Originally published: 19/04/2020 08:25

Last version published: 21/04/2020 13:41

Publication number: ELQ-80541-3

View all versions & Certificate

Last version published: 21/04/2020 13:41

Publication number: ELQ-80541-3

View all versions & Certificate

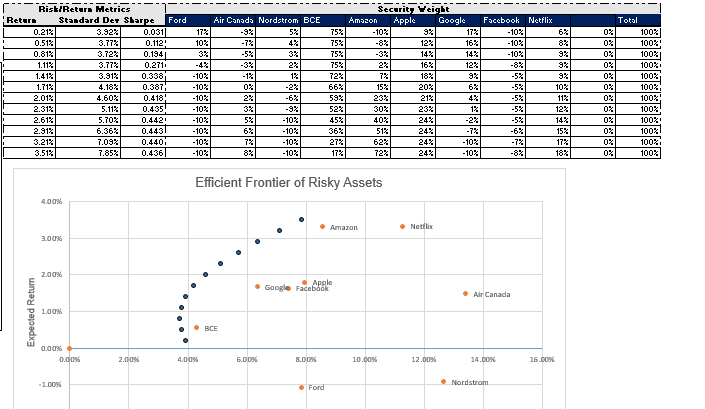

Optimal Portfolio - Markowitz Efficient Frontier (With Short Selling Option) Excel Model

Use this tool uses Efficient Market Hypothesis to determine the optimized portfolio allocation.

Further information

To gain a proper understanding of Efficient Market Hypothesis, and how it can be compared with your current asset allocation.

Need to download macros, and the excel solver (steps to download included)