Publication number: ELQ-64468-1

View all versions & Certificate

Wind Retrofit & Repowering Model — Evaluate Revamping, Repowering for Existing Onshore Wind Farms

Production-ready Excel model for financial evaluation of existing onshore wind farms. 8 countries, 5 analysis modes

Further information

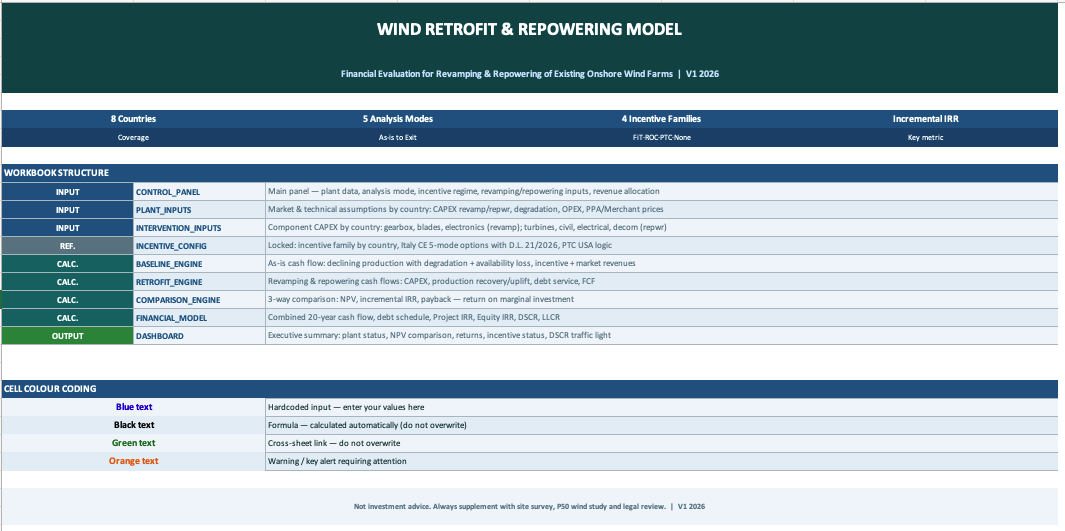

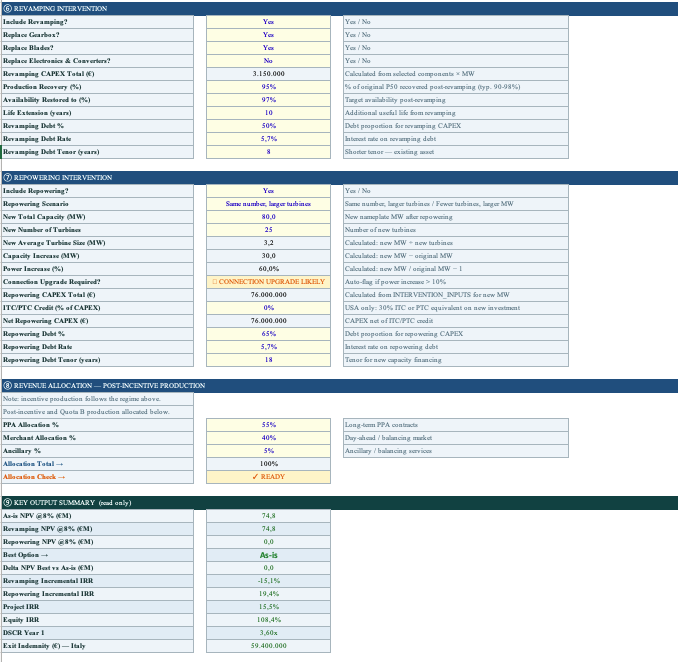

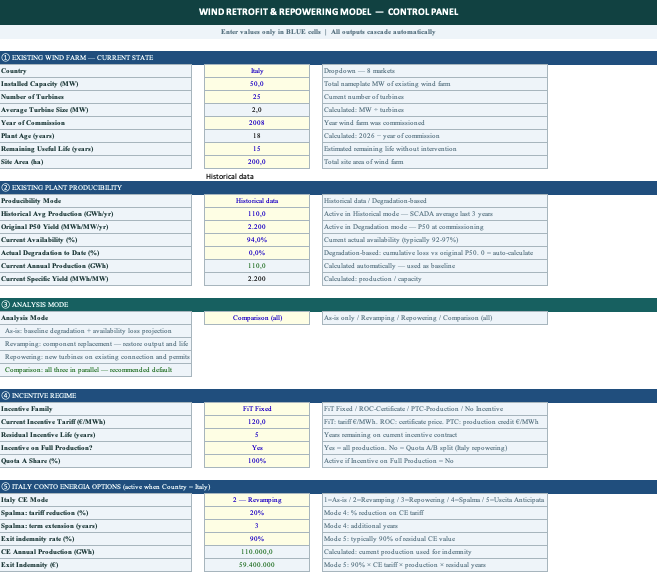

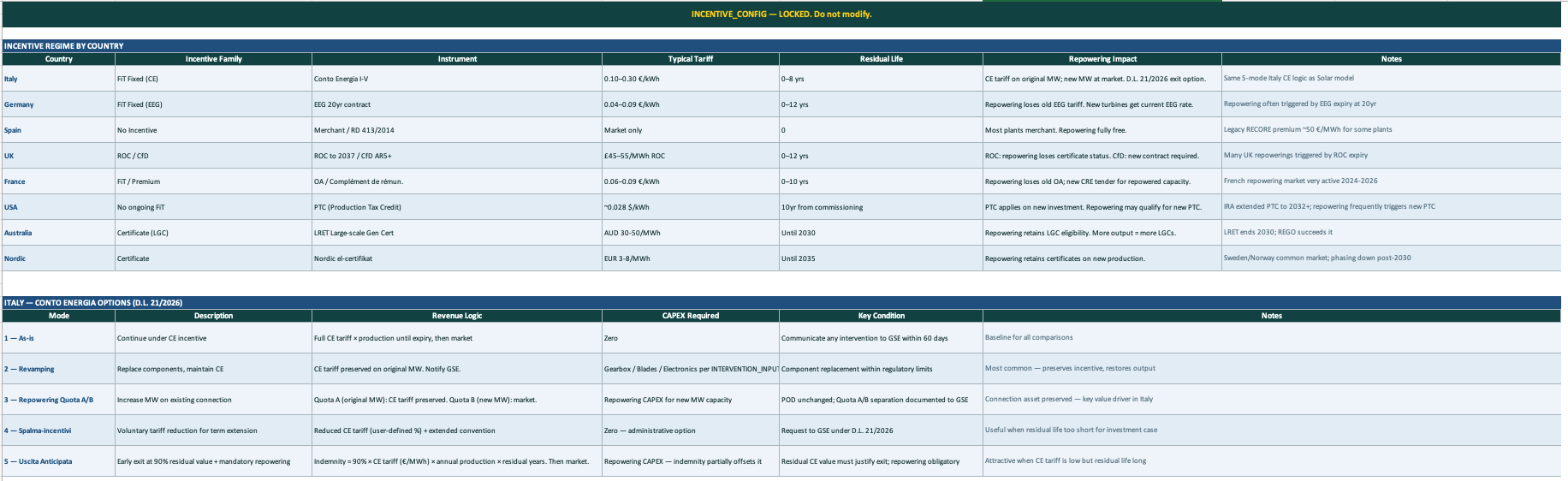

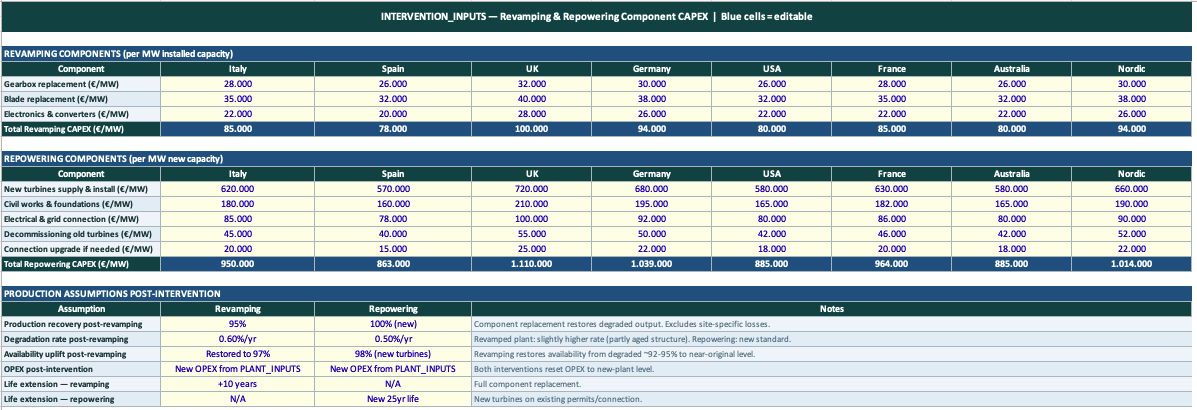

This model enables developers, advisors and asset managers to evaluate the financial case for revamping, repowering or maintaining an existing onshore wind farm across 8 international markets, producing a three-way NPV comparison — As-is versus Revamping versus Repowering — alongside incremental IRR, payback and a full 20-year DCF for the selected intervention. It models the existing plant baseline using degradation curves, availability loss trends and historical SCADA production data, applies country-specific incentive regimes across four families including Italy Conto Energia with all five D.L. 21/2026 options and USA Production Tax Credit mechanics, structures separate financing for revamping and repowering with appropriate tenor assumptions, and allocates post-incentive production across PPA, Merchant and Ancillary revenue streams with country-calibrated benchmark prices.

This model is best suited to operating onshore wind farms of 10 MW and above that are in the revamping or repowering evaluation window — typically plants aged 15-22 years with degraded availability, approaching or past EEG, ROC or CE incentive expiry, or where the existing grid connection and permit base creates repowering upside that would take years and significant cost to replicate on a greenfield site. It works particularly well for German wind farms approaching EEG expiry at 20 years, UK sites with residual ROC status, Italian CE plants under D.L. 21/2026, and USA projects where repowering may trigger a new PTC entitlement under the IRA extension. The comparison mode — running As-is, Revamping and Repowering in parallel — is the recommended default for any strategic review of an existing asset.

This model evaluates the financial case for revamping and repowering decisions and does not replace a site-specific technical assessment — production recovery assumptions post-revamping depend on the actual condition of individual turbines and should be validated with an independent technical advisor before any investment commitment. It covers onshore wind only and is not suited to offshore wind, which has a materially different cost structure, O&M model and regulatory framework. The Italy CE options module is calibrated for D.L. 21/2026 as of April 2026 — any subsequent regulatory changes should be reflected in the INCENTIVE_CONFIG parameters before use. It should not be used as the sole basis for a final investment or transaction decision without a site-specific P50 wind resource assessment, structural inspection of existing foundations and towers, and legal review of the applicable permit and incentive regime.