Originally published: 17/07/2026 12:54

Publication number: ELQ-97924-1

View all versions & Certificate

Publication number: ELQ-97924-1

View all versions & Certificate

RIA / Wealth-Management Practice Acquisition & SBA Underwriting Financial Model

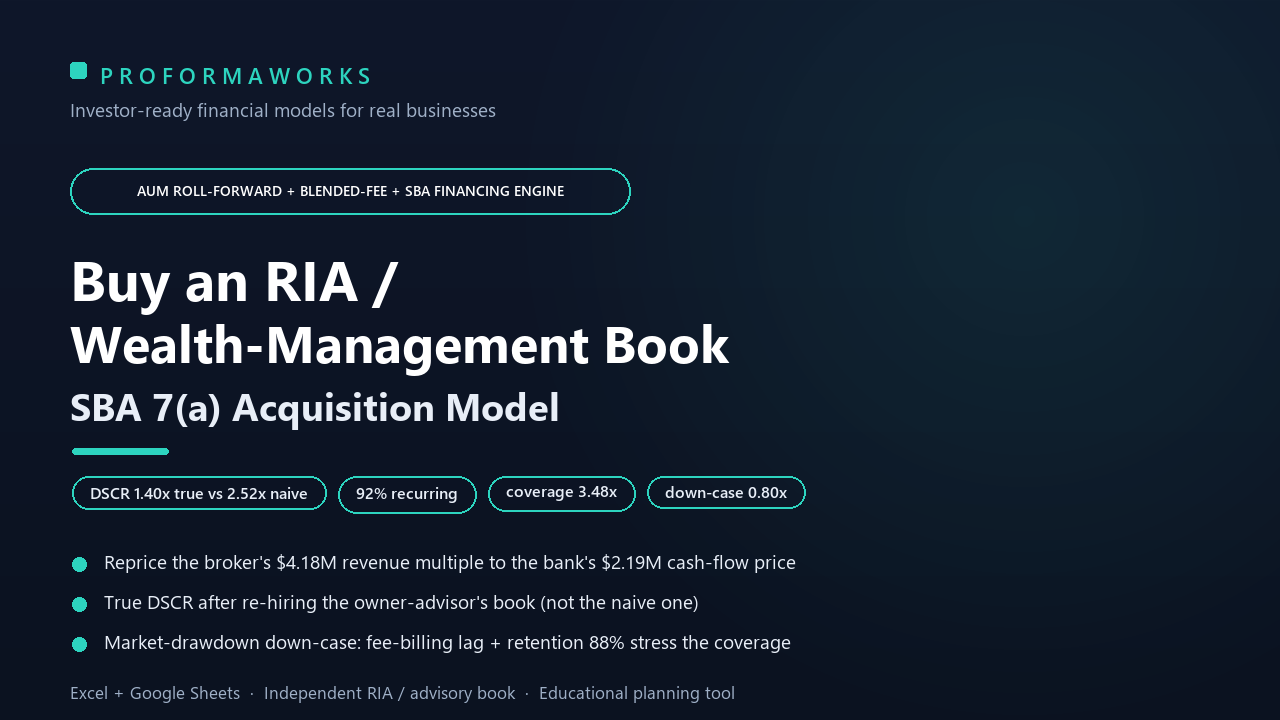

Underwrite an RIA book the way a lender will: AUM roll-forward, retention, market-drawdown and an SBA DSCR gate - broker's 2.2x-revenue price vs cash-flow.

- START HERE - quick start and how to drive the model

- Setup Inputs - AUM, blended fee schedule, revenue mix, retention, cost stack, 3 profile toggles

- AUM & Fee Engine - AUM roll-forward (market + net flows) x graduated blended fee; two-price panel

- Retention & Transition - transition-year haircut, retention roll-forward, earnout benchmark

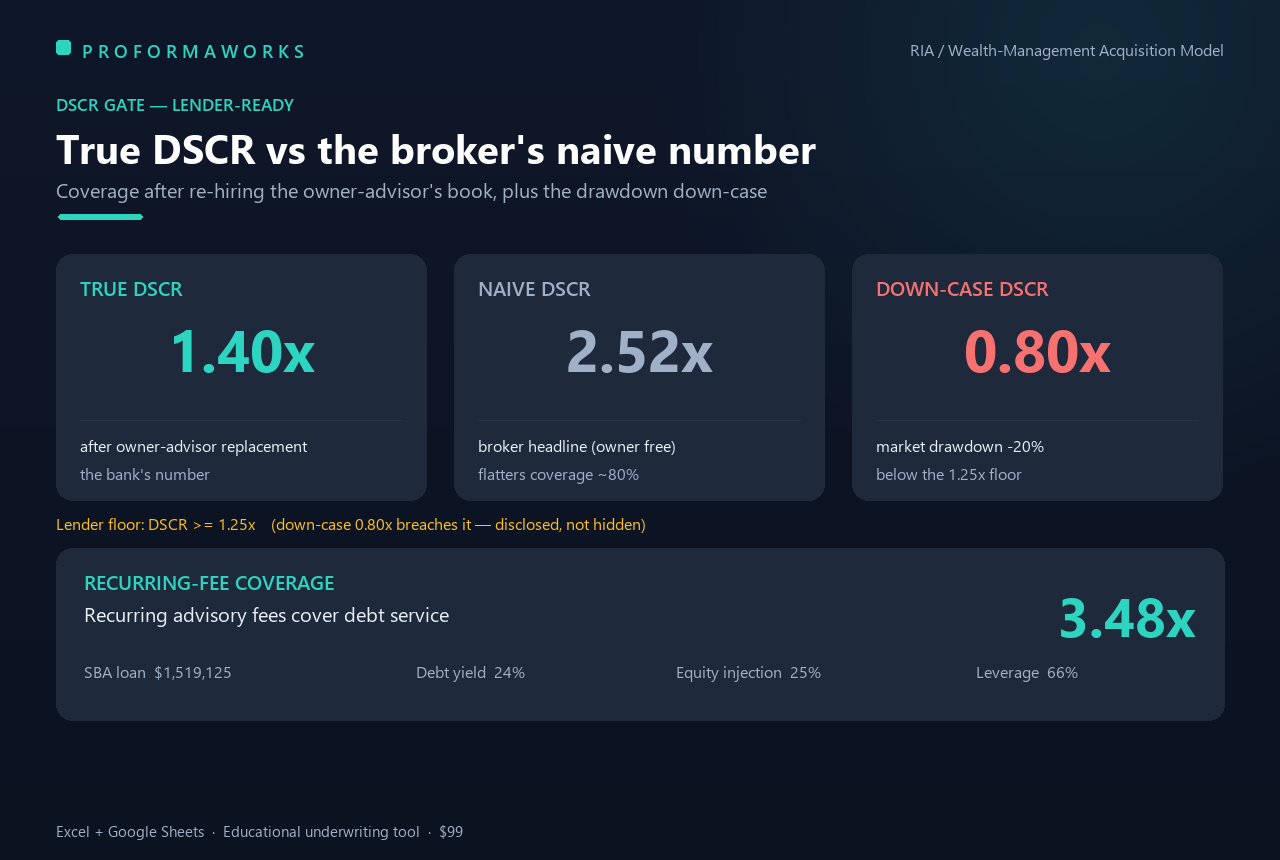

- SDE & Valuation - SDE bottom-up, owner-advisor replacement, Adjusted EBITDA, revenue-multiple vs cash-flow price

- Sources & Uses - SBA 7(a) capital stack sized to DSCR, seller note full-standby vs amortizing

- P&L 5-Year

- DSCR & Debt - true vs naive DSCR, recurring-fee coverage, debt yield, market-drawdown down-case, amortisation schedule

- Returns & Exit - cash-on-cash, 5-year multiple, honest note on IRR

- Dashboard - KPI cards and bankability grid

- Benchmarks & Sources - sourced RIA multiples, fee schedules, margins, SBA terms

Further information

- Price a wealth-management book on the cash flow a lender accepts, not on the broker 2.2x-recurring-revenue headline

- Build recurring advisory revenue bottom-up from an AUM roll-forward and a graduated blended fee

- See the true DSCR next to the naive one, after replacing the owner-advisor production

- Stress the book for a market drawdown and transition-year attrition before signing the LOI

- Structure and size an SBA 7(a) stack to the DSCR floor

- You are a solo or junior advisor buying a retiring advisor book (silver tsunami succession)

- You are an aggregator or RIA doing an add-on acquisition and need a lender-ready underwrite

- You need to hand an SBA lender a clean DSCR-gated model for a goodwill-heavy wealth practice

- You want to know how much you would overpay on a revenue multiple

- You want an operating or startup forecast for launching a new advisory firm (this is an acquisition underwrite)

- You are modelling a large platform or roll-up at aggregator multiples (this prices a single sub-$500M book)

- You need investment, tax or legal advice (this is an educational planning tool)