Originally published: 17/07/2026 12:49

Publication number: ELQ-83325-1

View all versions & Certificate

Publication number: ELQ-83325-1

View all versions & Certificate

Accounting / Bookkeeping / Tax Firm Acquisition & SBA Underwriting Financial Model

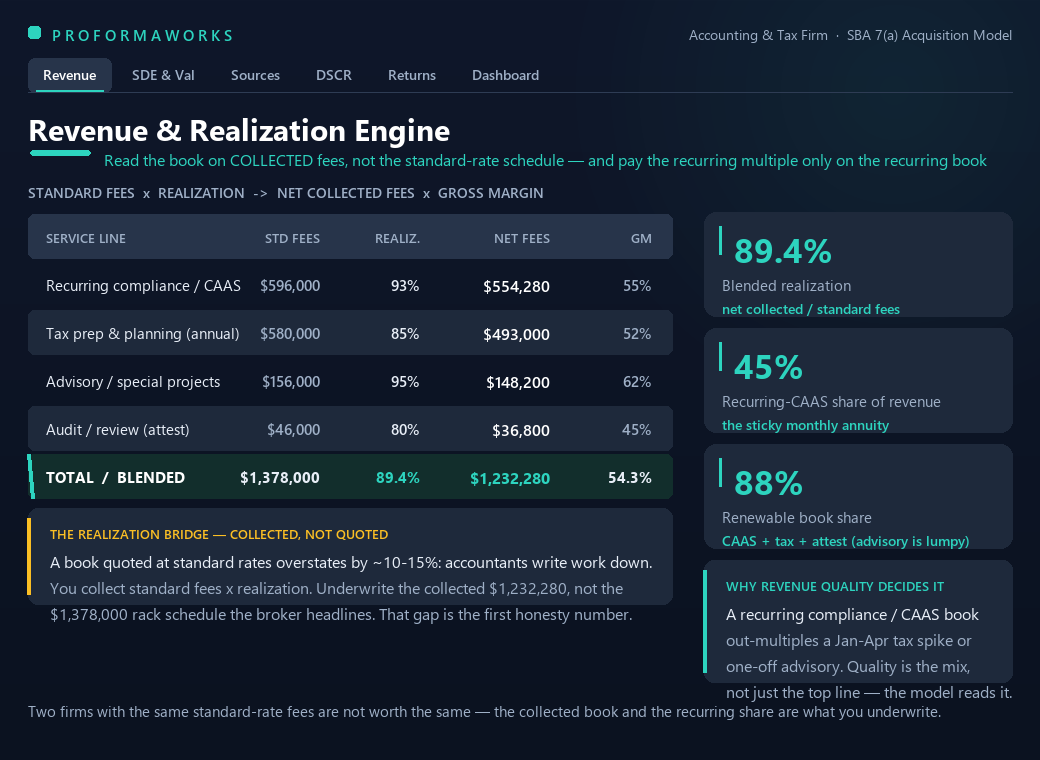

Underwrite an accounting / tax firm acquisition to the SBA lender's number: realization-rate bridge, recurring CAAS vs tax-season, and a true-vs-naive DSCR.

Further information

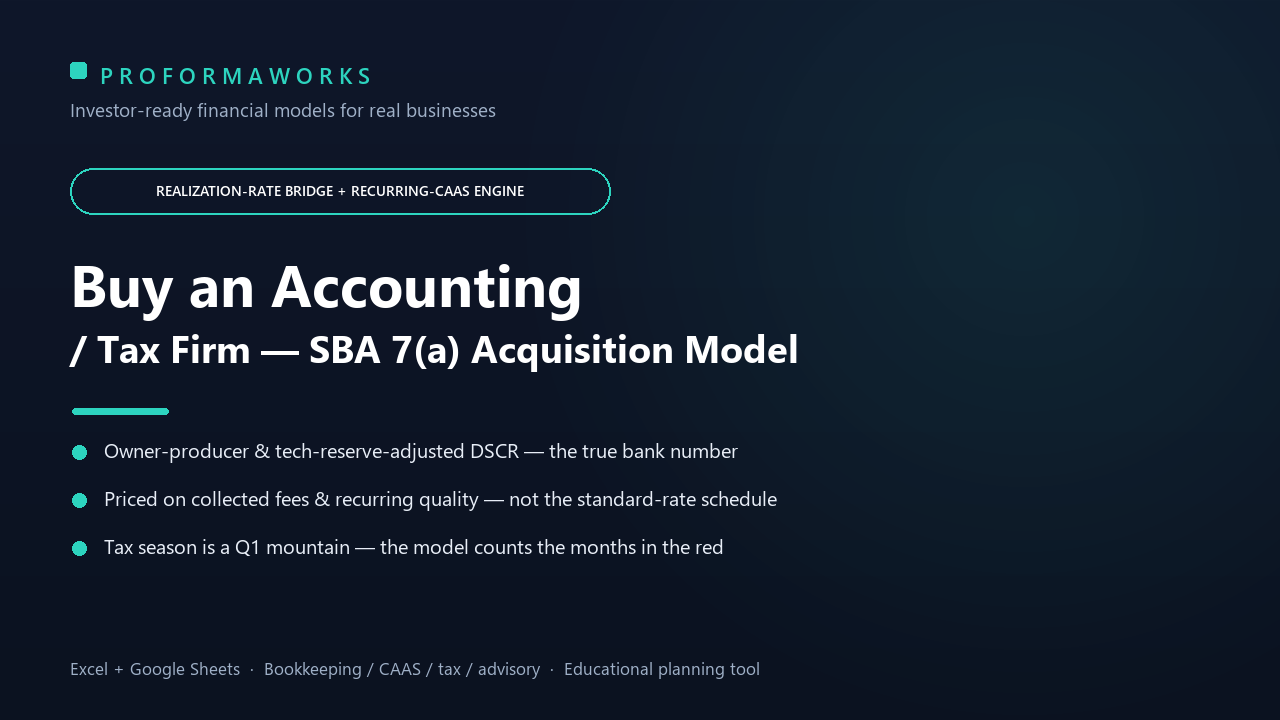

Underwrite an independent accounting / bookkeeping / tax firm acquisition to an SBA lender's standard: read the collected book, price the recurring quality, and clear the DSCR gate.

You are a searcher / ETA buyer, a first-time owner CPA, or a PE add-on operator evaluating or financing a single accounting / tax / bookkeeping firm.

You need a startup or operating forecast for a firm you already own, or a multi-office roll-up consolidation model.