-

+

44

more

Originally published: 20/01/2025 12:59

Publication number: ELQ-28234-1

View all versions & Certificate

Publication number: ELQ-28234-1

View all versions & Certificate

The Comprehensive Guide to the Evolution of Technology in Accounting

The Comprehensive Guide to the Evolution of Technology in Accounting

Founder of Ze-accountant - Cost & Budgeting Section Head - Instructor- business consultant for tech startups and SMEsFollow 22

Description

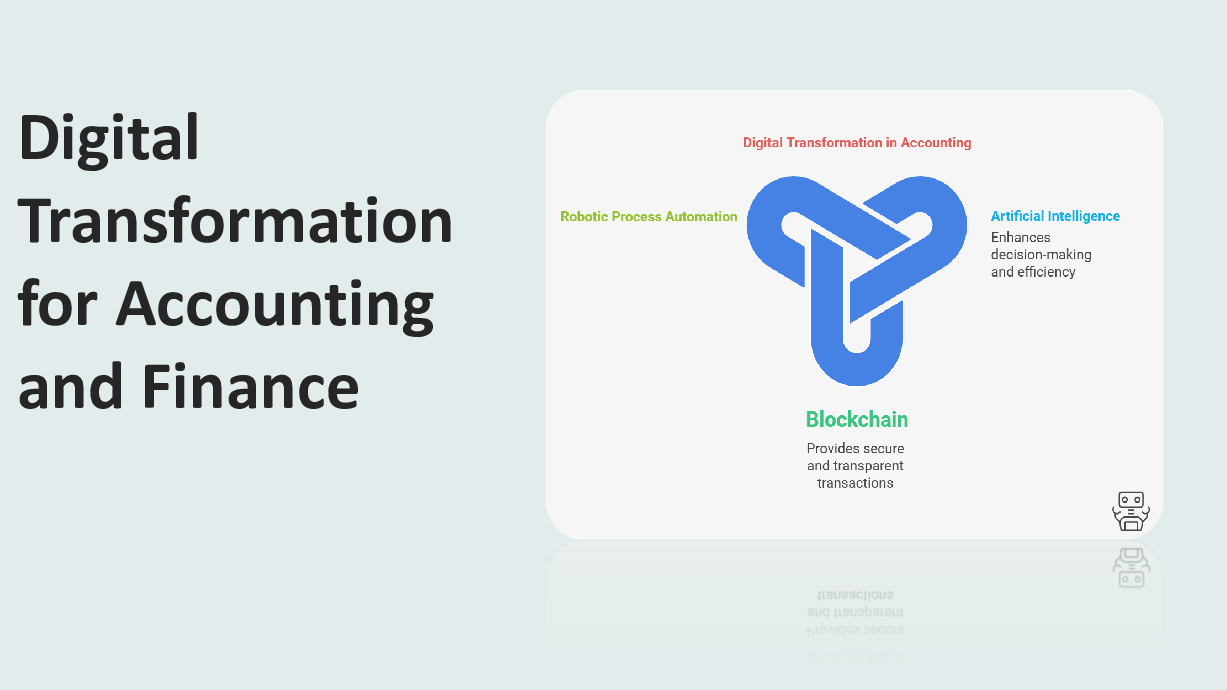

Artificial Intelligence in AccountingArtificial Intelligence (AI) is revolutionizing accounting by automating repetitive tasks and enhancing data analysis. AI can handle large volumes of data quickly, providing real-time insights into financial performance. For instance, machine learning algorithms can identify anomalies in transactions, flagging potential fraud or errors. AI-powered tools also assist with tax preparation, ensuring compliance by analyzing ever-changing regulations. Predictive analytics, driven by AI, enables accountants to forecast cash flow, optimize budgets, and make data-driven decisions. This transformation allows accountants to focus on strategic tasks rather than manual data entry, ultimately increasing efficiency and accuracy.

Artificial Intelligence in Microsoft ExcelMicrosoft Excel, enhanced with AI, has become a more powerful tool for financial professionals. Features like "Ideas" use AI to analyze datasets and suggest patterns or trends. Power Query enables advanced data cleansing and transformation, while integration with Power BI allows users to create dynamic dashboards and visualizations. AI in Excel can also automate predictive analysis, making forecasts based on historical data. Additionally, Excel’s AI capabilities simplify tasks like categorizing data, identifying outliers, and generating insights with minimal user input. This integration helps users save time and improve the accuracy of their financial models.

Risks of Artificial IntelligenceWhile AI offers significant benefits, it also poses risks. One major concern is data security; AI systems often handle sensitive financial information, making them a target for cyberattacks. Another risk is the reliance on inaccurate or biased data, which can lead to flawed decision-making. Overdependence on AI could result in diminished human oversight, causing critical errors to go unnoticed. Additionally, ethical concerns arise when AI systems make decisions without transparency, leading to regulatory challenges. Addressing these risks requires robust data governance, regular audits, and clear guidelines for AI deployment.

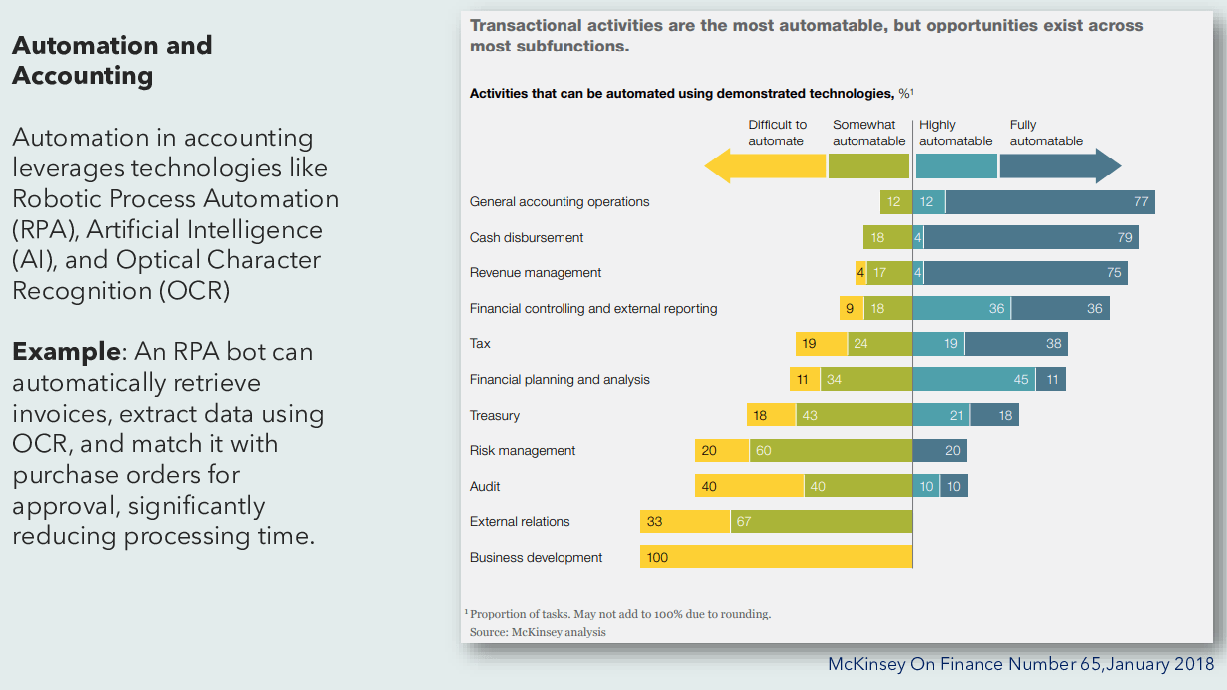

RPA Technology and Its Impact on AccountingRobotic Process Automation (RPA) is transforming accounting by automating rule-based tasks such as invoice processing, data entry, and reconciliation. RPA tools work 24/7, significantly reducing processing time and errors. For example, RPA can automatically match purchase orders with invoices, saving time and ensuring accuracy. This frees accountants to focus on high-value activities like strategic planning. Moreover, RPA helps in scaling operations without adding human resources. While RPA increases efficiency, its integration requires careful planning and monitoring to ensure seamless workflows and compliance with regulations.

Blockchain TechnologyBlockchain technology offers a decentralized, transparent, and secure method for recording transactions, making it a game-changer in accounting. Its immutable ledger ensures the integrity of financial data, reducing the risk of fraud. Blockchain simplifies audits by providing a clear and verifiable trail of all transactions. Smart contracts, powered by blockchain, automate agreements, ensuring that terms are executed without manual intervention. For instance, payments can be automatically released when conditions are met. The adoption of blockchain enhances trust and collaboration between parties, while also reducing costs associated with reconciliation and verification.

Artificial Intelligence in AccountingArtificial Intelligence (AI) is revolutionizing accounting by automating repetitive tasks and enhancing data analysis. AI can handle large volumes of data quickly, providing real-time insights into financial performance. For instance, machine learning algorithms can identify anomalies in transactions, flagging potential fraud or errors. AI-powered tools also assist with tax preparation, ensuring compliance by analyzing ever-changing regulations. Predictive analytics, driven by AI, enables accountants to forecast cash flow, optimize budgets, and make data-driven decisions. This transformation allows accountants to focus on strategic tasks rather than manual data entry, ultimately increasing efficiency and accuracy.

Artificial Intelligence in Microsoft ExcelMicrosoft Excel, enhanced with AI, has become a more powerful tool for financial professionals. Features like "Ideas" use AI to analyze datasets and suggest patterns or trends. Power Query enables advanced data cleansing and transformation, while integration with Power BI allows users to create dynamic dashboards and visualizations. AI in Excel can also automate predictive analysis, making forecasts based on historical data. Additionally, Excel’s AI capabilities simplify tasks like categorizing data, identifying outliers, and generating insights with minimal user input. This integration helps users save time and improve the accuracy of their financial models.

Risks of Artificial IntelligenceWhile AI offers significant benefits, it also poses risks. One major concern is data security; AI systems often handle sensitive financial information, making them a target for cyberattacks. Another risk is the reliance on inaccurate or biased data, which can lead to flawed decision-making. Overdependence on AI could result in diminished human oversight, causing critical errors to go unnoticed. Additionally, ethical concerns arise when AI systems make decisions without transparency, leading to regulatory challenges. Addressing these risks requires robust data governance, regular audits, and clear guidelines for AI deployment.

RPA Technology and Its Impact on AccountingRobotic Process Automation (RPA) is transforming accounting by automating rule-based tasks such as invoice processing, data entry, and reconciliation. RPA tools work 24/7, significantly reducing processing time and errors. For example, RPA can automatically match purchase orders with invoices, saving time and ensuring accuracy. This frees accountants to focus on high-value activities like strategic planning. Moreover, RPA helps in scaling operations without adding human resources. While RPA increases efficiency, its integration requires careful planning and monitoring to ensure seamless workflows and compliance with regulations.

Blockchain TechnologyBlockchain technology offers a decentralized, transparent, and secure method for recording transactions, making it a game-changer in accounting. Its immutable ledger ensures the integrity of financial data, reducing the risk of fraud. Blockchain simplifies audits by providing a clear and verifiable trail of all transactions. Smart contracts, powered by blockchain, automate agreements, ensuring that terms are executed without manual intervention. For instance, payments can be automatically released when conditions are met. The adoption of blockchain enhances trust and collaboration between parties, while also reducing costs associated with reconciliation and verification.

This Best Practice includes

1 PDF