Originally published: 16/03/2019 18:43

Last version published: 18/03/2020 07:30

Publication number: ELQ-70862-2

View all versions & Certificate

Last version published: 18/03/2020 07:30

Publication number: ELQ-70862-2

View all versions & Certificate

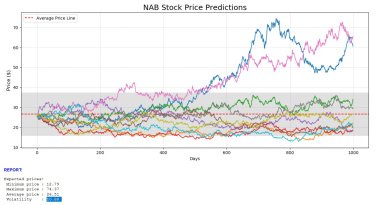

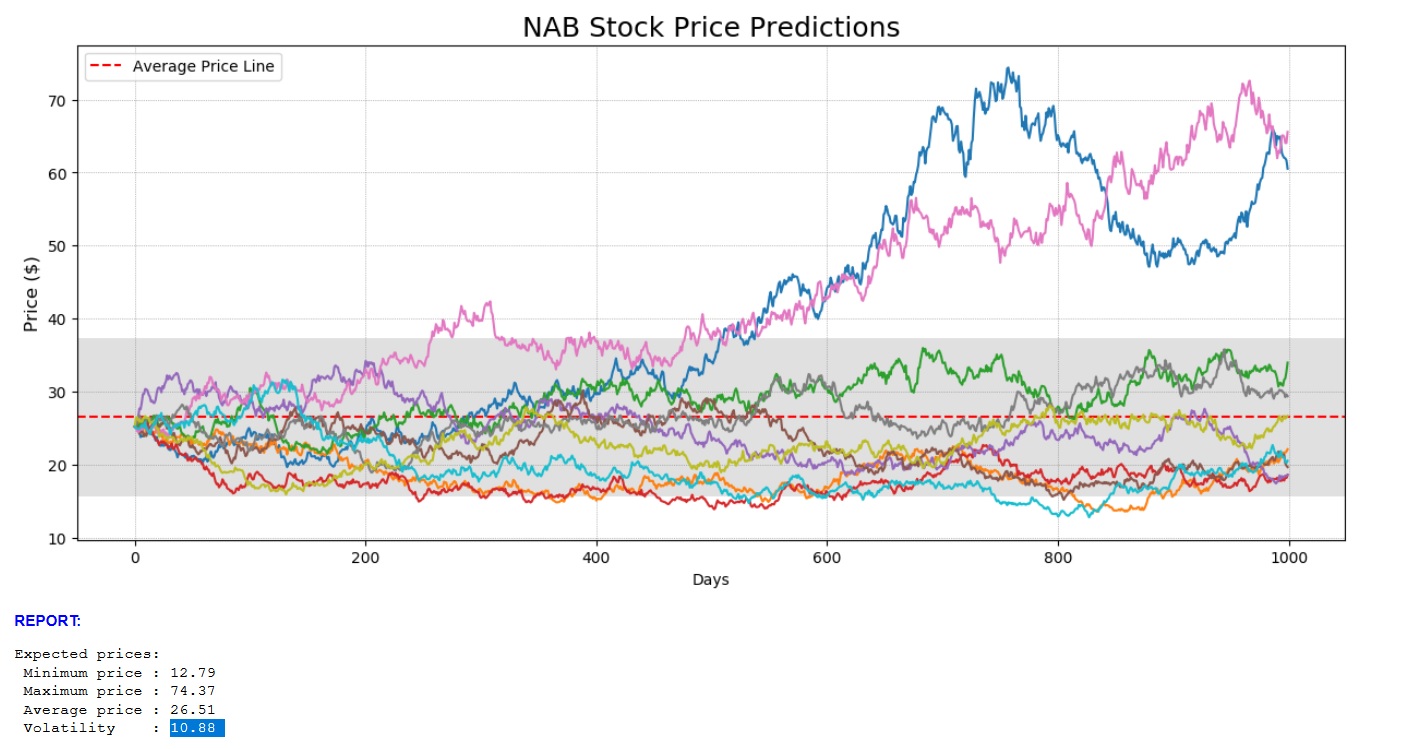

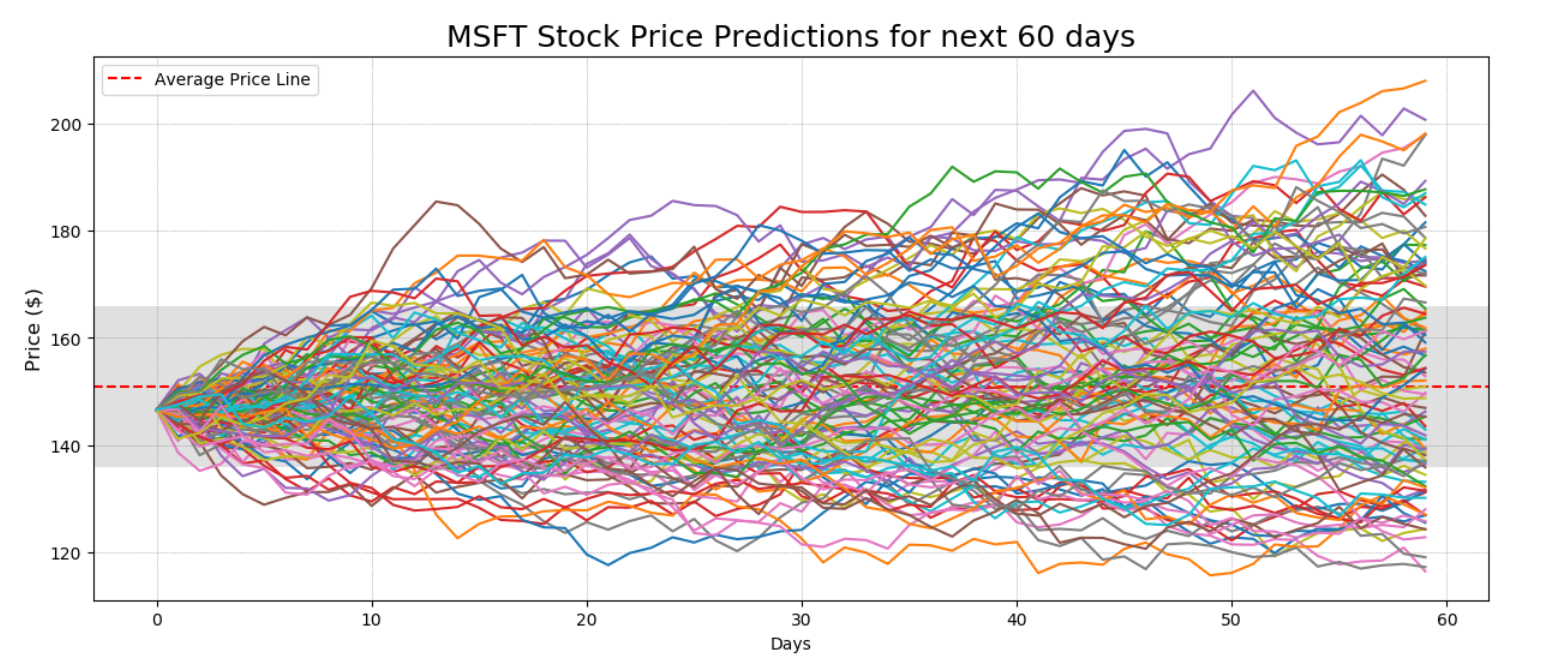

OneClick US S&P Stock Prediction Using Monte Carlo and Brownian Motion in Python

Monte Carlo and Brownian Motion Models Python script to predict future stock movements.

Further information

To provide one-click calculations of complex simulations

1. Availability of free Microsoft Azure account.

2. Availability of Libraries and Module used in the script.

3. Availability of Data from Yahoo Finance

4. Know how to run Jupyter Notebook

Local or cloud-based python version, libraries, modules are not appropriate

Yahoo finance data service API depreciated