Originally published: 09/09/2024 14:31

Last version published: 17/09/2024 23:35

Publication number: ELQ-98257-2

View all versions & Certificate

Last version published: 17/09/2024 23:35

Publication number: ELQ-98257-2

View all versions & Certificate

Working Capital Schedule

A Working Capital Schedule outlines the short-term assets and liabilities necessary for day-to-day operations.

Description

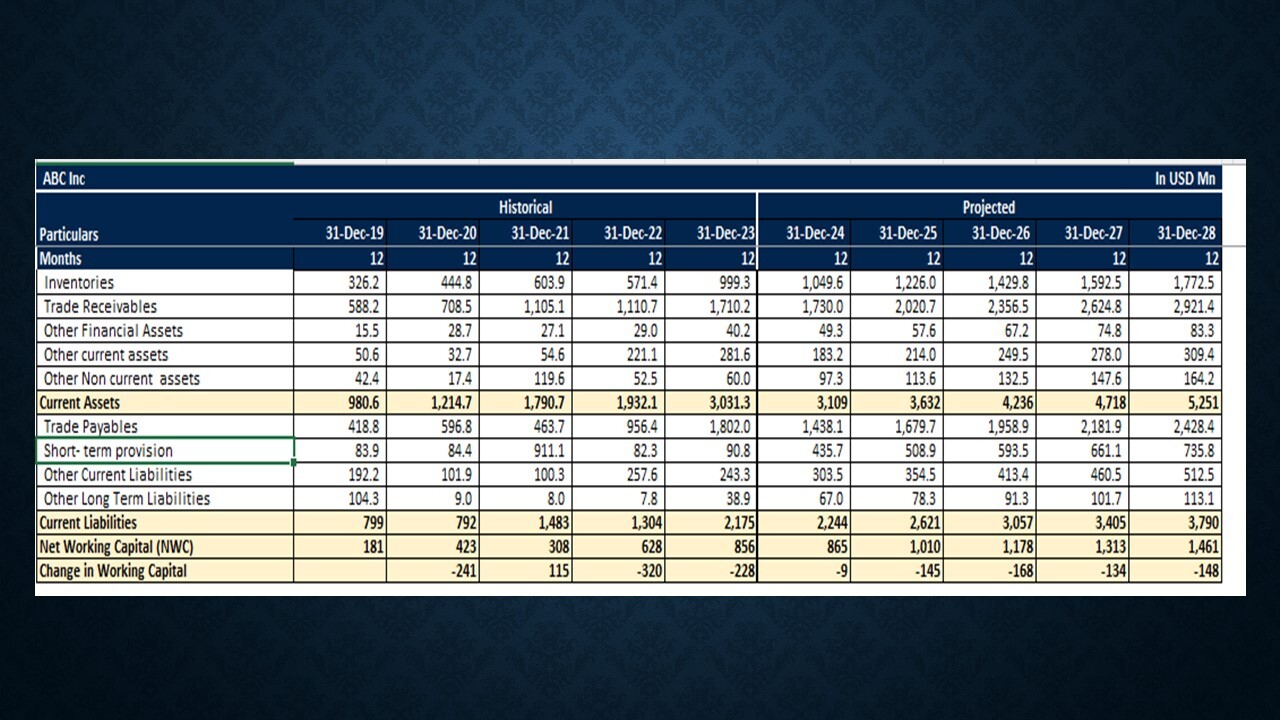

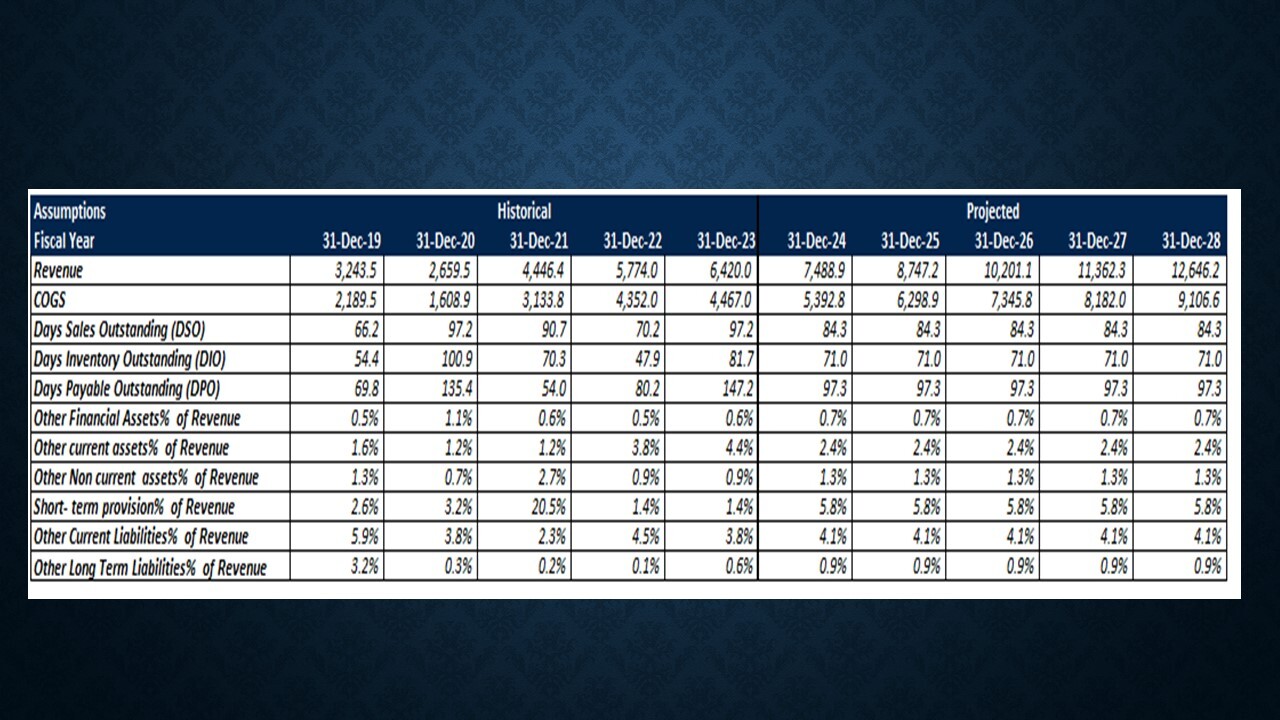

A Working Capital Schedule is a crucial tool for managing a company's short-term assets and liabilities, ensuring smooth day-to-day operations. It focuses on optimizing cash flow, inventory, and receivables and payables to maintain financial stability.To calculate debtors/ (accounts receivable), start by determining the annual revenue and then compute the daily sales by dividing this revenue by 365 days. Next, identify the Days Sales Outstanding (DSO), which reflects the average number of days it takes to collect payments from customers. Multiply the daily sales by the DSO to estimate the total debtors. This calculation helps in understanding how much capital is tied up in receivables and its impact on liquidity.

For creditors/(accounts payable), first, obtain the annual Cost of Goods Sold (COGS) and calculate the daily COGS by dividing this figure by 365 days. Determine the Days Payable Outstanding (DPO), which indicates the average number of days it takes to pay suppliers. By multiplying the daily COGS by the DPO, you can estimate the total creditors. This helps manage the timing of payments to suppliers and optimize cash flow.

When calculating inventory, start with the annual COGS and compute the daily COGS as described earlier. Identify the Days Inventory Outstanding (DIO), which is the average number of days it takes to sell inventory. Multiply the daily COGS by the DIO to estimate the inventory levels. This calculation helps in managing stock levels and ensuring that inventory investment aligns with sales cycles.Overall, the Working Capital Schedule provides valuable insights into cash flow management, operational efficiency, and financial planning, ensuring that the company has the necessary liquidity to meet short-term obligations and optimize its operational performance.

To simplify forecasting, all other current assets and liabilities are projected based on a percentage of revenue. This approach streamlines the budgeting process by applying a consistent, revenue-based percentage to estimate items such as prepaid expenses, short-term investments, and other receivables, as well as accrued expenses and other payables. This method ensures alignment with overall revenue growth while maintaining ease of use and clarity in financial planning, allowing for a straightforward and scalable approach to managing short-term financial elements.

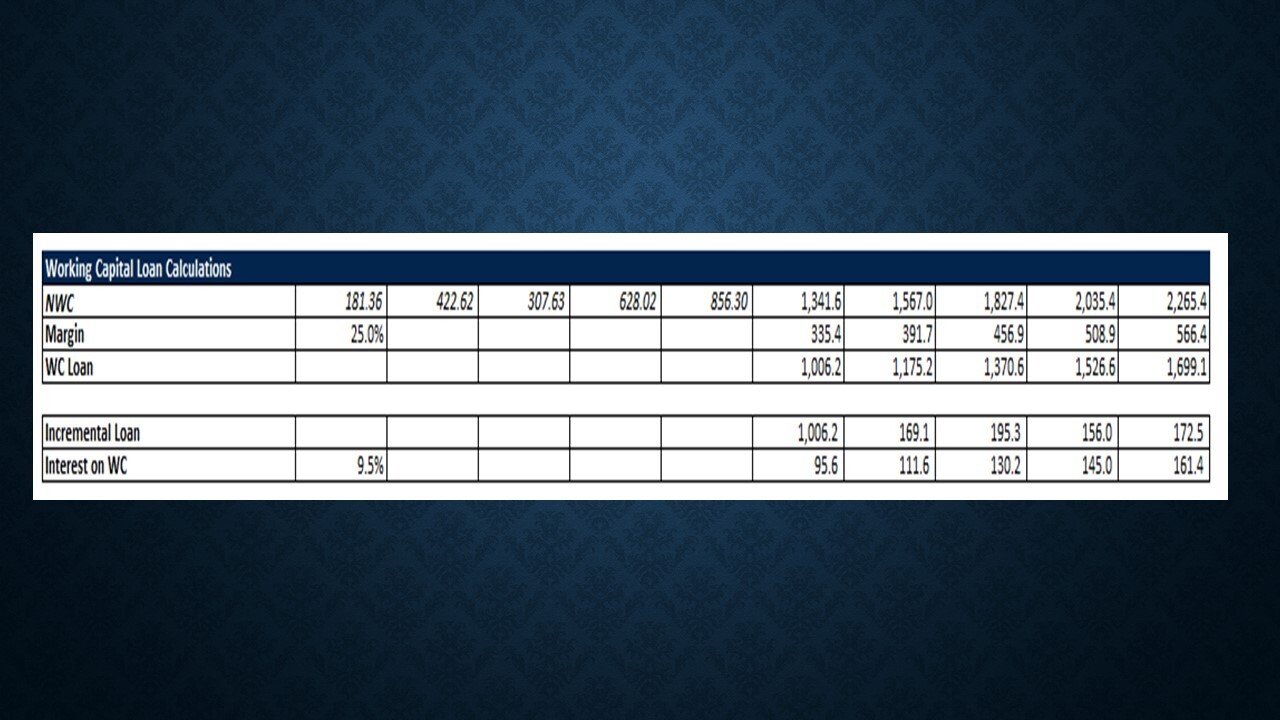

This model also incorporates the treatment of working capital loan calculations.

A Working Capital Schedule is a crucial tool for managing a company's short-term assets and liabilities, ensuring smooth day-to-day operations. It focuses on optimizing cash flow, inventory, and receivables and payables to maintain financial stability.To calculate debtors/ (accounts receivable), start by determining the annual revenue and then compute the daily sales by dividing this revenue by 365 days. Next, identify the Days Sales Outstanding (DSO), which reflects the average number of days it takes to collect payments from customers. Multiply the daily sales by the DSO to estimate the total debtors. This calculation helps in understanding how much capital is tied up in receivables and its impact on liquidity.

For creditors/(accounts payable), first, obtain the annual Cost of Goods Sold (COGS) and calculate the daily COGS by dividing this figure by 365 days. Determine the Days Payable Outstanding (DPO), which indicates the average number of days it takes to pay suppliers. By multiplying the daily COGS by the DPO, you can estimate the total creditors. This helps manage the timing of payments to suppliers and optimize cash flow.

When calculating inventory, start with the annual COGS and compute the daily COGS as described earlier. Identify the Days Inventory Outstanding (DIO), which is the average number of days it takes to sell inventory. Multiply the daily COGS by the DIO to estimate the inventory levels. This calculation helps in managing stock levels and ensuring that inventory investment aligns with sales cycles.Overall, the Working Capital Schedule provides valuable insights into cash flow management, operational efficiency, and financial planning, ensuring that the company has the necessary liquidity to meet short-term obligations and optimize its operational performance.

To simplify forecasting, all other current assets and liabilities are projected based on a percentage of revenue. This approach streamlines the budgeting process by applying a consistent, revenue-based percentage to estimate items such as prepaid expenses, short-term investments, and other receivables, as well as accrued expenses and other payables. This method ensures alignment with overall revenue growth while maintaining ease of use and clarity in financial planning, allowing for a straightforward and scalable approach to managing short-term financial elements.

This model also incorporates the treatment of working capital loan calculations.

This Best Practice includes

1 Excel File