Originally published: 23/04/2018 08:56

Publication number: ELQ-96976-1

View all versions & Certificate

Publication number: ELQ-96976-1

View all versions & Certificate

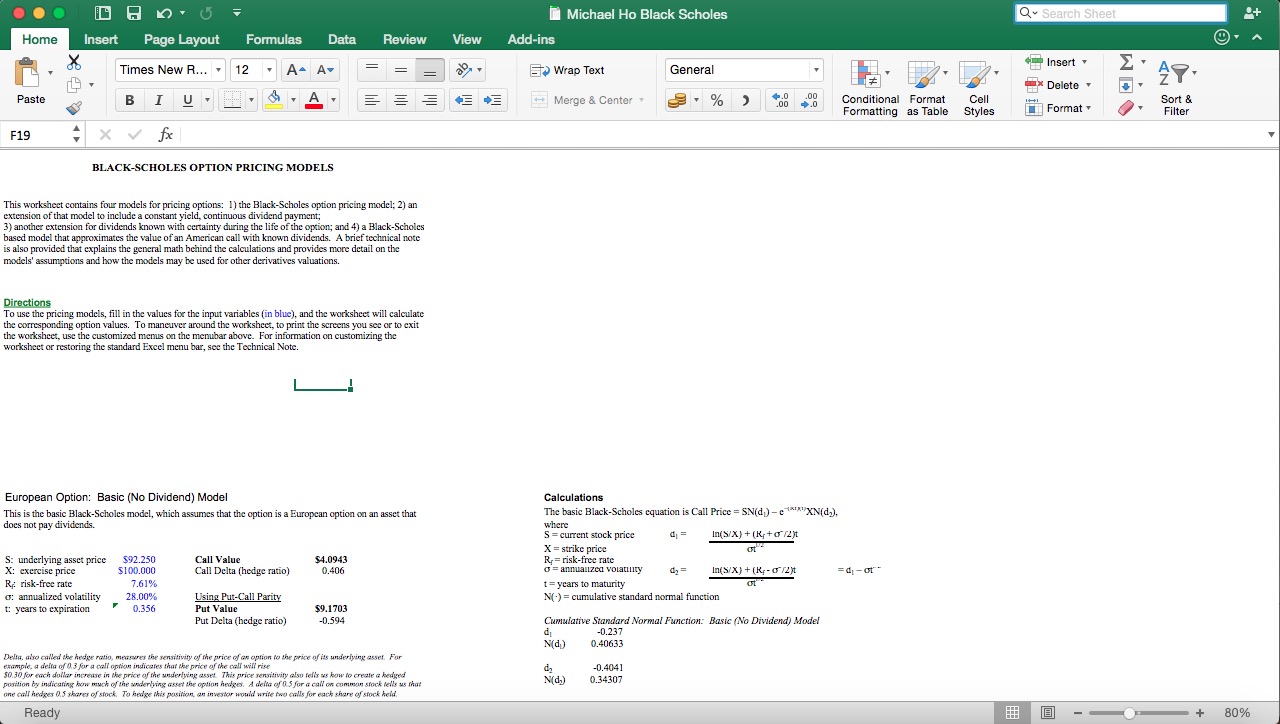

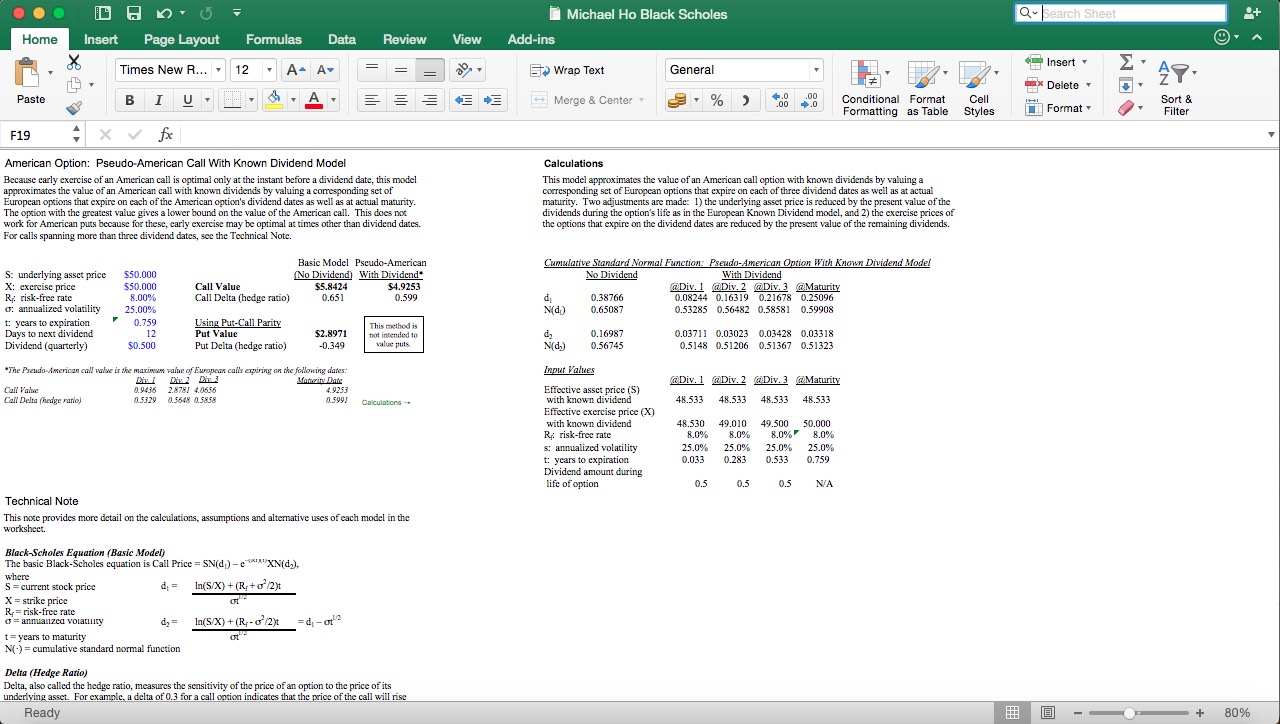

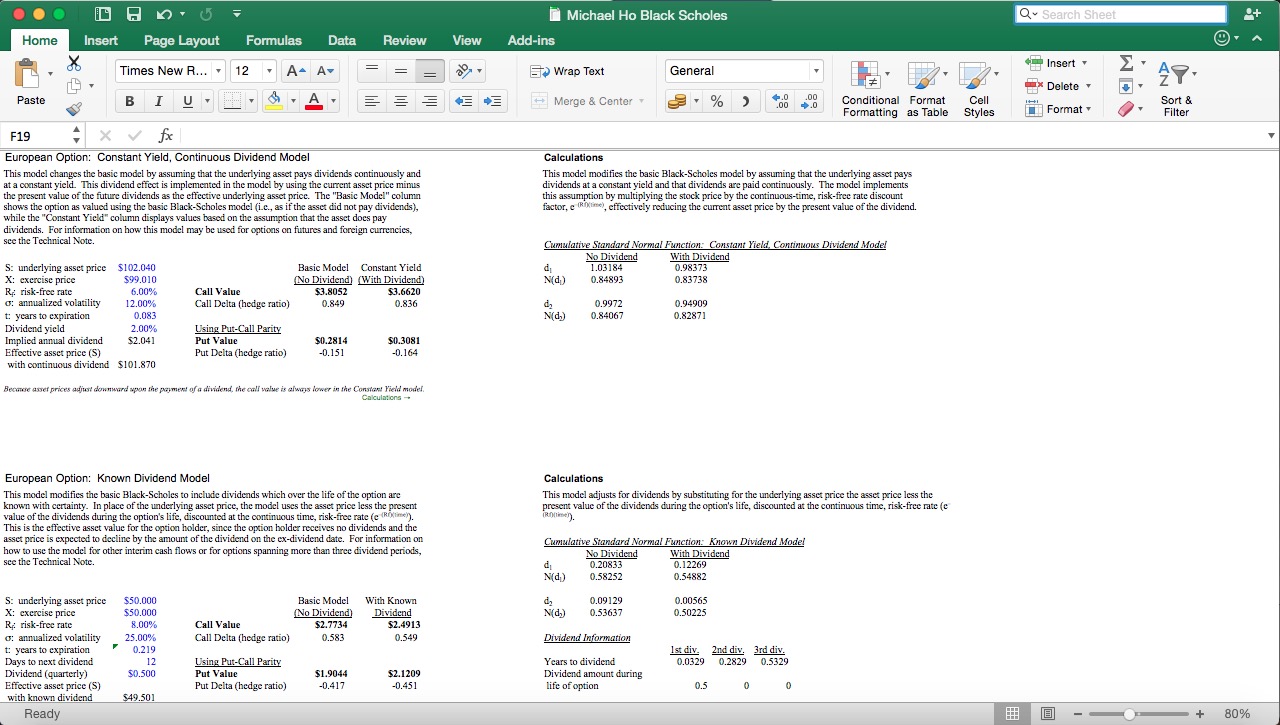

Black-Scholes Option Pricing Models

This document comprises of 4 incredibly useful Black-Scholes option pricing models.