Publication number: ELQ-20266-1

View all versions & Certificate

Offshore Wind Ultimate Model + Portfolio Manager — From Single Offshore Project to Full Pipeline in One Purchase

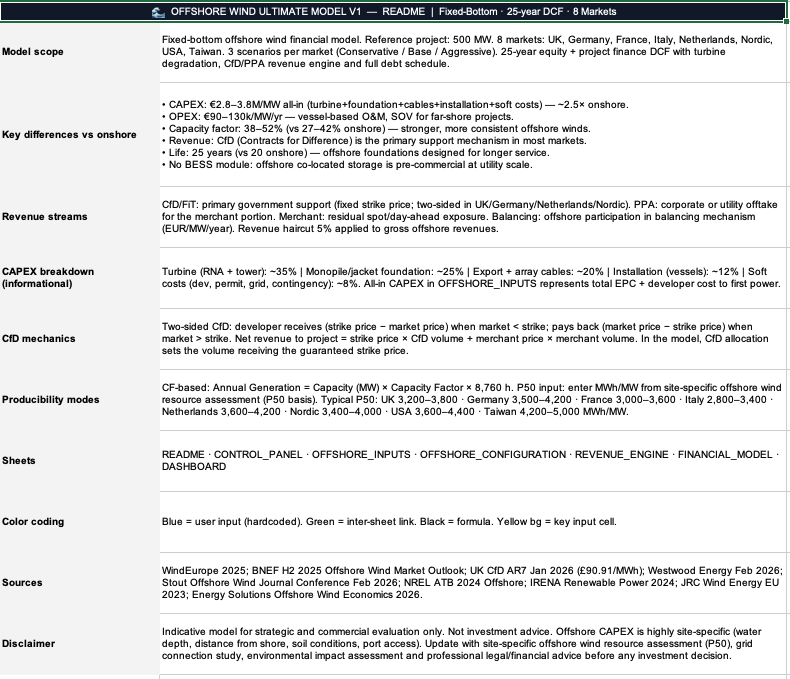

The Offshore Wind Ultimate Model and Portfolio Manager bundled together. Build a bankable fixed-bottom offshore wind business case for any of 8 markets,

Further information

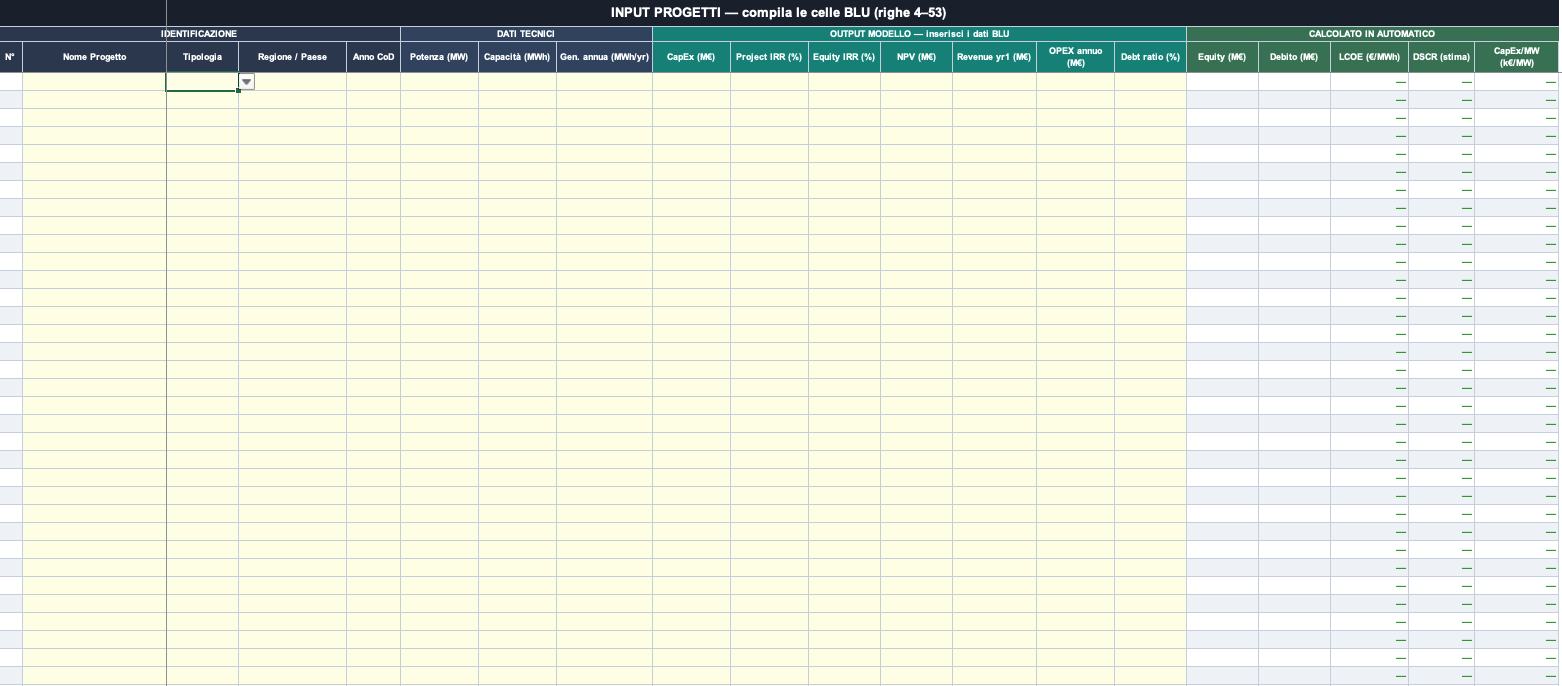

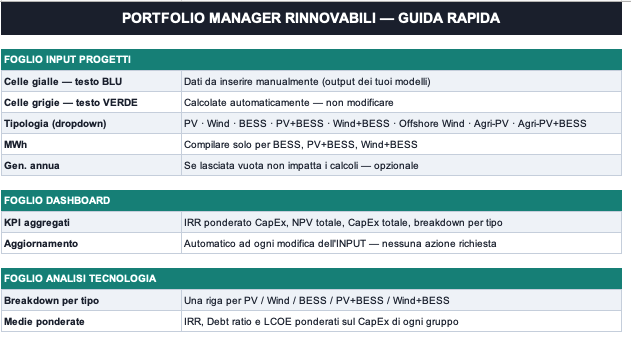

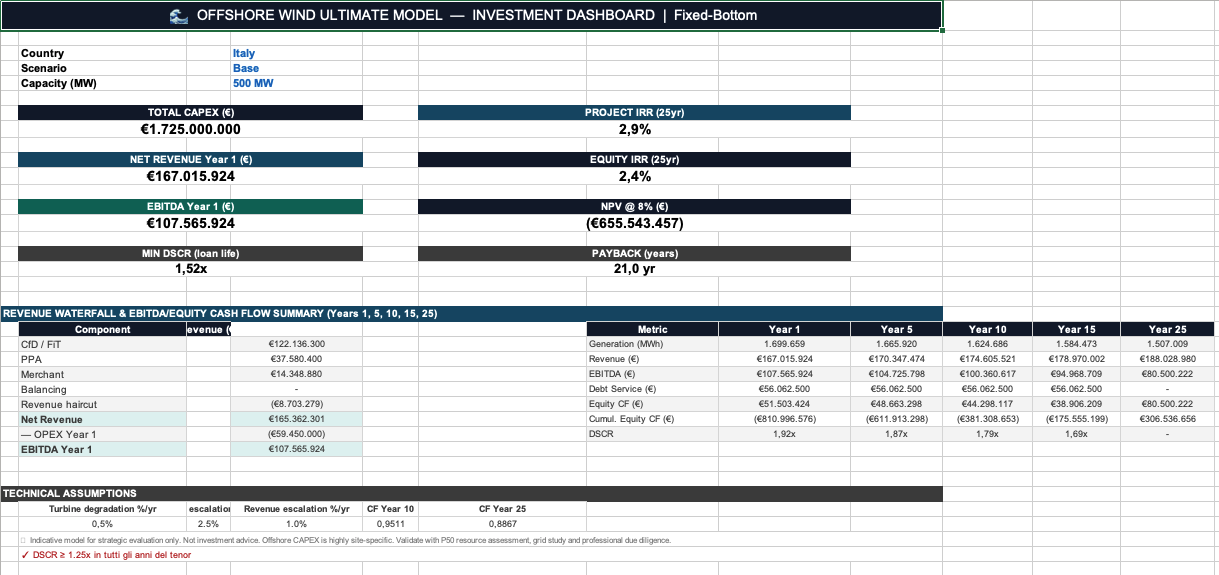

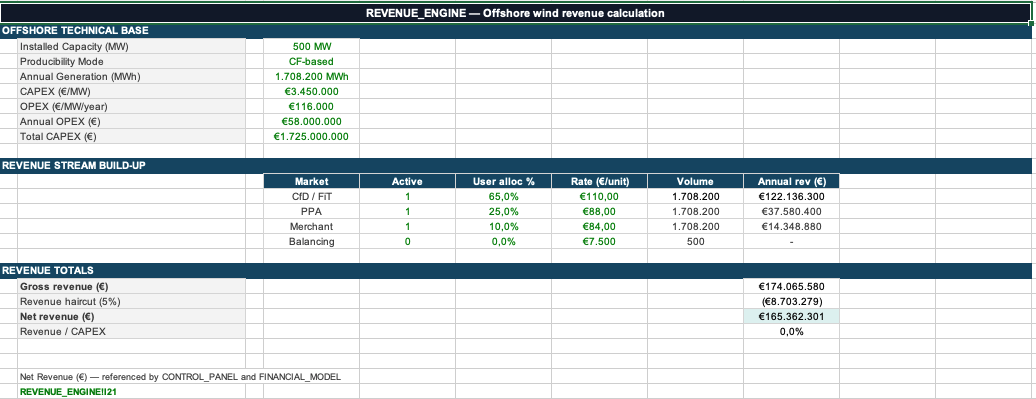

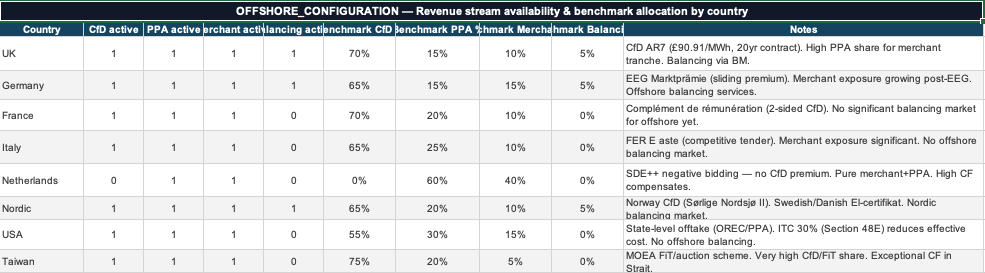

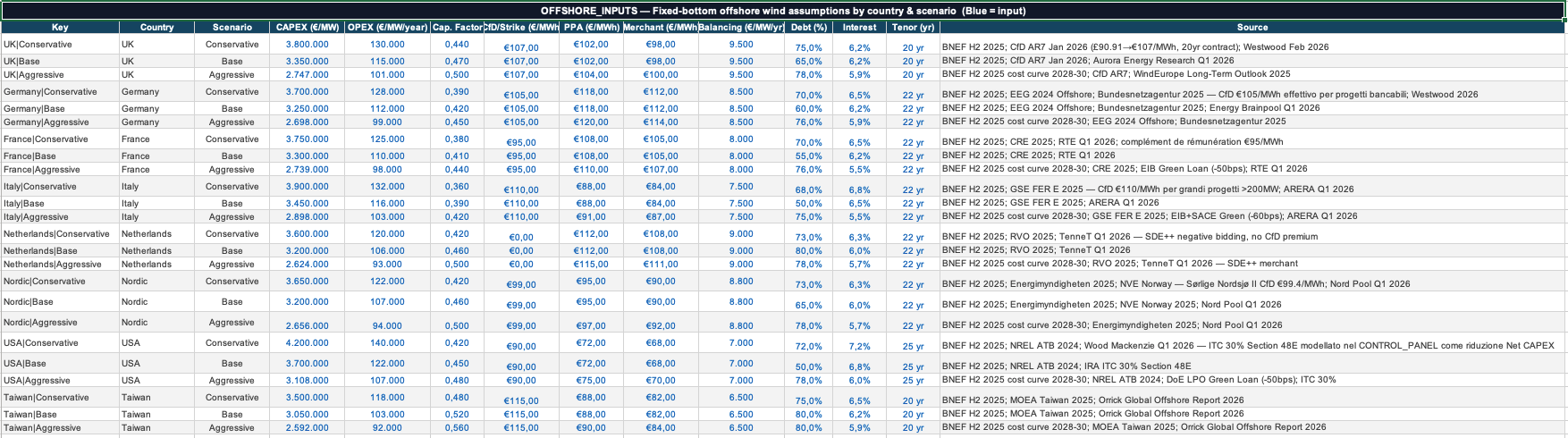

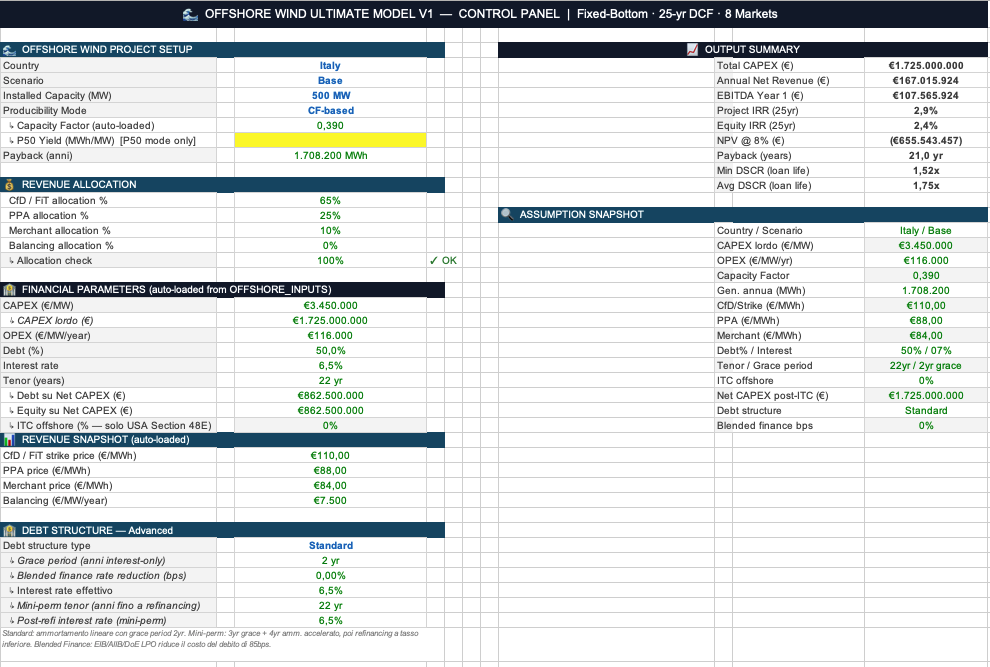

This bundle enables developers, advisors and investors to evaluate individual fixed-bottom offshore wind projects across 8 international markets and aggregate their results into a consolidated portfolio view without building either tool from scratch. The Offshore Wind Ultimate Model produces Project IRR, Equity IRR, NPV, Min DSCR and Avg DSCR from a fully integrated 25-year cash flow with turbine degradation, two-sided CfD revenue mechanics, country-specific market configurations and three debt structure options — standard, mini-perm and blended finance. The Portfolio Manager aggregates those outputs alongside projects of any other technology into a CapEx-weighted portfolio IRR, total NPV, LCOE per project, DSCR traffic light and a technology breakdown across up to 50 active projects.

This bundle is best suited to professionals evaluating fixed-bottom offshore wind projects in the 200–1,000 MW range at early-stage feasibility or commercial evaluation, where the CfD or FiT support structure is known and the debt financing approach is being screened. It works particularly well for UK, German, French and Nordic markets where CfD mechanics are central to the revenue structure, and for USA projects where the IRA Section 48E ITC needs to be reflected in the financial model. It is also well suited to portfolio contexts where offshore wind sits alongside onshore renewables and the investor needs a single consolidated view of returns across technologies.

This model covers fixed-bottom offshore wind only and is not designed for floating offshore wind, which has a materially different cost structure, installation methodology and financing profile. It does not include a co-located BESS module, as offshore battery storage at utility scale remains pre-commercial. CAPEX assumptions are highly site-specific in offshore wind — water depth, distance from shore, soil conditions and port access can each shift the all-in cost significantly — and the model's pre-loaded assumptions should be treated as a starting point requiring site-specific validation before any investment decision. Neither tool replaces full project finance models, environmental impact assessments or grid connection studies required for a final financing or investment decision.