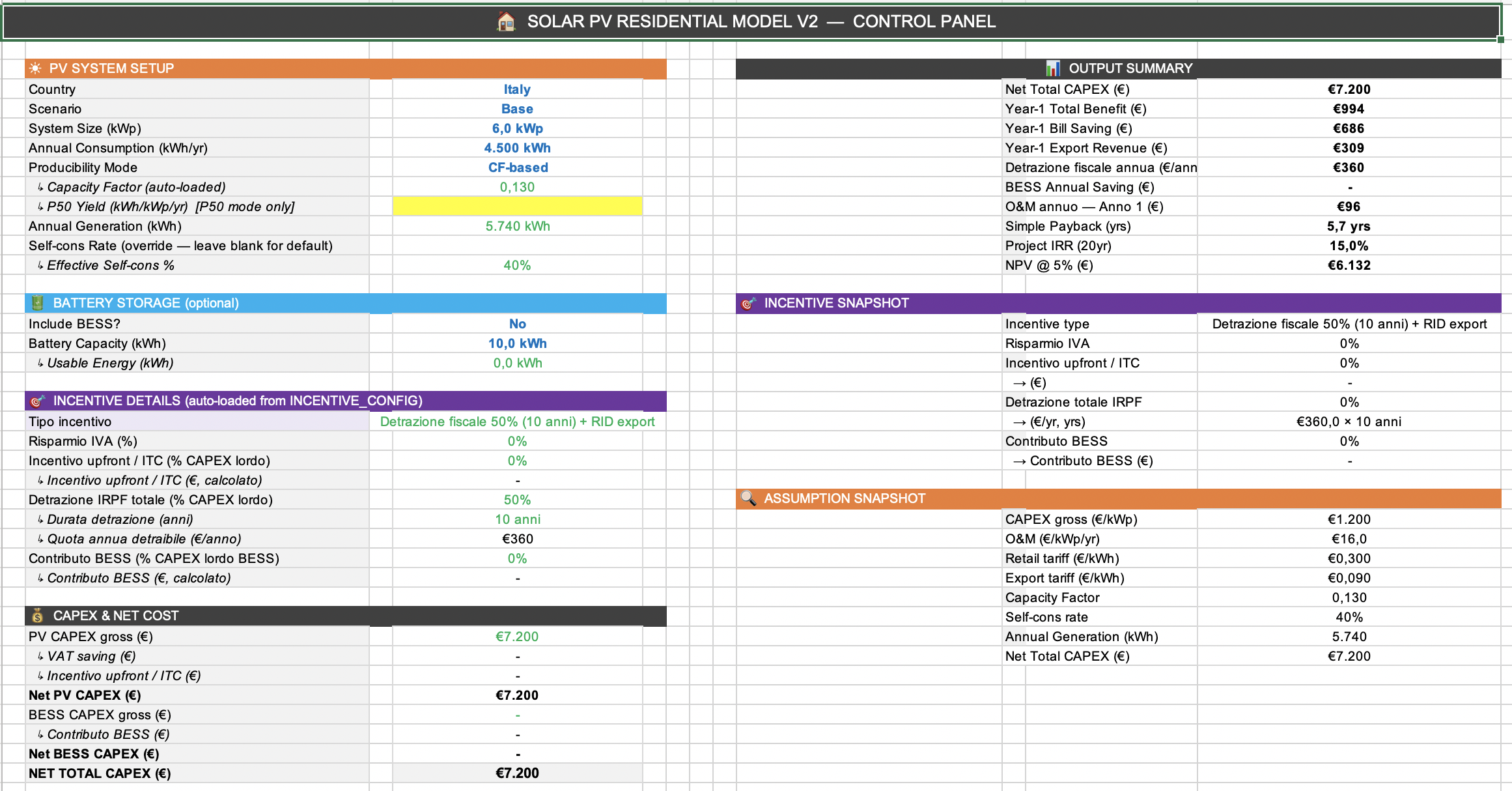

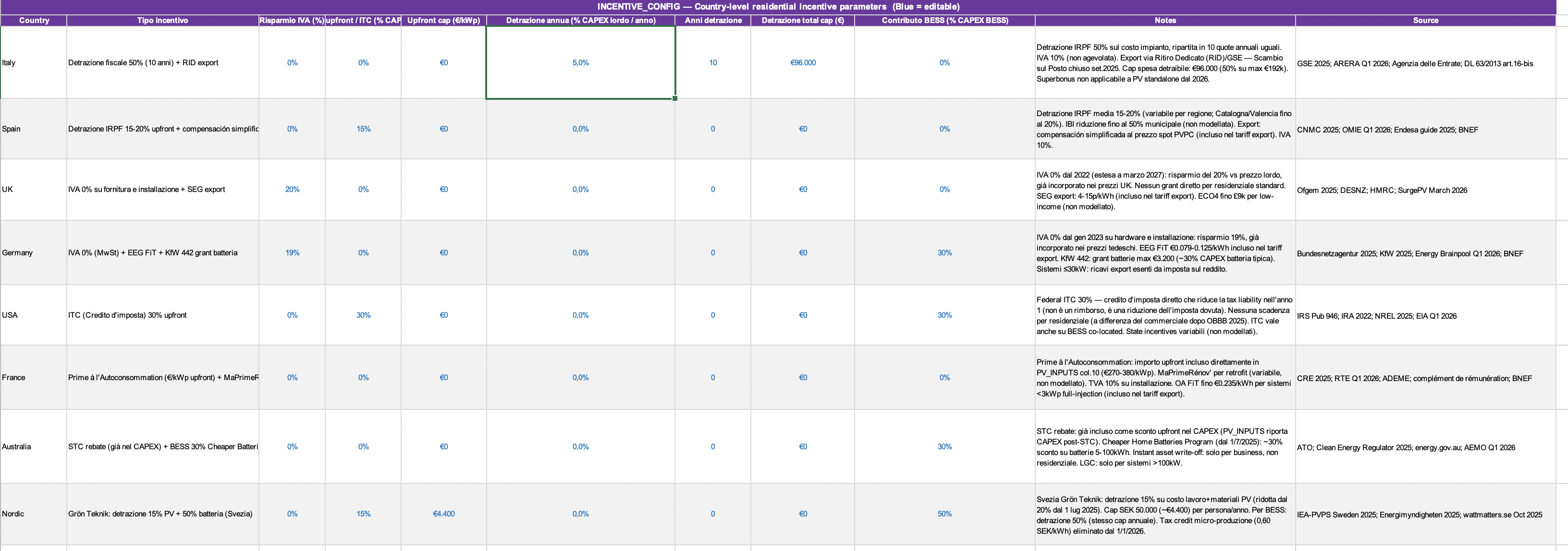

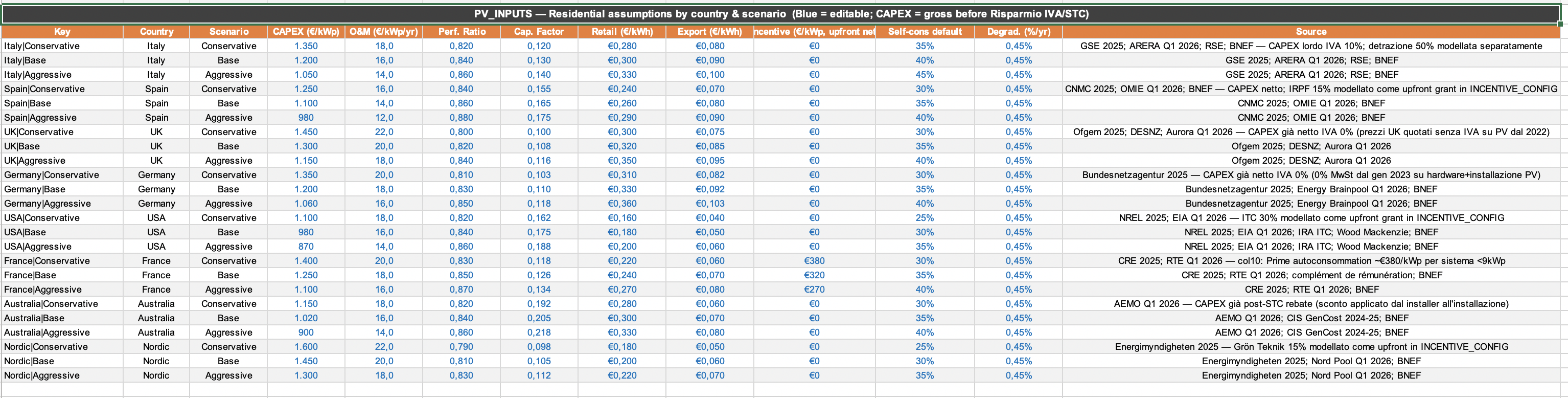

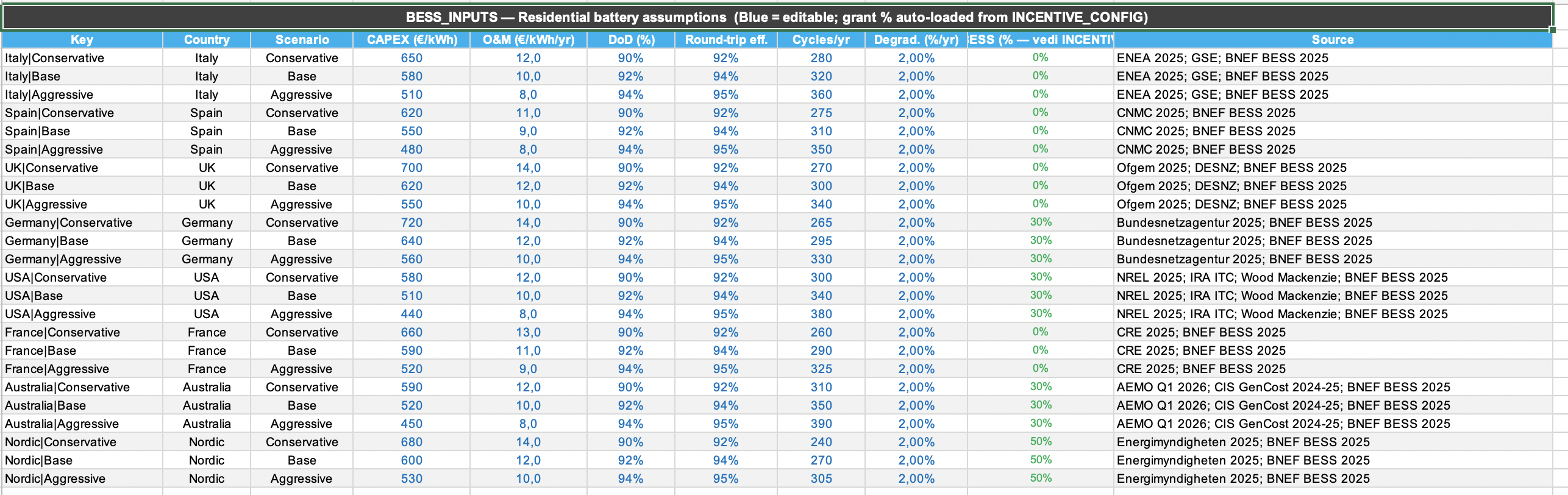

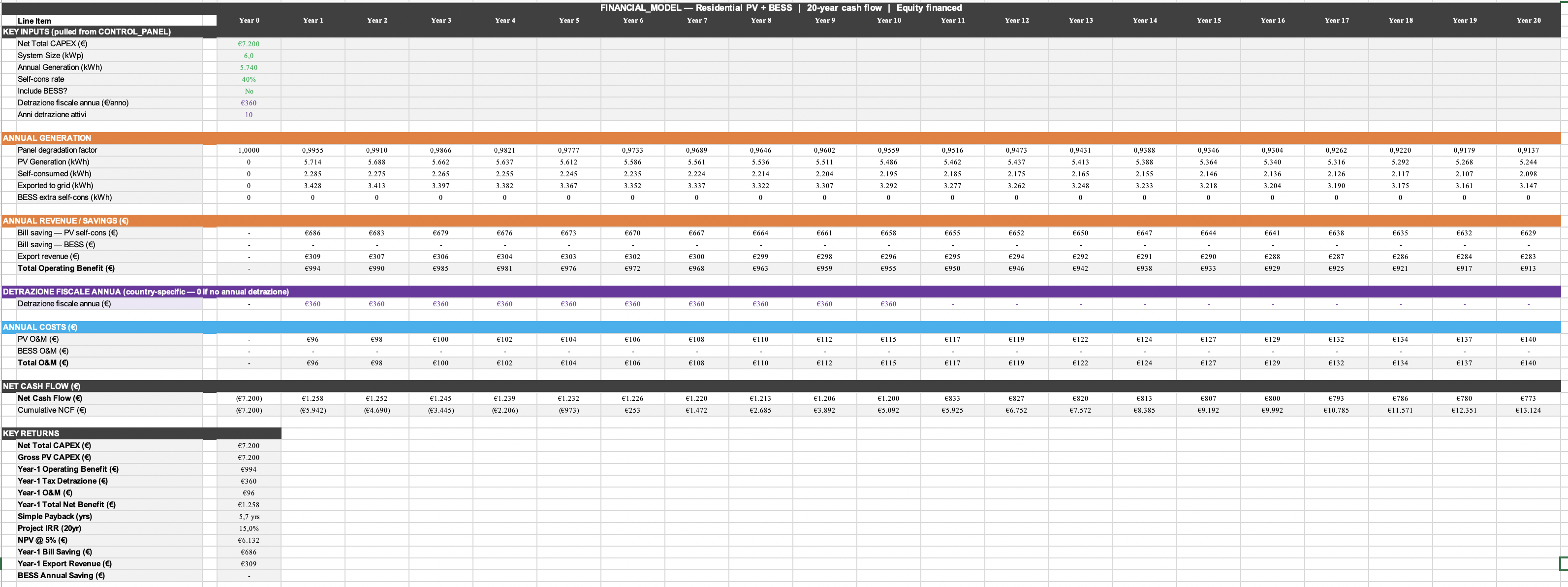

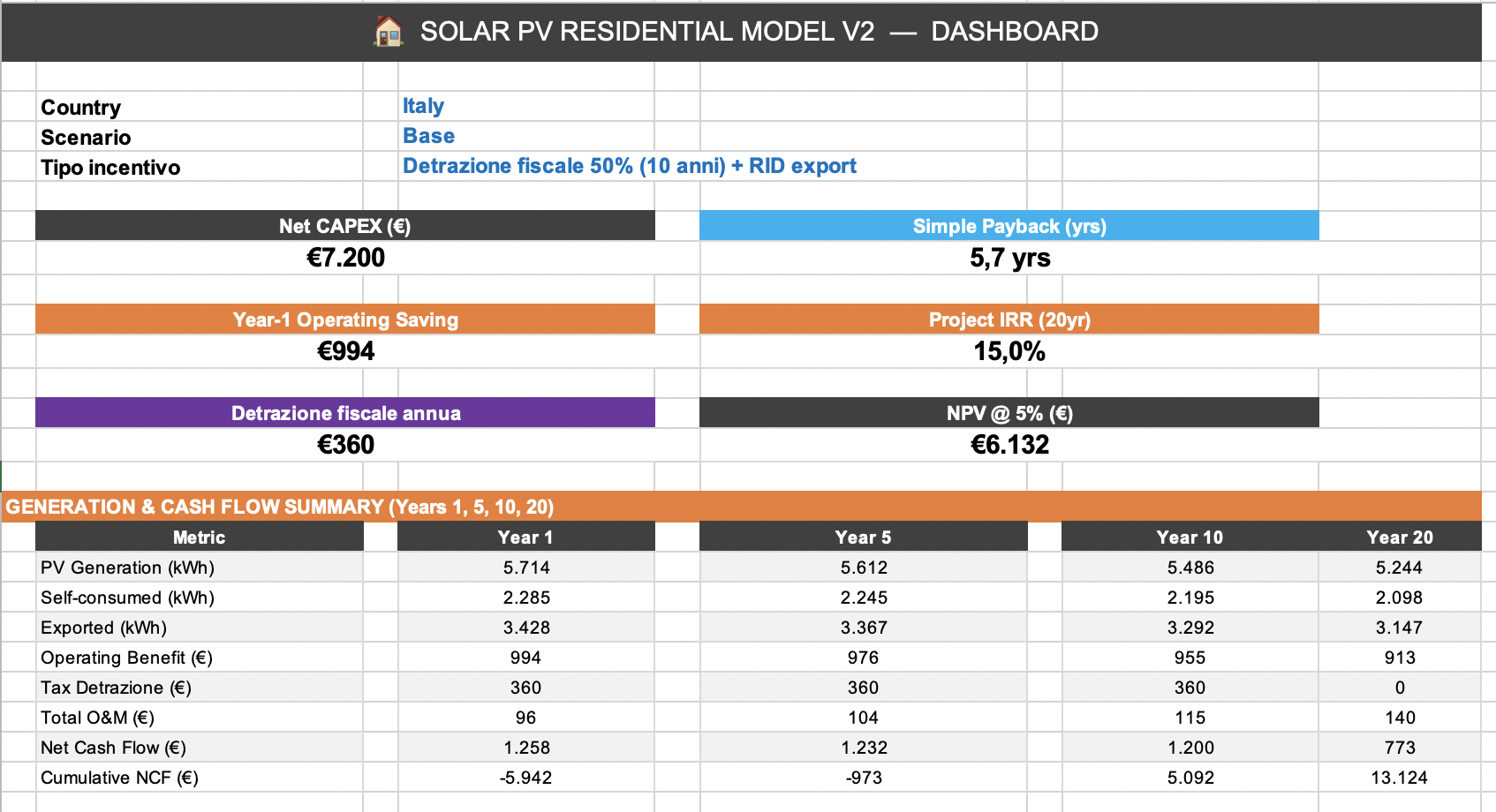

This model enables solar installers, advisors and homeowners to evaluate the financial return of a residential solar PV installation across 8 international markets, correctly modelling each country's specific incentive structure and timing. It calculates annual bill savings on self-consumed energy at country-specific retail tariffs, export revenue at separate feed-in rates, and annual tax deductions or upfront credits according to the applicable mechanism — annual detrazione spread over 10 years for Italy, ITC upfront in year zero for the USA, Prime à l'Autoconsommation paid per kWp for France, and so on. It produces simple payback, Project IRR and NPV from a full 20-year equity cash flow with panel degradation and O&M escalation, and evaluates the incremental value of adding co-located battery storage including applicable battery grants by country.

This model is best suited to standard residential solar PV installations in the 3–15 kWp range at pre-sale or early feasibility stage, where the homeowner is a private individual subject to personal income tax and the incentive is a personal tax deduction, a direct rebate or an upfront grant. It works particularly well for Italy where the annual detrazione timing materially affects the payback profile compared to a simple CAPEX reduction, for the USA where the ITC and any co-located BESS credit significantly compress net cost, and for Australia where the STC rebate and Cheaper Home Batteries Program together can reduce the combined PV and storage outlay substantially. It is also well suited to advisory contexts where the same analysis needs to be replicated across multiple countries for a comparative customer presentation.

This model is designed for private residential customers subject to personal income tax and is not suited to commercial or industrial entities under corporate tax regimes — for those, the Solar PV C&I Model handles the different depreciation and incentive logic. It does not model debt financing and is therefore not appropriate for leveraged residential lending analysis. It should not be used as the sole basis for a tax planning decision: the actual incentive entitlement depends on individual tax liability, property ownership status and local regulatory conditions, and must be confirmed with a qualified local advisor. It is not designed for utility-scale or large commercial systems above approximately 15 kWp, which fall under different tariff and regulatory frameworks in most markets.