Originally published: 07/04/2020 09:13

Last version published: 07/04/2020 12:42

Publication number: ELQ-61850-2

View all versions & Certificate

Last version published: 07/04/2020 12:42

Publication number: ELQ-61850-2

View all versions & Certificate

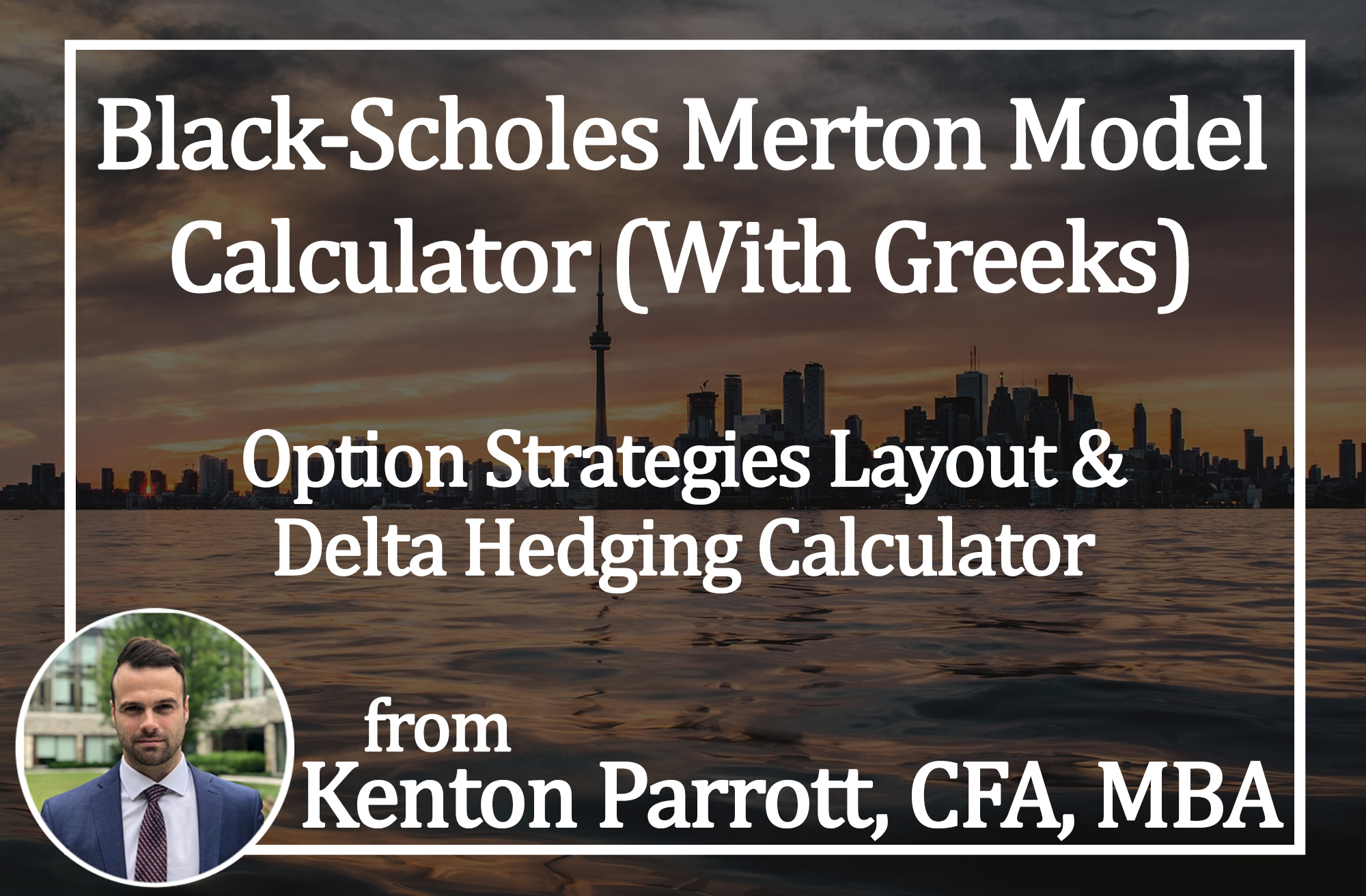

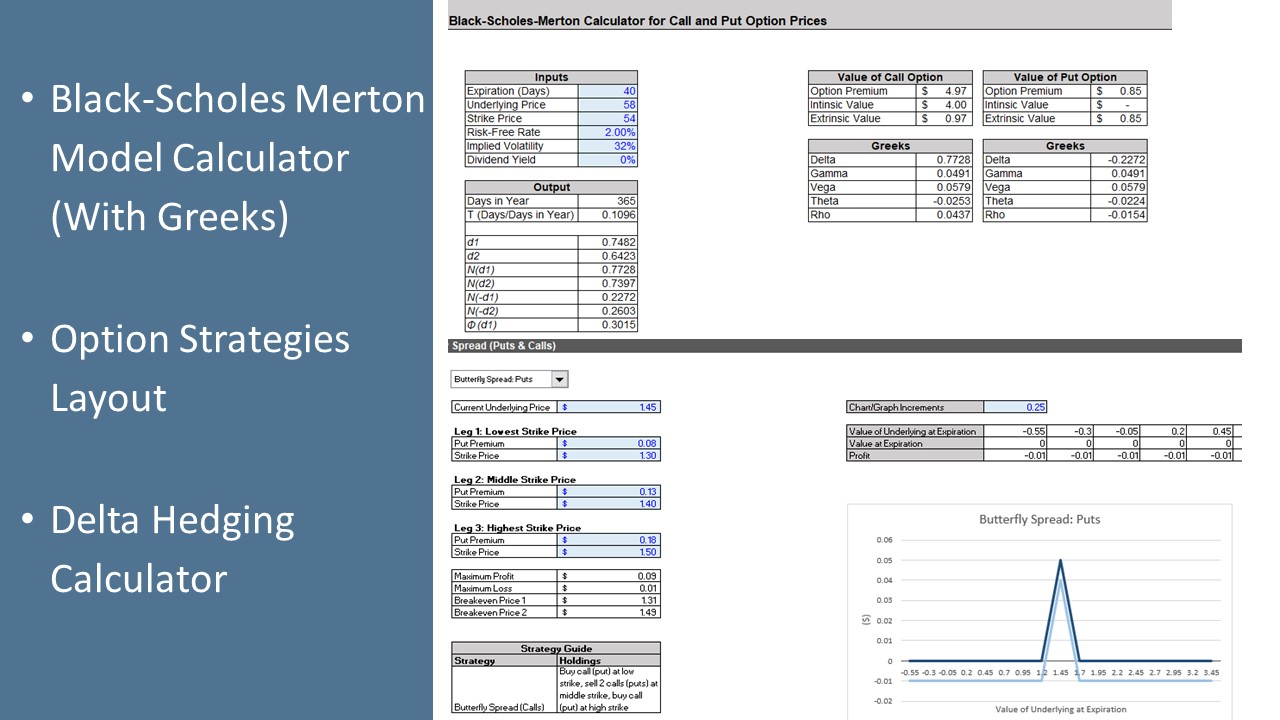

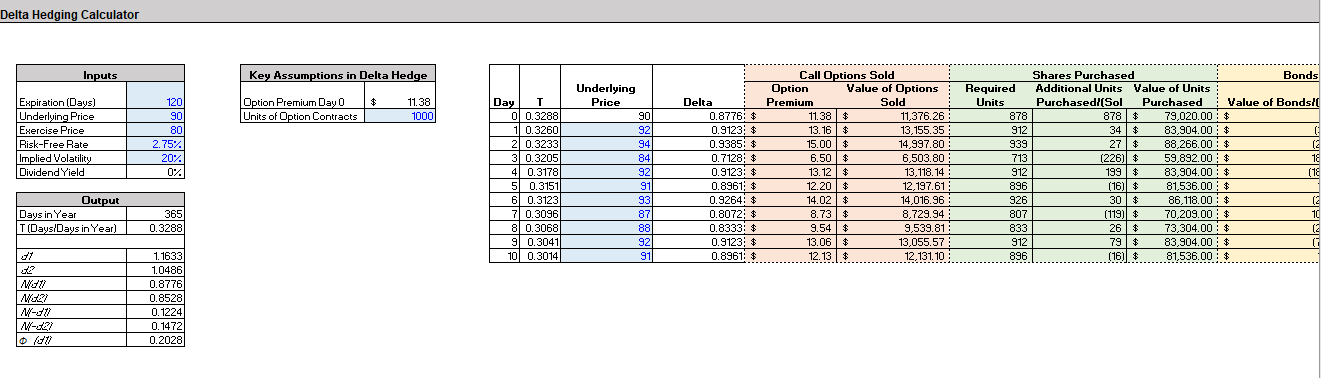

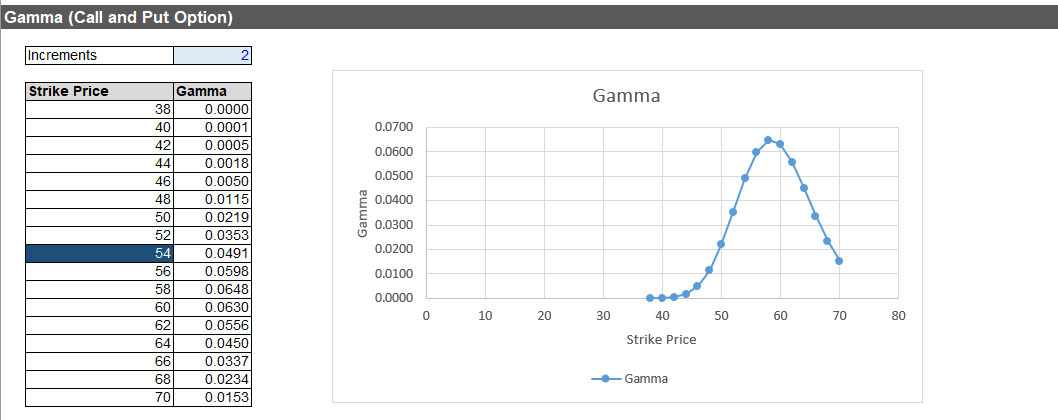

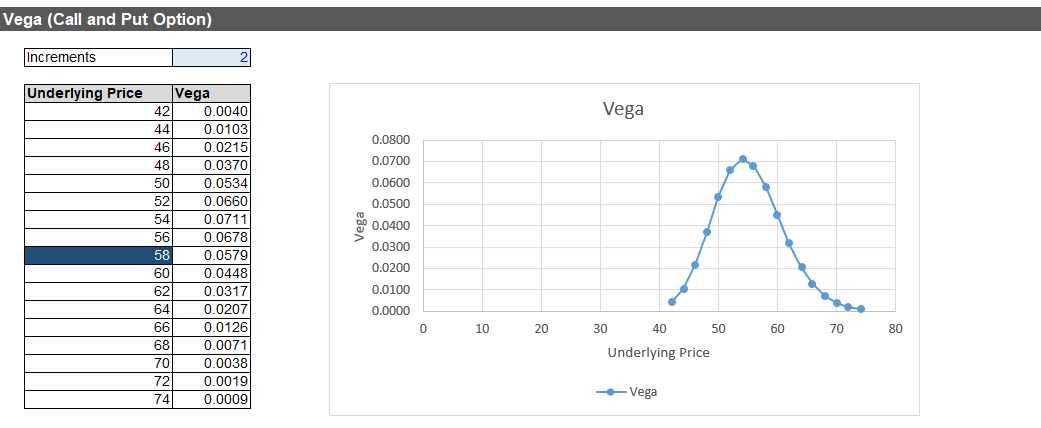

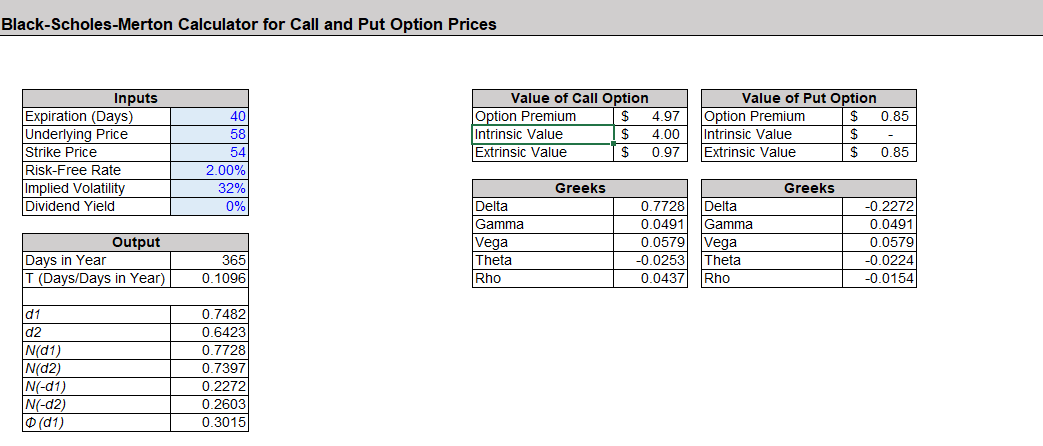

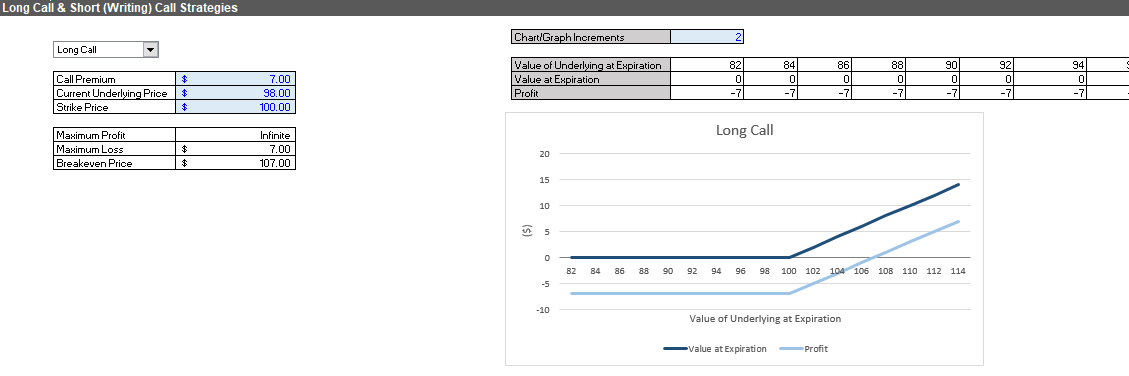

Black-Scholes Merton Model Calculator (With Greeks), Option Strategies Layout and Delta Hedging Calculator

This model can be used by students and professionals to determine the value of options, and specific trading strategies.

Further information

To discover how option prices are derived, as well as an in-depth understanding of the factors that influence option pricing (i.e. The Greeks). Furthermore, this model will help users understand the payoff metrics of multiple option strategies, and gain additional info on how option strategies can be delta-hedged.

Latest edition of Microsoft Excel