Last version published: 03/07/2025 12:28

Publication number: ELQ-70218-2

View all versions & Certificate

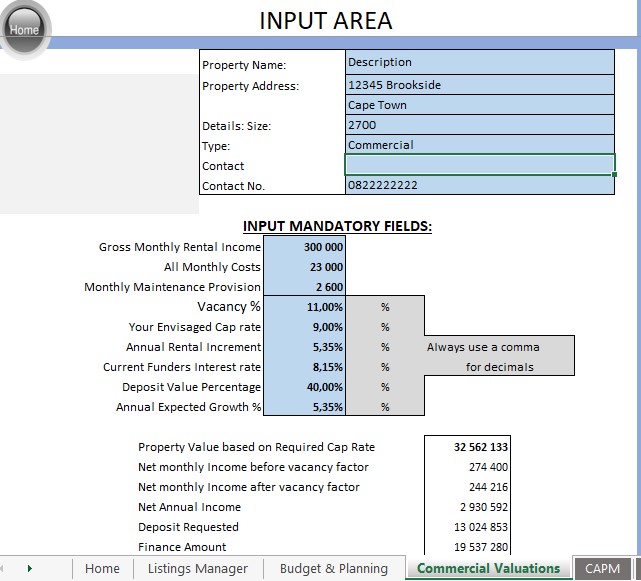

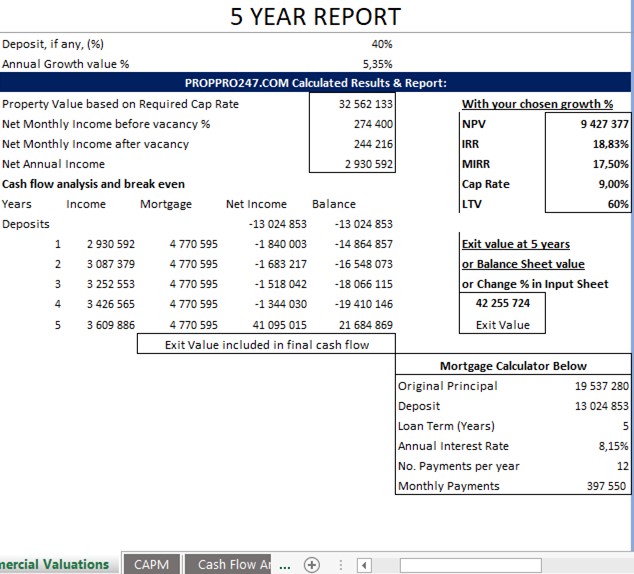

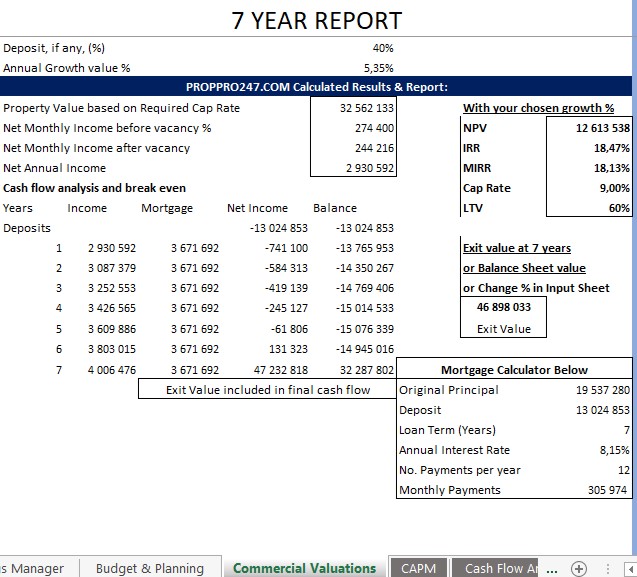

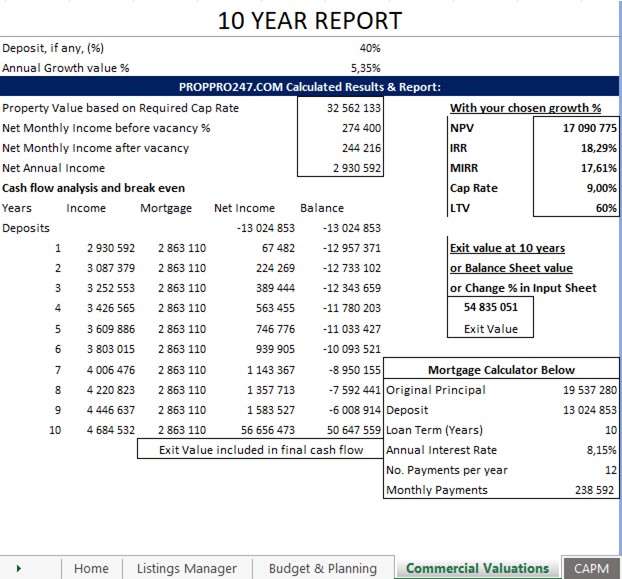

Commercial Property Valuations made easy with automated Cash Flow, Exit Values, NPV, IRR and MIRR

Commercial Real Estate Valuations the way Analysts and Investors need to see them with NPV, IRR, MIRR, Cash Flows and Exit Values

Masters in Accounting, Finance, Financial Modelling, Valuation Systems for Real Estate and BusinessFollow

Further information

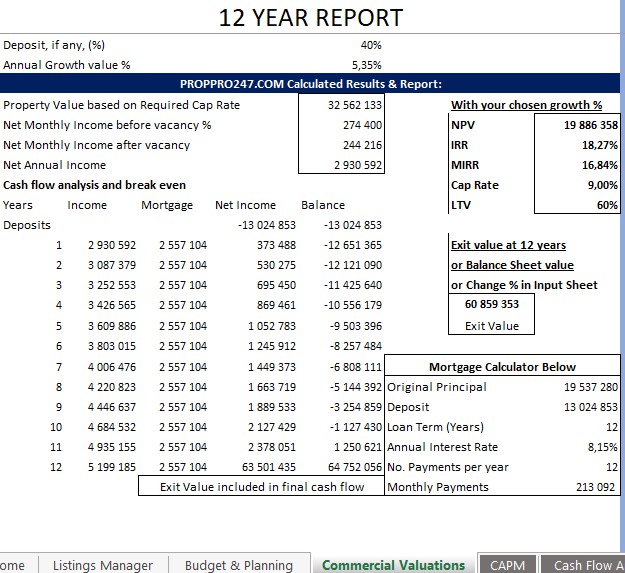

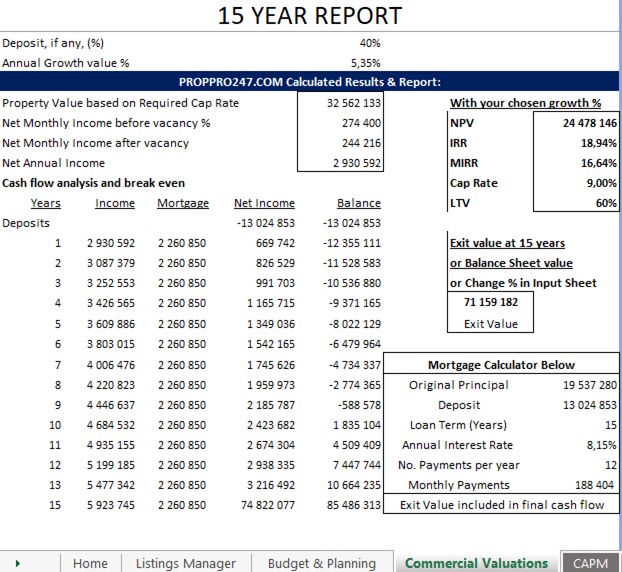

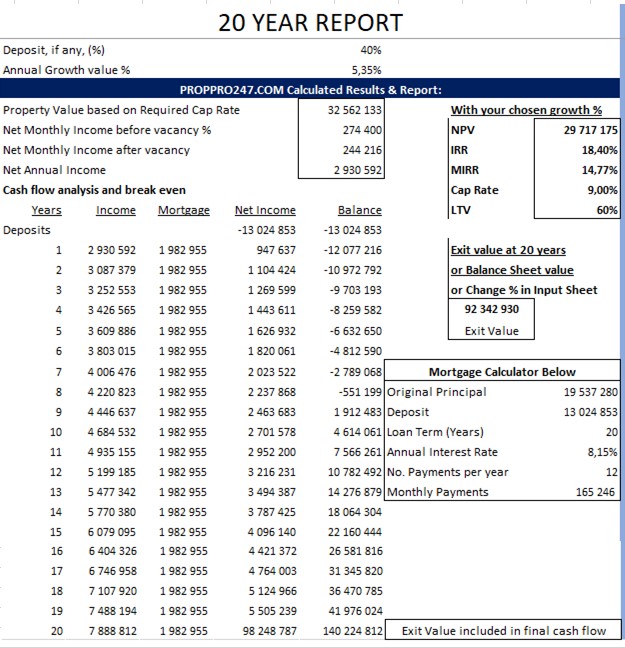

The main objective of this Valuation model is to be able to input basic data and see how the value measures against certain critical formulas such as NPV, IRR and MIRR. You are able to within a second change the cap rate and see how this effects the returns across 5 to 20 years. Change any data and perform CRE Valuations as the professionals will have.

Where you have buildings that are tenanted you will have the exact science. Untenanted buildings are valued exactly the same in that a predicted rental/lease amount is used to apply a value.

This is not a valuation mechanism for developments. We have specific development valuation models which must include XNPV and CIRR which re the date-sensitive version of NPV and IRR respectively