Originally published: 26/11/2024 10:44

Publication number: ELQ-71923-1

View all versions & Certificate

Publication number: ELQ-71923-1

View all versions & Certificate

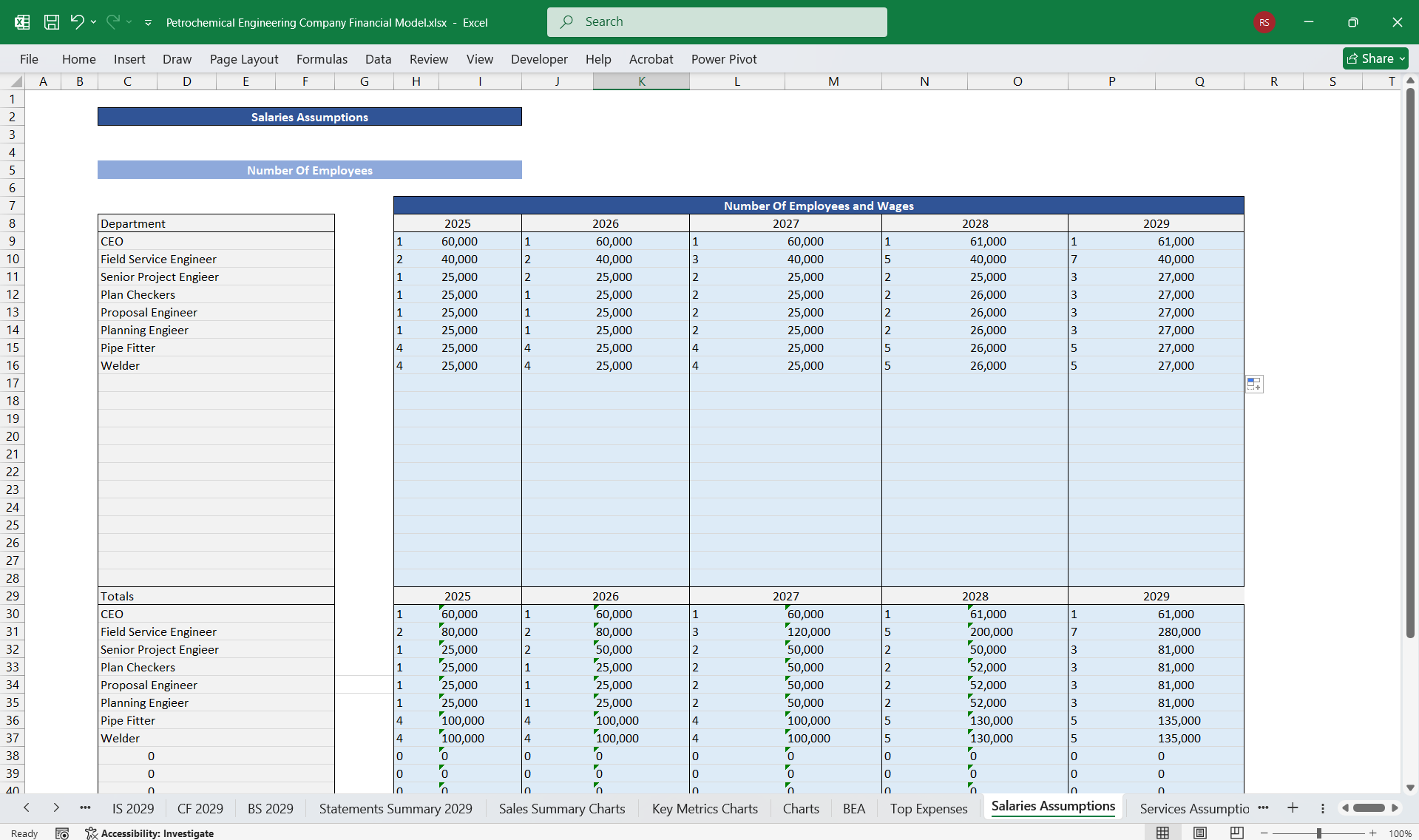

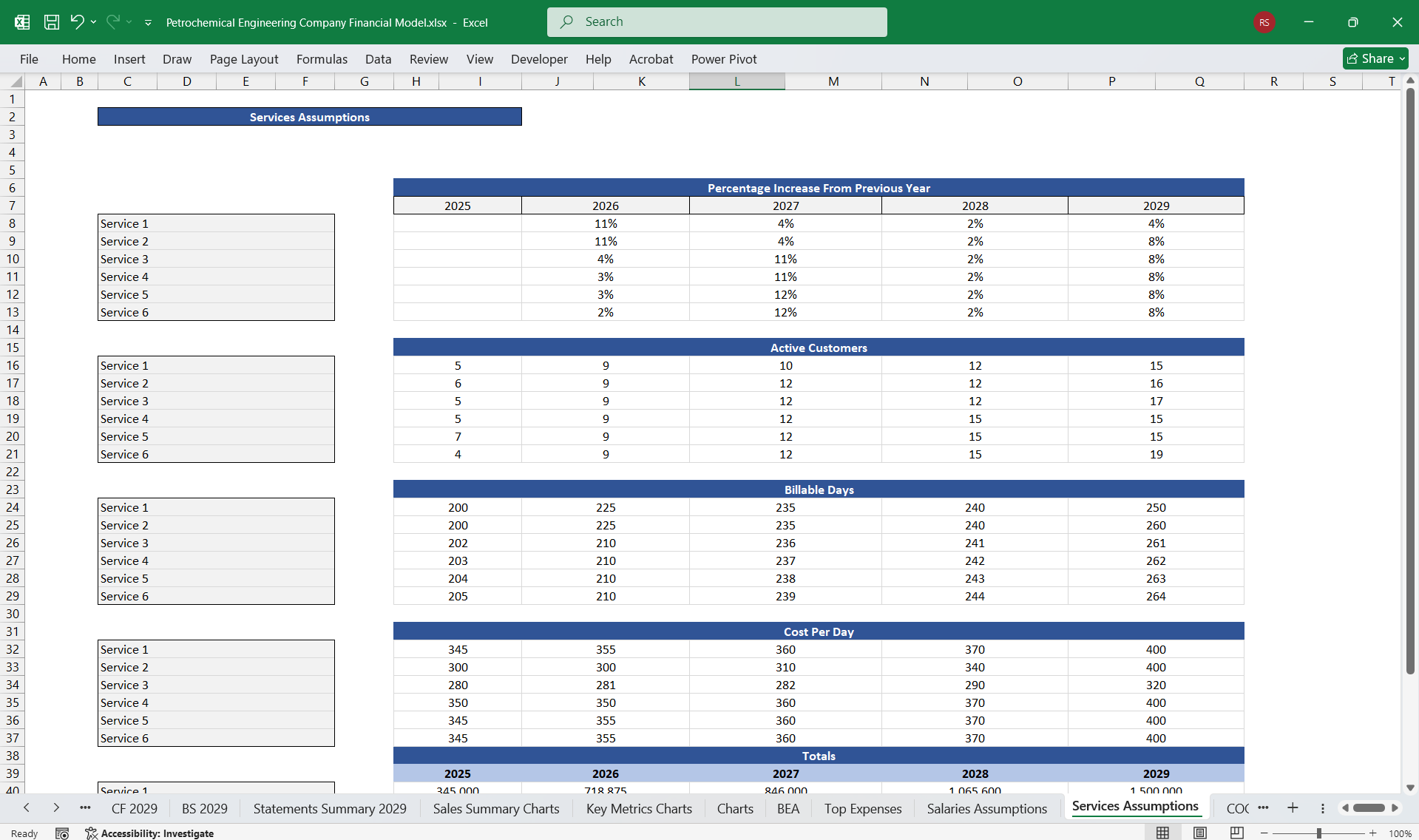

Petrochemical Engineering Company Financial Model

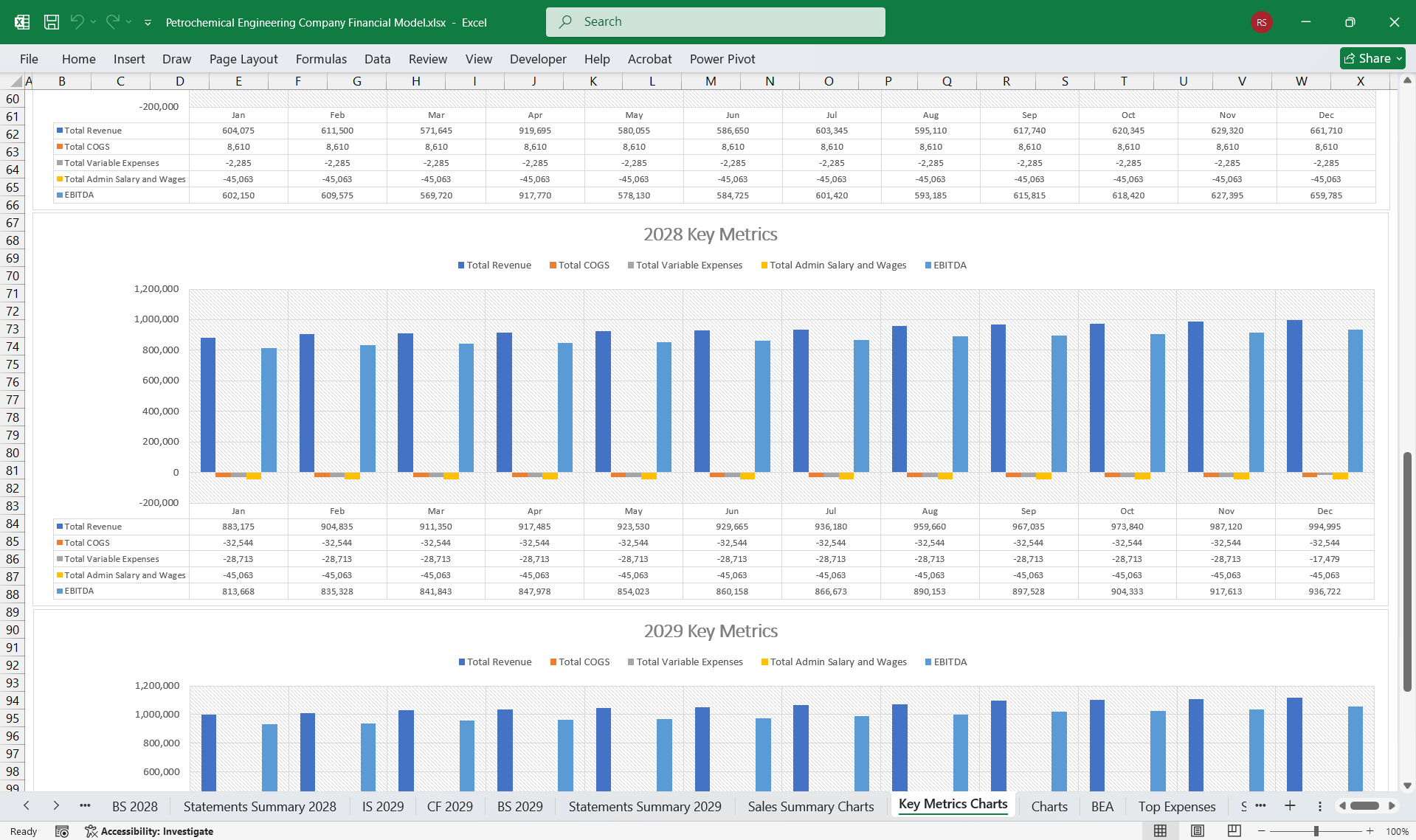

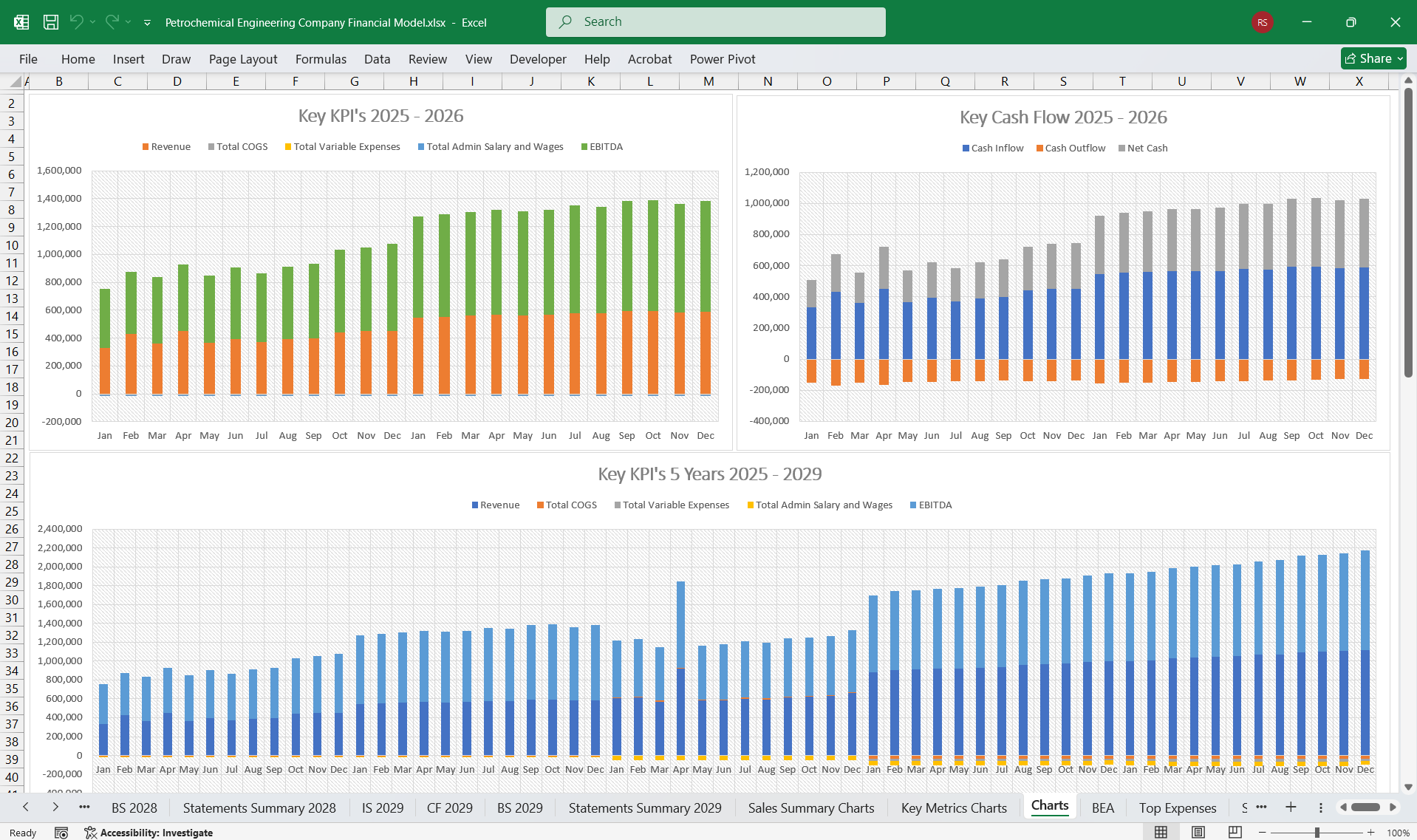

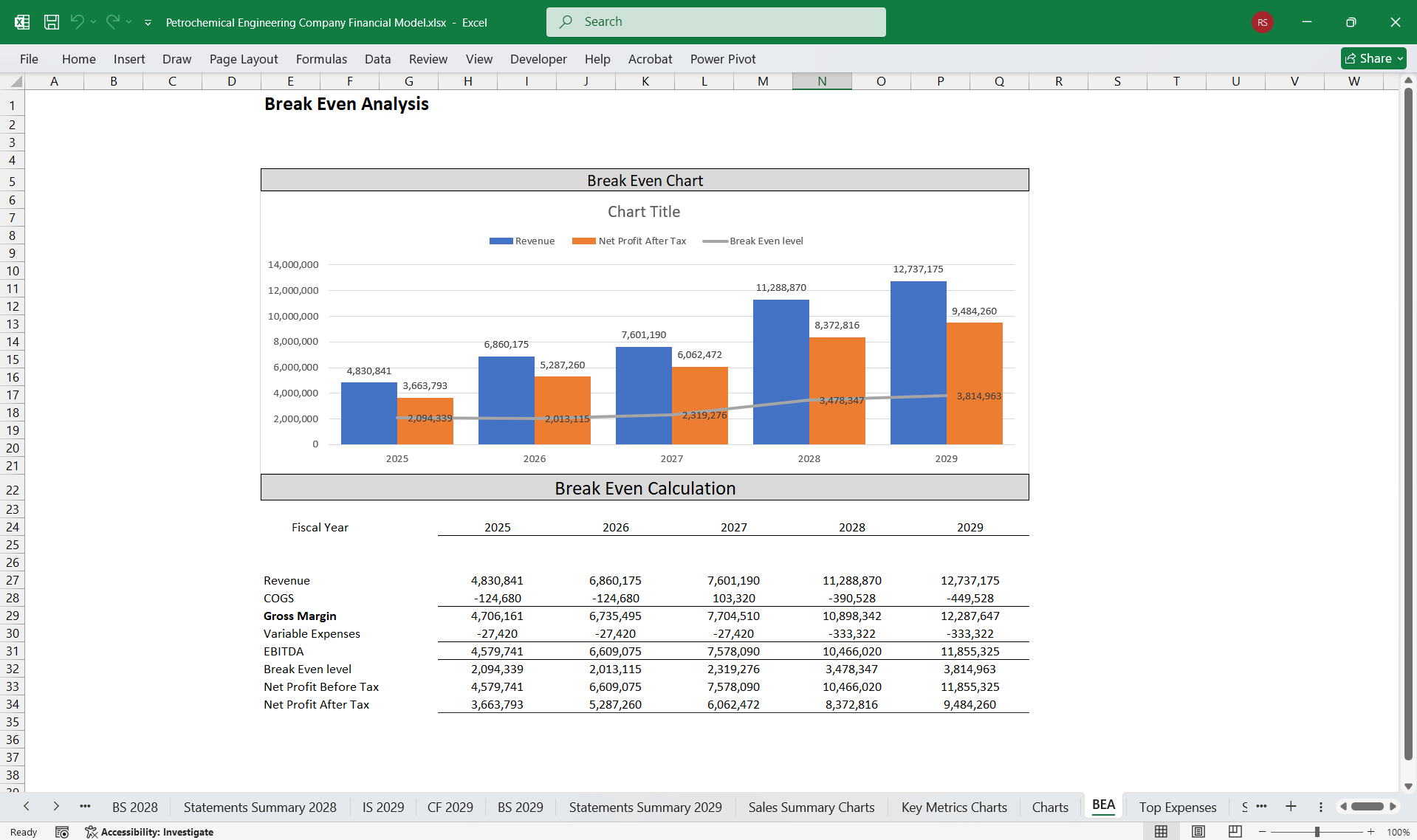

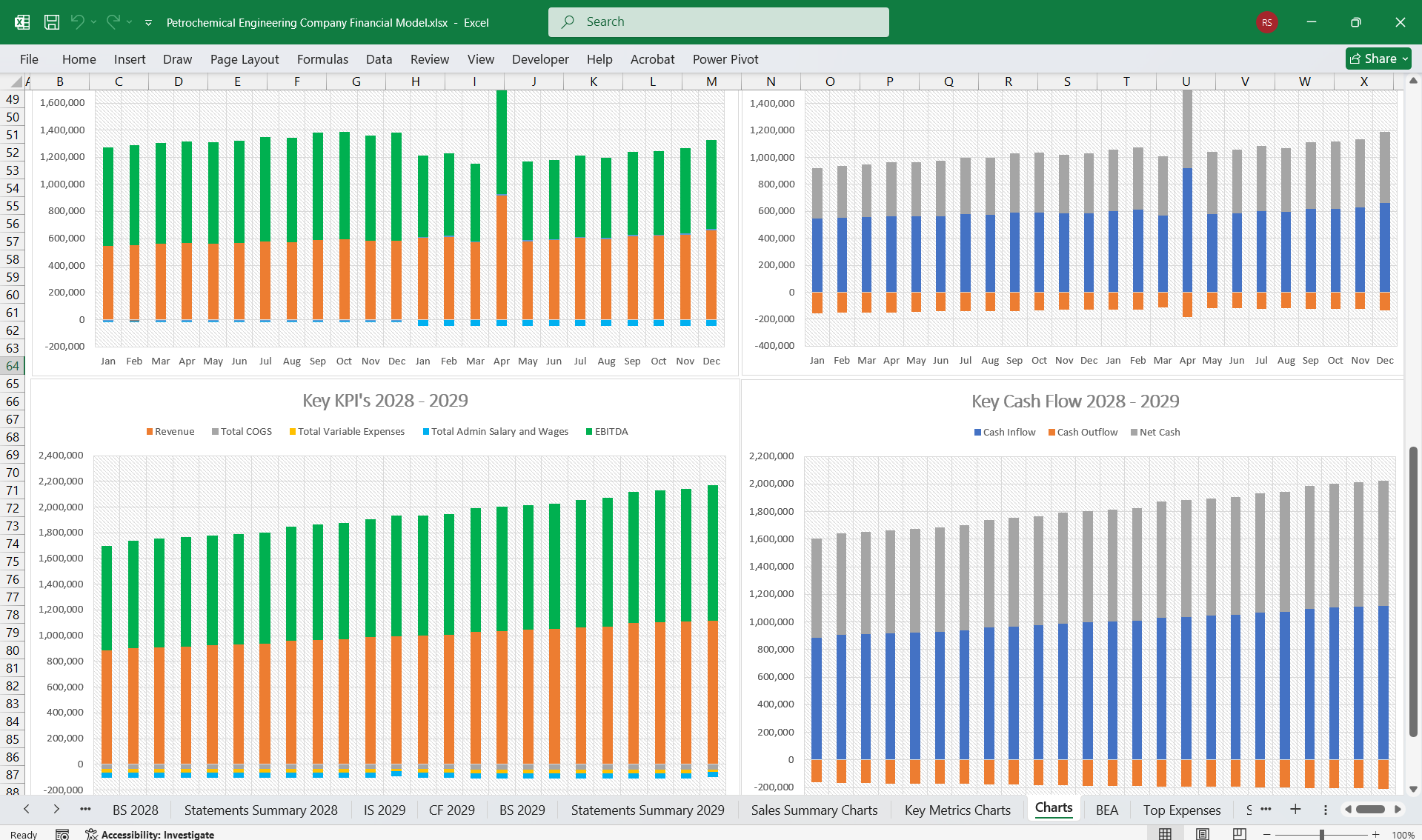

This is a 5-year 3 Statement financial model for a Petrochemical Engineering Company that involves incorporating key elements from its business operations.

AllFinancialModels offer a curated selection of high-quality yet financial model templates designed to support a wide range of business needs.Follow

petrochemical engineeringengineeringfinancial modeloil and gasfinance modelpetrochemicalspetroleum engineeringpetroleum distillateshydrocarbon explorationexcel

Description

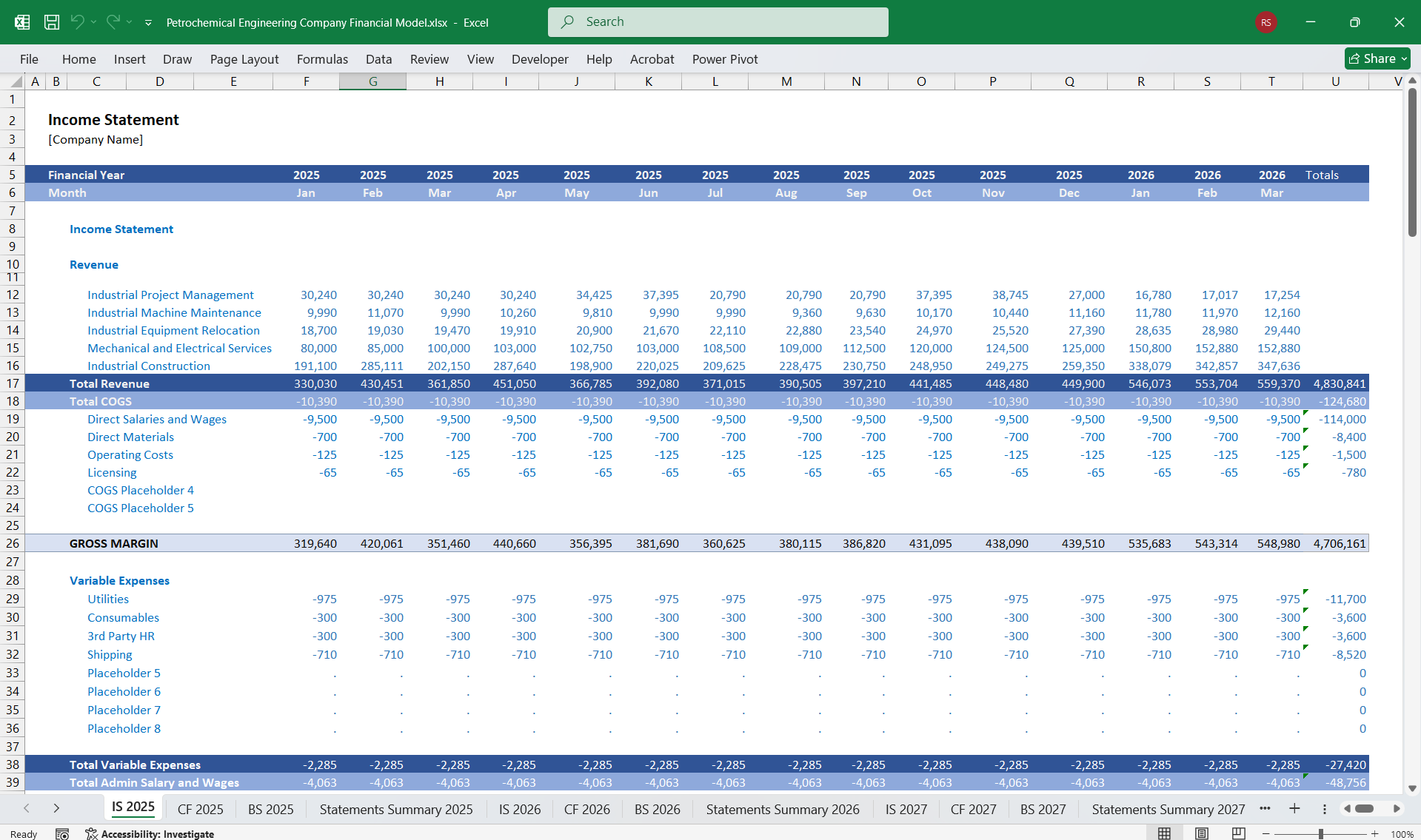

This is a financial model for a Petrochemical Engineering Company that involves incorporating key elements from its business operations, segmented into different services. Below is a detailed structure for the financial model, with considerations for an Income Statement, Cash Flow Statement, and Balance Sheet, along with revenue and expense breakdowns for the specified service areas:

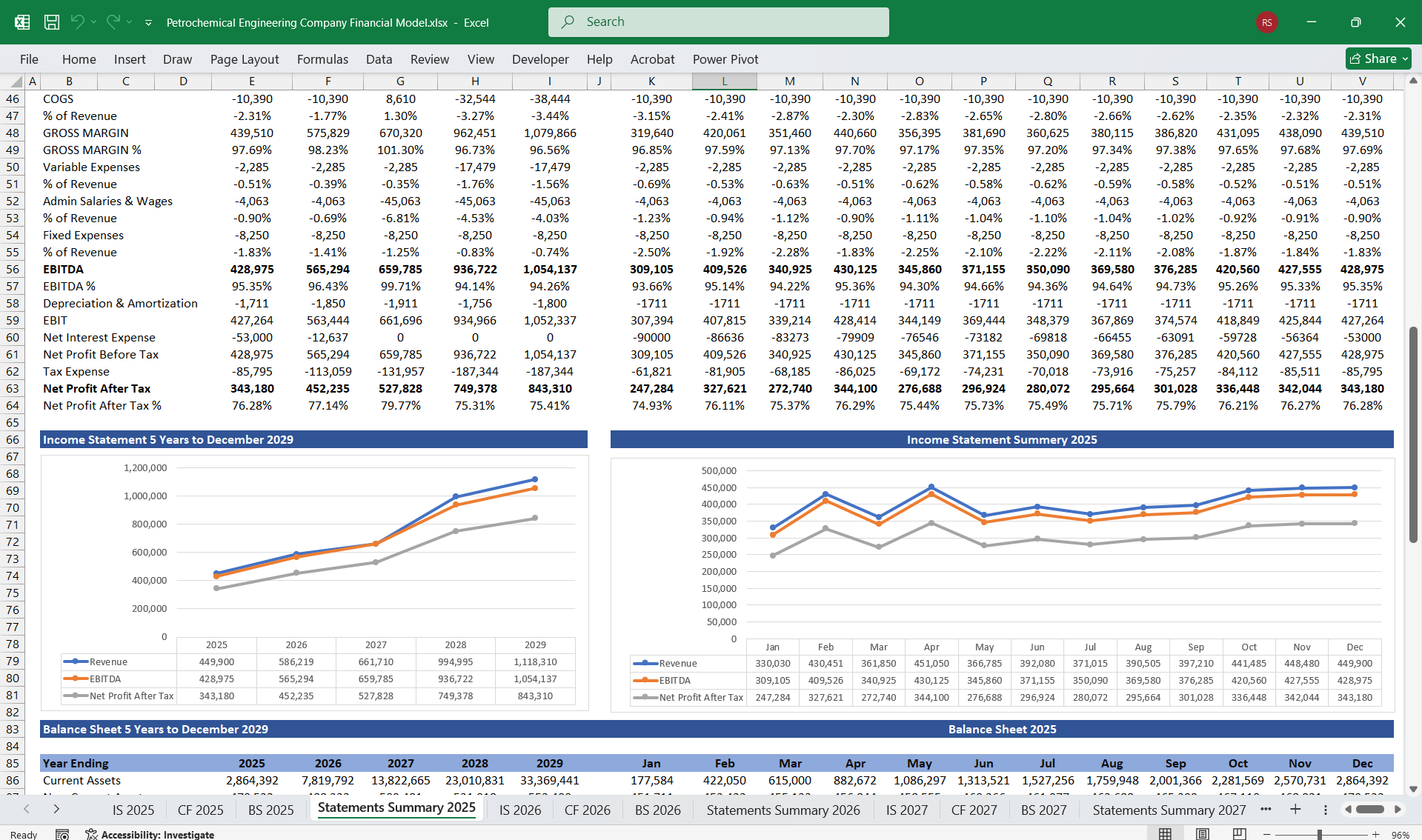

1. Income StatementThe Income Statement captures revenues and expenses to calculate profitability.

Revenue BreakdownInclude income streams from the following services:

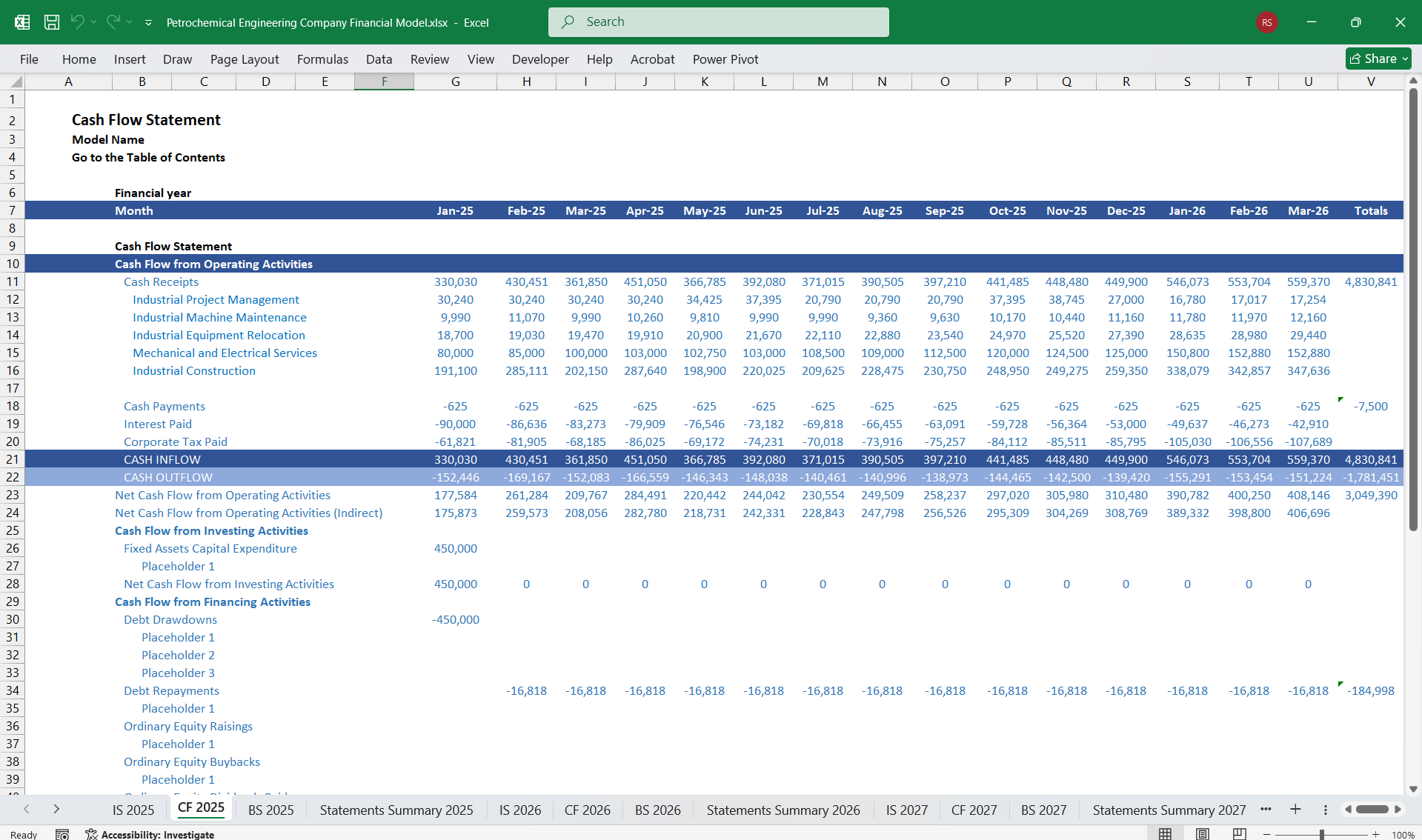

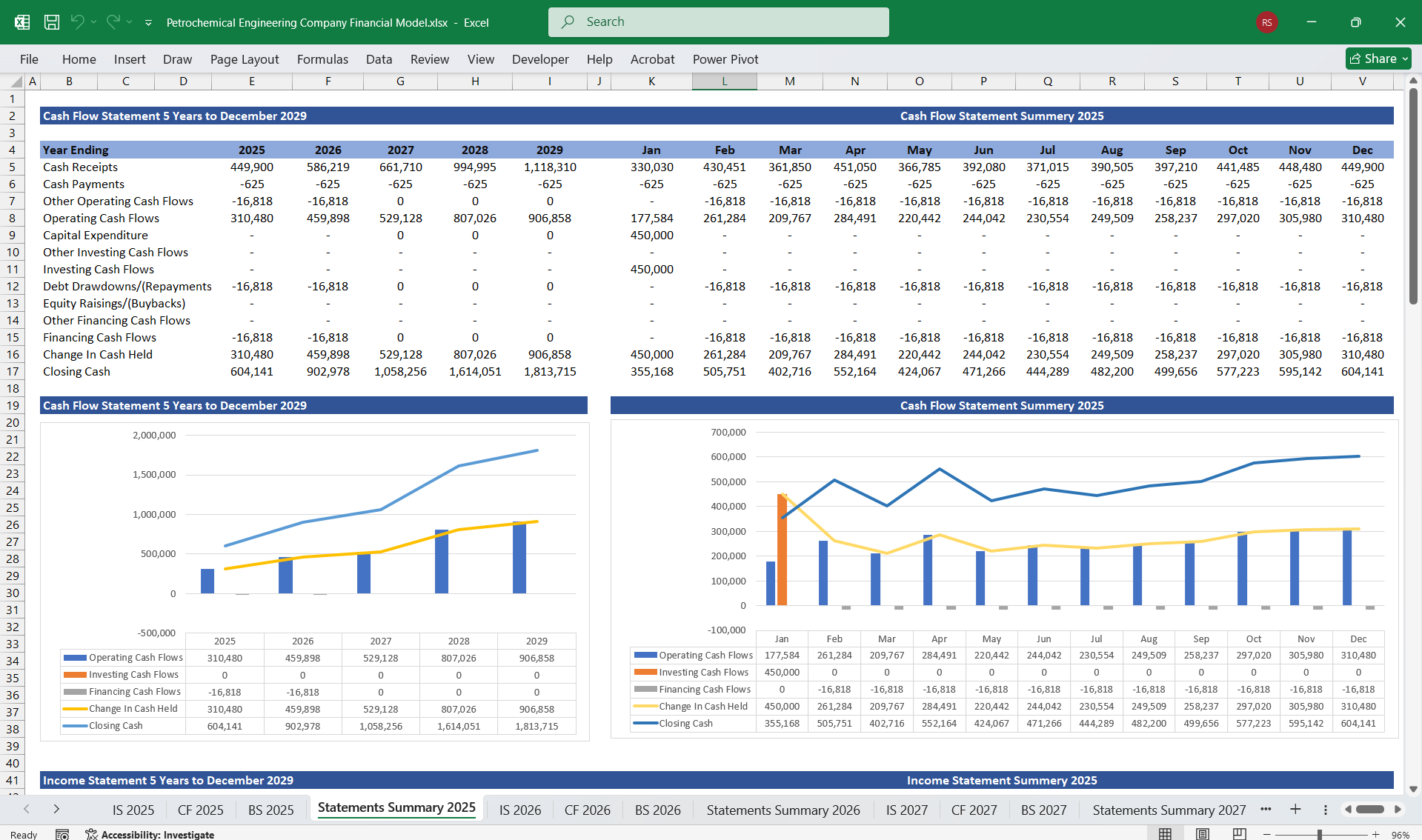

Operating Activities

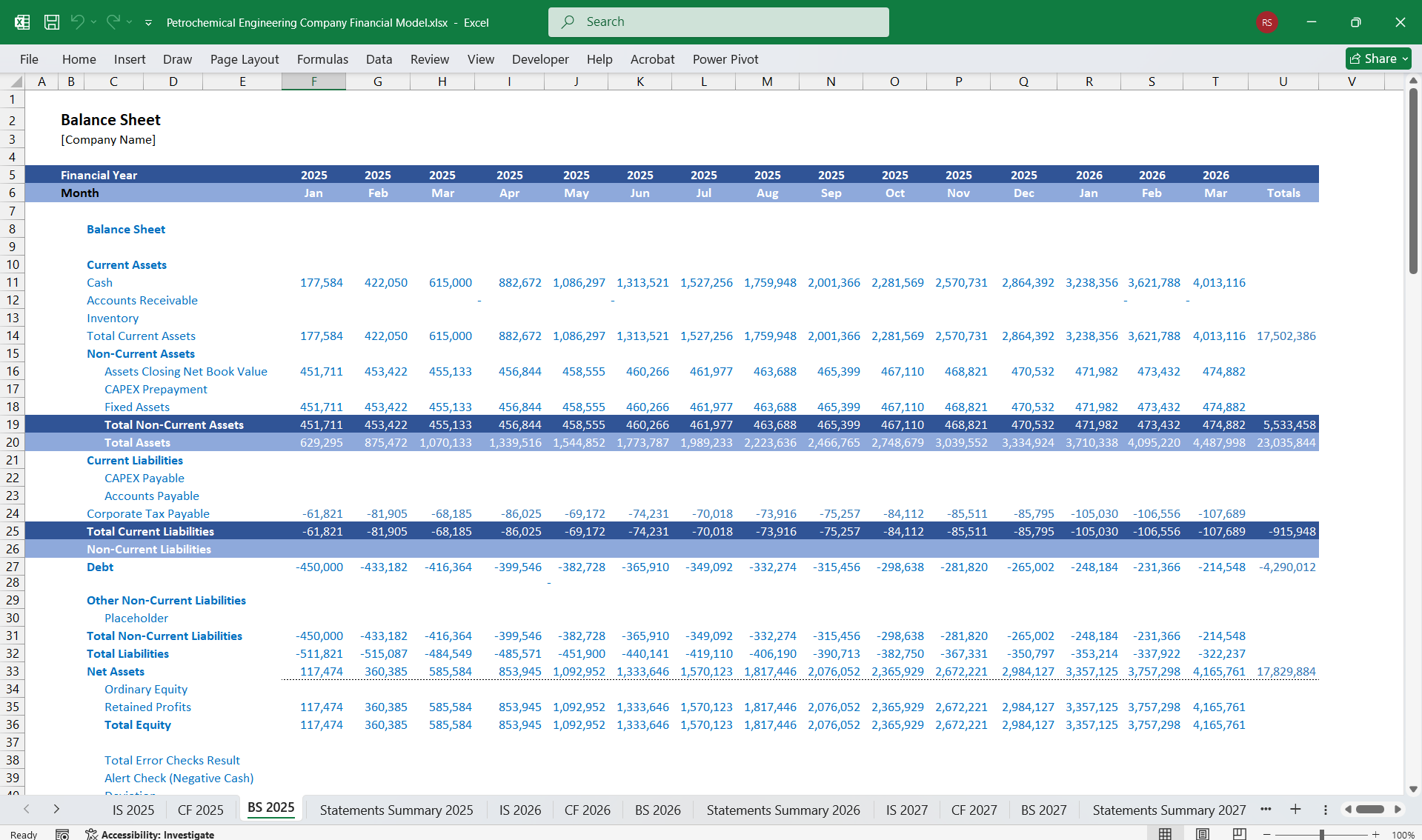

3. Balance SheetThe Balance Sheet provides a snapshot of assets, liabilities, and equity.

Assets

This is a financial model for a Petrochemical Engineering Company that involves incorporating key elements from its business operations, segmented into different services. Below is a detailed structure for the financial model, with considerations for an Income Statement, Cash Flow Statement, and Balance Sheet, along with revenue and expense breakdowns for the specified service areas:

1. Income StatementThe Income Statement captures revenues and expenses to calculate profitability.

Revenue BreakdownInclude income streams from the following services:

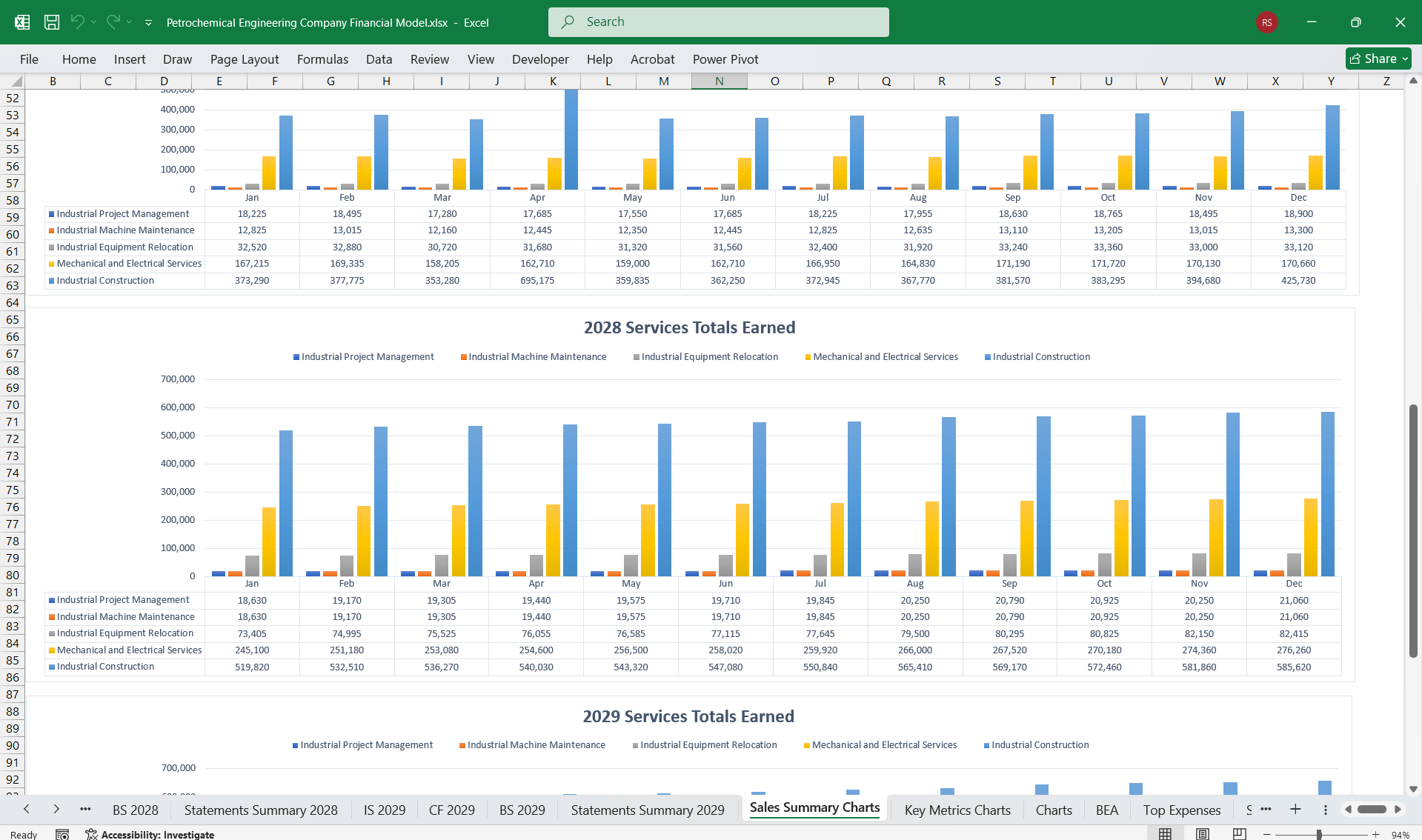

- Industrial Project Management:

- Revenue from consulting, planning, and oversight of projects.

- Potential for recurring revenue if long-term contracts exist.

- Industrial Machine Maintenance:

- Service charges for regular maintenance contracts.

- Emergency maintenance or repairs at higher margins.

- Industrial Equipment Relocation:

- Income from logistical operations for moving equipment between facilities.

- Specialized fees for handling hazardous or oversized equipment.

- Mechanical and Electrical Services:

- Revenue from electrical installations, mechanical repairs, and upgrades.

- Industrial Construction:

- Contractual income from design-build projects.

- Progress payments on large-scale industrial builds.

- Cost of Goods Sold (COGS):

- Labor costs (engineers, technicians).

- Equipment, materials, and supplies for projects and maintenance.

- Subcontractor costs for specific tasks.

- Operating Expenses:

- Administrative overhead.

- Marketing and sales efforts.

- Employee training and development.

- R&D for better tools and technologies.

- Depreciation/Amortization:

- Depreciation of machinery and vehicles used in relocation and construction.

- Amortization of intellectual property or software licenses.

- Taxes and Interest:

- Tax obligations.

- Interest on business loans or equipment financing.

- Gross Profit.

- Operating Profit (EBIT).

- Net Profit.

Operating Activities

- Cash Inflows:

- Payments received from clients for project milestones, maintenance contracts, and equipment relocation jobs.

- Cash Outflows:

- Payments to suppliers, employees, and subcontractors.

- Utility costs and other day-to-day expenses.

- Cash Outflows:

- Capital expenditures on new industrial equipment or facilities.

- Investment in software or technology for operational efficiency.

- Cash Inflows:

- Proceeds from the sale of old equipment or assets.

- Cash Inflows:

- Borrowings for large-scale construction or new machinery purchases.

- Equity injections from investors.

- Cash Outflows:

- Loan repayments.

- Dividends to shareholders.

3. Balance SheetThe Balance Sheet provides a snapshot of assets, liabilities, and equity.

Assets

- Current Assets:

- Cash and cash equivalents.

- Accounts receivable (client payments due for services rendered).

- Inventory of tools, machinery parts, and consumables.

- Non-Current Assets:

- Property, plant, and equipment (PP&E) used in construction, maintenance, and relocation.

- Intangible assets like software systems or licenses.

- Current Liabilities:

- Accounts payable (supplier invoices due).

- Short-term loans or lease obligations.

- Non-Current Liabilities:

- Long-term loans or bonds for equipment and construction.

- Pension liabilities for employees.

- Owner’s equity or retained earnings.

- Share capital if applicable.

- Industrial Project Management:

- Revenue: Based on consulting fees and project oversight percentages.

- Costs: Primarily labor (engineers/project managers) and travel expenses.

- Industrial Machine Maintenance:

- Revenue: Revenue is predictable if tied to recurring contracts.

- Costs: Spare parts, tools, and technical labor.

- Industrial Equipment Relocation:

- Revenue: High margins for complex relocations.

- Costs: Transportation logistics, crane or rig rentals, specialized labor.

- Mechanical and Electrical Services:

- Revenue: Depends on service contracts and installations.

- Costs: Electrical/mechanical components and skilled technicians.

- Industrial Construction:

- Revenue: Milestone-based payments.

- Costs: Materials (steel, concrete), labor, and subcontractor costs.

- Gross Margin by Service Line - Profitability per service.

- Operating Margin - Overall operational efficiency.

- DSO (Days Sales Outstanding) - Efficiency in receivables collection.

- ROA (Return on Assets) - Effectiveness in utilizing assets.

This Best Practice includes

1 Excel Financial Model

Further information

Eliminates the need to create project finance trackers from scratch and includes all common Petrochemical Engineering company actual and projection components.