Publication number: ELQ-78272-1

View all versions & Certificate

Single & Dual-Stream MRF Financial Model — Techno-Economic Analysis & ProjectFinance

A ready-to-use Excel model to assess the financial viability of a single-stream or dual-stream MRF — full P&L, cash flow, project & equity returns, debt sizing.

Waste-to-Energy & Circular Economy Financial Models | 20+ Years Hands-On ExperienceFollow

Further information

Objectives of your Downloadable Best Practice

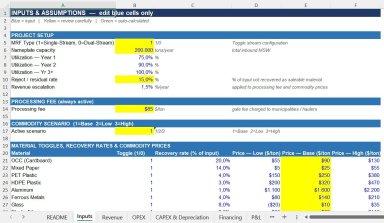

This model enables users to assess the financial viability of a single-stream or dual-stream Materials Recovery Facility (MRF) from first principles. Specifically, it allowsyou to:

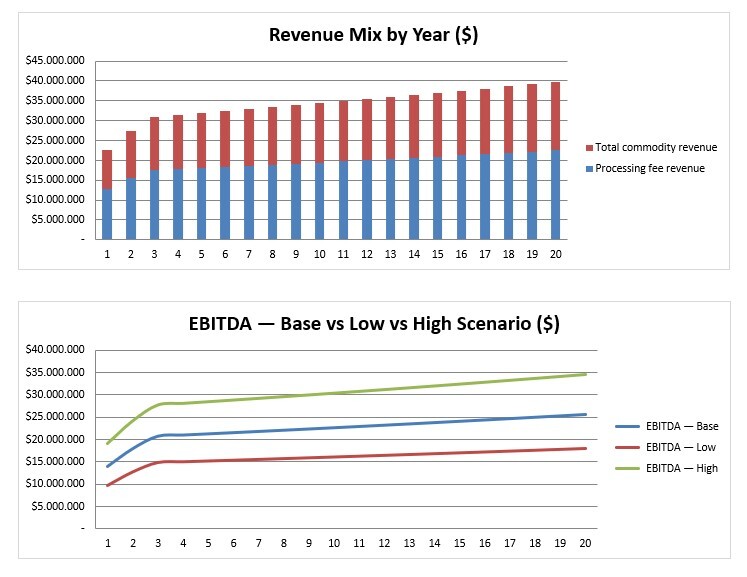

• Model revenue from processing fees and up to 8 individual material streams(OCC, Mixed Paper, PET, HDPE, Aluminium, Ferrous Metals, Glass, Plastic Film),each toggleable on/off;

• Switch between single-stream and dual-stream configurations with one cell;

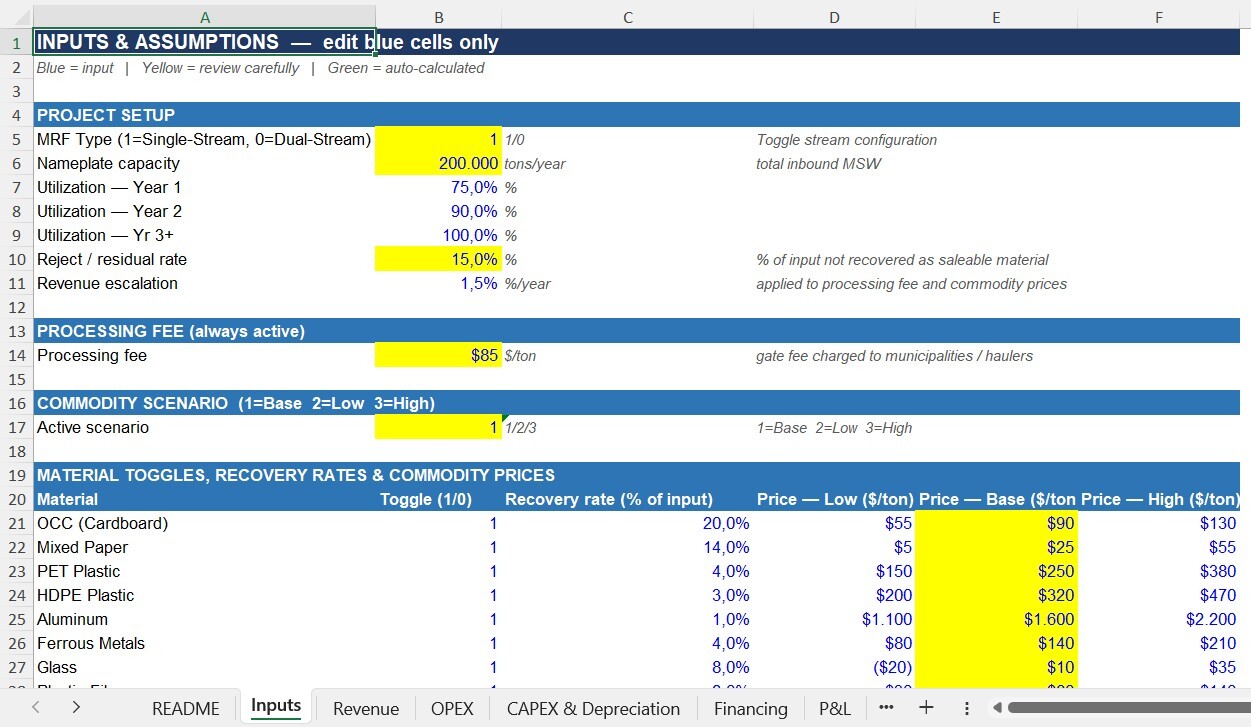

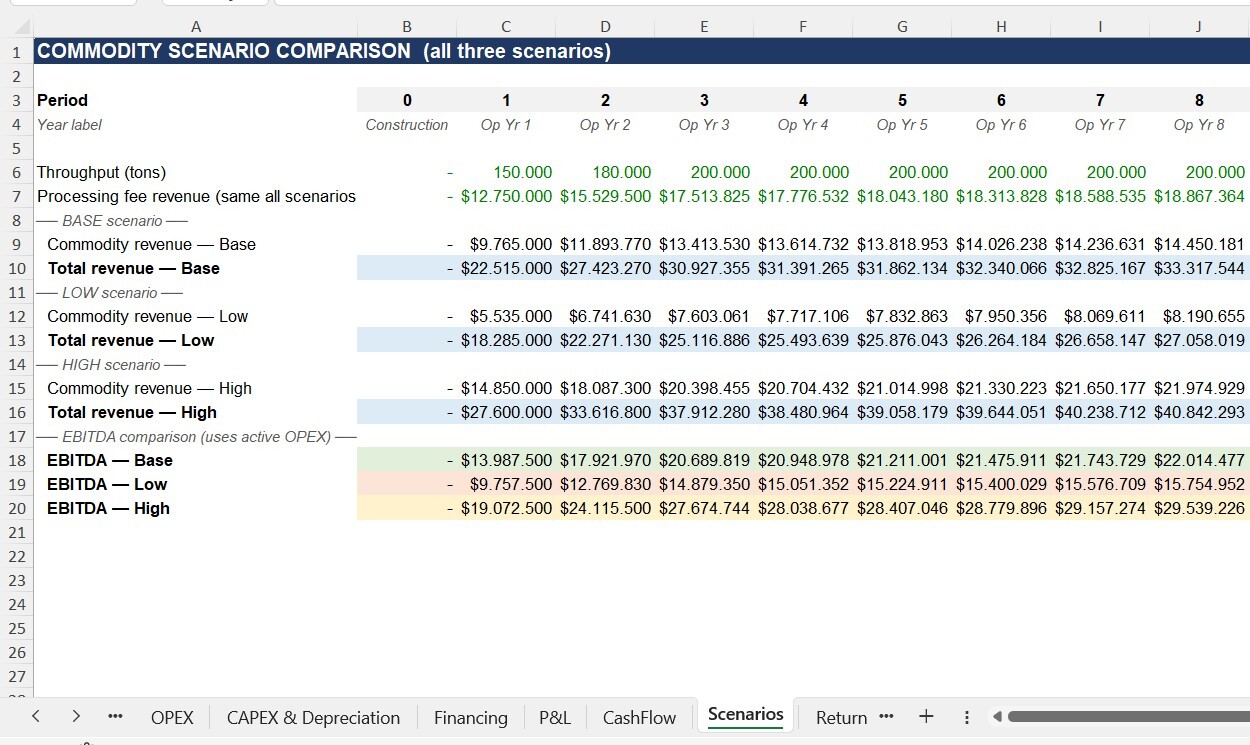

• Run and compare three commodity pricing scenarios (Base, Low, High)simultaneously to quantify the impact of market volatility on project viability;

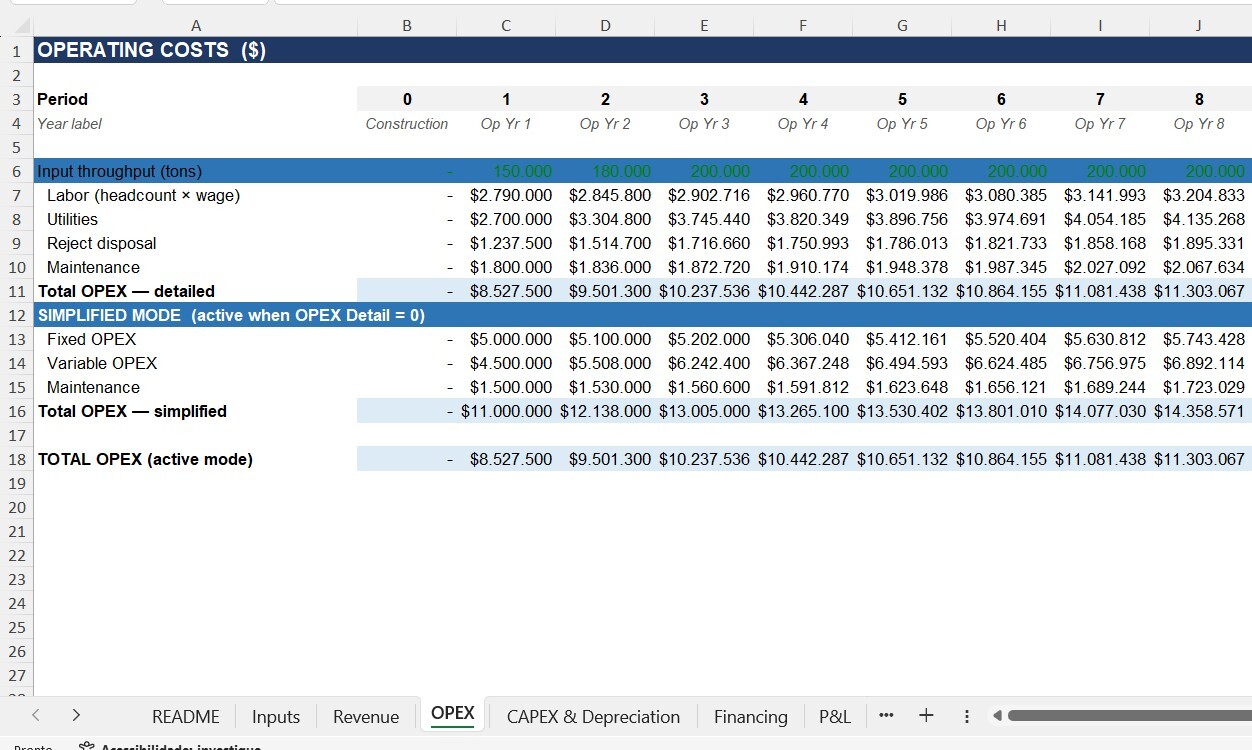

• Model operating costs in either detailed mode (labor + utilities + reject disposalmaintenance) or simplified mode (fixed $/yr + variable $/ton);

• Size capital expenditure, depreciation and a project finance debt structure;

• Generate a fully linked financial model (P&L, cash flow, debt schedule) from asingle input tab;

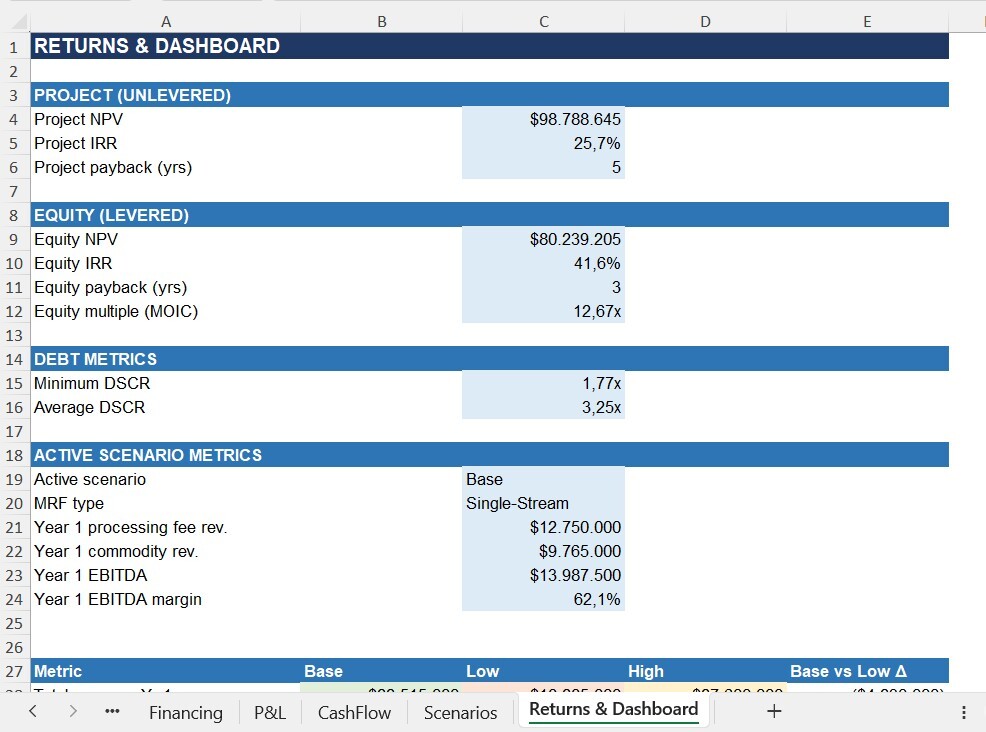

• Calculate project and equity returns: NPV, IRR, payback, DSCR and equitymultiple;

• Produce lender-ready output including annual DSCR and debt service coveragemetrics.

Conditions for which this Downloadable Best Practice applies best

This model is best suited for:

• Feasibility and pre-feasibility analysis of new or retrofit single-stream and dual-stream MRF projects processing municipal solid waste;

• Developers, EPCs, municipalities and consultants building an initial investmentcase or preparing a feasibility study for a recycling facility;

• Investors, private equity and lenders running first-pass due diligence on an MRFopportunity, particularly where commodity price risk is a key concern;

• Projects with a clearly defined material mix and processing fee structure;

• Users who need a transparent, auditable model that can be adapted and presentedto municipalities, co-investors or financing institutions.

Conditions for which this Downloadable Best Practice does not apply ideally

This model is not the best fit if:

• Your project requires mass-balance simulation of individual material streamsthrough multiple sorting stages (this requires process simulation software, not afinancial model);

• You need a probabilistic (Monte Carlo) risk model — this is a deterministic modelwith scenario analysis, not a full stochastic simulation;

• Your financing structure involves sculpted debt service, mezzanine tranches ortax equity — the financing module uses equal principal repayment;

• You require jurisdiction-specific tax treatment (e.g. bonus depreciation, taxcredits, loss carry-forward) beyond a flat corporate tax rate;

• Your project horizon exceeds 20 operating years without modifying the columnstructure;

• You need integration with commodity price feeds or live market data — all inputsare manual and must be calibrated by the user.