Originally published: 05/03/2018 13:26

Publication number: ELQ-44540-1

View all versions & Certificate

Publication number: ELQ-44540-1

View all versions & Certificate

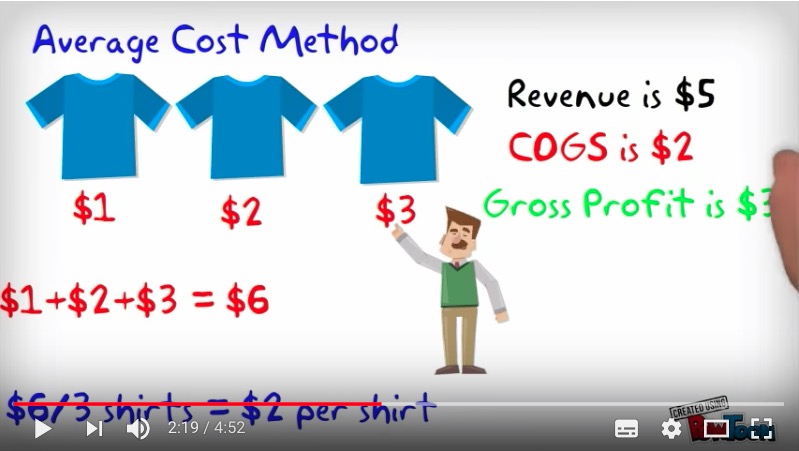

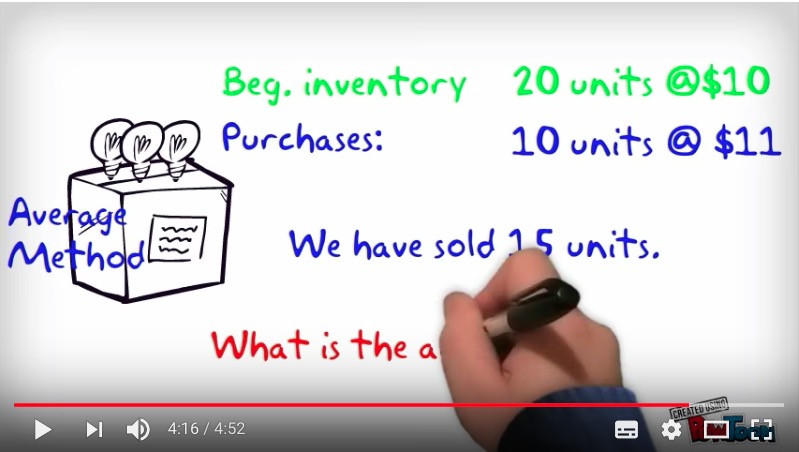

Inventory Management Assumptions - FIFO, LIFO and Average Cost Methods

This video demonstrates the different methods of inventory tracking and accounting inventory assumptions.

Add to bookmarks