Publication number: ELQ-74584-1

View all versions & Certificate

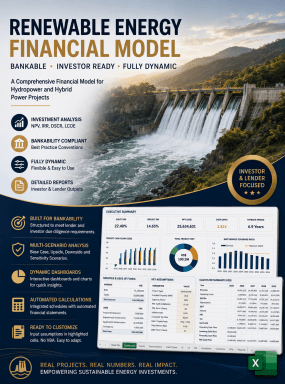

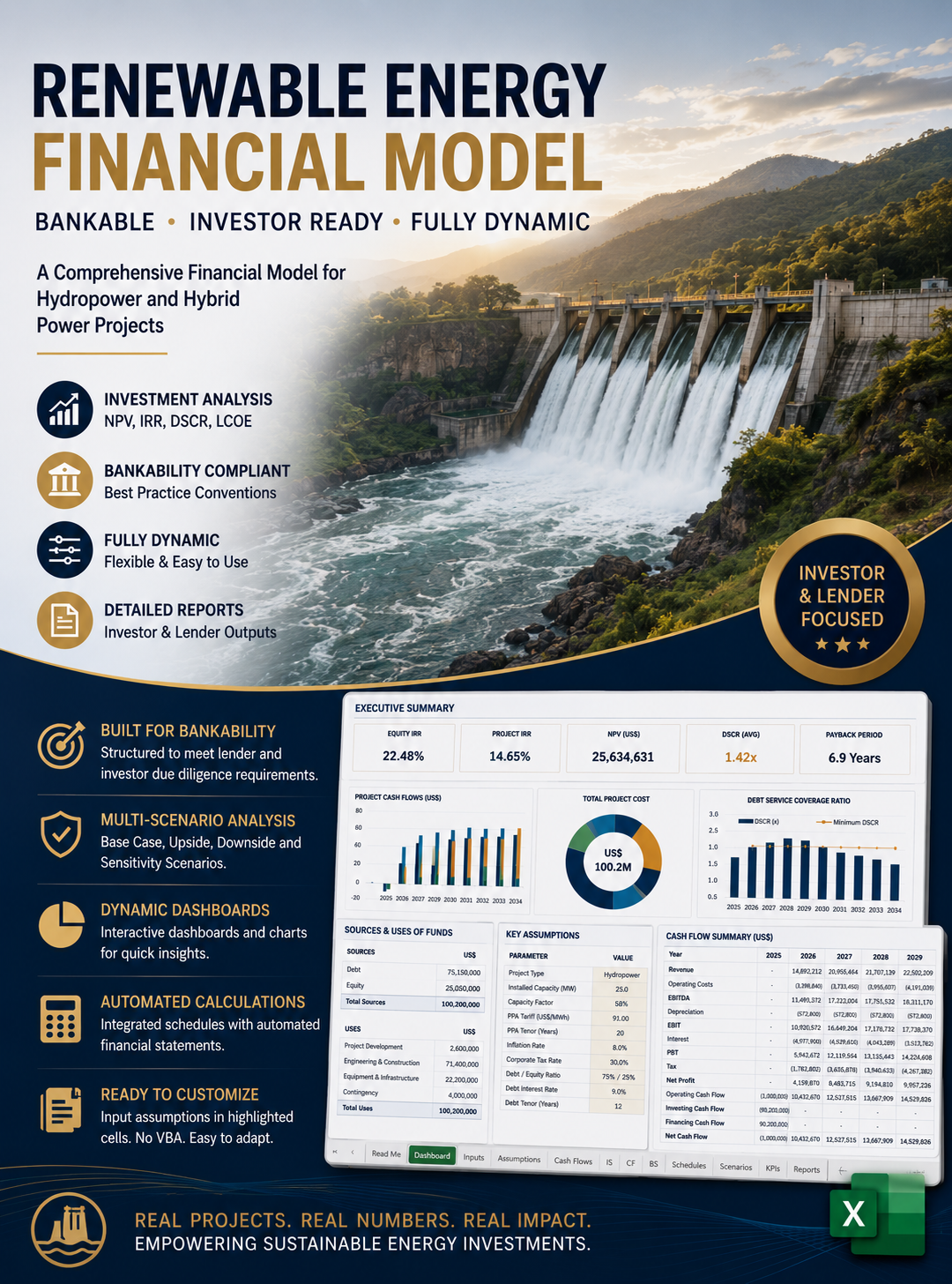

Small Hydropower Bankable Financial Model

Bankable Excel model for run-of-river hydropower: hydrology to returns.

Further information

Objectives of the Small Hydropower Bankable Financial Model

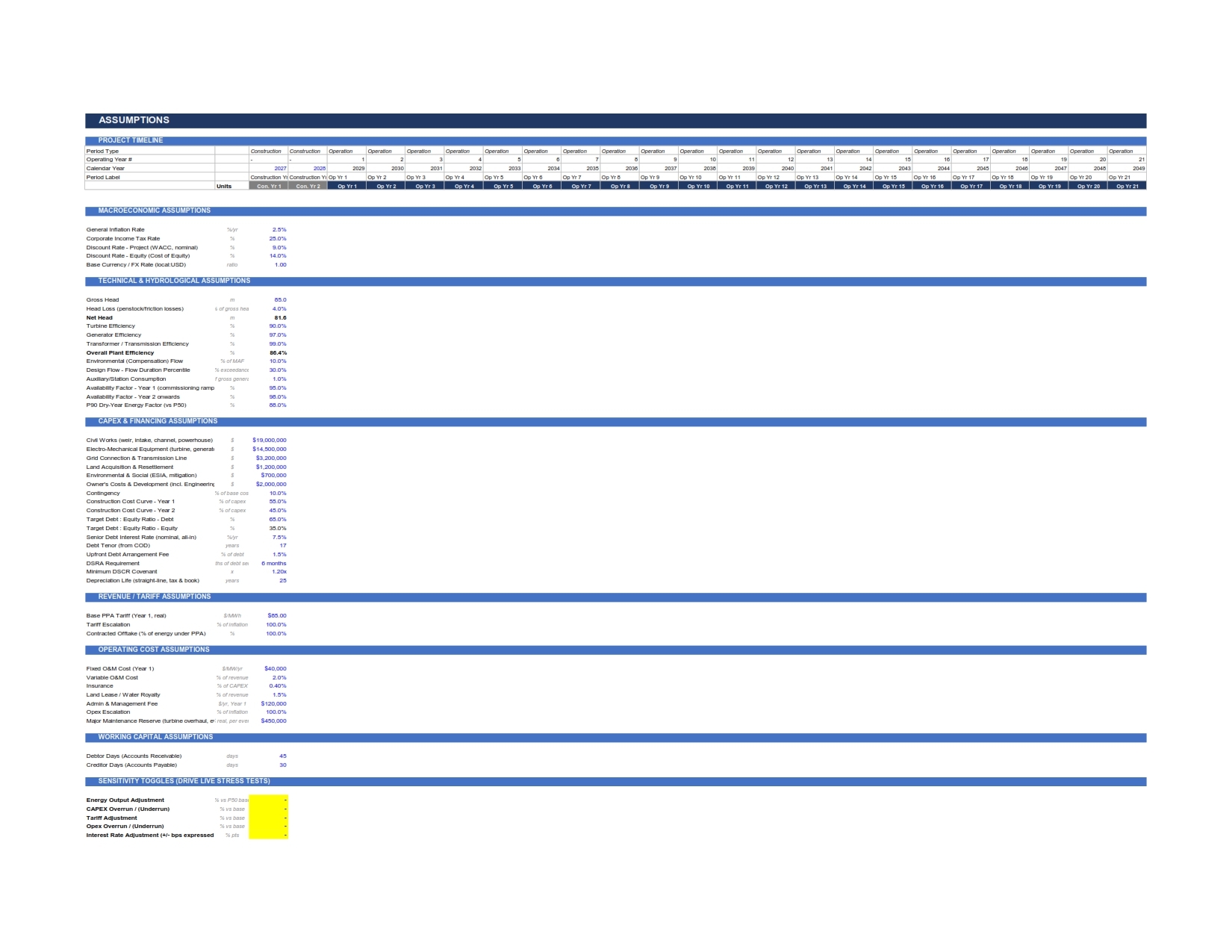

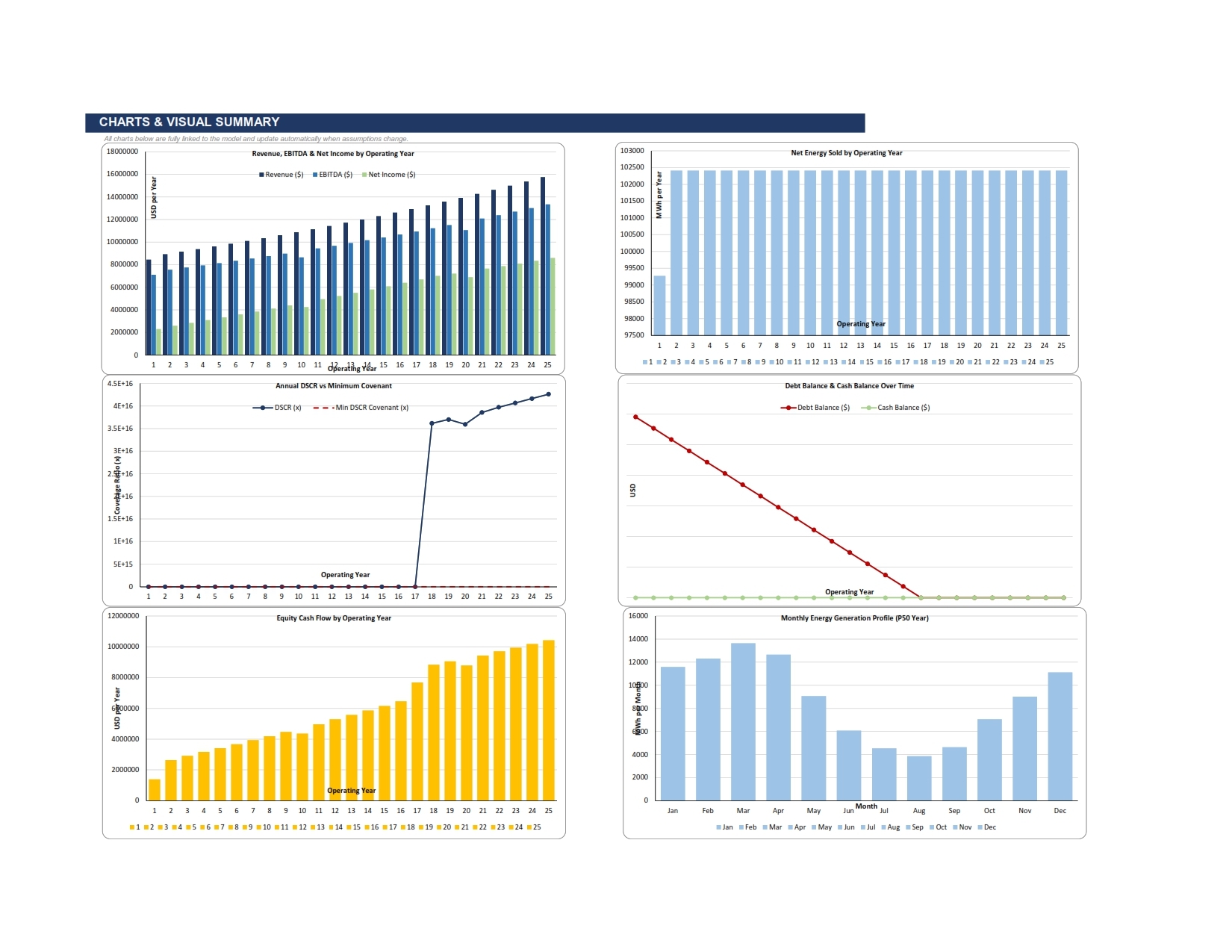

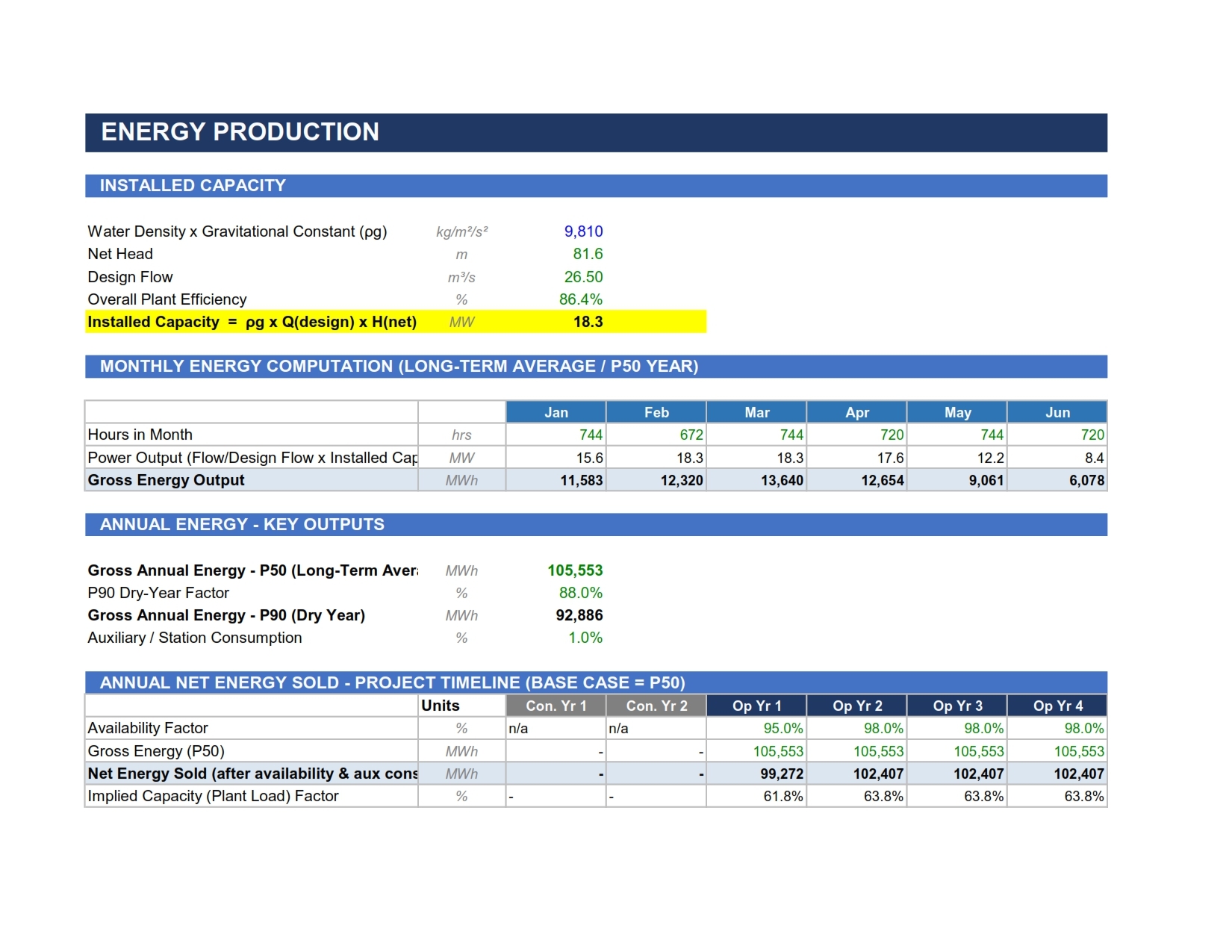

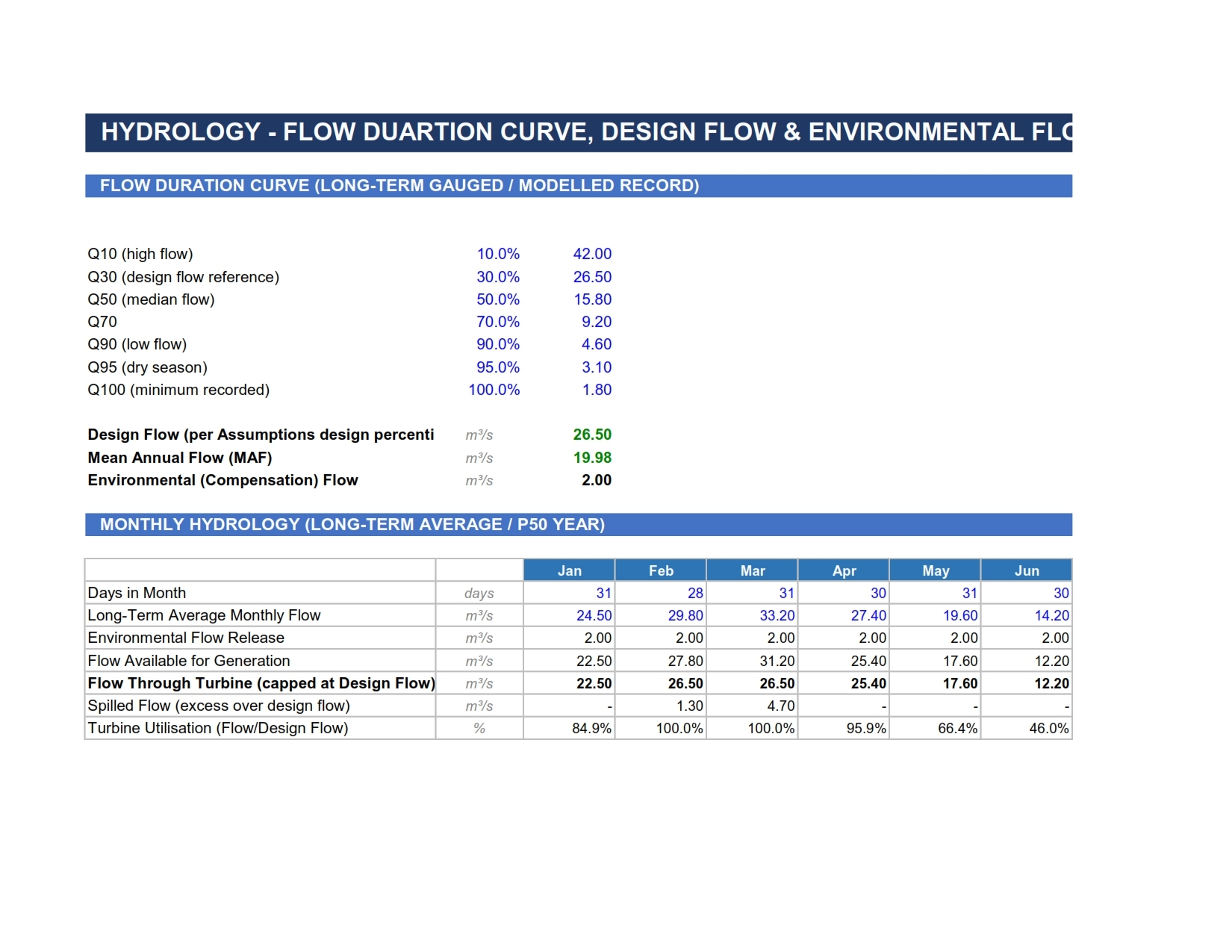

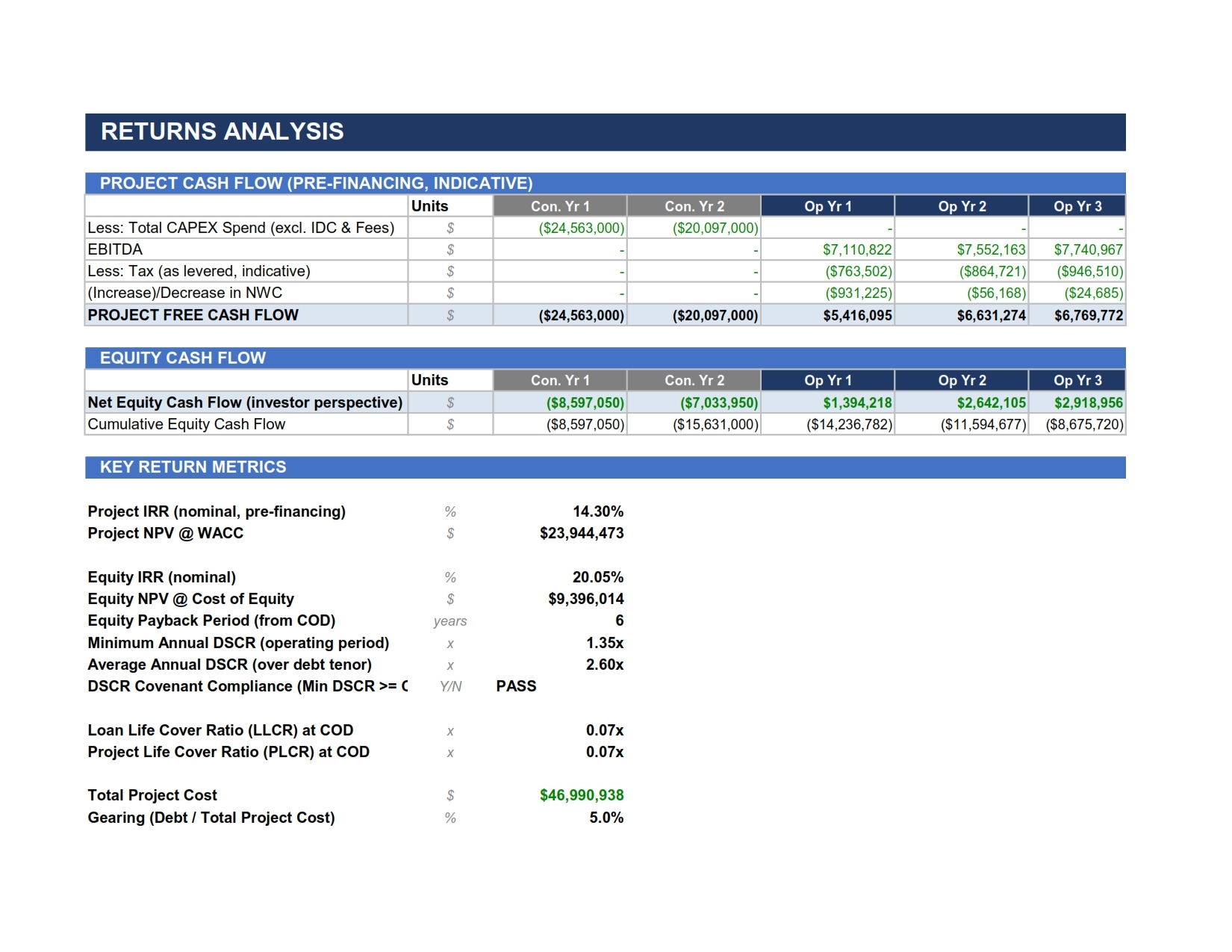

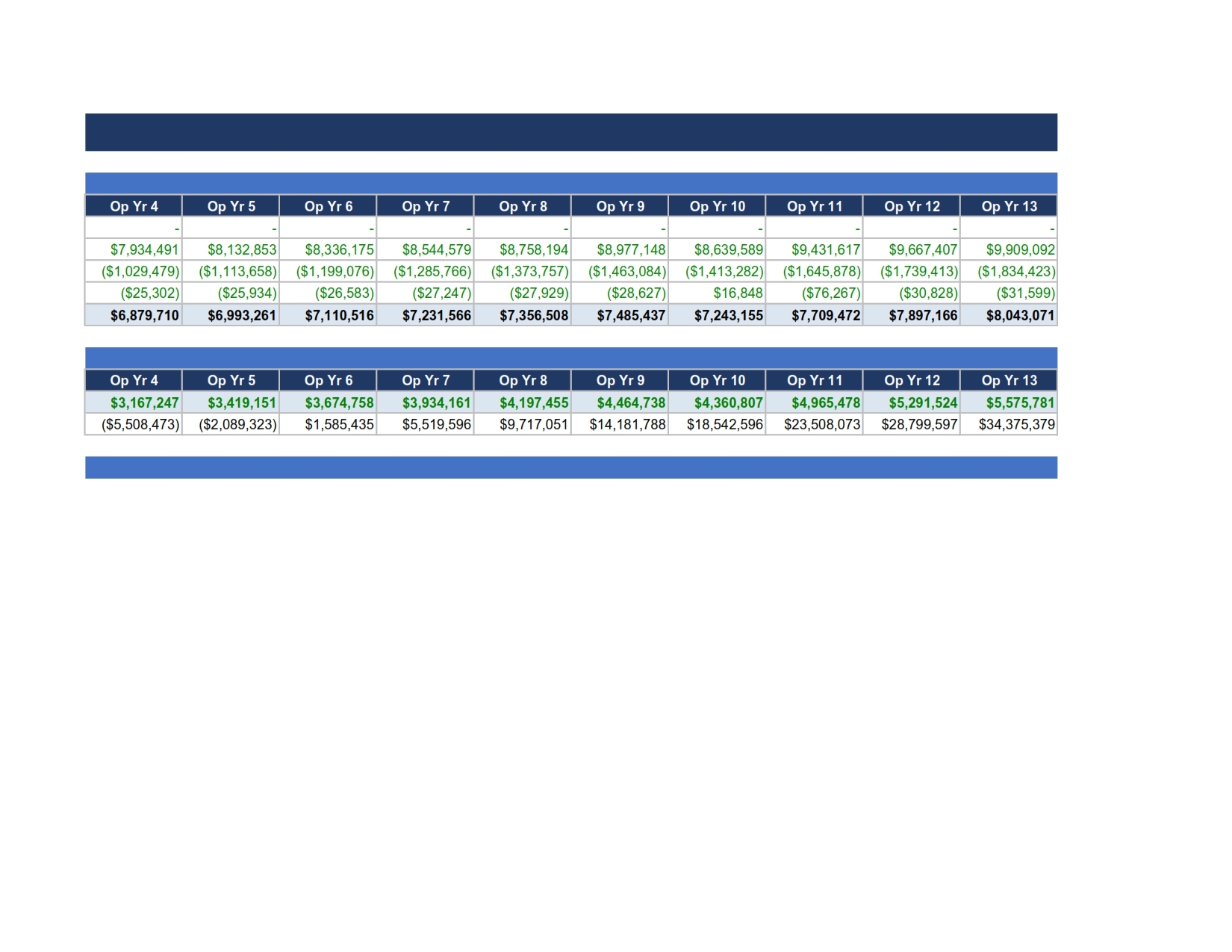

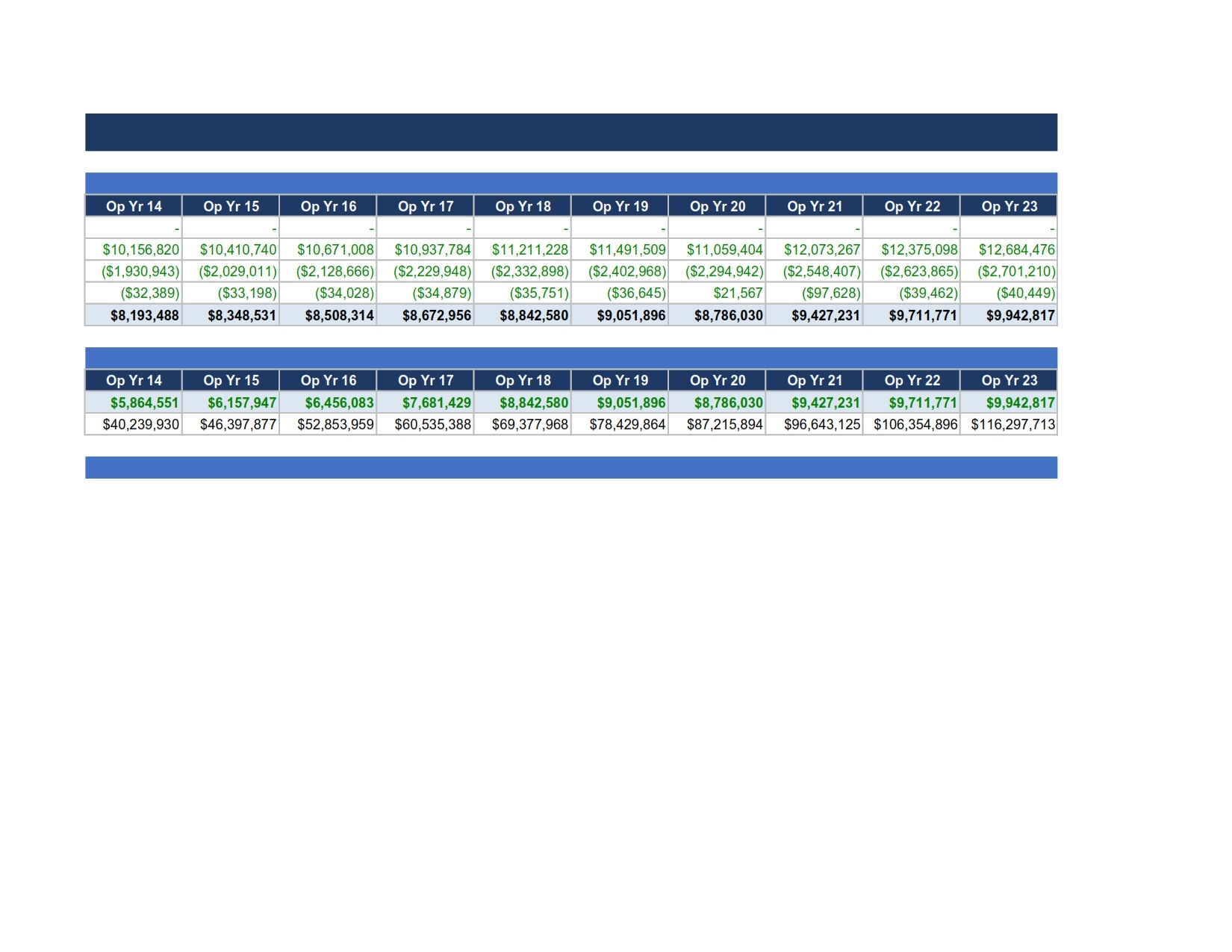

1. Translate technical hydrology into bankable outputs — convert flow duration curves, environmental flow policy, and design flow selection into installed capacity and annual energy (P50/P90) that lenders and engineers can independently verify.

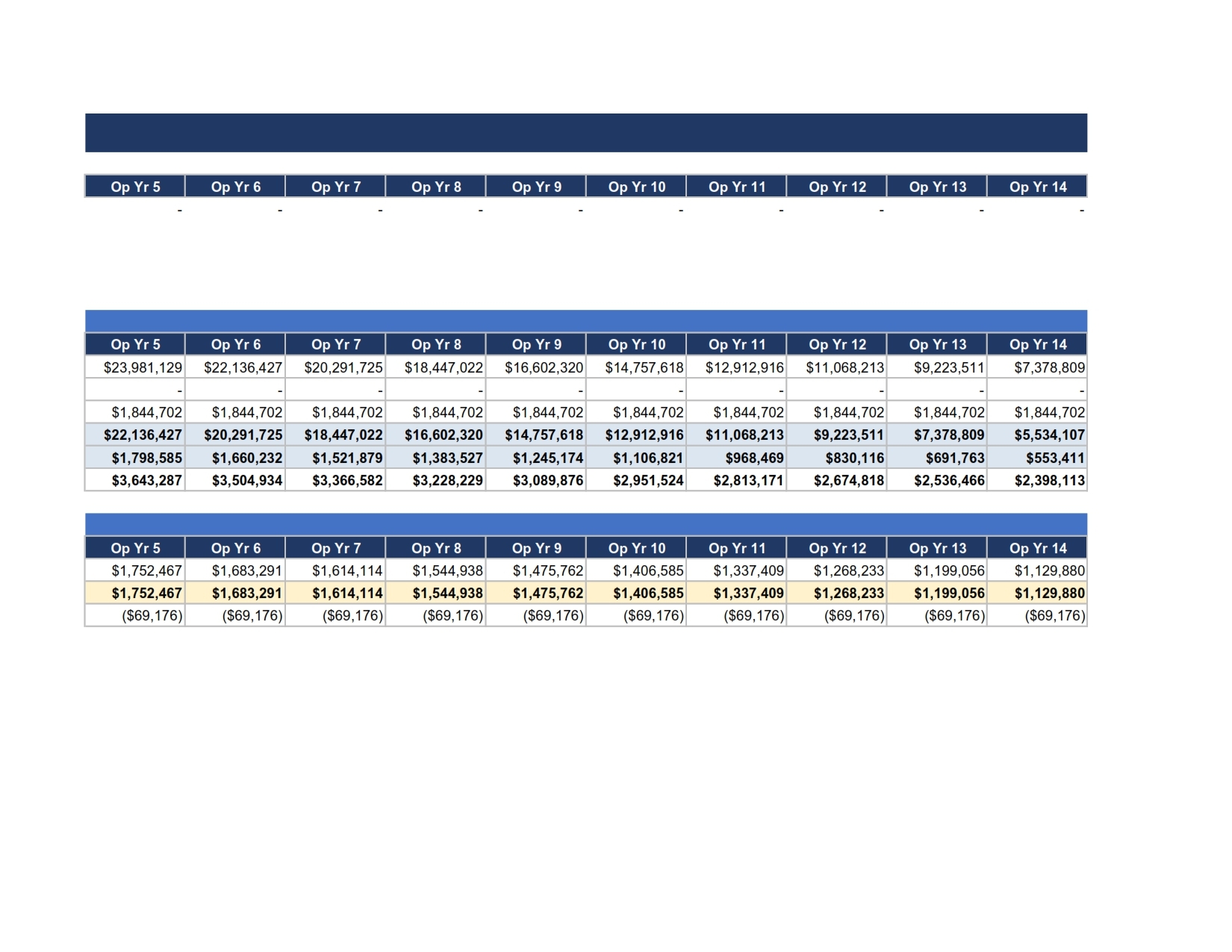

2. Size and structure the financing — determine total project cost, optimal debt/equity gearing, tenor, and DSRA requirements that keep debt service coverage within lender covenants.

3. Test bankability against lender criteria — produce the standard credit metrics (DSCR, LLCR, PLCR) that determine whether a lender's credit committee will approve the deal.

4. Quantify investor returns — calculate Project IRR and Equity IRR (and NPVs) to assess whether the project meets sponsor and equity investor return thresholds.

5. Stress-test key risks — show how hydrological shortfall, capex overrun, tariff downside, opex overrun, and interest rate movement affect returns and coverage, individually and combined.

6. Ensure full auditability — link every output back to its source assumption with transparent formulas (no black boxes), color-coded inputs vs. calculations, and automated integrity checks that catch errors immediately.

7. Support the full lifecycle of a transaction — serve equally as a feasibility/IM tool for sponsors, a due-diligence tool for lenders and independent engineers, and a live negotiating tool for structuring debt terms and tariff.

8. Provide a reusable, adaptable template — allow assumptions (hydrology, costs, tariff, financing terms) to be swapped out for a new site without rebuilding the model's architecture.

Conditions Under Which This Financial Model Applies Best

1. Run-of-river hydropower projects — the hydrology, design flow, and environmental flow logic are built specifically for run-of-river schemes with no significant reservoir/storage; it is not structured for large storage/dam projects with multi-year regulation or pumped-storage economics.

2. Small-to-mid scale capacity — best suited to projects roughly in the 1–30 MW range, where a single-turbine or few-turbine configuration and a simplified linear flow-to-power relationship remain reasonably accurate. Larger multi-unit cascades with staggered dispatch would need a more granular structure.

3. Single offtake / single tariff structure — assumes one PPA tariff (with a defined escalation mechanism) applied to substantially all energy produced. Projects with merchant sales, multiple offtakers, or split contracted/merchant volumes would need the Revenue sheet extended.

4. Conventional project finance structure — a standard senior debt + sponsor equity capital structure, single-tranche debt, straight-line amortization, and a DSRA. Projects with mezzanine debt, multiple debt tranches, sculpted/cash-sweep amortization, or blended concessional financing would require adaptation of the Debt sheet.

5. Annual periodicity is sufficient — suited to long-term feasibility, financing, and lender due diligence where annual cash flows are the standard reporting unit. It is not built for short-term liquidity/working-capital management or intra-year covenant testing that requires quarterly or monthly cash flow detail.

6. Availability of basic hydrological data — requires at least a long-term monthly average flow series and a flow duration curve (even from regional regression or a short gauge record). Projects with no hydrological study at all would need that data commissioned before the model's outputs are meaningful.

7. Fixed-price or largely fixed-scope EPC cost basis — the CAPEX build-up assumes a defined cost breakdown by category with a contingency margin; it is not designed for cost-reimbursable or highly uncertain scope contracts without a defined estimate.

8. Corporate/standard tax and inflation environment — straightforward corporate income tax and general inflation indexation are modelled; projects in jurisdictions with tax holidays, accelerated depreciation incentives, VAT/import duty exemptions, or carbon credit revenue streams would need those features added.

9. Feasibility, financing, and due-diligence stages — most valuable from pre-financing feasibility through financial close and periodic lender monitoring; it is not an operational/real-time SCADA or asset management tool for day-to-day plant dispatch.

10. Users comfortable with Excel-based, formula-driven models — best applied by sponsors, advisors, or lenders who will actively recalibrate assumptions (hydrology, costs, tariff, financing terms) to their specific site rather than use the illustrative defaults as-is.

Conditions Under Which This Financial Model Does Not Apply Ideally

1. Storage/reservoir or pumped-storage hydropower — projects with multi-year or seasonal storage, reservoir regulation, or pumped-storage arbitrage economics need reservoir operation modelling (storage balance, spill rules, multi-year carryover) that this run-of-river structure doesn't provide.

2. Very large or multi-unit cascade schemes — large hydropower (typically well above ~30 MW) or cascades of multiple plants with staggered dispatch, shared infrastructure, or complex hydraulic interaction between units need a more granular, unit-by-unit dispatch structure than the single linear flow-to-power relationship used here.

3. Merchant or multi-offtaker revenue structures — projects selling into a wholesale/merchant market, with variable spot pricing, capacity markets, ancillary services revenue, or multiple offtakers with different tariffs and volumes, need a materially expanded Revenue sheet; this model assumes one tariff applied to substantially all output.

4. Complex capital structures — deals with multiple debt tranches, mezzanine or subordinated debt, sculpted/cash-sweep amortization tied to a target DSCR, interest rate hedging/swaps, or blended concessional and commercial financing need a more sophisticated Debt sheet than the single-tranche, straight-line structure provided.

5. Short-term liquidity or intra-year cash management — because the model runs on annual periods, it is not suited to working-capital management, seasonal cash flow timing within a year, or covenant tests that require quarterly/monthly granularity.

6. Projects without any hydrological data — sites lacking even a regional flow duration curve or a long-term average monthly flow series will produce unreliable outputs; the model doesn't generate hydrology from first principles (e.g., rainfall-runoff modelling) — it consumes hydrological study outputs as an input.

7. Uncertain or cost-reimbursable EPC scope — projects without a defined CAPEX estimate (e.g., very early-stage concepts, cost-plus contracts, or highly uncertain scope) will not benefit from the fixed cost-category build-up and contingency approach used here.

8. Special tax, incentive, or environmental revenue regimes — projects benefiting from tax holidays, accelerated/bonus depreciation, import duty exemptions, carbon credits (Article 6, voluntary carbon markets), green certificates, or capacity payments need those revenue/tax mechanics added; the base model only handles standard corporate tax and inflation indexation.

9. Non-USD, multi-currency, or hedged financing structures — the model works in a single base currency without FX translation, hedging costs, or multi-currency debt tranches; projects with foreign-currency debt against local-currency revenue need a currency risk module layered in.

10. Operational/asset management use — this is a financing and feasibility tool, not a SCADA, dispatch, or real-time operations and maintenance management system; it won't support day-to-day plant operating decisions or real-time production monitoring.

11. Non-power-generation renewable technologies — solar, wind, battery storage, or thermal generation projects have fundamentally different production drivers (irradiance, wind speed, degradation curves, dispatch/charging logic) and would need a different production/energy sheet entirely, even though the financing/returns architecture could be adapted.