Originally published: 11/07/2019 07:56

Last version published: 25/04/2025 07:23

Publication number: ELQ-37109-14

View all versions & Certificate

Last version published: 25/04/2025 07:23

Publication number: ELQ-37109-14

View all versions & Certificate

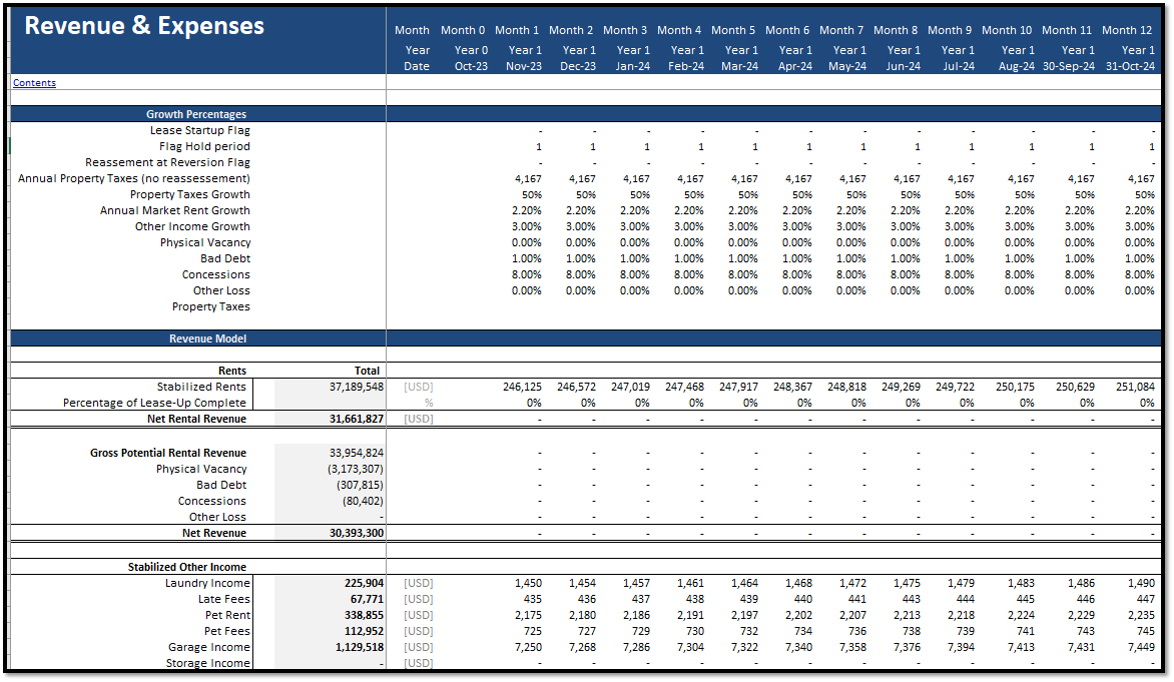

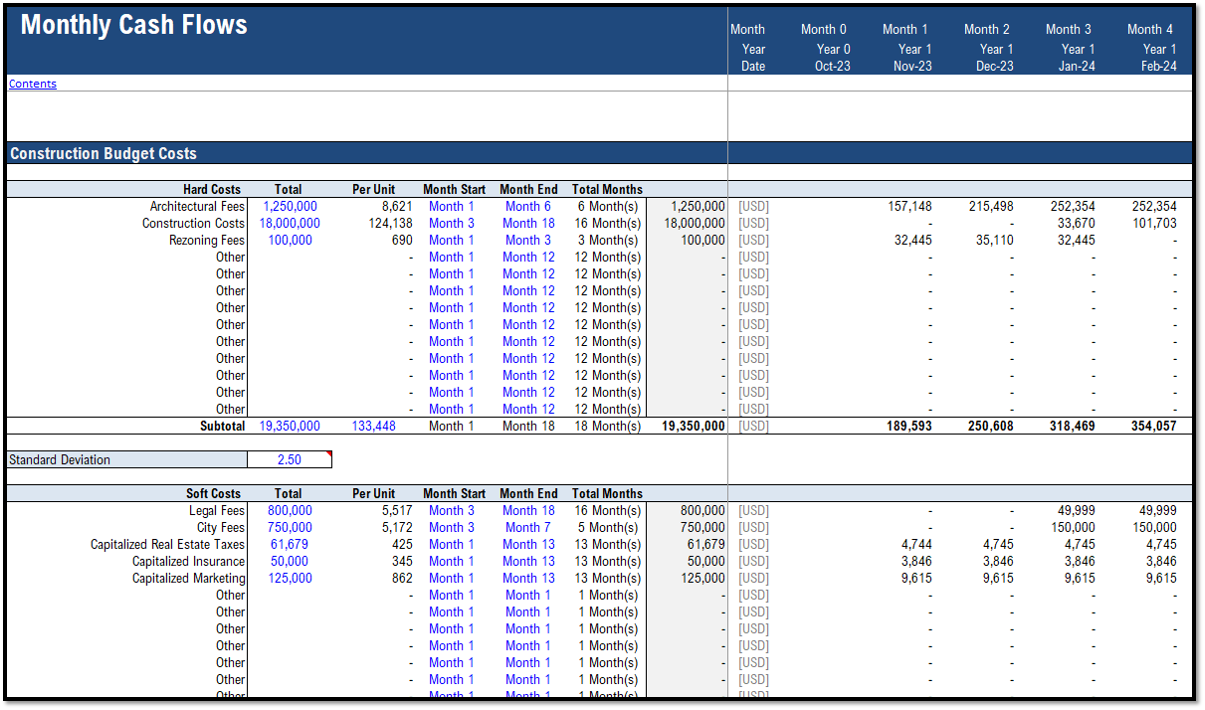

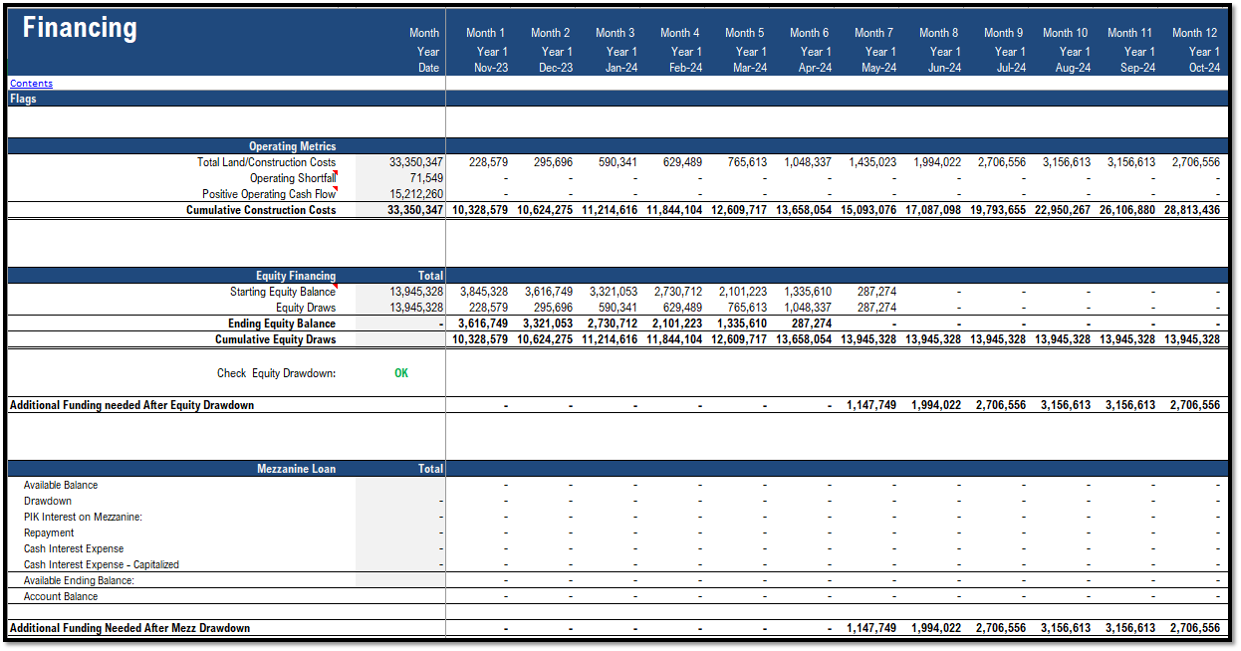

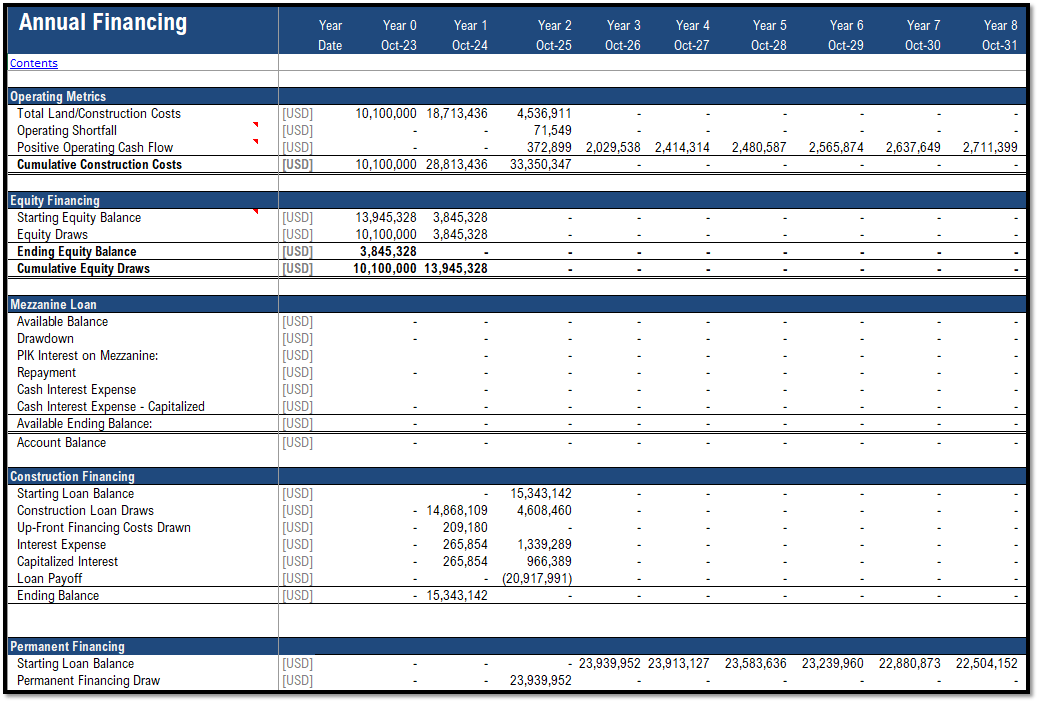

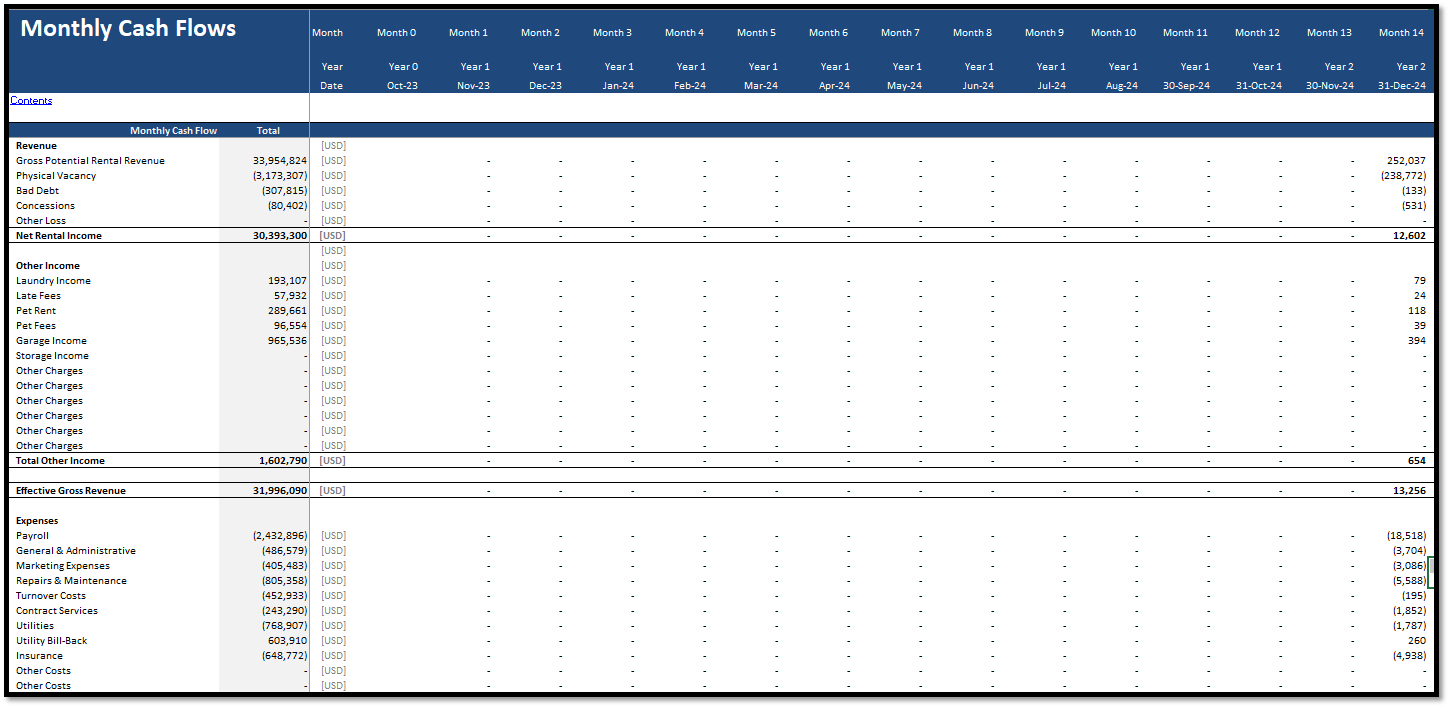

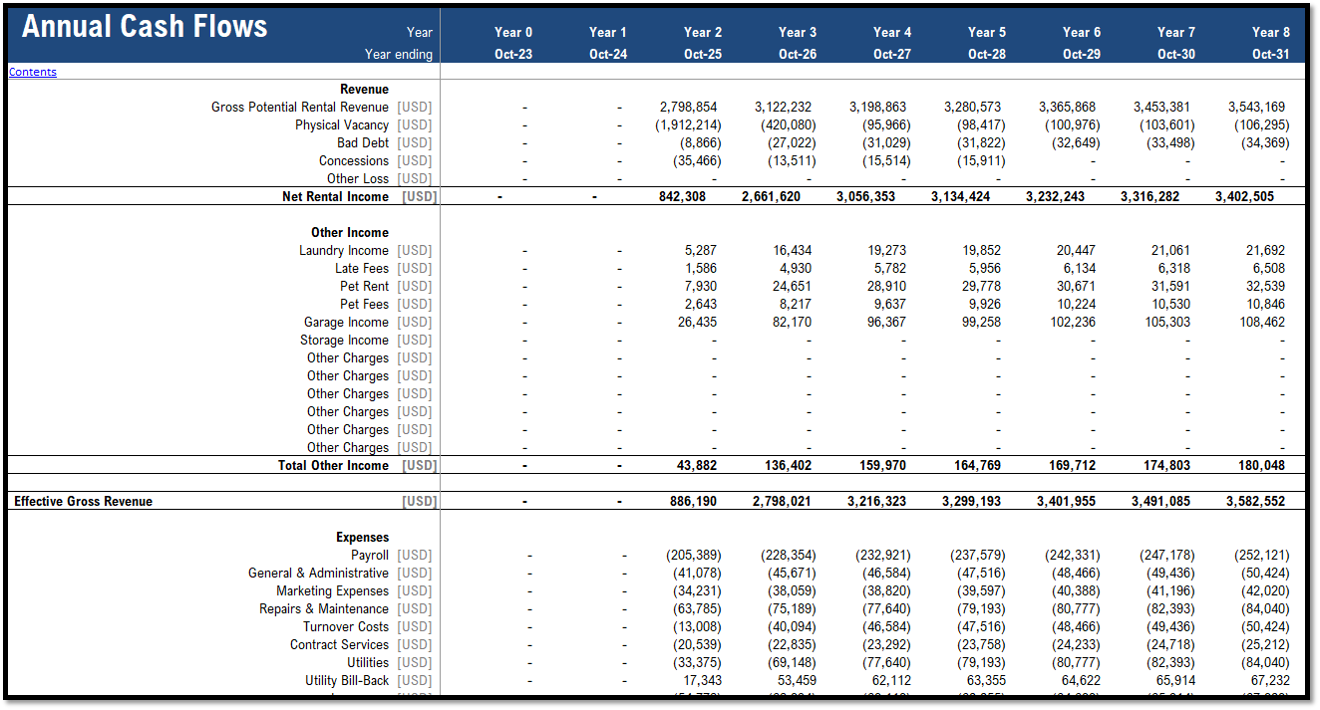

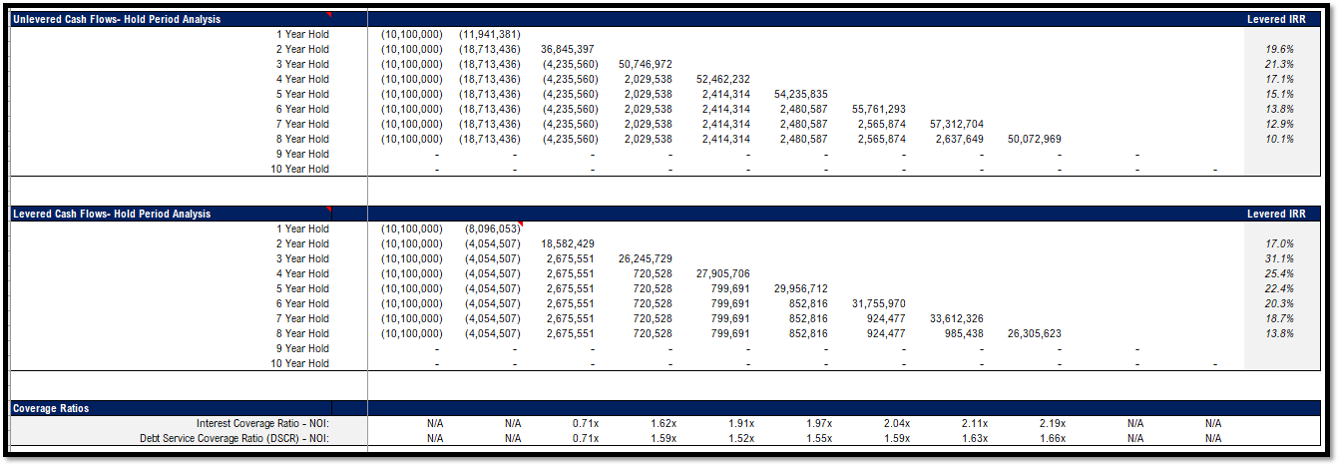

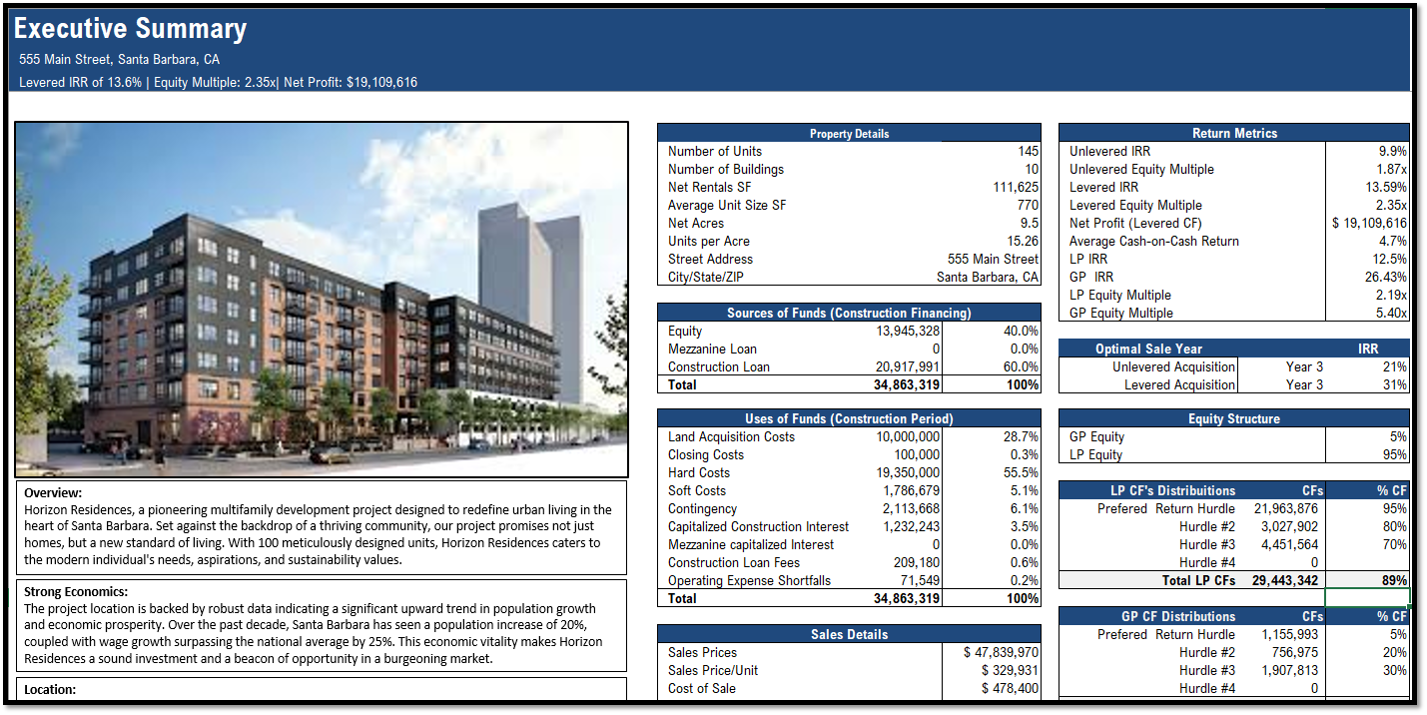

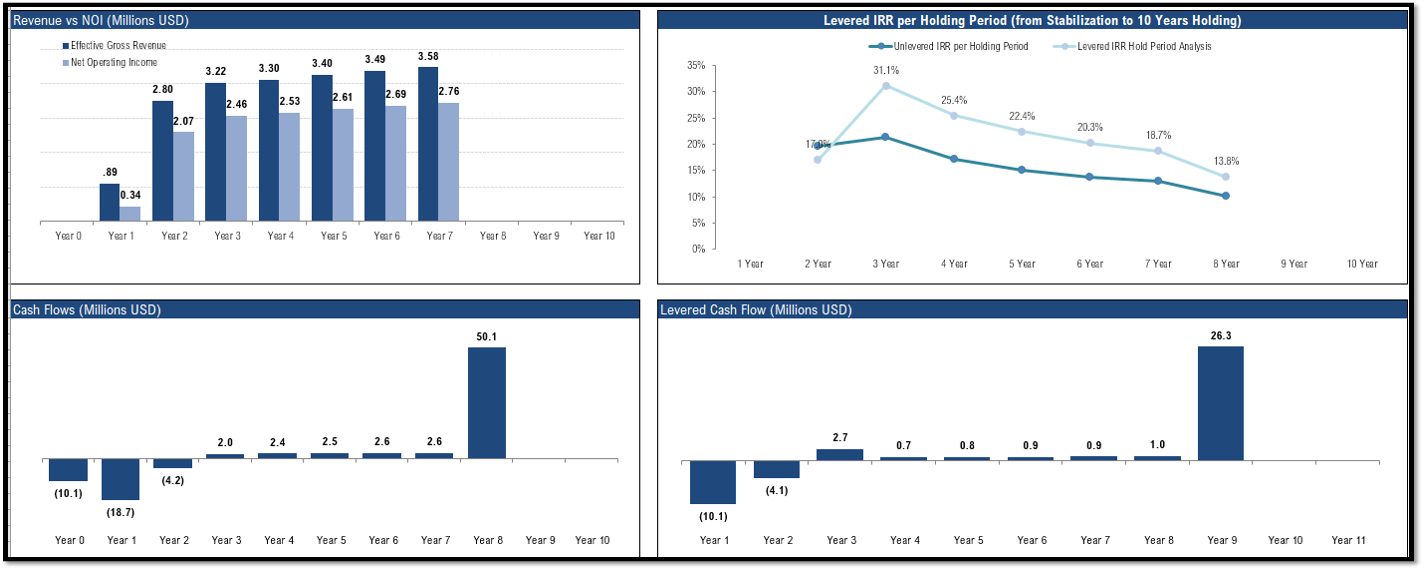

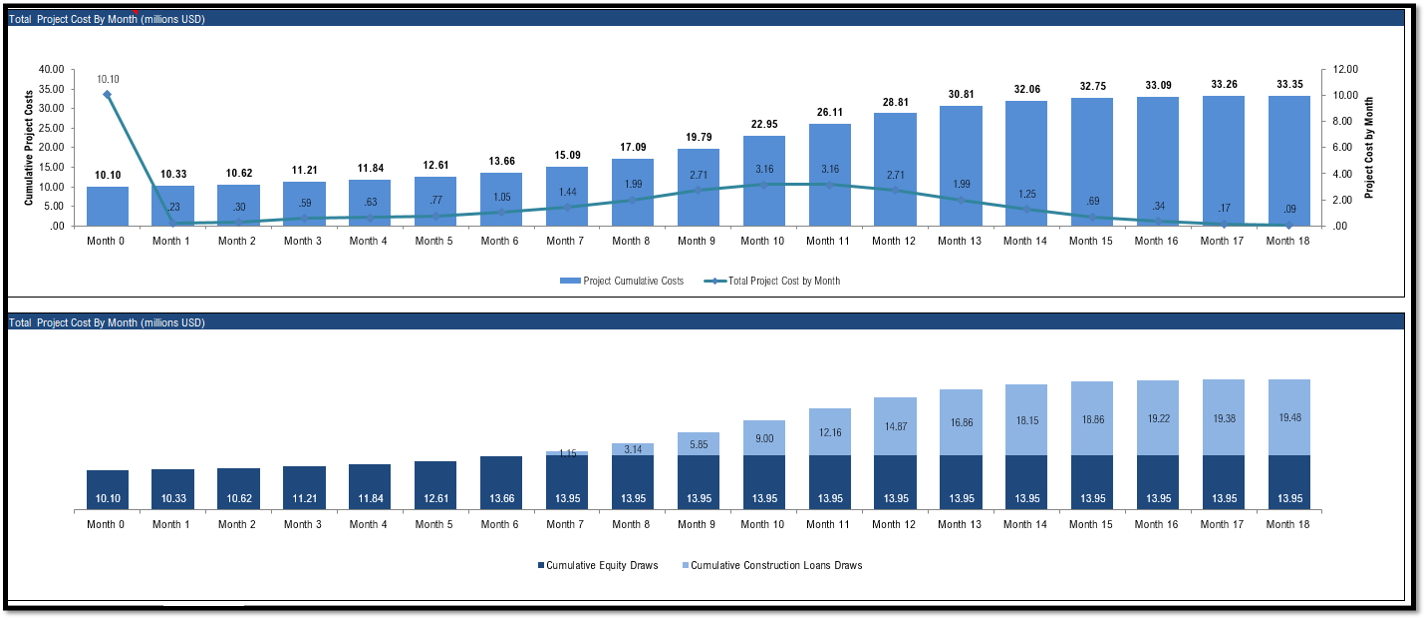

Real Estate Multi Family Development Excel Model

The real estate model provides a comprehensive tool for evaluating multi-family property investments with dynamic cash flow analysis and flexible financing.

Further information

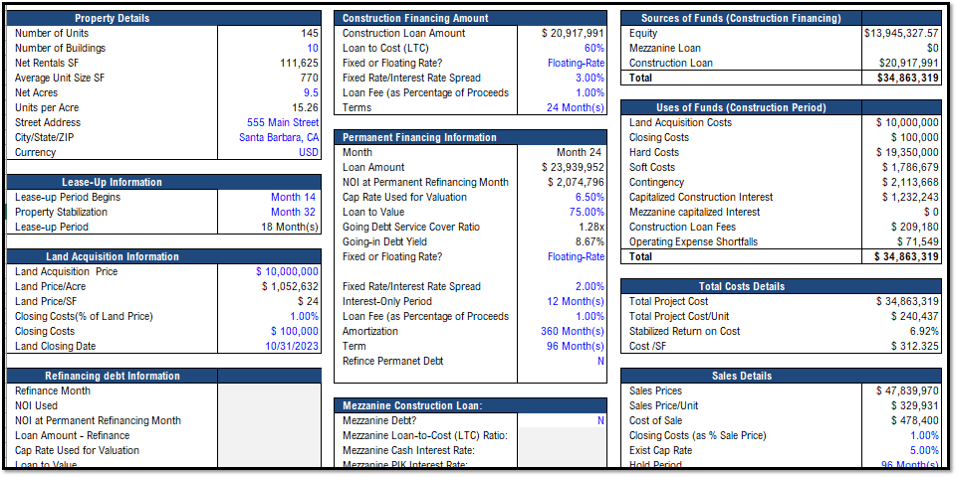

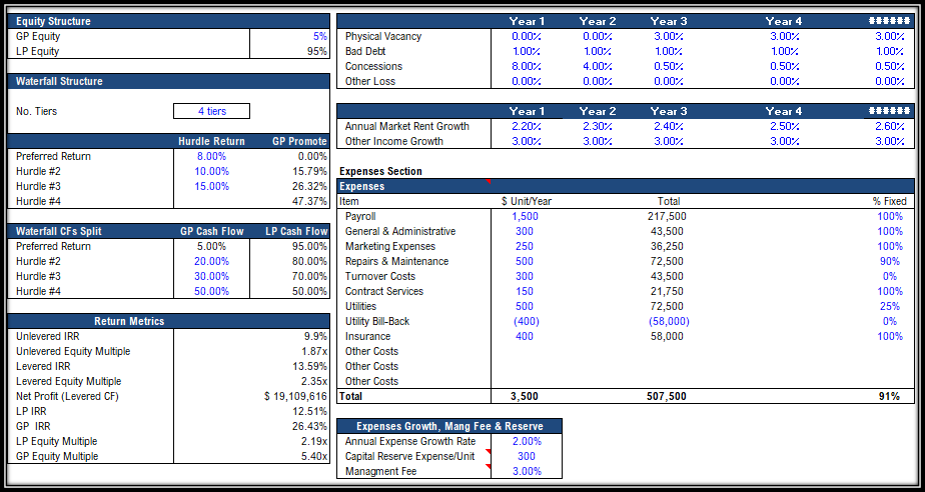

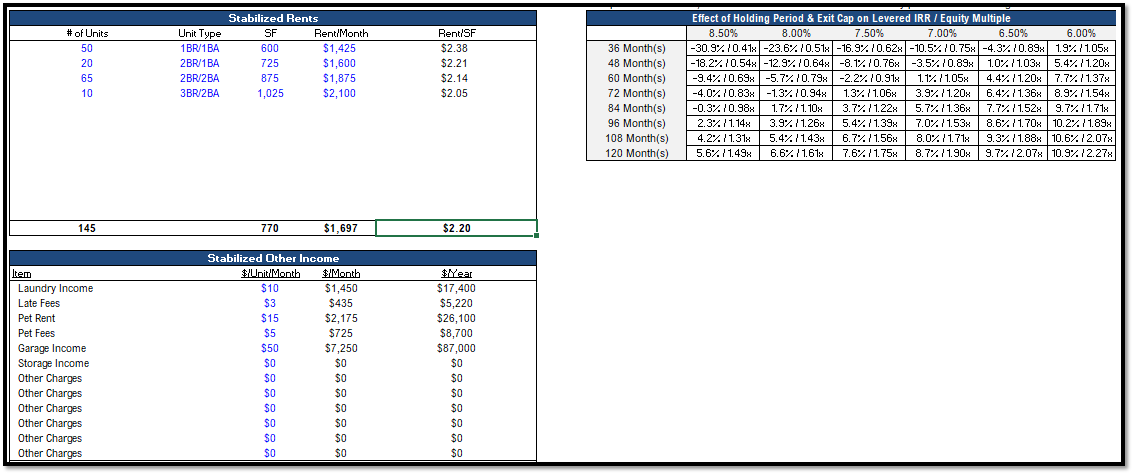

Evaluate the feasibility of a Multi-familiar property development project (with lease-up and selling options) from an investment/investors point of view, taking into account various parameters such as operational, leverage capital expenditures, equity structure, etc..

Real Estate Development of a multi-familiar project, with some slight adaptation, can also be applied to other real estate investments.

Does not work well for non-real estate businesses.