Originally published: 06/02/2023 10:54

Last version published: 20/11/2023 10:55

Publication number: ELQ-69880-5

View all versions & Certificate

Last version published: 20/11/2023 10:55

Publication number: ELQ-69880-5

View all versions & Certificate

IFRS 16 Lease Accounting Excel Calculation Model

Excel calculation model to calculate accounting movements and balances for up to 15 lease agreements based on IFRS 16 requirements from a lessee perspective.

ifrslease accountinglesseedashboardlease liabilityright-of-use assetexcelcalculation modellease agreementcash flow

Description

PURPOSE OF MODEL

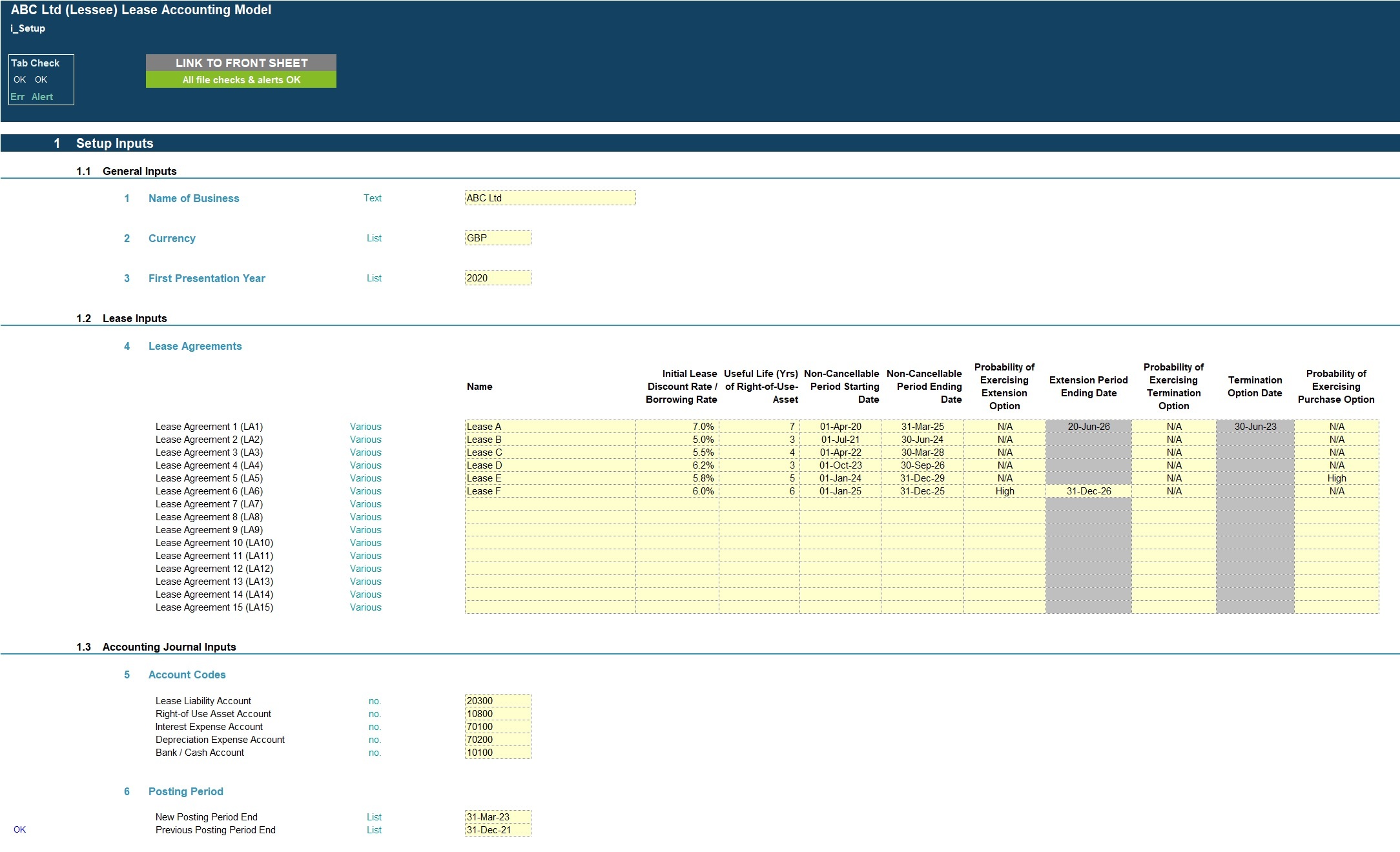

User-friendly Excel calculation model to calculate accounting movements and balances for up to 15 lease agreements based on IFRS 16 requirements from a lessee perspective. These include lease liability balances, interest expense, right-of-use asset balances, depreciation charges, lease payments, changes in discount rates and months to maturity. The calculation model will automate the lease accounting calculations, journal entries and key disclosures and intended as a supporting working file for the General Ledger lease agreement postings.

The calculation model summarises the balances and movements across all lease agreements for a presentation period of up to 5 years as selected by the user which is available on a monthly and annual basis. The calculation model also includes adjustments for extension, termination and purchase options and journal entries.

The model follows good practice financial modelling principles and includes instructions, line item explanations, checks and input validations.

KEY OUTPUTS

The calculation model is generic and not industry-specific. The key outputs include:

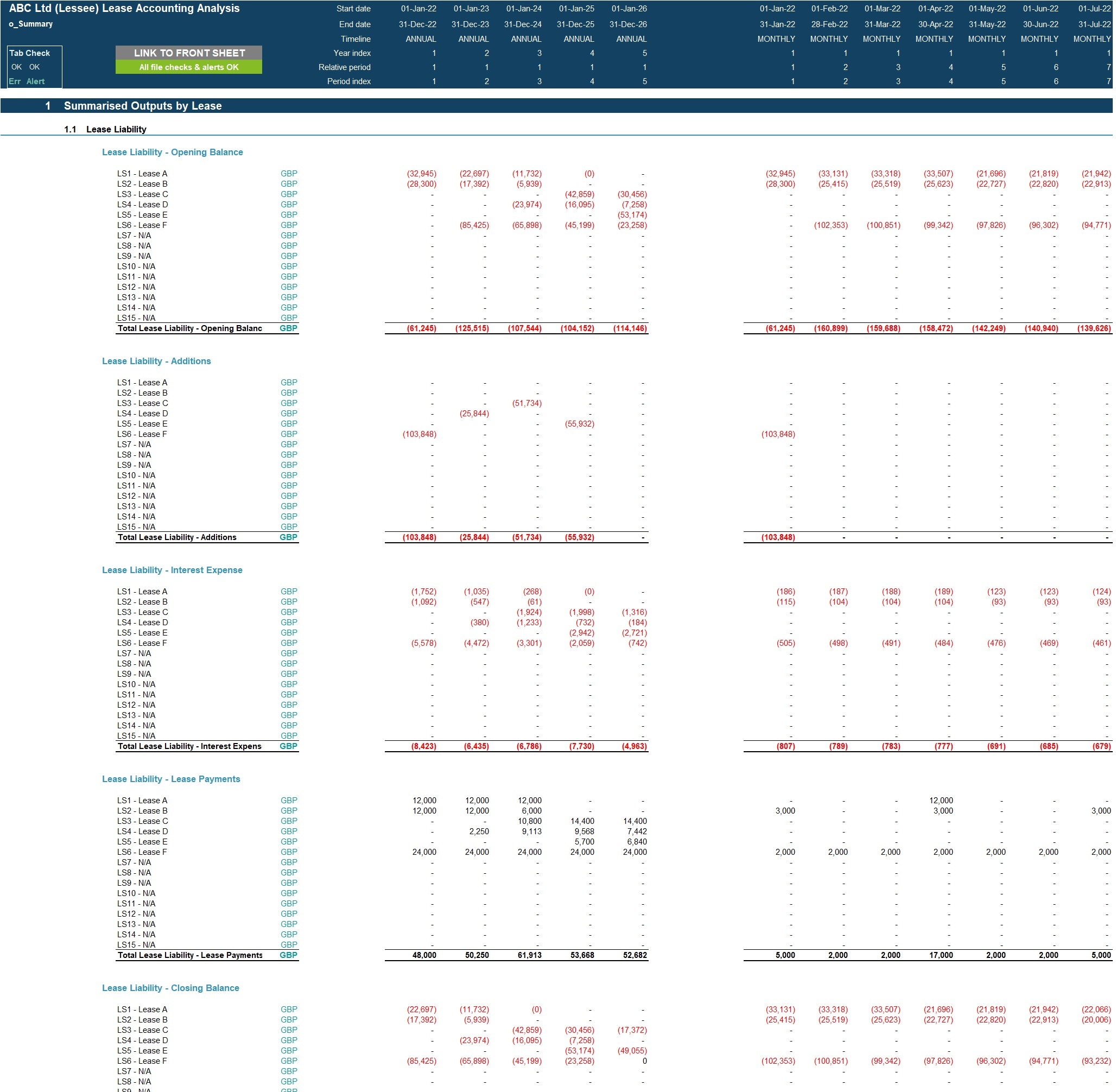

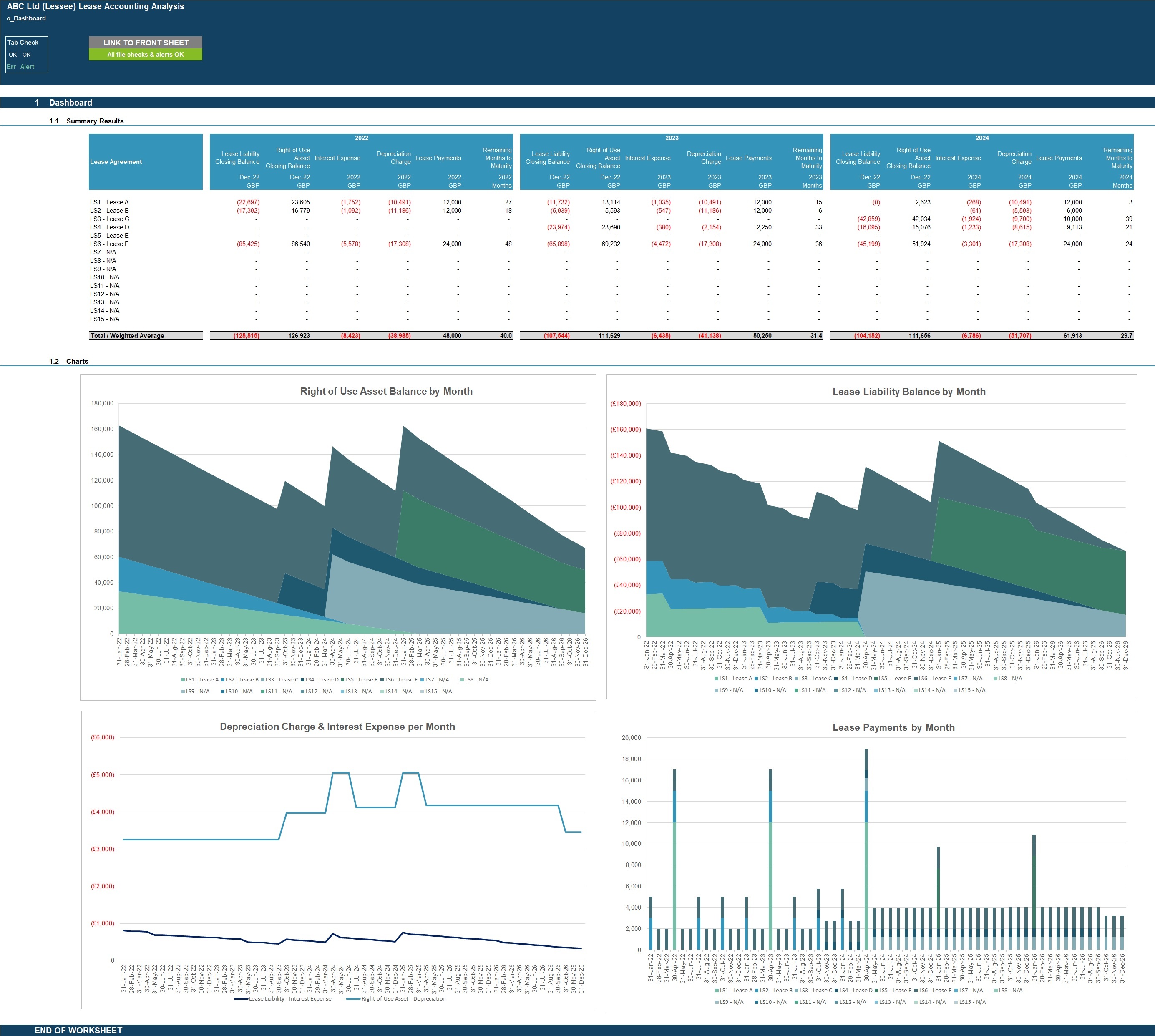

- Lease liability control account on a monthly and annual basis and by lease agreement. Control account includes opening balance, additions, interest expense, changes in discount rates, lease payments and closing balance.

- Right-of-use asset control account on a monthly and annual basis and by lease agreement. Control account includes opening balance, additions, changes in discount rate, depreciation charge and closing balance.

- Months to maturity calculation on a monthly and annual basis and by lease agreement as well as overall weighted average.

- Charts showing lease liability and right-of-use asset balances by month.

- Charts showing depreciation charge, interest expenses and lease payments by month.

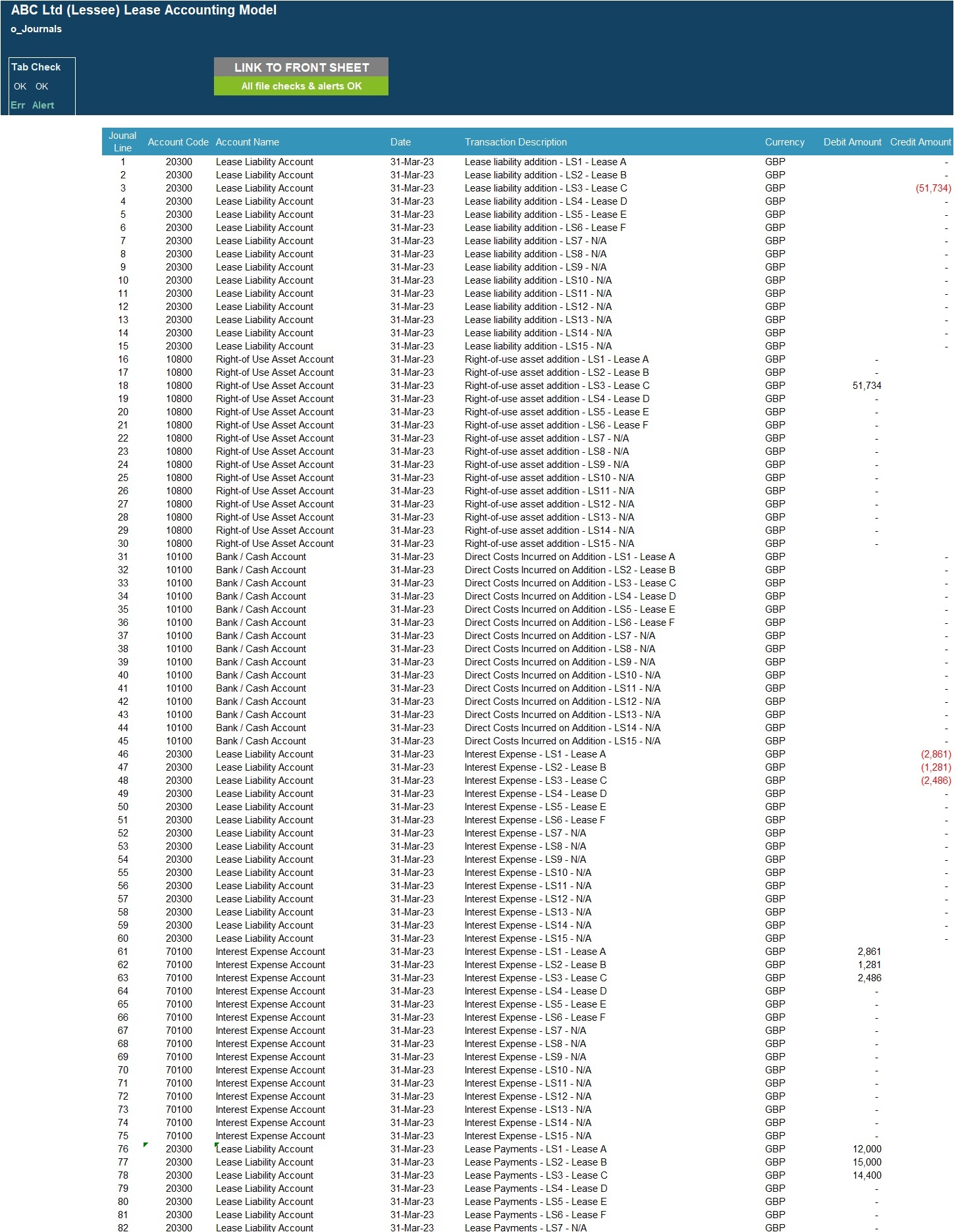

- Journal entries for selected period including additions, lease payments, interest expense, depreciation expense and change in discount rates.

KEY INPUTS

Inputs are split into setup inputs and cash flow item inputs. All inputs include user-friendly line item explanations and input validations to help users understand what the input is for and populate correctly.

Setup Inputs:

- Name of business;

- Currency;

- First presentation year;

- Names of lease agreements;

- Lease discount rate;

- Lease useful life;

- Non-cancellable starting and ending periods;

- Extension period (if applicable) and probability of exercising extension option;

- Termination period (if applicable) and probability of exercising termination option;

- Probability of exercising purchase option;

- Account codes for journal entries;

- New and previous posting period for journal entries.

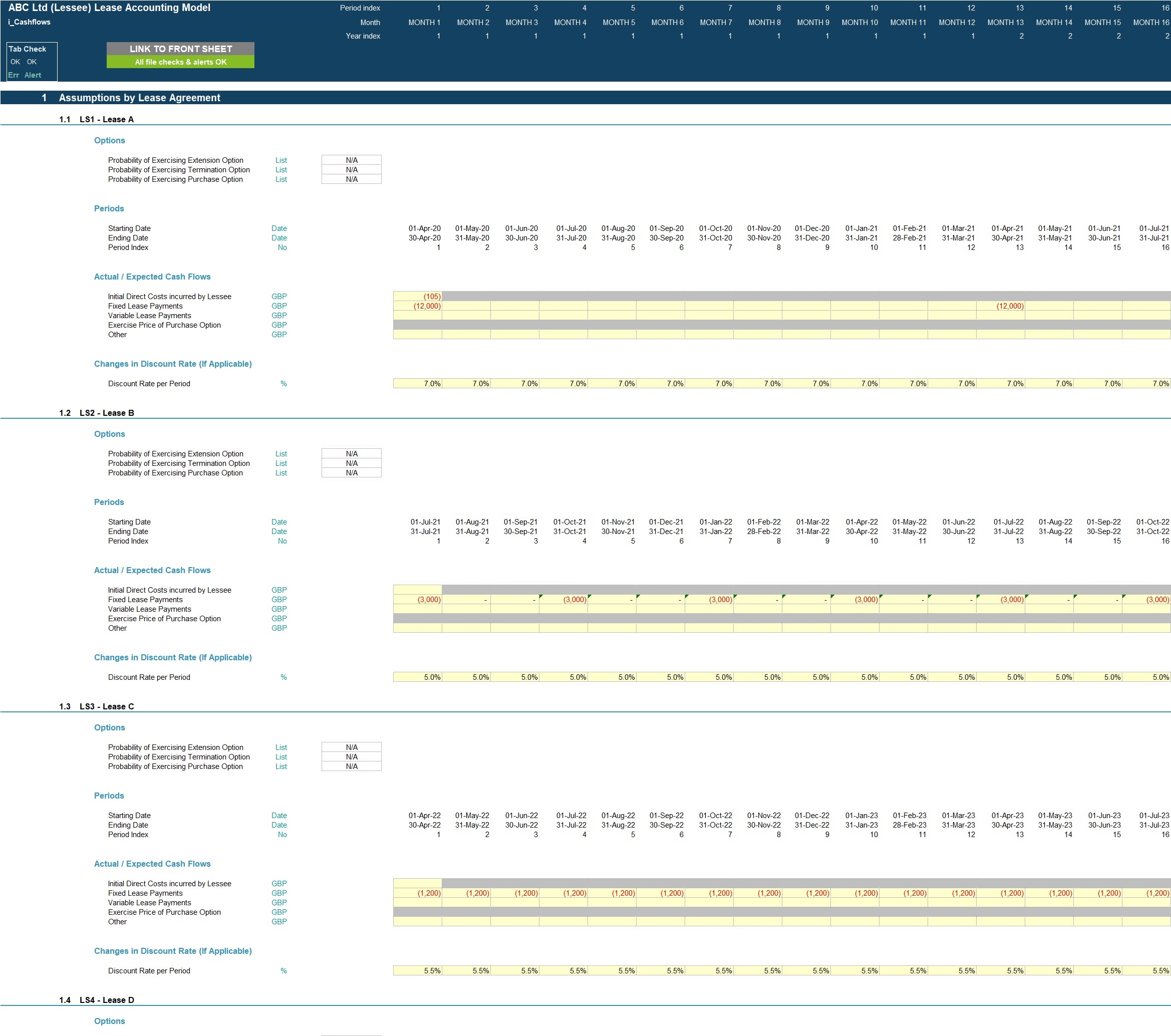

Cash flow inputs:

- Initial direct costs incurred (if applicable);

- Fixed lease payments;

- Variable lease payments (if applicable);

- Exercise price of purchase option (if applicable);

- Other cash flows (if applicable);

- Changes in discount rate by period.

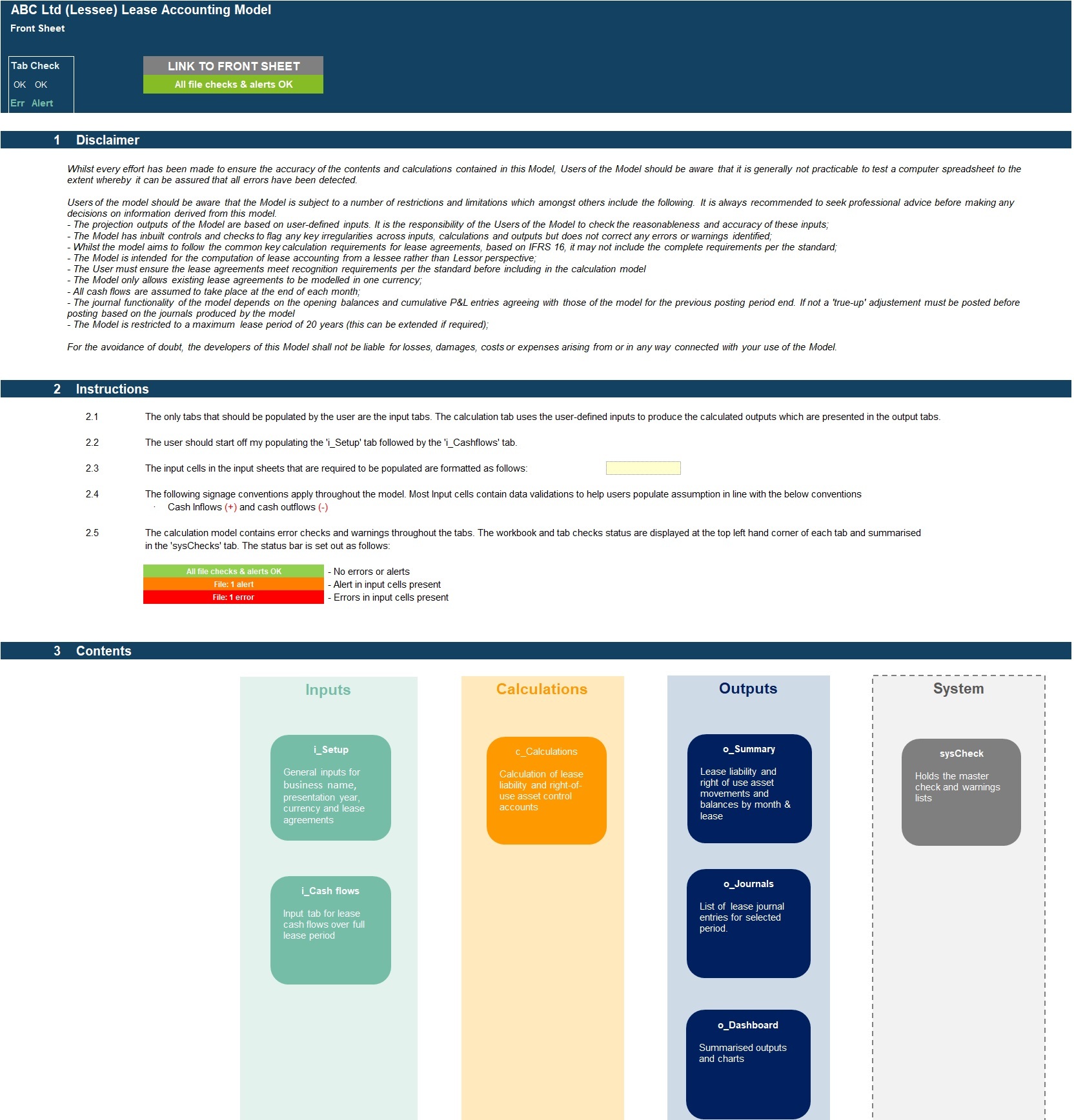

MODEL STRUCTURE

The model comprises of 8 tabs split into input ('i_'), calculation ('c_'), output ('o_’) and system tabs. The tabs to be populated by the user are the input tabs which include ‘i_Setup’ for setup assumptions, ‘i_cashflows’ to input applicable lease cash flows. The calculation tabs takes the user-defined inputs to calculate and produce the outputs which are presented in the ‘o_summary’, ‘o_journals’ and ‘o_Dashboard’ tabs.

System tabs include:

- A 'Front Sheet' containing a disclaimer, instructions and contents;

- A checks dashboard containing a summary of checks by tab.

KEY FEATURES

Other key features of this tool include the following:

- The model follows good practice financial modelling guidelines and includes instructions, line item explanations, checks and input validations;

- The model allows for a maximum of 15 lease agreements (this can be extended if required).

- The model allows the inclusion of extension, termination and purchase options with drop down to select probability option will be exercised;

- The model includes 5 different cash flow types for each lease agreement including: initial direct costs, fixed lease payments, variable lease payments, exercise price of purchase option and any other cash flows;

- The model allows for lease agreements with any starting and ending date to be included and summarises lease balance and movement results across a 5 year period as selected by the user;

- Business name, currency, first presentation year and lease assumptions are fully customisable

- The model includes a checks dashboard which summarises all the checks included in the various tabs making it easier to identify any errors.

ABOUT PROJECTIFY

We are financial modelling professionals with experience working in big 4 business modelling teams and strong experience supporting businesses with their financial planning and decision support needs. Our aim is to provide robust and easy-to-use models that follow good practice financial modelling guidelines and assist individuals and businesses with key financial planning and analysis processes.

We are keen to make sure our customers are satisfied with the tools / models they purchase and will be more than happy to assist with any questions or support required following or in advance of purchase.

We are also always keen to receive feedback so please do let us know any feedback you have on our models by sending us a message or submitting a review.

PURPOSE OF MODEL

User-friendly Excel calculation model to calculate accounting movements and balances for up to 15 lease agreements based on IFRS 16 requirements from a lessee perspective. These include lease liability balances, interest expense, right-of-use asset balances, depreciation charges, lease payments, changes in discount rates and months to maturity. The calculation model will automate the lease accounting calculations, journal entries and key disclosures and intended as a supporting working file for the General Ledger lease agreement postings.

The calculation model summarises the balances and movements across all lease agreements for a presentation period of up to 5 years as selected by the user which is available on a monthly and annual basis. The calculation model also includes adjustments for extension, termination and purchase options and journal entries.

The model follows good practice financial modelling principles and includes instructions, line item explanations, checks and input validations.

KEY OUTPUTS

The calculation model is generic and not industry-specific. The key outputs include:

- Lease liability control account on a monthly and annual basis and by lease agreement. Control account includes opening balance, additions, interest expense, changes in discount rates, lease payments and closing balance.

- Right-of-use asset control account on a monthly and annual basis and by lease agreement. Control account includes opening balance, additions, changes in discount rate, depreciation charge and closing balance.

- Months to maturity calculation on a monthly and annual basis and by lease agreement as well as overall weighted average.

- Charts showing lease liability and right-of-use asset balances by month.

- Charts showing depreciation charge, interest expenses and lease payments by month.

- Journal entries for selected period including additions, lease payments, interest expense, depreciation expense and change in discount rates.

KEY INPUTS

Inputs are split into setup inputs and cash flow item inputs. All inputs include user-friendly line item explanations and input validations to help users understand what the input is for and populate correctly.

Setup Inputs:

- Name of business;

- Currency;

- First presentation year;

- Names of lease agreements;

- Lease discount rate;

- Lease useful life;

- Non-cancellable starting and ending periods;

- Extension period (if applicable) and probability of exercising extension option;

- Termination period (if applicable) and probability of exercising termination option;

- Probability of exercising purchase option;

- Account codes for journal entries;

- New and previous posting period for journal entries.

Cash flow inputs:

- Initial direct costs incurred (if applicable);

- Fixed lease payments;

- Variable lease payments (if applicable);

- Exercise price of purchase option (if applicable);

- Other cash flows (if applicable);

- Changes in discount rate by period.

MODEL STRUCTURE

The model comprises of 8 tabs split into input ('i_'), calculation ('c_'), output ('o_’) and system tabs. The tabs to be populated by the user are the input tabs which include ‘i_Setup’ for setup assumptions, ‘i_cashflows’ to input applicable lease cash flows. The calculation tabs takes the user-defined inputs to calculate and produce the outputs which are presented in the ‘o_summary’, ‘o_journals’ and ‘o_Dashboard’ tabs.

System tabs include:

- A 'Front Sheet' containing a disclaimer, instructions and contents;

- A checks dashboard containing a summary of checks by tab.

KEY FEATURES

Other key features of this tool include the following:

- The model follows good practice financial modelling guidelines and includes instructions, line item explanations, checks and input validations;

- The model allows for a maximum of 15 lease agreements (this can be extended if required).

- The model allows the inclusion of extension, termination and purchase options with drop down to select probability option will be exercised;

- The model includes 5 different cash flow types for each lease agreement including: initial direct costs, fixed lease payments, variable lease payments, exercise price of purchase option and any other cash flows;

- The model allows for lease agreements with any starting and ending date to be included and summarises lease balance and movement results across a 5 year period as selected by the user;

- Business name, currency, first presentation year and lease assumptions are fully customisable

- The model includes a checks dashboard which summarises all the checks included in the various tabs making it easier to identify any errors.

ABOUT PROJECTIFY

We are financial modelling professionals with experience working in big 4 business modelling teams and strong experience supporting businesses with their financial planning and decision support needs. Our aim is to provide robust and easy-to-use models that follow good practice financial modelling guidelines and assist individuals and businesses with key financial planning and analysis processes.

We are keen to make sure our customers are satisfied with the tools / models they purchase and will be more than happy to assist with any questions or support required following or in advance of purchase.

We are also always keen to receive feedback so please do let us know any feedback you have on our models by sending us a message or submitting a review.

This Best Practice includes

1 Blank Excel Model and 1 Excel Model with Populated Example

Further information

Calculation and visualisation of accounting movements and balances for a number of lease agreements from a lessee perspective