Last version published: 12/11/2025 12:37

Publication number: ELQ-97275-6

View all versions & Certificate

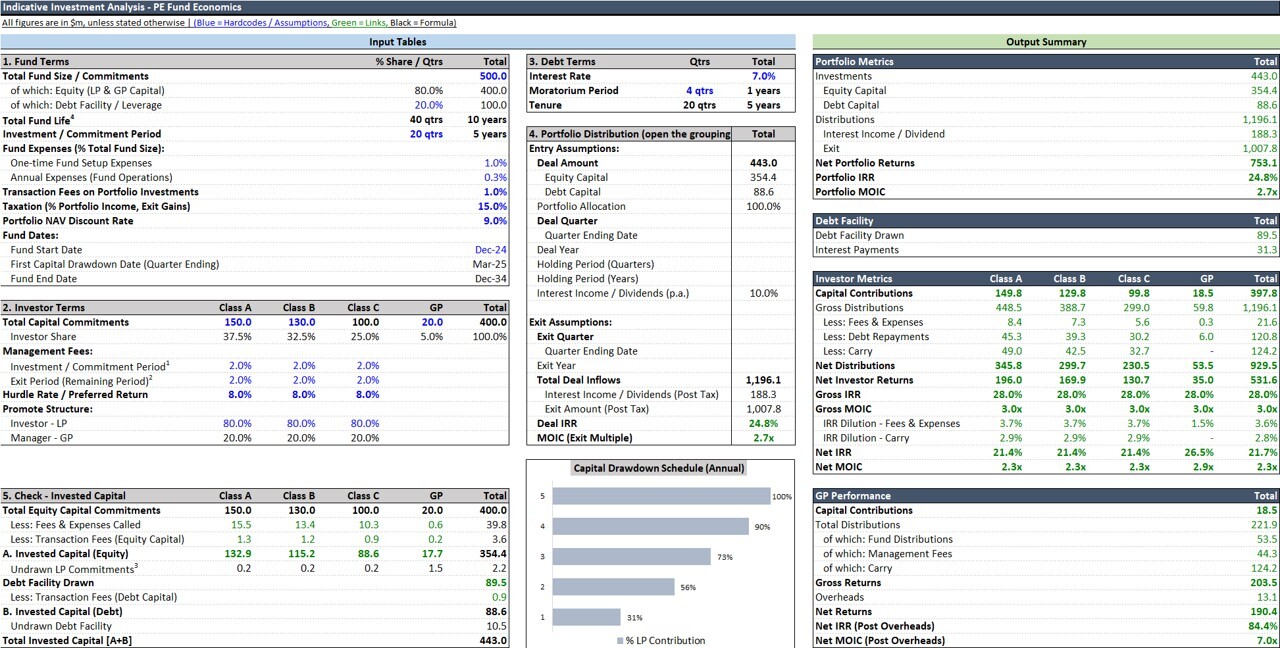

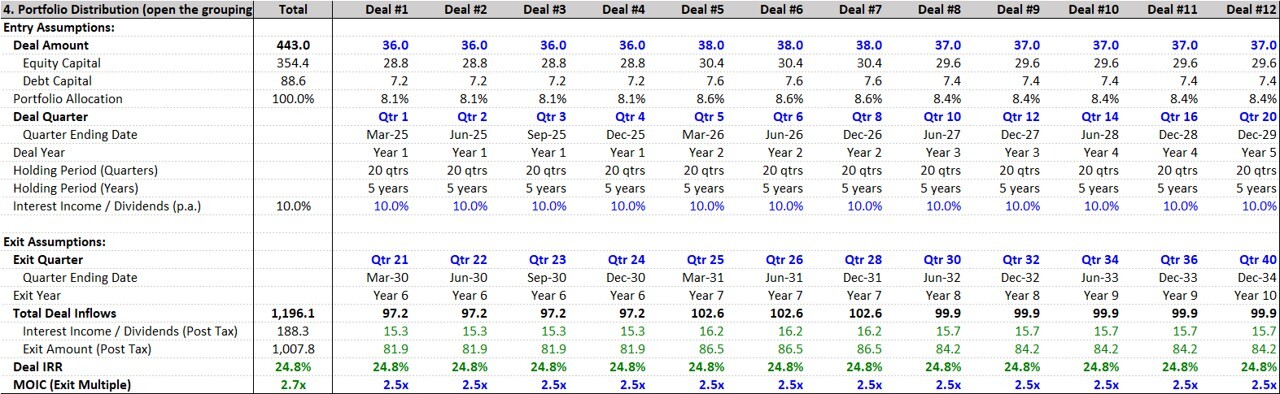

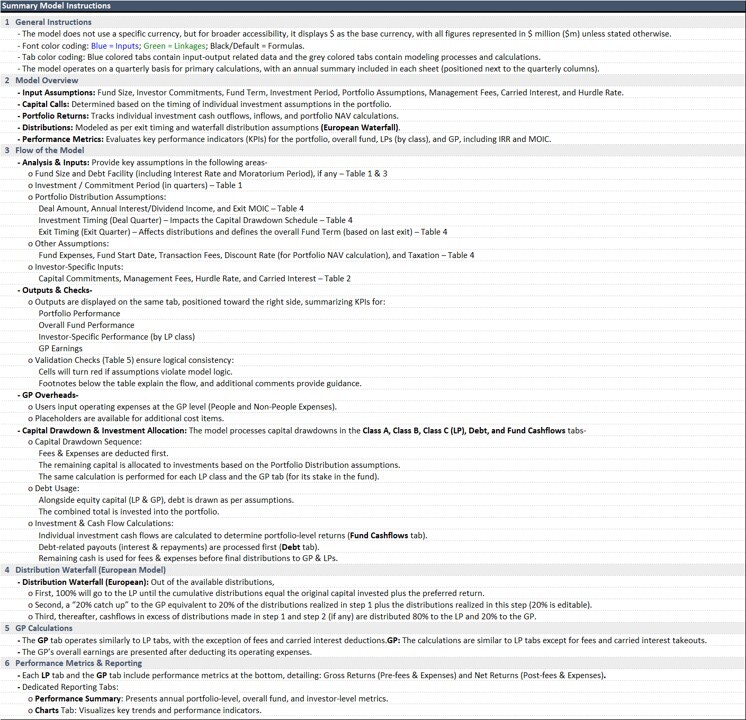

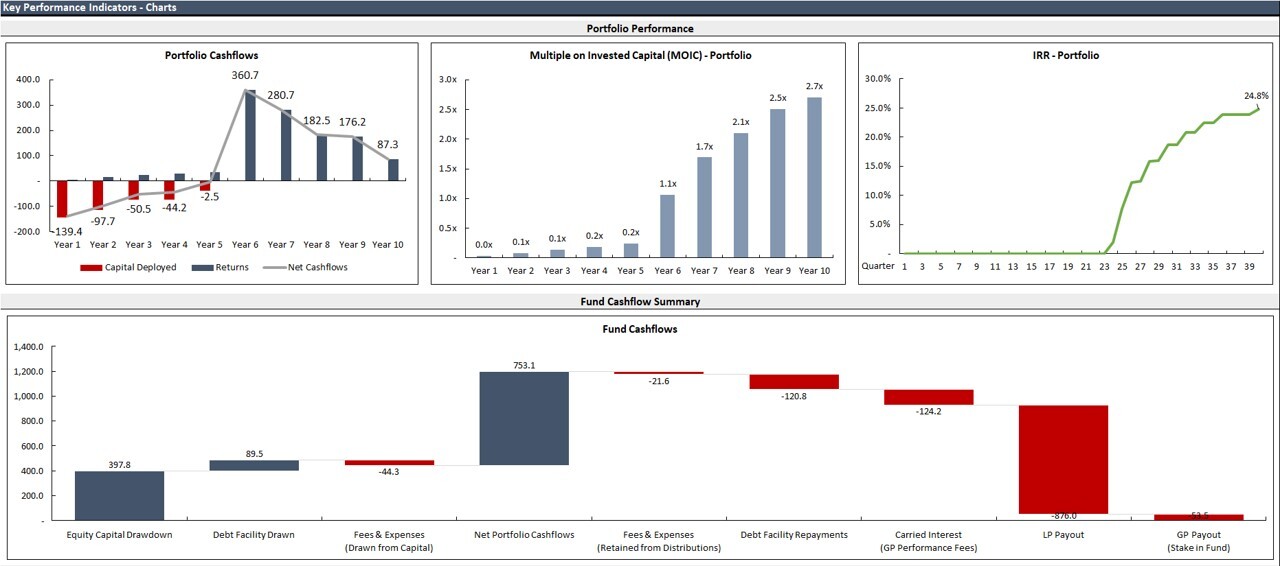

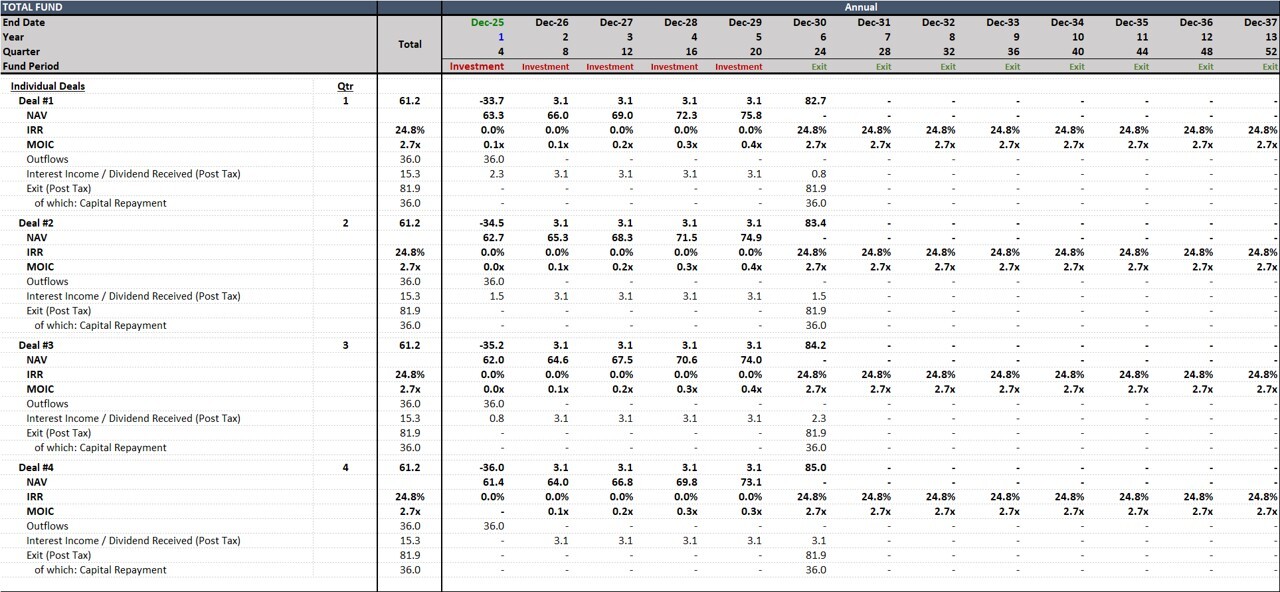

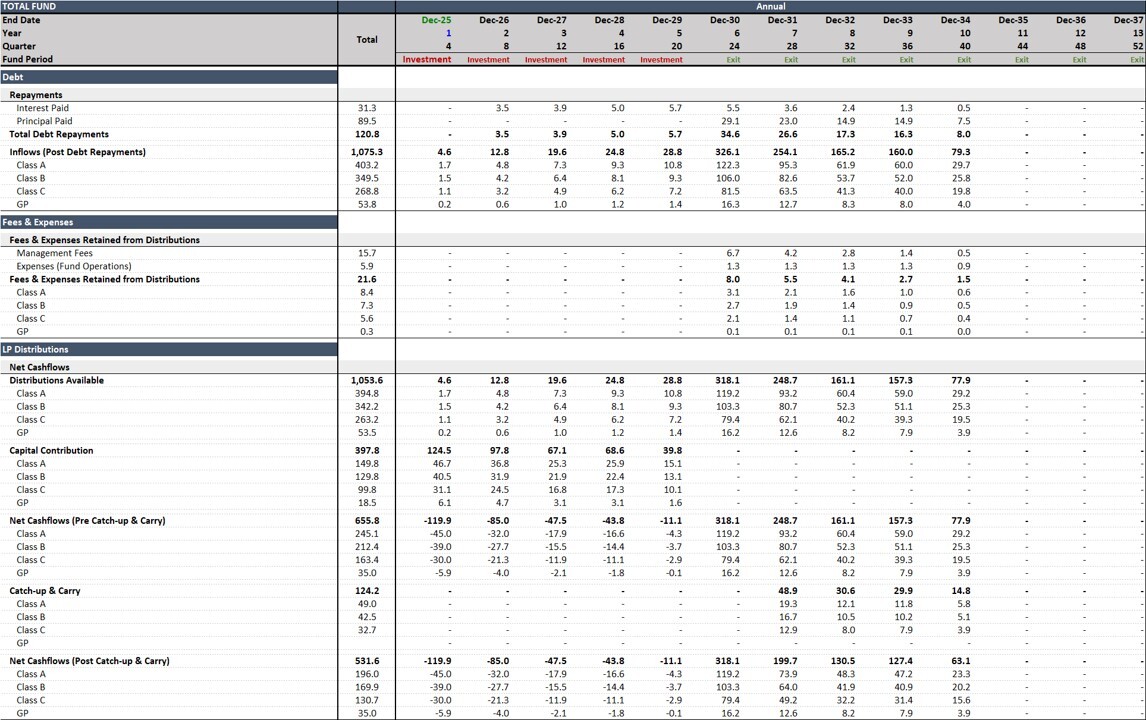

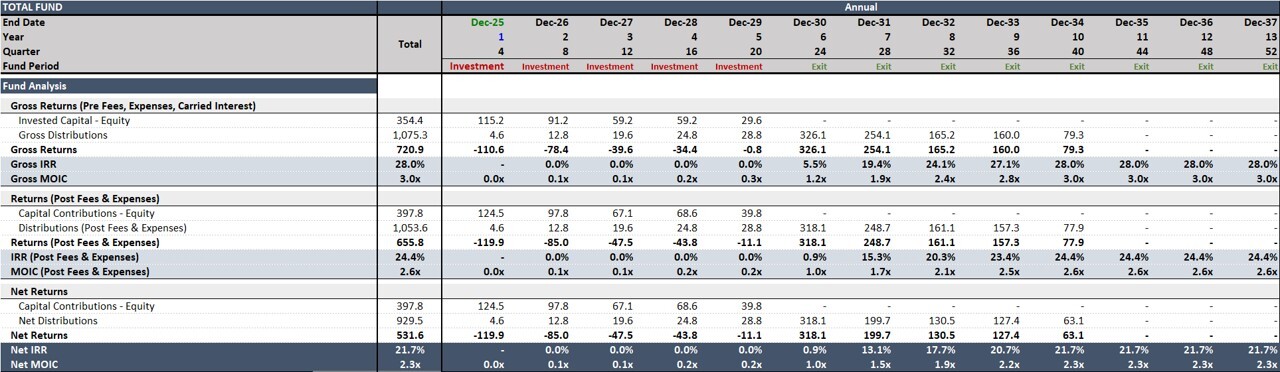

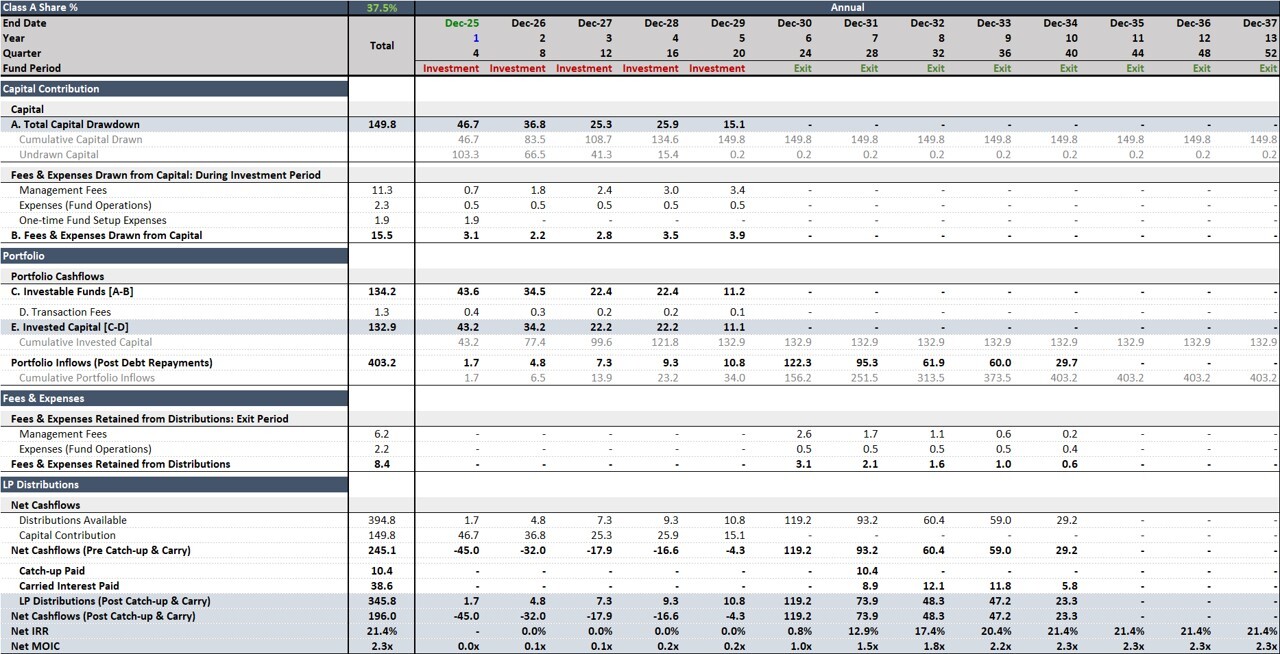

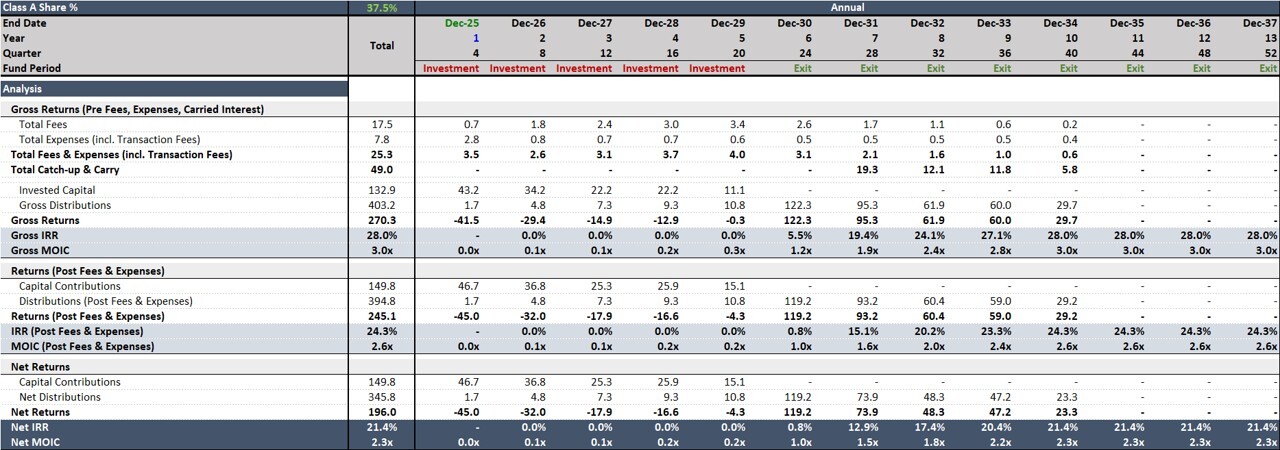

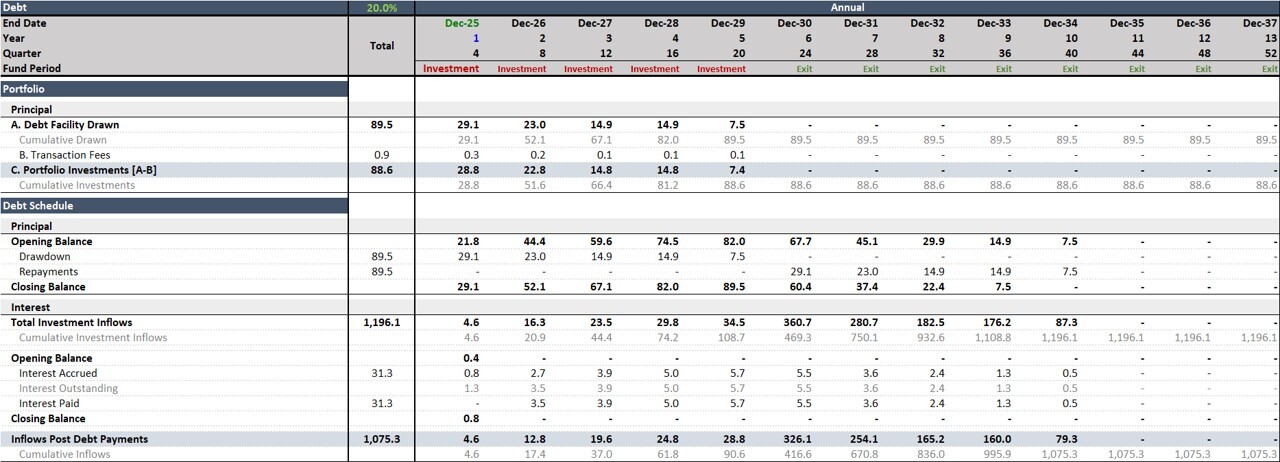

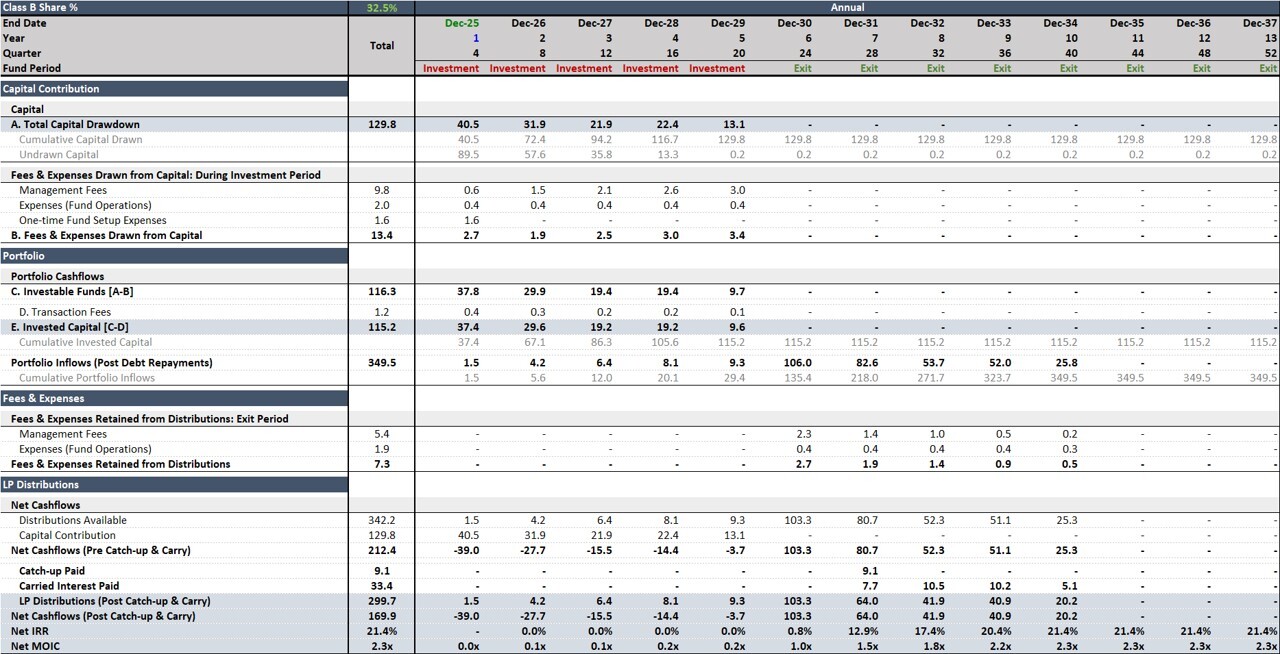

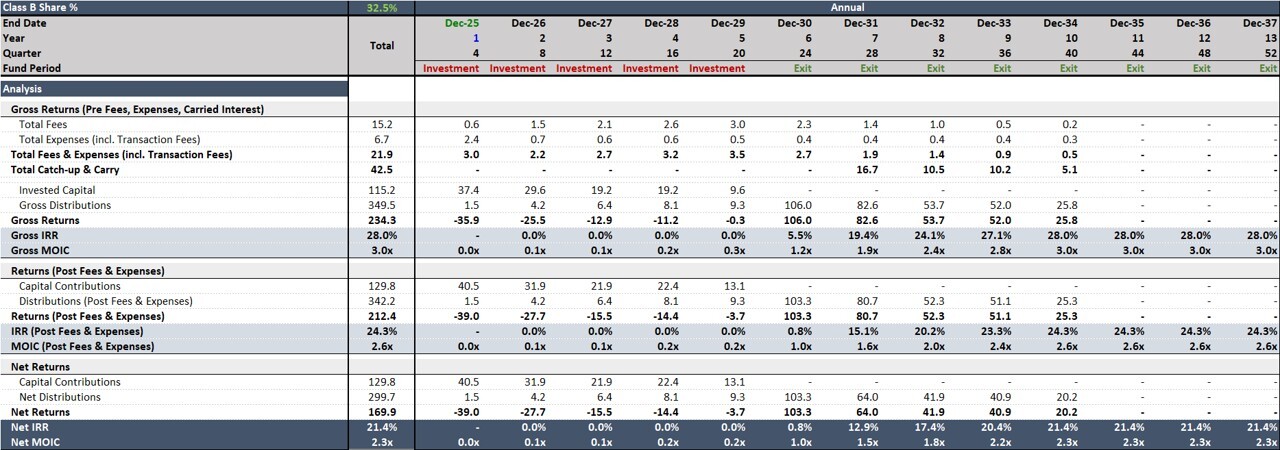

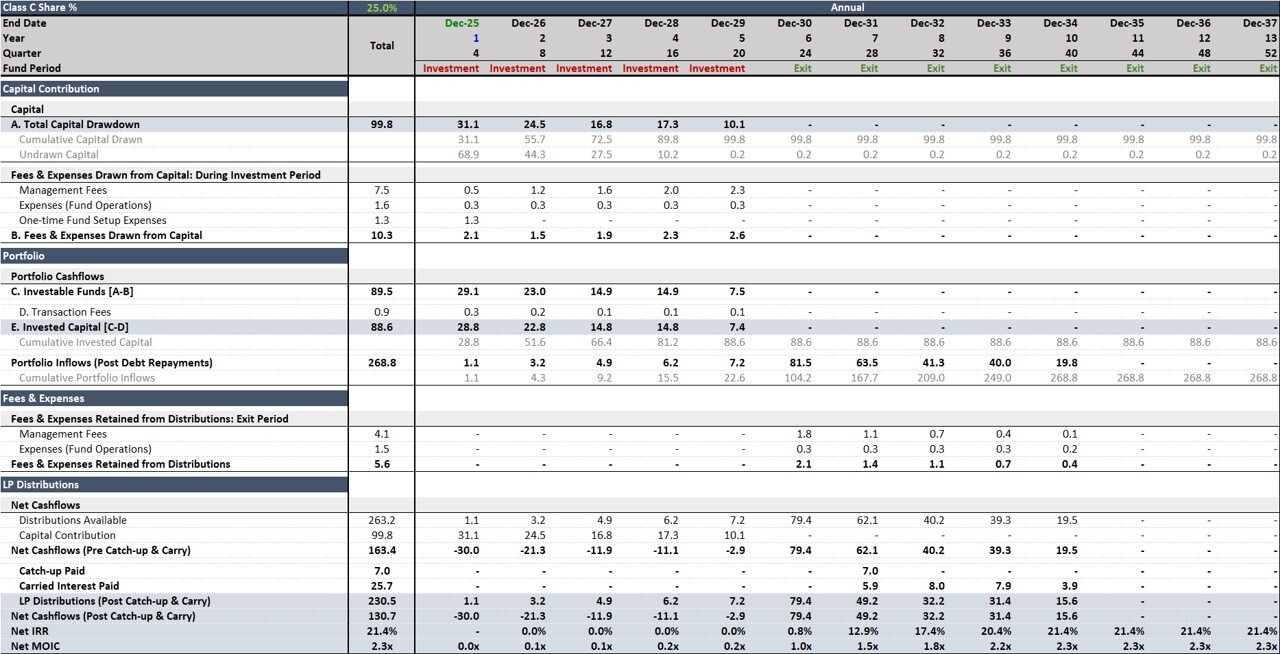

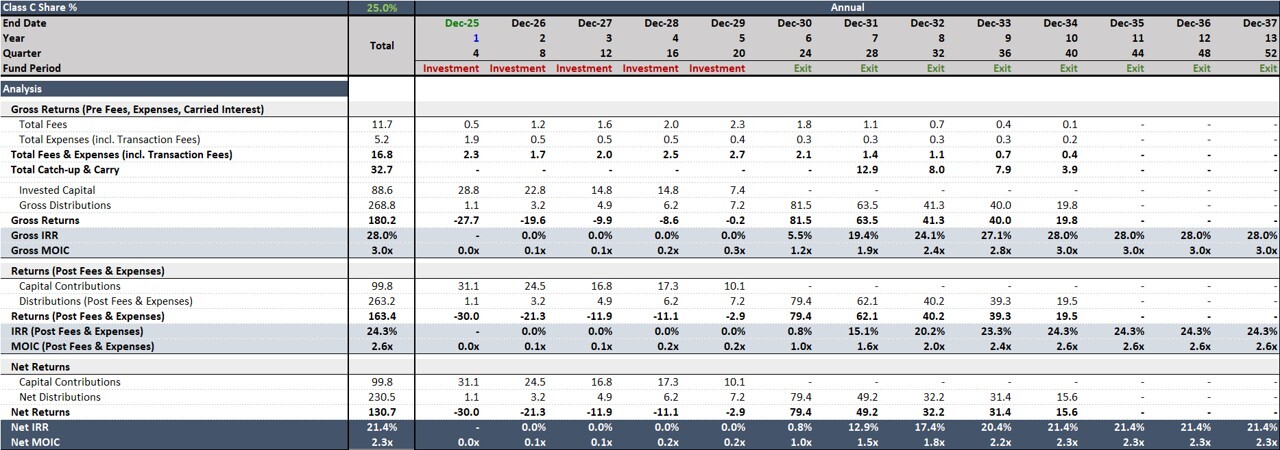

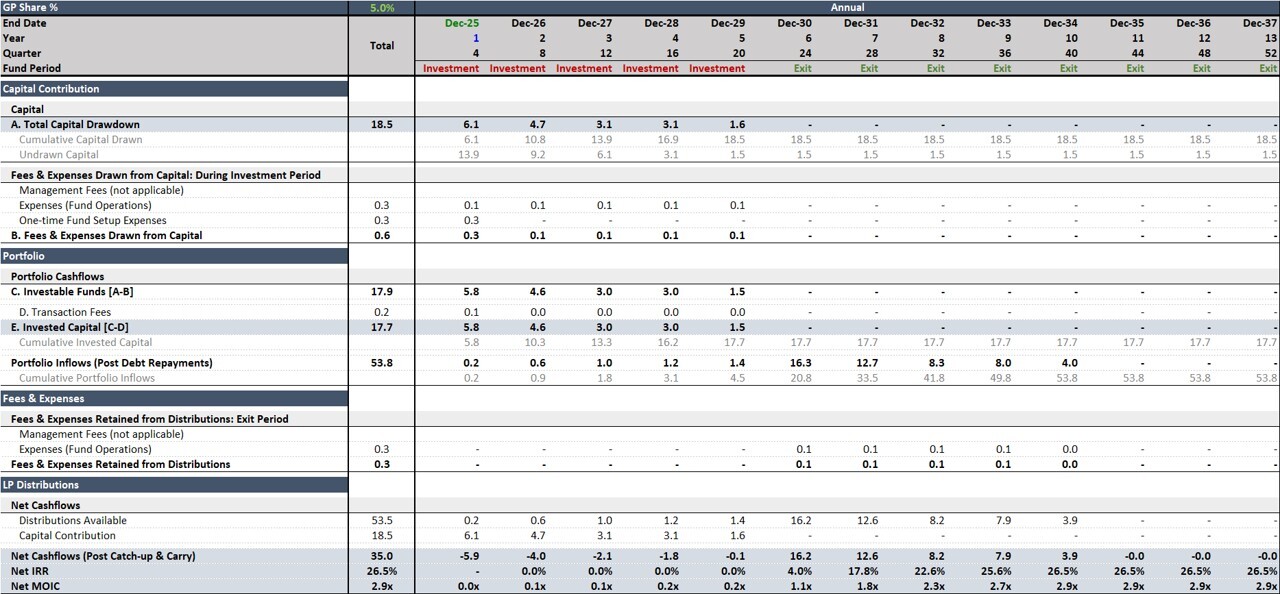

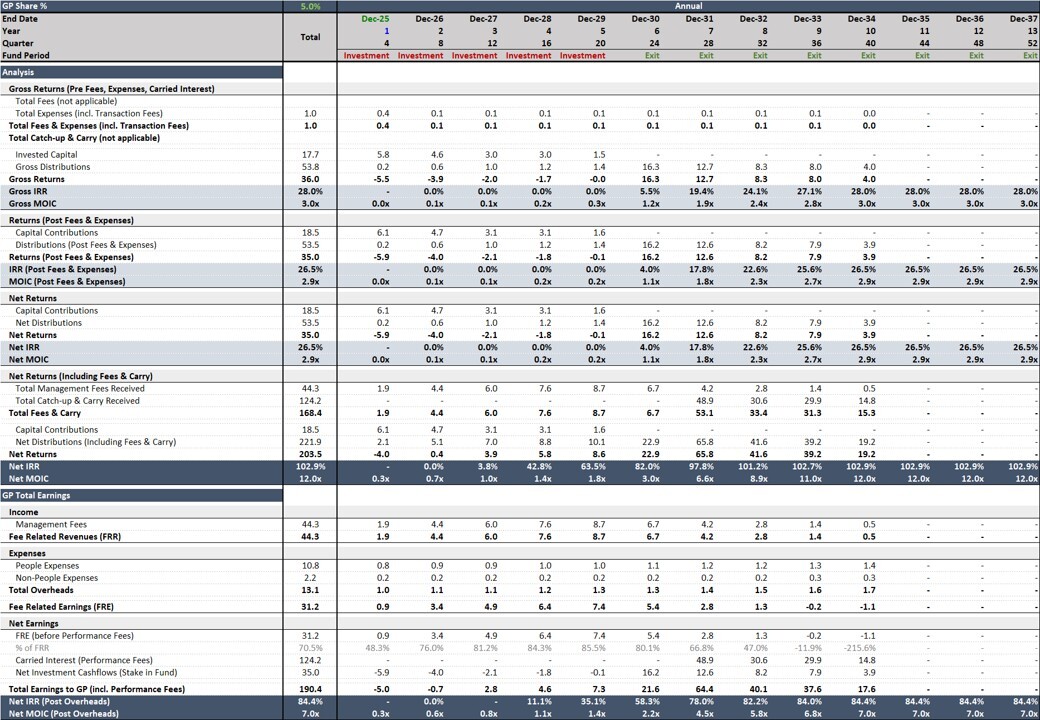

Private Equity Fund Cashflows Model

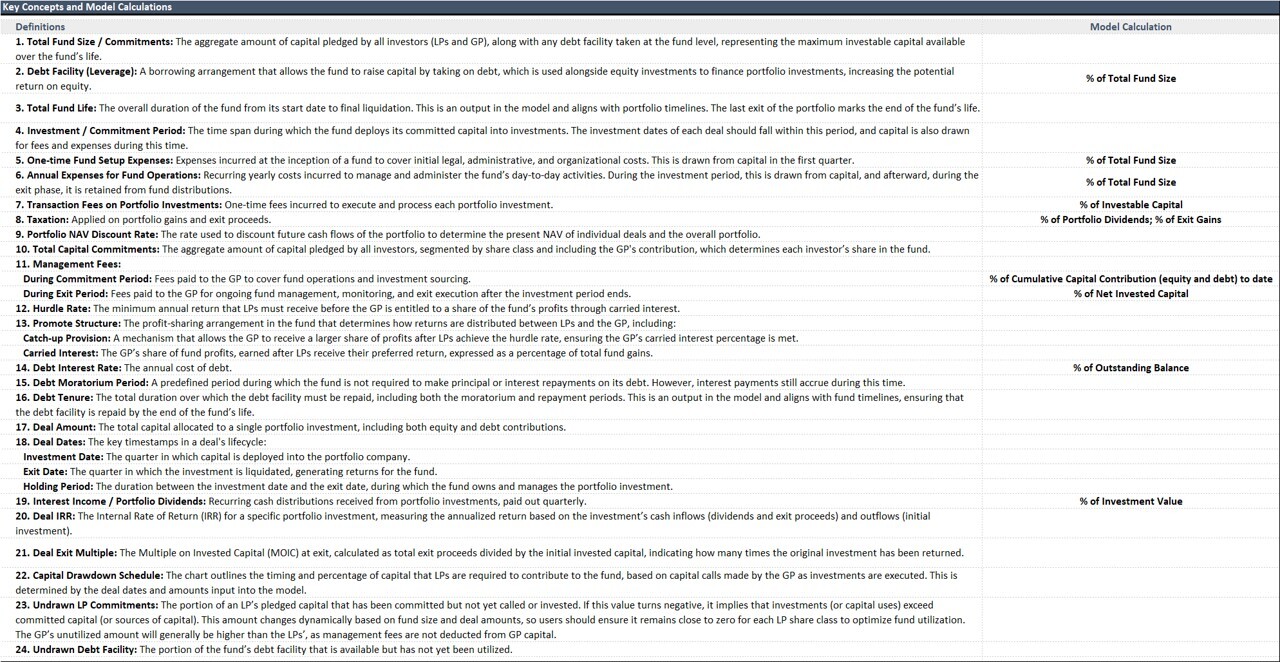

The Private Equity Fund Cashflows Model is designed to help LPs and GPs analyze fund cash flows and returns at all the investor, manager, and portfolio levels.

Further information

This model aims to provide a robust, standardized framework for evaluating private equity fund performance. It helps users simulate capital flows, assess fund-level returns, understand waterfall structures, and evaluate the impact of assumptions. Whether for deal screening, fund structuring, or investor presentations, the model serves as a decision-making tool for professionals needing transparency, accuracy, and flexibility in fund analysis.

This model works best for analyzing closed-ended private equity funds using American or European waterfall structures. It is highly effective for fund managers, analysts, and investors looking to model capital drawdowns, distributions, returns, and sensitivity scenarios. While optimized for traditional PE fund structures, its modular design allows easy adaptation for sector-specific strategies, fund variants, and tailored investment scenarios.

The model is built for closed-ended private equity fund structures and may require customization for open-ended funds, complex multi-tiered waterfalls, or region-specific regulatory layers. While not configured for these out-of-the-box, the framework is flexible and can be easily extended to suit such use cases with minimal adjustments.