Originally published: 01/07/2026 13:07

Publication number: ELQ-74723-1

View all versions & Certificate

Publication number: ELQ-74723-1

View all versions & Certificate

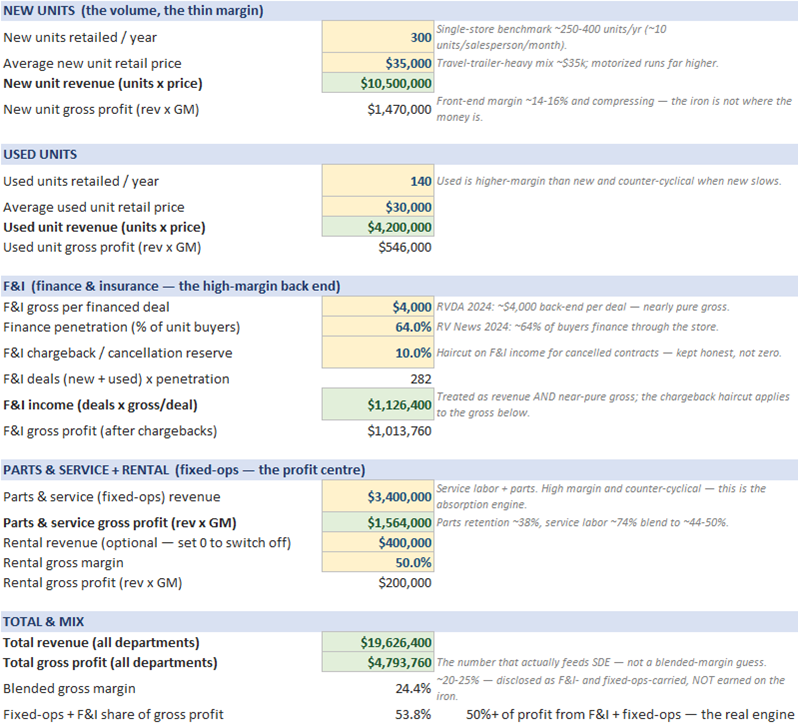

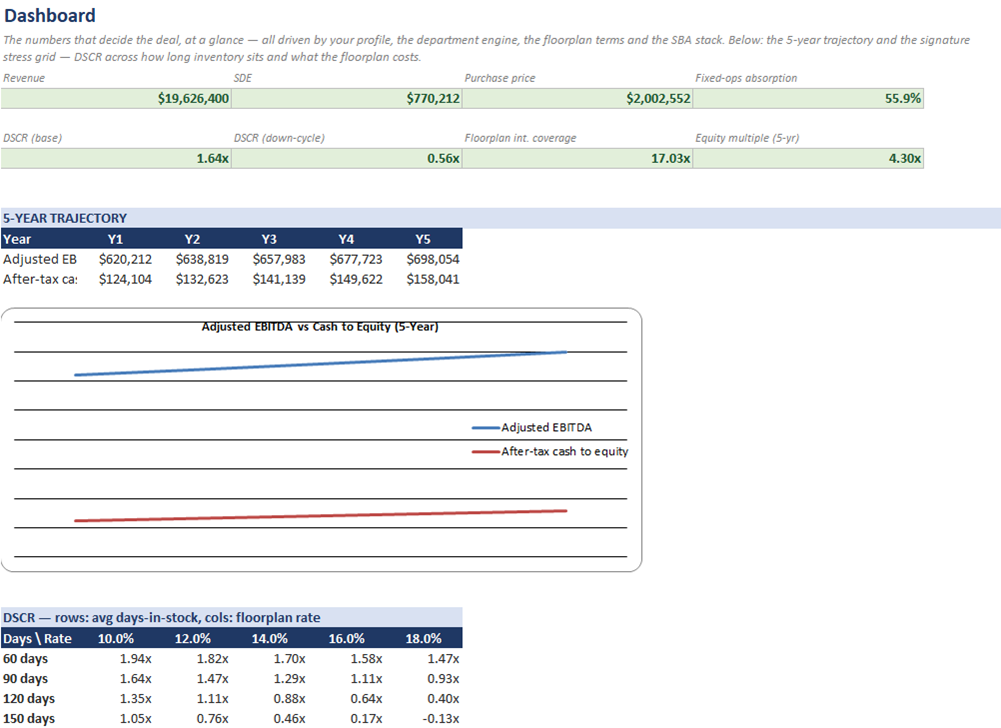

RV Dealership Acquisition & SBA Underwriting Financial Model (Floorplan + F&I + Absorption + DSCR)

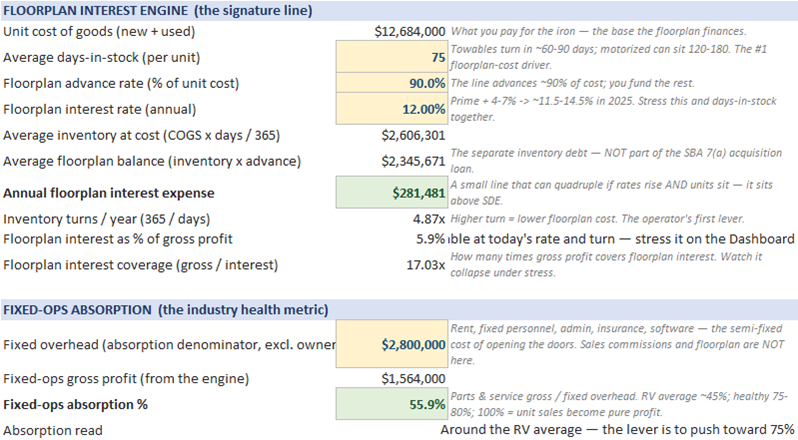

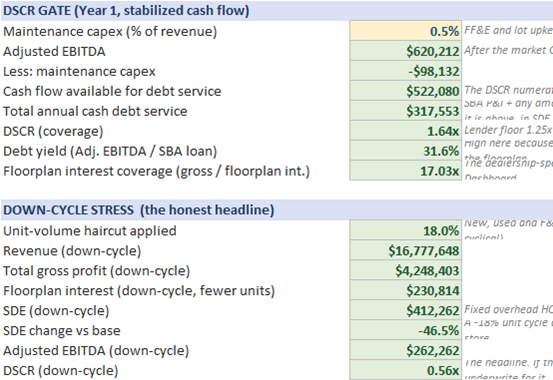

Underwrite a single-store RV dealership acquisition: gross by department, floorplan interest, fixed-ops absorption, SBA 7(a) DSCR and a down-cycle stress.

Further information

Underwrite an RV dealership acquisition the way an SBA lender and a disciplined buyer will - on absorption, floorplan carry and the down-cycle, not the seller's good-year P&L.

You are buying or valuing a single-store RV (or boat/powersports) dealership with an SBA 7(a) loan and need a lender-ready, stress-tested underwrite.

You need a multi-store roll-up consolidation model, a real-estate (RV park) model, or simple operating bookkeeping - this is a single-store acquisition underwrite.