Originally published: 05/12/2022 10:06

Last version published: 05/01/2024 08:53

Publication number: ELQ-75613-2

View all versions & Certificate

Last version published: 05/01/2024 08:53

Publication number: ELQ-75613-2

View all versions & Certificate

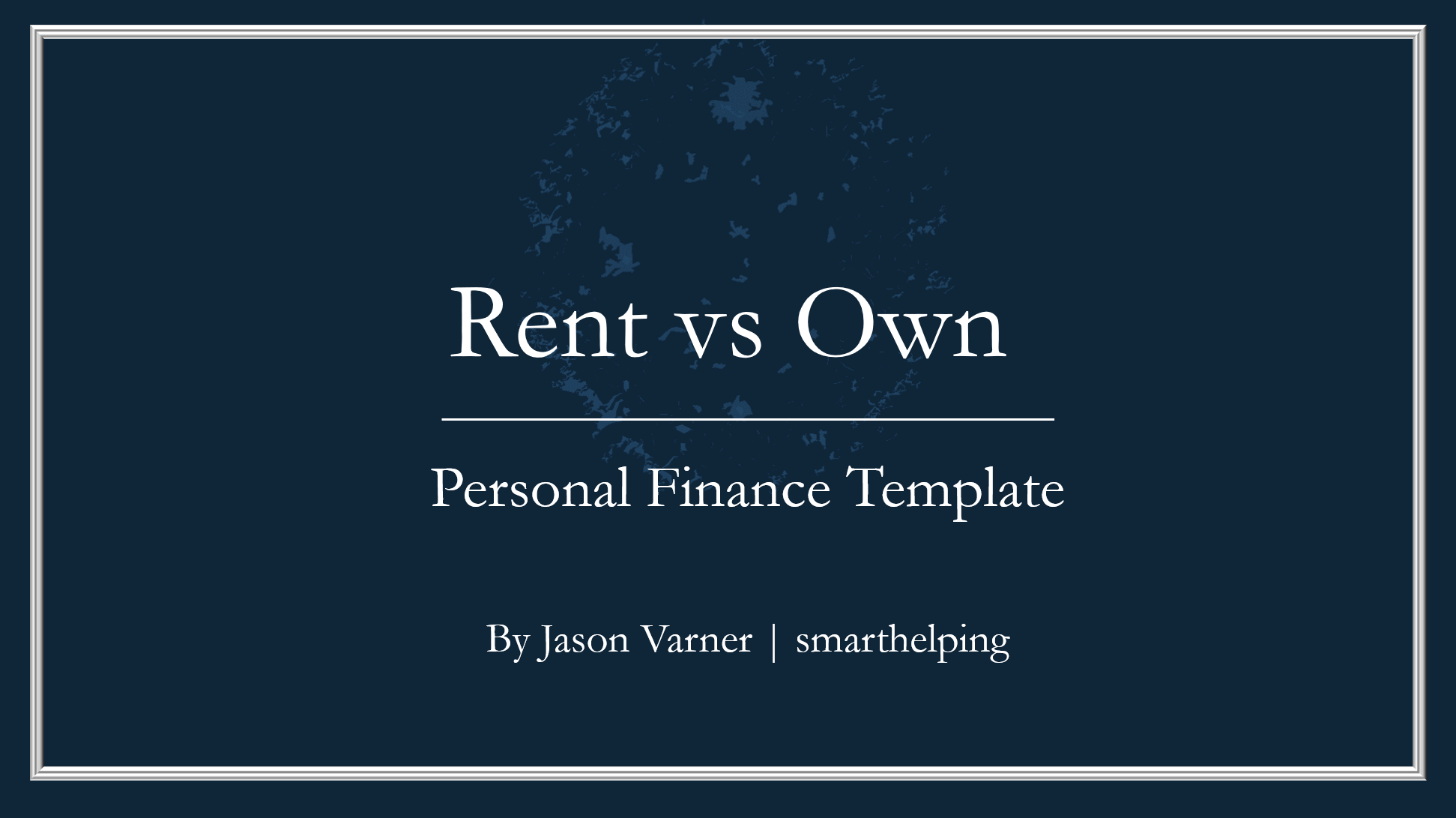

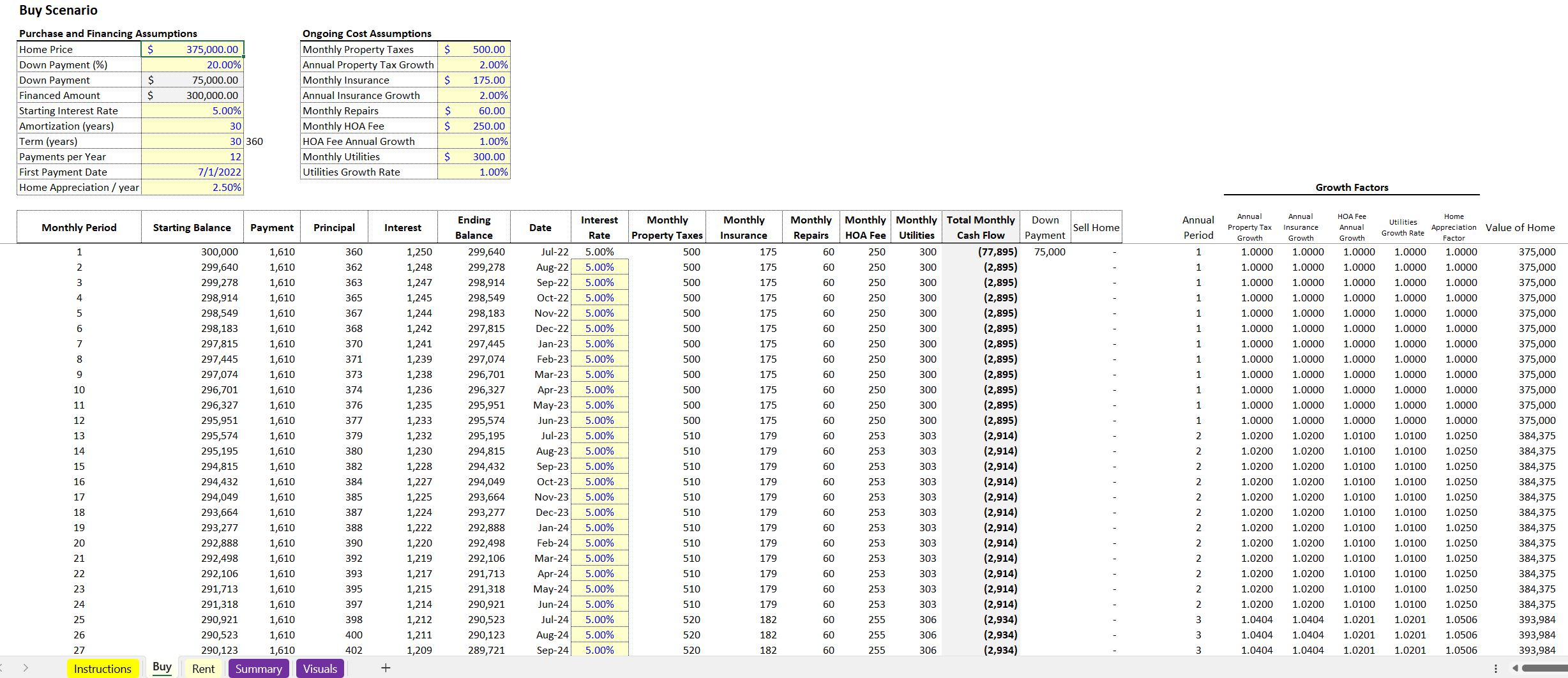

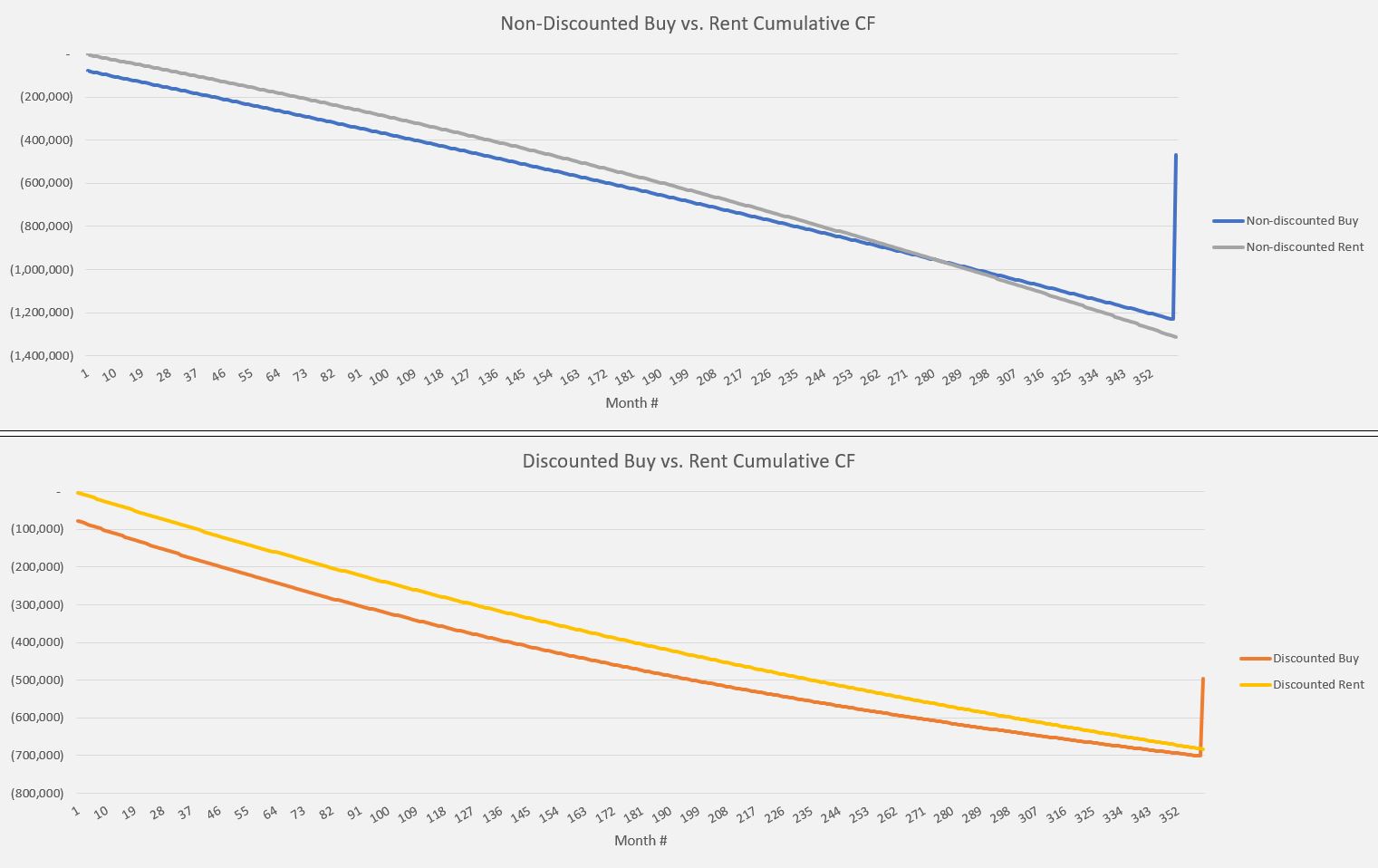

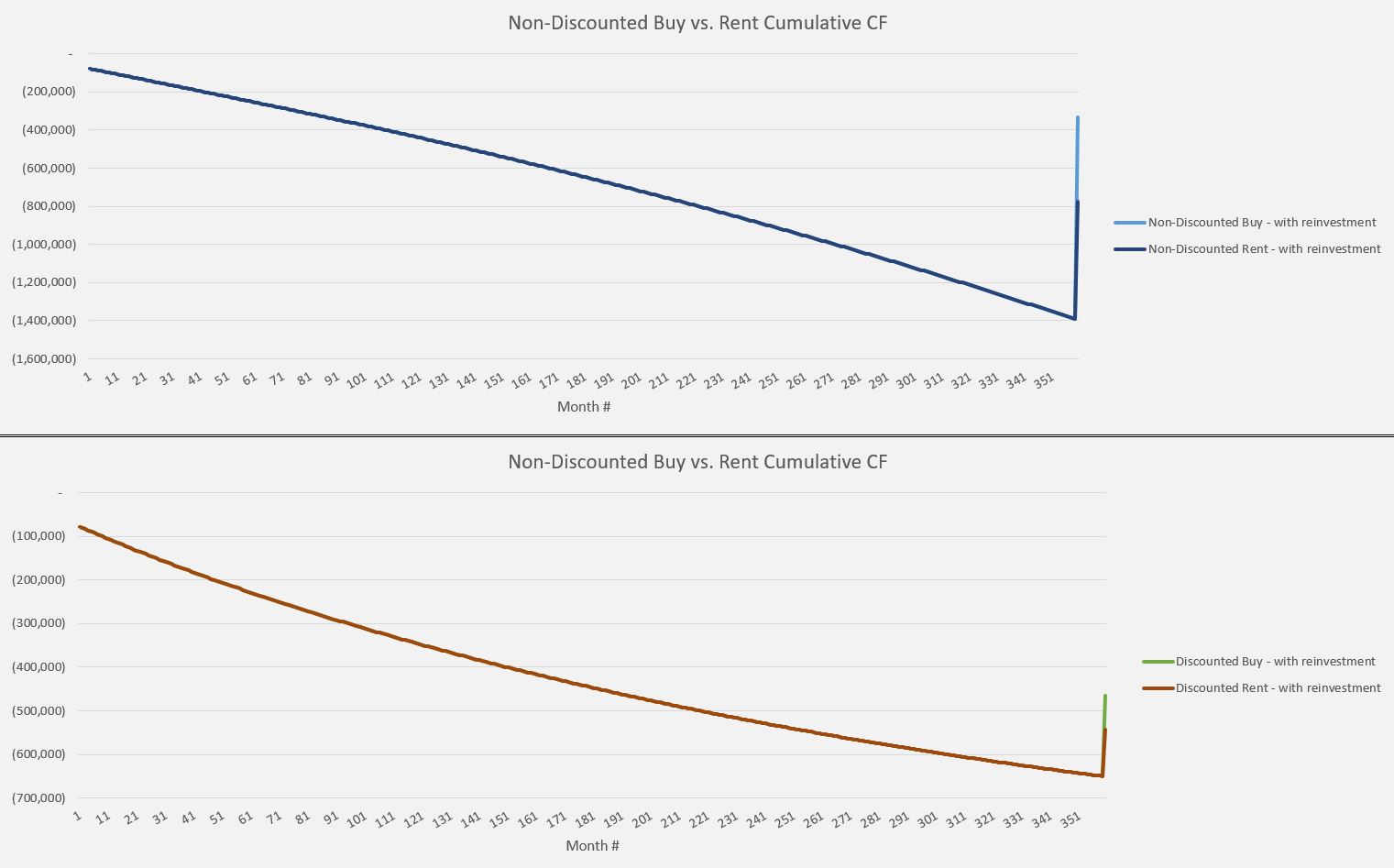

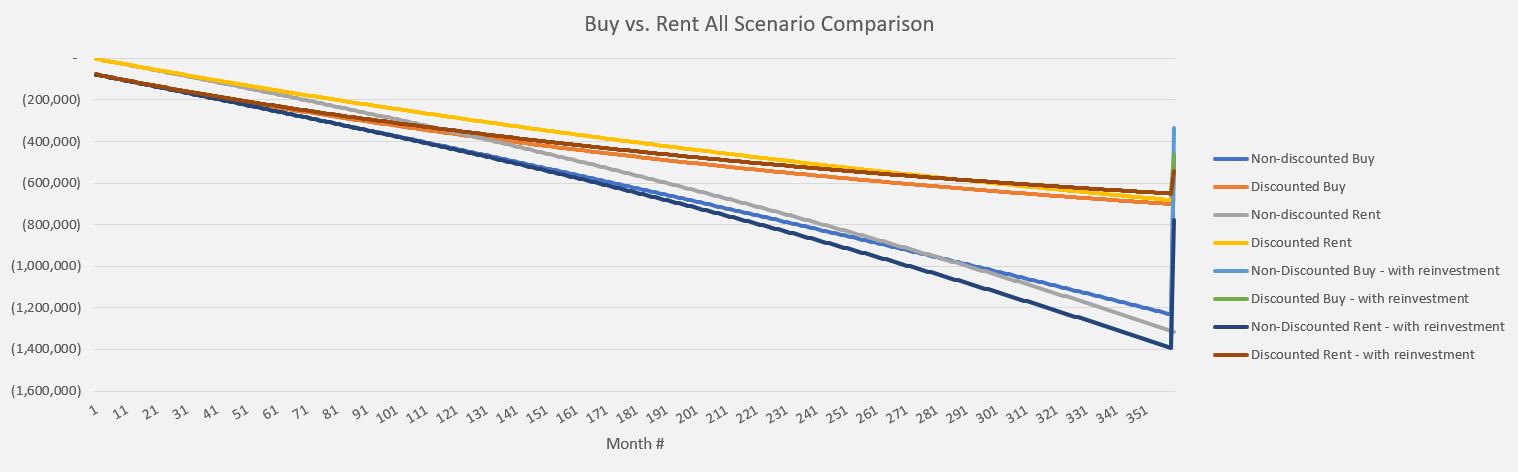

Rent vs Own Calculator

A financial analysis template comparing the present value cost of renting vs. owning a home (or any capital asset).

Further information

Display the non-discounted and discounted value of total costs to buy vs. rent

Comparing a capital asset / home purchase with debt vs. renting.